Apparel Logistics Market Size, Share & Industry Analysis, By Transportation Mode (Roadways, Airways, Seaways, Railways, and Multimodal), By Service Type (Transportation, Warehousing & Distribution, Freight Forwarding, Reverse Logistics, and Value-Added Services), By Distribution Channel (Offline Retail, Online Retail, and Omni-channel Retail), By End User (Fashion Brands & Retailers, Apparel Manufacturers, E-commerce Fashion Platforms, Luxury Apparel Companies, and Sportswear & Athleisure Brands), and Regional Forecasts, 2026-2034

(Offer valid till 15th Aug 2026)

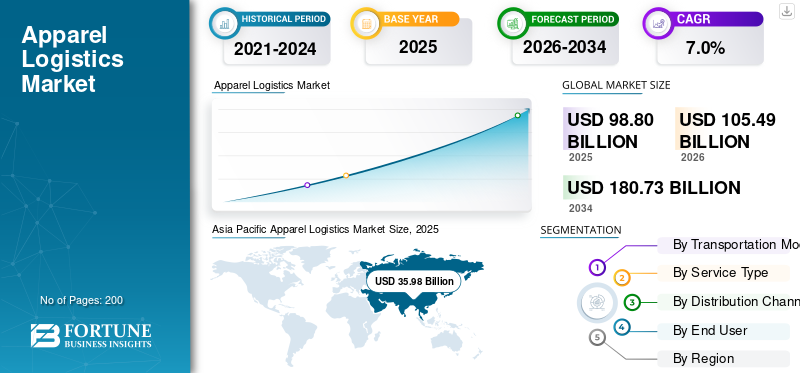

Apparel Logistics Market Size and Future Outlook

The apparel logistics market size was valued at USD 98.80 billion in 2025. The market is projected to grow from USD 105.49 billion in 2026 to USD 180.73 billion by 2034, exhibiting a CAGR of 7.0% during the forecast period. Asia Pacific dominated the apparel logistics market with a market share of 36.41% in 2025.

The market represents the movement, storage, handling, and delivery of finished apparel products across domestic and international supply chains. It includes transportation, warehousing and distribution, freight forwarding, reverse logistics, customs handling, packaging, labeling, and last-mile delivery for fashion brands, retailers, manufacturers, and e-commerce platforms. The market is closely linked with fashion cycles, seasonal launches, fast-changing consumer demands, and the rising demand for efficient supply chain operations.

The industry will evolve toward faster, more flexible, and more technology-driven logistics models. Fashion companies are under pressure to maintain lean inventories while still meeting high consumer expectations for availability, speed, visibility, and returns convenience. This is increasing demand for advanced inventory management, automated fulfillment centers, real-time shipment tracking, and integrated distribution services. E-commerce and omni-channel retail are also reshaping apparel logistics, as brands must serve stores, marketplaces, warehouses, and direct-to-consumer customers from connected networks.

Key applications include retail replenishment, e-commerce fulfillment, cross-border apparel movement, fashion warehousing, reverse logistics, luxury apparel handling, sportswear distribution, and value-added services such as tagging, repacking, and quality checks. A significant market trend include automation, greener transport, nearshoring, data-led planning, and stronger returns processing.

Major companies including DHL Group, Kuehne+Nagel International AG, DSV A/S, and DB Schenker are investing in automation, fashion-dedicated fulfillment, sustainable shipping, and regional distribution networks to improve customer experiences and respond to changing market needs.

Download Free sample to learn more about this report.

Apparel Logistics Market Key Takeaways

- 2025 Market Size: USD 98.80 Billion

- 2026 Market Size: USD 105.49 Billion

- 2034 Forecast Market Size: USD 180.73 Billion

- CAGR: 7.0% from 2026–2034

- Asia Pacific dominated the apparel logistics market with a 36.41% share in 2025.

- Transportation held the largest share among service types in 2025.

- Roadways dominated the transportation mode segment in 2025.

Asia Pacific

Asia Pacific led the market with USD 35.98 billion in 2025, supported by its strong apparel manufacturing and export base.

North America led the global market with a 49.53% share in 2025.

North America is projected to reach USD 27.12 billion in 2026, maintaining its position as the second-largest regional market.

Europe

Europe is projected to reach USD 24.35 billion in 2026, driven by cross-border e-commerce and mature retail logistics.

U.S.

The U.S. apparel logistics market was valued at USD 18.43 billion in 2025, representing approximately 18.7% of global sales.

