Anti-Venom Market Size, Share & Industry Analysis, By Species (Snake, Scorpion), By Type (Polyvalent, Monovalent), By Mode Of Action (Cytotoxic, Neurotoxic), By End-use (Hospitals, Clinics), and Regional Forecast, 2026-2034

Anti-Venom Market Overview

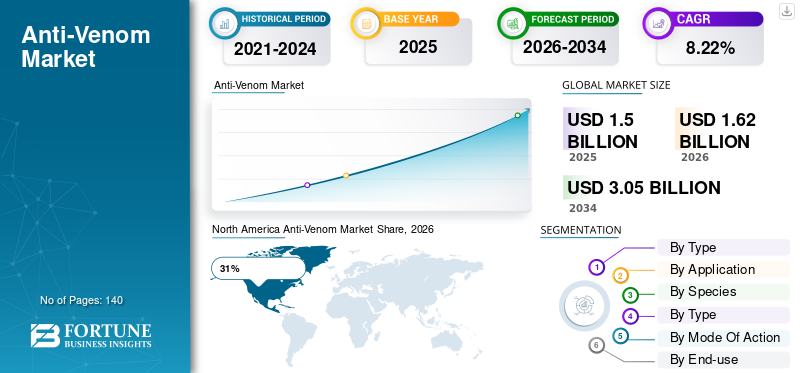

The global anti-venom market size was valued at USD 1.50 billion in 2025. The market is projected to grow from USD 1.62 billion in 2026 to USD 3.05 billion by 2034, exhibiting a CAGR of 8.23% during the forecast period.

The anti-venom market plays a critical role in global emergency healthcare systems due to the rising incidence of venomous snakebites, scorpion stings, and other toxic envenomation cases. The anti-venom market Report highlights increasing demand from hospitals, trauma centers, military healthcare units, and rural medical networks where venomous bites remain a major public health issue. Anti-venom manufacturers are focusing on improved purification technologies, plasma fractionation processes, and species-specific immunoglobulin formulations to increase treatment effectiveness and minimize adverse reactions. Growing awareness regarding rapid envenomation management, expanding government procurement programs, and increasing investments in biotechnology production facilities are strengthening the anti-venom market Size globally. Demand for polyvalent anti-venom products continues to dominate due to their broad-spectrum therapeutic utility.

The United States anti-venom market is witnessing strong demand due to the presence of advanced emergency care infrastructure, increasing awareness regarding venom treatment protocols, and rising encounters with venomous snakes and scorpions in southern states. The Anti-Venom Industry Analysis indicates that the U.S. market benefits from significant research activities related to recombinant anti-venom development and toxin-neutralizing biologics. Hospitals, poison control centers, and trauma units are increasing procurement of high-efficacy anti-venom products to manage severe envenomation cases. Growing partnerships between biotechnology companies and healthcare institutions are also strengthening the anti-venom market Outlook in the United States. Demand is particularly high in regions with rattlesnake and coral snake exposure risks.

Download Free sample to learn more about this report.

Key Takeaways

Market Size & Growth

- Global market size 2025: USD 1.50 billion

- Global market size 2034: USD 3.05 billion

- CAGR (2026–2034): 8.23%

Market Share – Regionals

- North America: 31%

- Europe: 24%

- Asia-Pacific: 34%

- Rest of World: 11%

Country-Level Shares

- Germany: 27% of Europe’s market

- United Kingdom: 21% of Europe’s market

- Japan: 12% of Asia-Pacific market

- China: 29% of Asia-Pacific market

anti-venom market Latest Trends

The anti-venom market Trends are evolving rapidly with the integration of biotechnology, recombinant DNA techniques, and next-generation immunotherapy platforms. Manufacturers are increasingly investing in species-targeted anti-venom formulations to improve neutralization efficiency and reduce serum-related side effects. One of the major trends in the anti-venom market Research Report is the shift toward freeze-dried anti-venom products that offer longer shelf life and easier transportation in remote healthcare regions. This trend is highly beneficial for tropical and underdeveloped areas where cold-chain logistics remain limited.

