Application Integration Market Size, Share & Industry Analysis, By Component (Software and Services), By Integration Type (Application to Application (A2A), Data Integration, Process Integration, API Integration, and B2B Integration), By Deployment (On-premise and Cloud), By Enterprise Type (Large Enterprises and Small & Medium Enterprises (SMEs)), By Industry (BFSI, IT & Telecom, Healthcare, Retail, Manufacturing, Government, and Others), and Regional Forecast, 2026-2034

APPLICATION INTEGRATION MARKET SIZE AND FUTURE OUTLOOK

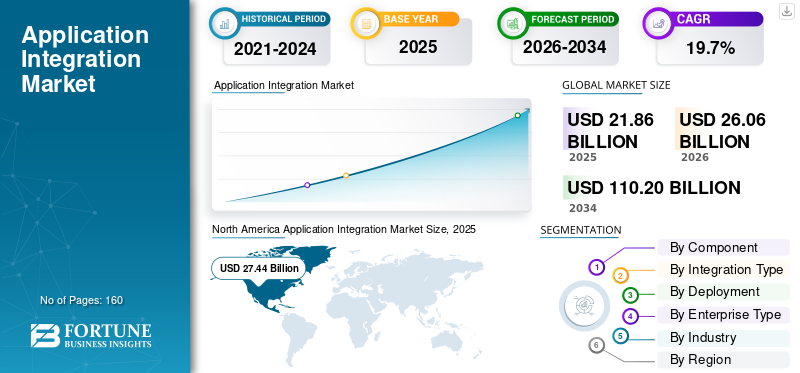

The global application integration market size was valued at USD 21.86 billion in 2025. The market is projected to grow from USD 26.06 billion in 2026 to USD 110.20 billion by 2034, exhibiting a CAGR of 19.7% during the forecast period. North America dominated the global application integration market with a market share of 34.03% in 2025.

The global application integration market comprises software and services that enable the seamless connection, coordination, and data exchange between disparate enterprise applications, systems, and databases in real time or near real time. These solutions are widely used across industries such as BFSI, IT & telecom, healthcare, retail, manufacturing, government, and others to streamline operations and enhance interoperability. The market’s growth is driven by rapid cloud adoption, accelerating digital transformation initiatives, rising demand for real time data sharing, and the need to modernize legacy integration architectures.

Boomi, LP, IBM Corporation, Informatica Inc., Microsoft Corporation, MuleSoft LLC, Oracle Corporation, SAP SE, SnapLogic Inc., Software AG, and Workato Inc. are the top players in the market.

Download Free sample to learn more about this report.

Application Integration Market KEY TAKEAWAYS

- 2025 Market Size: USD 21.86 billion

- 2026 Market Size: USD 26.06 billion

- 2034 Forecast Market Size: USD 110.20 billion

- CAGR: 19.7% from 2026–2034

- North America dominated the market with a 34.03% share in 2025.

- The Software segment accounted for the largest market share in 2025.

- API Integration is expected to register the highest CAGR during the forecast period.

North America

North America held 34.03% share in 2025.

Europe

Europe held a significant share of the global market.

Asia Pacific

Asia Pacific is expected to record the highest CAGR during the forecast period.

China

China, India, and Southeast Asia are key growth markets in Asia Pacific.

Middle East & Africa

Middle East & Africa and South America are expected to witness significant growth during the forecast period.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Need for Seamless Real Time Data Exchange Fuels Market Development

The rising need for seamless real time data exchange is becoming a critical requirement as enterprises operate across diverse and interconnected application ecosystems. Organizations increasingly depend on instant data flow to support timely decision making, improve process efficiency, and maintain operational stability. For instance,

- According to IDC, 82% of enterprises plan to adopt event driven architecture for multiple use cases within 24 months as they manage increasingly diverse data sources. This shift underscores the need for seamless, real time cloud based integration across modern applications and systems.

This requirement has strengthened with the expansion of cloud services, SaaS platforms, and digital workflows that rely on continuous data synchronization. Consequently, real time application integration capabilities are emerging as a strategic priority for businesses seeking to enhance system interoperability and overall digital performance.