Japan

Japan remains an important apparel logistics market, supported by advanced retail networks and efficient supply chain infrastructure.

Read More

APPAREL LOGISTICS MARKET TRENDS

Sustainable and Low-Emission Fashion Logistics is a Key Market Trend

Sustainability is becoming one of the major market trend as brands reduce emissions across ocean freight, air cargo, warehouses, and last-mile delivery. Fashion companies are asking logistics partners to provide greener transport, route optimization, low-emission fuels, and transparent carbon reporting. This trend supports premium distribution services and helps logistics providers differentiate their offerings.

- For instance, in October 2023, Inditex partnered with Maersk’s ECO Delivery Ocean program to reduce maritime transport emissions by more than 80%.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Fashion E-Commerce Accelerates Demand for Agile Apparel Logistics

Rising online fashion sales are increasing demand for fast fulfillment, parcel delivery, returns handling, and real-time visibility. Apparel buyers expect flexible delivery, easy returns, and better customer experiences, forcing brands to improve supply chains and work with specialized logistics partners. This supports apparel logistics market growth across fulfillment centers, last-mile delivery, warehousing and distribution, and reverse logistics, especially in high-penetration e-commerce industries.

- For instance, in October 2025, DHL reported that omni-channel strategies, AI personalization, cross-border expansion, and logistics excellence are shaping global e-commerce growth.

MARKET RESTRAINTS

High Fulfillment and Return Costs Limit Market Profitability

Apparel logistics faces pressure from high return rates, labor costs, warehouse expenses, fuel volatility, and fragmented order sizes. Online fashion often requires individual picking, packing, shipping, inspection, repacking, and restocking, which raises the cost of each logistics service. These pressures can reduce margins for logistics providers and apparel brands, especially when consumer expectations demand free or low-cost returns.

- For instance, in March 2025, Avery Dennison reported that one-fourth of the U.S. and U.K. fashion retailers had limited or no item-level stock visibility.

MARKET OPPORTUNITIES

Automated Fulfillment Networks Creates Strong Growth Opportunity

Automation creates a major opportunity for the market by improving order accuracy, speed, labor productivity, and inventory management. Automated fulfillment centers can process mixed apparel orders faster while supporting store replenishment and e-commerce shipping from the same facility. This helps retailers respond to market needs, reduce delivery times, and improve customer experiences across online and offline channels.

- For instance, in October 2025, Macy’s opened its largest automated fulfillment and store replenishment center in North Carolina to improve delivery speed and efficiency.

MARKET CHALLENGES

Supply Chain Disruptions Challenges Timely Apparel Delivery

Apparel logistics is highly exposed to port congestion, geopolitical issues, container shortages, customs delays, and sudden demand swings. Since fashion products are seasonal and trend-sensitive, delayed shipments can quickly reduce product value and increase markdown risk. These disruptions make supply chains harder to manage and force brands to hold buffer stock, diversify sourcing, or use expensive air freight.

- For instance, in 2024, Vogue Business reported that Red Sea disruptions caused some European fashion retailers to face shipping delays for around three weeks.

Segmentation Analysis

By Transportation Mode

Roadways Dominate Due to Store Replenishment and Last-Mile Movement

On the basis of transportation mode, the market is segmented into roadways, airways, seaways, railways, and multimodal.

Roadways dominate the market as apparel products require frequent movement between ports, warehouses, stores, and consumers. Trucking supports domestic replenishment, last-mile delivery, returns collection, and regional fulfillment. It also provides flexibility for fashion companies responding to quick-changing consumer demands and urgent market needs, especially where retail stores and e-commerce networks operate together.

- For instance, in October 2024, GXO signed a transport delivery agreement with Matalan to serve over 200 U.K. and Ireland stores.

Airways segment is expected to grow at a CAGR of 8.4% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

Transportation Leads as Apparel Requires Continuous Physical Movement

On the basis of service type, the market is segmented into transportation, warehousing & distribution, freight forwarding, reverse logistics and value-added services.

Transportation held largest apparel logistics market share as finished garments move repeatedly across ports, distribution centers, retail outlets, and homes. Apparel brands rely on road, sea, air, and multimodal networks to maintain seasonal availability and meet delivery commitments. As consumer expectations rise, transportation remains the largest spending area within apparel logistics, supported by faster replenishment and stronger cross-border movement.

- For instance, in February 2025, GXO expanded Castore’s logistics operations across warehousing and transportation in the U.K. and U.S.

Reverse logistics segment is expected to grow at a CAGR of 9.7% over the forecast period.