Download Free sample to learn more about this report.

Digital toxicology databases and AI-assisted venom identification tools are also emerging as important market trends. Healthcare providers are increasingly using rapid diagnostic systems to identify venom species and administer the most effective anti-venom therapy quickly. In addition, governments in Asia-Pacific, Africa, and Latin America are expanding funding for anti-venom stockpiling initiatives due to the high burden of snakebite mortality. The Anti-Venom Industry Report further indicates rising demand for region-specific anti-venom products designed for local venomous species.

anti-venom market Dynamics

DRIVER

Rising Incidence of Venomous Snakebites and Scorpion Stings Globally.

The increasing number of venomous snakebite and scorpion sting cases is one of the strongest growth drivers in the anti-venom market Analysis. Rural populations in tropical and subtropical regions face significant risks due to agricultural activities, deforestation, and climate-related habitat shifts that increase human interaction with venomous species. Governments and healthcare agencies are recognizing envenomation as a major public health issue, leading to expanded anti-venom procurement and emergency treatment programs. Hospitals and trauma centers are maintaining larger anti-venom inventories to ensure immediate treatment availability. Rising awareness campaigns regarding snakebite management and first-aid protocols are further contributing to anti-venom market Growth. Pharmaceutical companies are also expanding production capacities to address increasing demand from public healthcare systems. The anti-venom market Forecast remains favorable as healthcare authorities prioritize toxin-neutralizing therapies in emergency medicine infrastructure development.

RESTRAINT

Complex Manufacturing Processes and Limited Profitability.

The anti-venom market faces substantial restraints due to the highly specialized and expensive manufacturing process involved in anti-venom production. Traditional anti-venom manufacturing requires animal immunization, plasma extraction, purification, and extensive quality testing, which significantly increases operational costs. In many regions, anti-venom products are considered low-profit specialty therapeutics, reducing commercial incentives for pharmaceutical manufacturers. Supply shortages are common because demand is concentrated in low-income regions where healthcare budgets remain limited. Regulatory compliance requirements related to biologic production and toxin handling also create barriers for market expansion. In addition, short shelf life and transportation challenges affect distribution in remote areas. These factors collectively limit product accessibility and create fluctuations in anti-venom supply chains. The Anti-Venom Industry Analysis indicates that inconsistent reimbursement systems in developing economies further constrain market expansion.

OPPORTUNITY

Development of Recombinant and Next-generation Anti-Venom Vherapies.

The emergence of recombinant biotechnology and monoclonal antibody research presents substantial opportunities for the anti-venom market Opportunities landscape. Companies are exploring synthetic anti-venom therapies that can offer higher specificity, reduced allergic reactions, and scalable manufacturing capabilities. Recombinant anti-venoms may eliminate dependence on animal-derived plasma, reducing production variability and contamination risks. Increasing investments in venom proteomics and toxin mapping technologies are also creating opportunities for highly targeted therapies. Government-funded neglected tropical disease initiatives are supporting anti-venom innovation programs globally. Expansion into underserved African, Asian, and Latin American markets represents another major opportunity for manufacturers. Pharmaceutical firms are also collaborating with research institutes to develop region-specific venom neutralization products. The anti-venom market Research Report highlights rising opportunities for portable freeze-dried formulations that can improve treatment accessibility in rural healthcare settings.

CHALLENGE

Inadequate Healthcare Access in High-Risk Regions.