MARKET RESTRAINTS

High Complexity and Cost of Integration, Along with Data Security and Privacy Concerns

High complexity and cost of integration, along with data security and privacy concerns continue to restrain broader market adoption as enterprises face challenges in connecting legacy systems with modern cloud applications. For instance,

- As per Saritasa, 62% of organizations continue relying on legacy environments that complicate hybrid integration efforts. These barriers are intensified by growing concerns around API management and maintaining secure connectivity across applications and systems.

Implementing application integration solutions often demands substantial financial investment, advanced technical expertise, and extensive customization, which can deter smaller organizations. These obstacles are compounded by heightened security and privacy risks associated with cross platform data movement and increased exposure to potential breaches. Consequently, many businesses adopt integration technologies cautiously, limiting the pace of deployment despite their long term operational benefits.

MARKET OPPORTUNITIES

Rapid Expansion of AI Driven and Low-Code Integration Platforms

The rapid expansion of AI driven and low code integration platforms represents a major opportunity for the application integration market growth, as these technologies significantly reduce the complexity traditionally associated with connecting diverse enterprise systems.

- According to industry experts, the low code and no code platforms segment is projected to grow from 20 billion dollars in 2025 to about 100 billion dollars by 2033. This surge reflects increasing investment in integration services that enhance operational efficiencies across applications and services.

These application integration platforms automate a wide range of integration tasks, allowing organizations to streamline workflows and build scalable connections with far less manual intervention. They also empower non-technical users to create and manage integrations independently, easing the pressure created by the global shortage of skilled integration specialists. As adoption increases, businesses can accelerate digital transformation initiatives, improve operational agility, and enhance overall application integration efficiency.

APPLICATION INTEGRATION MARKET TRENDS:

Growing Shift toward Event Driven and Real Time Integration Architectures

A growing shift toward event driven and real time integration architectures is emerging as a prominent trend as organizations seek faster, more responsive data flows across distributed systems. Enterprises are increasingly adopting event streaming frameworks to support low latency interactions and improve the performance of modern applications. This shift is reinforced by the rise of microservices and cloud native environments, which require continuous real time communication to operate efficiently. For instance,

- As per a global Solace survey, 85% of businesses are moving toward event driven architectures to support real time operations. This momentum reinforces the need for advanced integration tools as organizations aim to hold the largest market share in digital modernization.

As a result, event driven application integration is becoming a core component of digital infrastructure strategies aimed at enhancing agility and operational intelligence.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Component

Software Dominates Due to its Core Role in Application Connectivity

Based on component, the market is divided into software and services.

Software leads the market because enterprises primarily invest in robust integration platforms, middleware, and iPaaS solutions that act as the core layer connecting heterogeneous applications.

Services are projected to grow at the highest CAGR as organizations increasingly rely on consulting, customization, and managed integration services to address complex hybrid environments and skills gaps.

By Integration Type

A2A Integration Leads Owing to its Widespread Legacy System Use

Based on integration type, the market is divided into Application to Application (A2A), data integration, process integration, API integration, and B2B integration.

A2A integration dominates due to the large installed base of legacy and enterprise systems that require continuous point to point or hub based connectivity.

API integration is expected to record the highest CAGR as businesses rapidly modernize toward microservices, open APIs, and ecosystem connectivity for real time digital services.

By Deployment

On Premise Holds Maximum Share as Many Firms Rely on Legacy Systems

Based on deployment, the market is divided into on-premise and cloud.

On-premise deployment currently leads the market as many mission-critical integrations are still tied to legacy infrastructure, data residency requirements, and existing investments in on-site middleware.

Cloud deployment is anticipated to register the highest CAGR as organizations shift workloads to SaaS and public cloud platforms, seeking scalable, subscription-based integration solutions.

By Enterprise Type

Large Enterprises Take the Lead as They Manage Expansive and Complex IT Environments

Based on enterprise type, the market is divided into large enterprises and small & medium enterprises (SMEs).

Large enterprises dominate the market as they operate complex application landscapes across multiple regions and business units, resulting in higher integration spending.

Small and medium enterprises are expected to record the maximum CAGR as cloud based and low code integration tools lower entry barriers and make advanced capabilities affordable.

By Industry

BFSI leads as Financial Operations Rely on Secure and Interconnected Systems

By industry, the market is segmented into BFSI, IT & telecom, healthcare, retail, manufacturing, government, and others.

