Antimony Market Size, Share & Industry Analysis, By Application (Flame Retardants, Chemicals & Alloys, Lead Acid Batteries, Ceramics & Glass, and Others) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

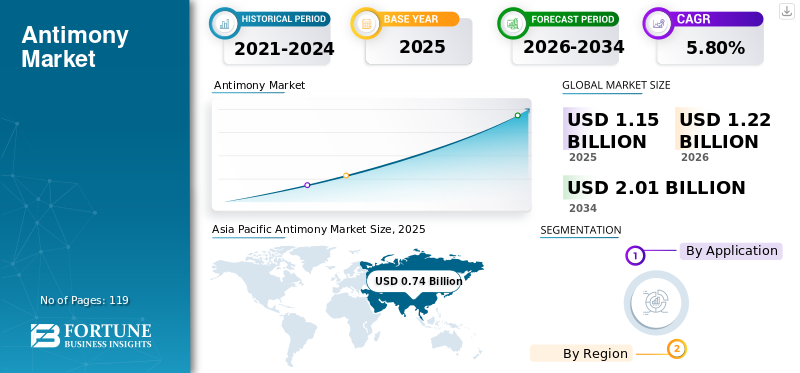

The global antimony market size was USD 1.15 billion in 2025 and is projected to grow from USD 1.22 billion in 2026 to USD 2.01 billion by 2034, exhibiting a CAGR of 5.80% during the forecast period. Asia Pacific dominated the antimony market with a market share of 64.40% in 2025. Moreover, the antimony market in the U.S. is projected to grow significantly, reaching an estimated value of USD 106.57 million by 2034, driven by the growing demand for OSHA regulated flame retardant clothing.

Antimony also called as stibnite (Sb) is a silver-grey chemical element with a silky, glossy surface. At ambient temperature, it is stable, but when heated, it interacts with oxygen to generate stibnite trioxide (Sb2O3). It has a melting point of 630°C and a density of 6.697 g/cm3 despite its low melting point. It is extremely rare in the Earth's crust, with only 0.4 parts per million (ppm) in the upper crust. It can be found in over 100 different mineral species, often combined with other elements, including mercury, silver, and gold. Stibnite is the most common ore material (Sb2S3). In 2011, 2014, and 2017, it was on the EU's list of key raw commodities.

Certain semiconductor devices, such as infrared detectors and diodes, are made with Sb in the electronics sector. To increase their hardness and strength, it is alloyed with certain other metals such as lead. Batteries make use of a Pb-Sb alloy. cable sheathing, and bullets are some of the other applications for alloys. Flame retardant materials, ceramics, glass, paints, and enamels are all made using its compounds.

The COVID-19 outbreak had a heavy toll on the mining industry. The global market was hit by disruptions in supply chains from key locations and uncertainty in demand throughout the world. Additionally, the government restrictions on mobility and production operations and the workforces confronting the risk of infections add another depth to the calamity. Consumers, communities, and industries worldwide suffered economic, social, and commercial consequences as a result of the COVID-19 pandemic. Regardless of the pandemic's subsequent path, the scenario was predicted to have long-term consequences.

The post-COVID condition displayed market recovery indicators, such as lower unemployment. Regardless of projects being restarted, rising product and raw material costs indicated a solid economic recovery.

Download Free sample to learn more about this report.

ANTIMONY MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.15 Billion

- 2026 Market Size: USD 1.22 Billion

- 2034 Forecast Market Size: USD 2.01 Billion

- CAGR: 5.80% from 2026–2034

- Asia Pacific dominated the antimony market with a 64.40% share in 2025.

- Flame retardants held the largest application share and are expected to account for 60.72% in 2026.

- Chemicals & alloys and lead-acid batteries segments are projected to witness significant growth through 2034.

North America

North America reached USD 0.09 billion in 2025 with a 7.60% share and is expected to maintain USD 0.09 billion in 2026.

Europe

Europe accounted for USD 0.21 billion in 2025 and is projected to reach USD 0.23 billion in 2026.

Asia Pacific

Asia Pacific generated USD 0.74 billion in 2025 and is expected to reach USD 0.79 billion in 2026.

U.S.

The market is valued at USD 0.076 billion by 2026 and is projected to reach USD 106.57 million by 2034.

Japan

The antimony market is expected to reach USD 0.068 billion by 2026.