One of the primary challenges in the anti-venom market is the lack of adequate healthcare infrastructure in regions with the highest incidence of venomous bites and stings. Many rural communities in Africa, Asia-Pacific, and Latin America face delayed treatment access due to poor transportation systems and insufficient hospital facilities. Healthcare professionals in remote areas may also lack specialized training for venom identification and anti-venom administration. In addition, counterfeit or substandard anti-venom products continue to create safety concerns in some markets. Limited cold-chain infrastructure affects the storage and distribution of temperature-sensitive biologics. The anti-venom market Outlook also faces challenges associated with uneven species coverage, as some anti-venom products may not effectively neutralize local venom variants. Furthermore, patient affordability remains a major issue in low-income regions where healthcare insurance penetration is limited.

anti-venom market Segmentation

By Type

Snake anti-venom represents nearly 72% of the anti-venom market Size due to the global burden of venomous snakebite cases, especially in Asia-Pacific, Africa, and Latin America. The Anti-Venom Industry Report identifies cobra, viper, rattlesnake, and krait bites as major contributors to demand. Governments are increasingly maintaining emergency stockpiles of snake anti-venom to reduce mortality and long-term disability caused by envenomation. Pharmaceutical manufacturers are focusing on polyvalent snake anti-venoms capable of neutralizing toxins from multiple snake species. Increasing agricultural activities in rural regions continue to expose workers to venomous snakes, further supporting market demand.

Scorpion anti-venom accounts for nearly 28% of the anti-venom market Share and is witnessing increased demand across desert and tropical regions where venomous scorpion species are highly prevalent. Countries in the Middle East, North Africa, India, and Latin America are major consumers of scorpion anti-venom therapies. Pediatric envenomation cases are particularly driving market demand because children face higher mortality risks from neurotoxic scorpion venom. The anti-venom market Analysis indicates rising investments in rapid-response emergency treatment programs in high-risk regions.

To know how our report can help streamline your business, Speak to Analyst

By Application

Polyvalent anti-venom holds approximately 68% of the anti-venom market Share because it can neutralize venom from multiple species, making it highly practical in emergency treatment scenarios where venom identification may be delayed. Hospitals and rural healthcare centers prefer polyvalent formulations due to their broader therapeutic coverage and operational convenience. The anti-venom market Research Report highlights strong demand for polyvalent products in regions with diverse venomous snake populations. Manufacturers are continuously improving purification methods to minimize hypersensitivity reactions associated with polyvalent serum administration.

Monovalent anti-venom contributes nearly 32% of the anti-venom market Size and is valued for its high specificity against individual venom species. These products are commonly used in advanced healthcare systems where rapid venom identification is possible through toxicology diagnostics and clinical expertise. Monovalent anti-venom often provides more efficient toxin neutralization with lower protein load exposure, reducing the risk of serum-related complications. The Anti-Venom Industry Analysis indicates growing interest in monovalent therapies for specialized treatment centers and precision medicine applications.

By Species

Snake anti-venom dominates the anti-venom market with nearly 72% market share due to the high prevalence of venomous snakebite cases across Asia-Pacific, Africa, and Latin America. Demand for snake anti-venom products continues to increase because of rising agricultural activities, rural population exposure, and expanding emergency healthcare awareness programs. The anti-venom market Analysis highlights strong demand for therapies targeting cobra, viper, rattlesnake, and krait envenomation. Hospitals and trauma centers remain the major consumers of snake anti-venom because immediate administration is critical for survival and recovery. Pharmaceutical manufacturers are investing in improved purification technologies and freeze-dried formulations to increase product stability and treatment efficiency.

Scorpion anti-venom accounts for approximately 28% of the anti-venom market Share and is witnessing rising demand in desert and tropical regions where scorpion stings are highly prevalent. Countries across the Middle East, North Africa, India, and Latin America are key consumers of scorpion anti-venom therapies. Pediatric envenomation cases are significantly driving product demand because children are more vulnerable to neurotoxic scorpion venom. The anti-venom market Trends indicate increasing investments in emergency toxicology programs and rapid-response treatment systems for scorpion sting management. Manufacturers are focusing on highly purified anti-venom formulations to reduce hypersensitivity reactions and improve clinical outcomes.

By Type

Polyvalent anti-venom holds nearly 68% of the anti-venom market Share because it is capable of neutralizing venom from multiple species, making it highly suitable for emergency healthcare settings. Hospitals and rural healthcare centers prefer polyvalent anti-venom because venom identification is often delayed during medical emergencies. The anti-venom market Research Report indicates strong adoption of polyvalent formulations in regions with diverse venomous snake populations. Manufacturers are continuously improving plasma purification methods to minimize allergic reactions and serum sickness associated with traditional anti-venom therapies. Public healthcare systems are also increasing procurement of polyvalent products to strengthen emergency preparedness programs.