BFSI holds the highest market share because banks, insurers, and financial institutions depend heavily on integration to connect core banking, payment, risk management, and regulatory systems.

Healthcare is projected to register the highest CAGR as providers and payers accelerate interoperability initiatives, electronic health record connectivity, and data sharing for improved patient outcomes.

To know how our report can help streamline your business, Speak to Analyst

Application Integration Market Regional Outlook

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America Application Integration Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

North America holds the largest application integration market share as the region hosts a high concentration of large enterprises, advanced IT infrastructure, and early adopters of cloud and API based integration solutions. Strong presence of leading vendors and high digital transformation spending further reinforces its dominant position.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe holds a significant share as organizations across BFSI, manufacturing, and the public sector invest heavily in integration to meet regulatory requirements and support complex cross-border operations. Ongoing modernization of legacy systems and emphasis on data governance sustain robust demand for integration platforms.

Asia Pacific

Asia Pacific records the maximum CAGR as enterprises in China, India, and Southeast Asia rapidly adopt cloud services, SaaS applications, and digital platforms. Growing investments in IT modernization and expanding SME activity accelerate the uptake of scalable integration solutions.

Rest of The World

The Middle East & Africa and South America are expected to grow at a significant rate as governments and enterprises ramp up digital transformation programs and smart infrastructure projects. Increasing cloud adoption and rising focus on improving connectivity across financial, telecom, and public services create strong growth opportunities for integration vendors in these regions.

COMPETITIVE LANDSCAPE

Key Industry Players:

Leading Firms Execute Several Marketing Strategies to Maintain their Top Spot

Companies are introducing novel solutions to improve their market position. By catering to various customer requirements via technology, companies are striving to gain advantage. Partnerships, mergers, acquisitions, and a broad product portfolio are certain initiatives taken to cement their position.

LIST OF KEY APPLICATION INTEGRATION COMPANIES PROFILED:

- Boomi, LP (U.S.)

- IBM Corporation (U.S.)

- Informatica Inc. (U.S.)

- Microsoft Corporation (U.S.)

- MuleSoft, LLC (Salesforce) (U.S.)

- Oracle Corporation (U.S.)

- SAP SE (Germany)

- SnapLogic Inc. (U.S.)

- Software AG (Germany)

- Workato Inc. (U.S.)

- SAP SE (Germany)

KEY INDUSTRY DEVELOPMENTS:

- November 2025: New ChatGPT apps were released in preview for Business, Enterprise, and Edu users. Developers can now build interactive applications using the new Apps SDK.

- November 2025: Paytm introduced Paytm Checkin, an AI-based travel app for managing bookings across multiple transport modes. The app expands Paytm’s presence in AI-driven consumer services.

- June 2025: Launch went live after onboarding over 2,000 early adopters across more than 10 countries. The platform enables users to build full-stack, production-ready applications in minutes using AI-powered no-code tools.

- May 2025: HID launched the Integration Service to unify physical security, cybersecurity, and digital identity management. The platform simplifies complex security infrastructure management.

- April 2025: Informatica unveiled AI-powered data management enhancements within its IDMC platform. These updates aim to provide more reliable and AI-ready data across the enterprise.

REPORT COVERAGE

The global market analysis provides an in-depth study of the size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing information on market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 19.7% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component, Integration Type, Deployment, Enterprise Type, Industry, and Region |

|

ByComponent |

|

|

By Integration Type |

|

|

By Deployment |

|

|

By Enterprise Type |

|

|

By Industry |

|

|

By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 21.86 billion in 2025 and is projected to reach USD 120.20 billion by 2034.

In 2025, North America’s market value stood at USD 7.44 billion.

The market is expected to exhibit a CAGR of 19.7% during the forecast period.

The BFSI industry led the market in 2025.

Rising cloud deployment, intensifying demand for seamless data and application integration, and accelerating digital transformation initiatives are the key factors driving the market.

Boomi, LP, IBM Corporation, and Informatica Inc. are some of the prominent players in the market.

North America dominated the market in 2025 by holding the largest share.

Rising cloud adoption, growing need for seamless cross-application connectivity, and expanding digital transformation efforts are expected to drive product uptake.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us