By Distribution Channel

Offline Retail Dominates Due to Large Store-Based Apparel Sales

On the basis of distribution channel, the market is segmented into offline retail, online retail and omni-channel retail.

Offline retail dominates as physical stores account for a large share of apparel sales globally. Stores require regular replenishment, stock transfers, seasonal inventory planning, and returns movement. This keeps demand strong for warehousing and distribution, road transport, and store-facing distribution services, even as online fashion grows faster.

- For instance, in January 2025, H&M stated that 2025 investments would mainly support its store portfolio and supply chain.

Online retail segment is expected to grow at a CAGR of 10.2% over the forecast period.

By End User

Fashion Brands and Retailers Segment Dominate Due to Large Distribution Networks

On the basis of end user, the market is segmented into fashion brands & retailers, apparel manufacturers, e-commerce fashion platforms, luxury apparel companies and sportswear & athleisure brands.

Fashion brands and retailers dominate as they control large store networks, online channels, seasonal collections, and supplier relationships. Their operations require reliable inventory management, fast replenishment, returns handling, and integrated supply chains. These companies generate highest logistics demand as they balance store availability, e-commerce fulfillment, and improving customer experiences.

- For instance, in February 2025, Castore expanded its GXO partnership to support global logistics operations as the sportswear brand scaled internationally.

E-commerce fashion platforms segment is expected to grow at a CAGR of 10.7% over the forecast period.

Apparel Logistics Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America and the Middle East & Africa.

Asia Pacific

Asia Pacific Apparel Logistics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held a dominant market share in 2025, valuing at USD 35.98 billion, and also maintained the leading share in 2024, with USD 34.02 billion. This is due to its large apparel manufacturing base, export-led production hubs, rising domestic consumption, and expanding e-commerce ecosystem. China, India, Vietnam, South Korea, and Japan support apparel movement through ports, factories, fulfillment centers, and retail networks. The region benefits from strong sourcing activity, improving infrastructure, and growing demand for efficient supply chain operations across fast fashion and online channels.

- For instance, in October 2025, SHEIN’s Zhaoqing logistics park in China achieved carbon neutrality for FY2024 after reducing over 32,000 tonnes of CO₂e.

China Apparel Logistics Market

China market is projected to be one of the largest worldwide and 2025 revenues were at USD 10.33 billion, representing roughly 10.5% of global sales.

India Apparel Logistics Market

India market in 2025 was at USD 5.11 billion, accounting for roughly 5.2% of global revenues.

North America

North America is estimated to reach USD 27.12 billion in 2026 and secure the position of second-largest region in the market. North America will grow through strong U.S. apparel consumption, high parcel volumes, e-commerce fulfillment, and reverse logistics. The U.S. market is highly developed, with retailers investing in automation and faster delivery. Canada adds to stable cross-border demand, while Mexico benefits from nearshoring and road-linked supply chains.

U.S. Apparel Logistics Market

Based on North America’s strong contribution, the U.S. market reached at USD 18.43 billion in 2025, representing roughly 18.7% of global sales.

Europe

Europe is projected to record a growth rate of 5.1% in the coming years, and reach a valuation of USD 24.35 billion by 2026. Europe will grow steadily due to luxury fashion, cross-border e-commerce, mature retail networks, and strong multimodal infrastructure. Germany, the U.K., France, Italy, and the Netherlands support regional supply chains through ports, warehouses, and fulfillment hubs. Growth will be driven by greener logistics, better inventory management, and rising demand for premium distribution services.

Germany Apparel Logistics Market

Germany market in 2025 was at USD 4.63 billion, accounting for roughly 4.7% of global revenues.

U.K. Apparel Logistics Market

U.K. market in 2025 was valued at USD 4.21 billion, accounting for roughly 4.3% of global revenues.

Latin America

Latin America will expand as apparel retail formalizes, e-commerce adoption rises, and logistics outsourcing increases. Brazil leads the region due to its large domestic market, while Argentina and other markets add urban retail demand. Growth will depend on better road networks, warehouse modernization, and stronger logistics service reliability.