Read More

Antimony Market Trends

Recovery and Recycling to Foster Market Growth

The experiment of sustainable development at the start of the 21st century has become systemic, with environmental, economic, and social dimensions on an identical footing. Metal recycling is one of the important practices of sustainability, which is being adopted by various companies. Metal recycling ends the loop in the production process, resulting in reduction of the amount of waste that ends up into landfill.

The metal recycling can prove to be very effective with selection of the material that is to be recycled. The industrial significance of antimony can be largely associated with its use as a flame retardant in coatings, plastics, and electronics, as a decolorizing agent in glass, catalyst for the production of PET polymers, and as an alloy in lead-acid batteries.

Antimony has become a more important element in recent years due to increased industrial demand and China's dominance in primary production. Its products can be manufactured using recycled antimony. Secondary supply, such as recycling and valorizing industrial waste, may be a viable option for ensuring a more secure long-term supply.

Secondary Sb can be found in two places: waste from the processing of Sb-bearing commodities and end-of-life products from urban mines and manufacturing leftovers. According to the UNEP antimony's global end-of-life (EoL) recycling rate is expected to be between 1% and 10%. According to the Raw Materials Supply Assessment (RMSA) study, conducted by BIO by Deloitte in 2015, the EoL recycling rate in the EU might be as high as 28%. Lead-acid batteries are the most common source of secondary antimony. As a result, its supply is virtually entirely determined by the level of lead recycling and market conditions for lead and lead-acid battery trash.

Download Free sample to learn more about this report.

Antimony Market Growth Factors

Increasing Demand for Flame Retardants to Propel Antimony Market Growth

Most of the world's reserve is utilized in flame-retardant raw materials such as its trioxide. Powdered trioxide is chemically inserted or physically blended into various products, including textiles. Although it is not a flame retardant in and of itself, the flame retardant apparels are manufactured using Sb as it suppresses and decreases the spread of flames when mixed with halogens such as bromine in polymers. Sb2O3 is commonly utilized in plastics, rubbers, paints, textiles, and various industrial safety garments and clothing for children to make them resistant to the spread of fire. Additionally, the stringent regulations mandated by the Occupational Safety and Health Administration OSHA to practice flame retardant clothing are driving the demand for flame retardants, further boosting the antimony market. For instance, OHSA regulation 1910.269 is referred to as the 269 Standard. This factor is related to people working in the electric power generation, transformation, control, and transmission industries. Electrical arcs are a common hazard for these workers.

Employers must train employees about potential hazards, according to the 269 Standard. Electrical arcs and how they can cause flames should be taught to them. The 269 Standard also forbids personnel from wearing garments that could catch fire and injure them. Clothing that catches fire and continues to burn is prohibited.

RESTRAINING FACTORS

Availability of Substitutes May Hamper Market Growth

In some of its applications, it can be easily substituted. For example, a composite of chromium, tin, titanium, zinc, and zirconium can be used as replacement in pigments and glass. Sb can be partially replaced in flame-retardant materials by compounds such alumina trihydrate, magnesium hydroxide, and zinc borate. It can be replaced in plastics manufacturing with various combinations of cadmium, barium, calcium, lead, tin, zinc, and germanium. This is projected to limit market growth.

Antimony Market Segmentation Analysis

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Flame Retardants Segment to Hold the Key Share Owing To Better Performance

The market is segmented into flame retardants, chemicals & alloys, lead-acid batteries, emulsion and others applications. Because of the increasing demand from the polymer production industry, the flame retardants grade segment is anticipated to hold a dominant market share of 60.72% in 2026. By the conclusion of the projection period, the chemicals & alloys and lead-acid batteries segments are predicted to grow significantly.

REGIONAL INSIGHTS

Asia Pacific Antimony Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The Asia Pacific market accounted for USD 0.74 billion in 2025, representing 64.40% of the global industry, and is expected to reach USD 0.79 billion in 2026. In 2023, Asia Pacific led the global market, and this dominance is likely to continue due to the presence of a substantial production base and end-user industries. Because of its enormous reserves, China produces more than half of the world's production. In addition, the regional market is being driven by rising demand from other countries. The Japan market is valued at USD 0.068 billion by 2026, the China market is valued at USD 0.575 billion by 2026, and the India market is valued at USD 0.07 billion by 2026.