Monovalent anti-venom contributes approximately 32% of the anti-venom market Size and is preferred for species-specific venom treatment where accurate diagnosis is available. These products provide targeted toxin neutralization with reduced protein exposure, which lowers the risk of adverse immune reactions. The Anti-Venom Industry Analysis highlights growing demand for monovalent therapies in advanced healthcare systems with strong diagnostic capabilities. Hospitals equipped with specialized toxicology units increasingly use monovalent anti-venom for precision treatment approaches. Pharmaceutical companies are investing in region-specific monovalent formulations targeting medically significant venomous species.

By Mode Of Action

Cytotoxic anti-venom products are widely used for treating venom that causes severe tissue destruction, muscle damage, swelling, and necrosis. These therapies are especially important for viper snakebite treatment because cytotoxic venom can lead to permanent tissue injury and limb complications if untreated. The anti-venom market Outlook indicates increasing demand for cytotoxic anti-venom in regions with high incidences of hemotoxic and tissue-damaging envenomation cases. Hospitals and trauma centers prioritize rapid administration of cytotoxic anti-venom to prevent long-term disability and reduce surgical intervention requirements. Manufacturers are developing advanced purification techniques to improve toxin-neutralization efficiency and reduce serum-related complications.

Neurotoxic anti-venom plays a critical role in treating venom that affects the nervous system and causes paralysis, respiratory failure, and neurological complications. Cobra, krait, and scorpion envenomation cases are major contributors to the demand for neurotoxic anti-venom therapies. The anti-venom market Growth is strongly supported by increasing awareness regarding rapid intervention for neurotoxic venom exposure. Hospitals and emergency care units are expanding neurotoxic anti-venom inventories because delayed treatment can result in fatal outcomes. Pharmaceutical companies are focusing on high-efficacy formulations capable of rapid toxin neutralization and improved patient recovery rates.

By End-use

Hospitals account for the largest share of the anti-venom market due to their role as primary emergency treatment centers for venomous bites and stings. Emergency departments, trauma centers, and critical care units maintain extensive anti-venom inventories to ensure immediate administration during life-threatening envenomation cases. The anti-venom market Research Report highlights increasing investments by hospitals in advanced toxicology diagnostics and emergency response infrastructure. Hospitals are also adopting freeze-dried anti-venom products because they offer easier storage and rapid deployment advantages. Government healthcare agencies continue to support hospital procurement programs aimed at reducing mortality rates associated with snakebites and scorpion stings.

Clinics represent an important segment within the anti-venom market, particularly in rural and underserved regions where immediate hospital access may be limited. Local clinics and community healthcare centers are increasingly stocking anti-venom products to provide rapid first-line treatment for venomous bites and stings. The Anti-Venom Industry Report indicates rising government initiatives focused on improving toxicology treatment accessibility in remote areas through clinic-based healthcare programs. Clinics are also benefiting from the availability of freeze-dried anti-venom formulations that simplify storage and transportation requirements. Healthcare professionals working in clinics are receiving specialized training for venom identification and emergency treatment protocols.

anti-venom market Regional Outlook

North America

North America Anti-Venom Market Share, 2026 (%)

To get more information on the regional analysis of this market, Download Free sample

North America accounts for nearly 31% of the anti-venom market Share due to the presence of advanced healthcare infrastructure, sophisticated emergency response systems, and strong biologics manufacturing capabilities. The region continues to experience consistent demand for anti-venom products because of venomous snake and scorpion incidents across the United States and parts of Mexico. Hospitals, trauma centers, and poison control facilities maintain extensive anti-venom inventories to ensure rapid treatment during medical emergencies. The anti-venom market Analysis indicates rising investments in recombinant anti-venom research, toxin-neutralizing antibodies, and precision toxicology diagnostics throughout the region. Government healthcare agencies are increasingly supporting emergency preparedness programs focused on venom-related incidents. Biotechnology firms are also investing in highly purified anti-venom formulations designed to reduce allergic reactions and improve patient recovery outcomes. Veterinary applications are contributing to market expansion because pets and livestock frequently encounter venomous species in rural areas. Growing awareness regarding snakebite management, advanced diagnostic systems, and improved healthcare accessibility are expected to strengthen the anti-venom market Outlook in North America over the coming years.