Middle East & Africa

Middle East & Africa will grow from a smaller base, supported by import-led apparel demand, luxury retail, GCC logistics investment, and regional distribution hubs. UAE and Saudi Arabia are key markets due to high-value fashion imports, e-commerce expansion, and improving warehousing and distribution networks.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Players Compete Through Speed, Visibility, and Fulfillment Scale

The competitive landscape of the apparel logistics market is shaped by global 3PLs, freight forwarders, contract logistics specialists, parcel delivery providers, and regional distribution companies. Leading players compete by offering end-to-end fashion logistics solutions that combine transportation, warehousing and distribution, freight forwarding, customs brokerage, reverse logistics, and value-added services. Companies such as DHL Group, Kuehne+Nagel International AG, GXO Logistics, Inc., DSV A/S, A.P. Moller-Maersk, DB Schenker, and CEVA Logistics are strengthening fashion-focused networks to support shorter product lifecycles and volatile consumer demands.

Competition is increasingly based on speed, flexibility, digital visibility, automation, and sustainability. Apparel customers require a logistics service that can handle seasonal peaks, product launches, high return rates, and fragmented order profiles. As a result, leading providers are expanding automated warehouses, investing in transport management systems, improving inventory management, and offering multimodal distribution services across stores, marketplaces, and e-commerce channels.

Technology has become a major differentiator. Providers are using warehouse robotics, RFID, AI-based forecasting, and control towers to improve visibility across supply chains. Sustainability is another area of competition, with fashion brands asking logistics partners to reduce emissions through alternative fuels, optimized routing, and greener warehousing. At the same time, providers are expanding geographically to support nearshoring, cross-border e-commerce, and regional fulfillment.

The market remains competitive as apparel brands often use multiple providers across geographies. However, global firms with integrated transport, warehousing, and returns capabilities have an advantage as they can respond faster to consumer expectations and complex market needs.

- For instance, in February 2025, GXO expanded its Castore partnership to operate warehousing and transportation in the U.K., U.S., and Europe.

LIST OF KEY APPAREL LOGISTICS COMPANIES PROFILED

- DHL Group (Germany)

- Kuehne+Nagel International AG (Switzerland)

- DSV A/S (Denmark)

- DB Schenker (Germany)

- CEVA Logistics (France)

- GXO Logistics, Inc. (U.S.)

- P. Moller-Maersk (Denmark)

- Nippon Express Holdings, Inc. (Japan)

- Expeditors International of Washington, Inc. (U.S.)

- UPS Supply Chain Solutions (U.S.)

- FedEx Logistics (U.S.)

- GEODIS (France)

- Bolloré Logistics (France)

- XPO, Inc. (U.S.)

- Ryder System, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2026: DHL Supply Chain expanded its partnership with Pepco across Europe by operating five distribution centers covering approximately 290,000 square meters and supporting logistics for over 4,020 retail stores. The expansion strengthens apparel replenishment, inventory flow, and regional distribution efficiency while improving delivery reliability and fulfillment speed across multiple European fashion and discount retail markets.

- March 2026: Zalando announced the deployment of up to 50 AI-powered Nomagic robots across its European fulfillment centers to automate apparel and footwear logistics operations. The robots support item picking and shoebox handling, improving warehouse productivity, order accuracy, and processing speed while helping Zalando manage rising e-commerce order volumes and complex fashion inventory requirements across Europe.

- March 2026: ShipMonk opened its first fulfillment center designed specifically for apparel brands in Louisville, Kentucky. The facility spans 406,000 sq. ft., has 60 dock doors, and over 300,000 storage locations.

- February 2026: GXO launched a partnership with Hunkemöller in the Netherlands, marking the lingerie brand’s first outsourced B2B logistics operation and integrating B2B with e-commerce logistics.

- May 2025: DHL Supply Chain acquired IDS Fulfillment, adding over 1.3 million sq. ft. of multi-customer warehouse and distribution space across the U.S.

- January 2025: DHL Supply Chain acquired Inmar Supply Chain Solutions, adding 14 return centers and around 800 associates to strengthen North American reverse logistics.

- January 2025: GXO signed a long-term partnership with Calliope in Italy. Services include warehouse management, e-fulfillment, returns management, labeling, quality control, and global distribution from a 10,000 sq. meter warehouse.

REPORT COVERAGE

The apparel logistics market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Transportation Mode, Service Type, Distribution Channel, End User and Region |

| By Transportation Mode |

|

| By Service Type |

|

| By Distribution Channel |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 98.80 billion in 2025 and is projected to reach USD 180.73 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 35.98 billion.

The market is expected to exhibit a CAGR of 7.0% during the forecast period of 2026-2034.

Roadways segment led the market by transportation mode.

Expansion of fashion e-commerce is driving the market.

DHL Group, Kuehne+Nagel International AG, DB Schenker and FedEx Logistics are some of the top players in the market.

Asia Pacific held the largest share in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us