Europe

In 2025, Europe generated USD 0.21 billion, contributing 18.60% to global market revenue, and is projected to grow to USD 0.23 billion in 2026. Europe is one of the key market. Since the previous decade, the EU has been a major global producer of its oxide. Oxide manufacturing in the EU is reliant on unwrought element imports. It is imported from nations like China and India to meet the rest of the demand. High demand Lead Acid Batteries from Europe is expected to boost the demand. The UK market is valued at USD 0.009 billion by 2026, and the Germany market is valued at USD 0.02 billion by 2026.

North America

North America maintained a strong presence in the global market, reaching USD 0.09 billion in 2025, accounting for 7.60% share, and is expected to reach USD 0.09 billion in 2026. The market in North America is expected to expand significantly. The increased need for flame retardants is affecting growth in North America, owing to rigorous rules implemented by authorities to protect employees from risks. Furthermore, rising demand from the electronics sector for manufacturing consumer electronics assists growth. The U.S. market is valued at USD 0.076 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

Latin America and Middle East and Africa

North America maintained a strong presence in the global market, reaching USD 0.09 billion in 2025, accounting for 7.60% share, and is expected to reach USD 0.09 billion in 2026. Latin America contributed 3.00% to the global market in 2025, with a valuation of USD 0.04 billion, and is projected to reach USD 0.04 billion in 2026. Latin America and Middle East and Africa are expected to show sluggish growth due to growing industrialization and urbanization. The increasing mining activities and elemental stibnite reserves in Bolivia are expected to drive market growth.

List of Key Companies in Antimony Market

Key Companies Investing in Technologies to Broaden their Market Presence

With many global players, the market is consolidated in nature. Campine NV, United States Antimony Corp, Lambert Metals International, and Suzuhiro Chemical & Materials are the key manufacturers.

Players in the industry mostly operate based on the product's pricing and application features. Companies are getting into partnerships to enhance product portfolio in order to increase their market share and get a competitive edge.

LIST OF KEY COMPANIES PROFILED:

- Campine NV (Antwerp, Belgium)

- Huachang Antimony Industry (Yiyang, China)

- United States Antimony Corp (Montana, U.S.)

- Korea Zinc Co. Ltd, (Seoul, South Korea)

- Lambert Metals International (Bushey, U.K.)

- Mandalay Resources Ltd (Toronto, Canada)

- NYACOL Nano Technologies (Massachusetts. U.S.)

- Suzuhiro Chemical & Materials (Ibaraki, Japan)

KEY INDUSTRY DEVELOPMENTS:

- January 2021 – Campine expands its recycling efforts with innovative technology for recycling chemicals directly from post-consumer and industrial metal trash. Based in Beerse near Antwerp, Campine is involved in two main activities: lead recycling and the production of antimony trioxide, a chemical additive.

- June 2019- United States Antimony Corporation reported continuous capacity expansion at its smelter in Madero, Coahuila, Mexico. The third long rotary furnace (LRF) will be installed as part of this. Three more LRFs are in the company's inventory. The additional capacity is planned to meet production increases from the Company's Wadley and Sierra Guadalupe Mines, with furnace recovery in the 96 percent to 98 percent range.

REPORT COVERAGE

The global antimony market research study examines the industry in depth, focusing on critical factors such as key players operating, products, and raw materials. In addition, the study provides insights into market trends as well as key industry advancements. The study includes different variables that have contributed to the market's growth in recent years, in addition to the reasons listed above.

This study examines the industry's newest market dynamics and opportunities, as well as historical data and revenue growth estimates at the global, regional, and national levels.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.80% from 2026 to 2034 |

|

Unit |

Value (USD Billion) , Volume (Kilo Tons) |

|

Segmentation

|

By Application

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1.22 billion in 2026 and is expected to reach USD 2.01 billion by 2034.

In 2025, the Asia Pacific market size stood at USD 0.74 billion.

Growing at a CAGR of 5.80%, the market will exhibit a steady growth rate during the forecast period (2026-2034).

The Chemical & Materials segment is expected to be the leading segment in 2023.

Growing demand for flame retardants is expected to drive the market.

Campine NV, United States Antimony Corp, Lambert Metals International, and Suzuhiro Chemical & Materials are major players in the global markets.

- 2021-2034

- 2025

- 2021-2024

- 119

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us