Europe

Europe holds approximately 24% of the anti-venom market Share and remains an important center for pharmaceutical innovation, biologics manufacturing, and toxin-neutralization research. The region benefits from highly developed healthcare systems and increasing investments in advanced anti-venom therapies. European pharmaceutical companies are actively focusing on recombinant anti-venom products with enhanced efficacy, safety, and reduced immunogenicity. The Anti-Venom Industry Report highlights increasing collaborations between biotechnology companies, toxicology laboratories, and academic institutions throughout Europe. Governments are supporting anti-venom stockpiling initiatives and public health preparedness programs to strengthen emergency treatment capabilities. Rising travel-related envenomation cases and increasing awareness regarding exotic venomous species are also supporting market growth. Manufacturers are investing heavily in plasma purification technologies and antibody engineering platforms to improve product quality and production efficiency. The anti-venom market Forecast remains positive because healthcare providers are emphasizing rapid diagnosis, species-specific treatment protocols, and emergency toxicology preparedness. Continuous advancements in biologics research and emergency medicine infrastructure are expected to drive further market expansion across Europe.

Germany anti-venom market

Germany contributes nearly 27% of the Europe anti-venom market Share because of its strong pharmaceutical manufacturing sector and advanced biomedical research infrastructure. The country is recognized for significant investments in recombinant antibody technologies, plasma-derived therapeutics, and toxin-specific biologics research. German biotechnology firms are actively collaborating with research institutes and healthcare organizations to improve anti-venom treatment effectiveness and production efficiency. The anti-venom market Research Report indicates rising demand for highly purified biologics and advanced emergency toxicology treatments in Germany. Hospitals and emergency care facilities maintain strong anti-venom procurement systems to manage venom-related medical emergencies efficiently. Government support for biotechnology innovation and pharmaceutical modernization programs continues to strengthen the country’s role within the global Anti-Venom Industry Analysis. German manufacturers are also emphasizing the reduction of serum-related side effects associated with traditional anti-venom therapies. Increasing investments in precision medicine, biologics engineering, and advanced purification technologies are expected to support long-term market growth across Germany.

United Kingdom anti-venom market

The United Kingdom accounts for nearly 21% of the Europe anti-venom market Size due to its advanced healthcare infrastructure, strong biotechnology sector, and extensive pharmaceutical research activities. UK-based research institutions are actively involved in venom immunology studies, recombinant biologics development, and monoclonal antibody innovation programs. The anti-venom market Analysis highlights increasing investments in toxin-neutralization technologies and emergency toxicology preparedness throughout the country. Hospitals in the United Kingdom are improving response capabilities for imported envenomation cases associated with international travel and exotic pet ownership. Public health agencies are supporting awareness programs related to venomous bite management and emergency treatment procedures. Biotechnology firms are investing in advanced purification technologies aimed at improving anti-venom safety and therapeutic effectiveness. The anti-venom market Trends also indicate growing adoption of freeze-dried anti-venom products because of their storage and transportation advantages. Strong collaboration between pharmaceutical companies, universities, and healthcare organizations continues to accelerate innovation and support future market development in the United Kingdom.

Asia-Pacific

Asia-Pacific dominates the anti-venom market with nearly 34% market share due to the high prevalence of venomous snakebites and scorpion stings across densely populated rural regions. Countries such as India, China, Indonesia, Thailand, and Australia contribute significantly to regional demand because of tropical climates, agricultural activities, and large populations exposed to venomous wildlife. Governments throughout the region are expanding anti-venom distribution networks and strengthening rural emergency healthcare infrastructure. The anti-venom market Growth in Asia-Pacific is supported by increasing domestic biologics manufacturing capabilities and rising investments in plasma-derived therapeutics. Pharmaceutical companies are developing region-specific anti-venom formulations designed to target local venomous species effectively. Public awareness campaigns regarding snakebite first aid and emergency medical treatment are also improving product adoption rates. Hospitals and trauma centers are enhancing inventory management systems to address growing demand for life-saving anti-venom therapies. Freeze-dried anti-venom products are gaining popularity because they provide easier transportation and storage in remote healthcare environments. Continuous advancements in toxin research, antibody engineering, and healthcare modernization are expected to strengthen the anti-venom market Outlook in Asia-Pacific.

Japan anti-venom market

Japan represents nearly 12% of the Asia-Pacific anti-venom market Share because of its highly advanced biotechnology industry and modern healthcare infrastructure. The country focuses strongly on precision biologics, toxin-specific therapies, and innovative antibody engineering technologies. Japanese pharmaceutical companies are investing in advanced anti-venom purification systems aimed at improving safety profiles and reducing immunogenic reactions. The anti-venom market Research Report highlights increasing research related to marine toxins, exotic venom treatment, and recombinant biologics development in Japan. Hospitals maintain specialized toxicology units equipped to handle venomous bite and sting emergencies efficiently. Government healthcare programs continue to support innovation in emergency medicine and biologics manufacturing. Research institutions are collaborating with international pharmaceutical companies to accelerate advancements in toxin-neutralization therapies. The anti-venom market Trends in Japan also include growing demand for precision diagnostics and species-specific anti-venom products. Strong investments in pharmaceutical R&D and advanced healthcare technologies are expected to support future market expansion throughout the country.

China anti-venom market

China contributes approximately 29% of the Asia-Pacific anti-venom market Size due to its large rural population, expanding healthcare infrastructure, and high incidence of venomous snakebite cases. Agricultural workers and rural communities remain major consumers of anti-venom therapies across the country. The anti-venom market Analysis indicates growing government support for biologics manufacturing, emergency toxicology programs, and healthcare modernization initiatives. Chinese pharmaceutical companies are expanding plasma-derived therapeutic production facilities to strengthen domestic anti-venom supply chains and improve product accessibility. Hospitals and emergency healthcare centers are increasing procurement of advanced anti-venom formulations to manage rising patient volumes effectively. Research institutions are collaborating with biotechnology firms to develop recombinant anti-venom therapies and advanced venom diagnostic systems. The anti-venom market Trends also include increasing adoption of freeze-dried anti-venom products suitable for remote and underserved healthcare regions. Public awareness regarding venomous bite treatment and emergency response protocols is improving steadily across the country. Continuous investments in biologics innovation and healthcare infrastructure are expected to drive long-term anti-venom market growth in China.

Rest of World

The Rest of World region accounts for approximately 11% of the anti-venom market Share, with significant demand originating from Africa, Latin America, and the Middle East. These regions experience high rates of venomous snakebites and scorpion stings, particularly in remote rural communities where healthcare access remains limited. Governments and international health organizations are investing heavily in anti-venom procurement programs and emergency healthcare infrastructure to reduce mortality associated with envenomation. The anti-venom market Outlook in Africa remains strong because of widespread exposure to highly venomous snake species and increasing public health initiatives. Latin American countries are witnessing rising demand for anti-venom therapies among agricultural workers and rainforest populations. Middle Eastern markets are primarily driven by increasing scorpion sting treatment requirements and emergency medical preparedness programs. Manufacturers are focusing on affordable anti-venom production strategies and freeze-dried formulations to improve accessibility in underserved areas. The anti-venom market Forecast indicates growing investments in healthcare modernization, biologics manufacturing, and toxin-specific treatment programs across developing economies.

List of Top Anti-Venom Companies

- Bharat Serums and Vaccines Limited (BSV)

- Boehringer Ingelheim International GmbH

- Boston Scientific Corporation

- CSL Limited

- Haffkine Bio-Pharmaceutical Corporation Limited

- Incepta Pharmaceuticals Limited

- Merck & Co. Inc.

- Pfizer, Inc

- MicroPharm Limited

- Rare Disease Therapeutics Inc.

- South African Vaccine Producers (Pty) Ltd.

- Medtoxin Venom Laboratories

- Institute of Immunology

- Alomone Labs, Ltd.

- Sigma Aldrich

Top Two Companies by Market Share

- CSL Limited – Approximately 16% market share

- Bharat Serums and Vaccines Limited (BSV) – Approximately 13% market share

Investment Analysis and Opportunities

The anti-venom market Opportunities landscape is attracting growing investments from pharmaceutical companies, biotechnology firms, public health agencies, and international healthcare organizations. Increasing recognition of snakebite envenomation as a neglected tropical disease is encouraging governments to allocate larger healthcare budgets toward anti-venom accessibility and emergency treatment infrastructure. Investors are particularly interested in recombinant anti-venom technologies due to their scalability, improved safety profiles, and reduced dependence on animal-derived plasma.

Strategic collaborations between pharmaceutical manufacturers and research institutes are accelerating innovation in freeze-dried anti-venom products suitable for remote healthcare environments. Public-private partnerships are also expanding anti-venom stockpiling programs and rural healthcare distribution networks. The anti-venom market Forecast further highlights investment opportunities in rapid venom diagnostic systems, AI-assisted toxicology tools, and portable emergency treatment technologies designed for field deployment.

New Product Development

New product development in the anti-venom market is increasingly focused on improving therapeutic precision, safety, stability, and production efficiency. Pharmaceutical companies are investing heavily in recombinant anti-venom technologies capable of targeting specific venom toxins with enhanced neutralization performance. Advanced monoclonal antibody therapies are being explored as alternatives to traditional equine-derived serum products to minimize allergic reactions and serum sickness complications.

Nanotechnology-based toxin delivery interruption systems and rapid diagnostic kits are emerging as important innovation areas within the Anti-Venom Industry Analysis. Research institutions are mapping venom proteins using proteomics technologies to create highly targeted neutralization therapies. Manufacturers are also adopting advanced purification technologies to reduce protein impurities and improve biologic consistency. Increasing integration of artificial intelligence into venom classification and emergency treatment decision-making is expected to influence future anti-venom product development strategies globally.

Five Recent Developments (2023-2025)

- CSL Limited expanded biologics manufacturing capacity in 2024 to strengthen global anti-venom production and emergency supply distribution.

- Bharat Serums and Vaccines Limited introduced upgraded freeze-dried snake anti-venom formulations in 2023 for improved shelf stability in rural healthcare settings.

- Pfizer, Inc increased investments in recombinant antibody research programs focused on toxin-neutralization therapies during 2025.

- MicroPharm Limited announced collaboration agreements with toxicology research institutions in 2024 to develop advanced species-specific anti-venom products.

- South African Vaccine Producers (Pty) Ltd. expanded anti-venom accessibility initiatives across Sub-Saharan Africa in 2025 to address rising snakebite treatment demand.

Report Coverage of anti-venom market

The anti-venom market Report provides comprehensive analysis of market dynamics, product innovations, regional developments, competitive landscape, investment trends, and emerging therapeutic technologies. The report evaluates the impact of increasing snakebite and scorpion sting incidents on healthcare systems and analyzes demand trends across hospitals, emergency centers, military healthcare units, and rural medical facilities. Detailed segmentation analysis by type and application offers insights into evolving treatment preferences and procurement strategies.

Request for Customization to gain extensive market insights.

The anti-venom market Research Report also examines advancements in recombinant biologics, monoclonal antibodies, plasma purification technologies, and freeze-dried anti-venom products. Regional assessments cover North America, Europe, Asia-Pacific, and Rest of World markets, highlighting healthcare infrastructure developments and public health initiatives influencing market expansion. Company profiling sections analyze production capabilities, innovation strategies, and competitive positioning among major manufacturers.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us