Arc Welding Market Size, Share & Industry Analysis, By Welding Type (Gas Metal Arc Welding, Gas Tungsten Arc Welding, Shielded Metal Arc Welding, Flux-Cored Arc Welding, Plasma Arc Welding, and Submerged Arc Welding), By Equipment Type (Welding Power Sources, (Transformer-Based, and Inverter-Based), Welding Torches & Guns, Electrodes & Filler Materials, and Welding Accessories), By Automation Type (Manual, Semi-Automatic, and Automatic/Robotic), By End Use (Automotive, Building & Construction, Shipbuilding, Oil & Gas, Energy & Power, & Others), and Regional Forecast, 2026-2034

Arc Welding Market Size and Future Outlook

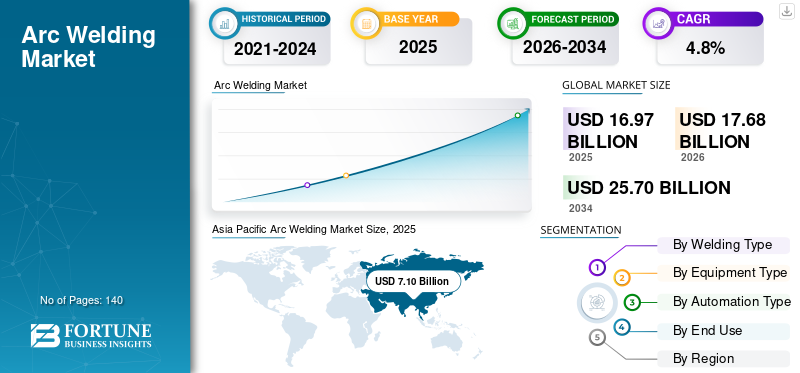

The global arc welding market size was valued at USD 16.97 billion in 2025. The market is projected to grow from USD 17.68 billion in 2026 to USD 25.70 billion by 2034, exhibiting a CAGR of 4.8% during the forecast period. Asia Pacific dominated the arc welding market with a market share of 41.83% in 2025.

Arc welding systems are critical industrial metal joining solutions used to perform high-strength fusion welding across structural steel, automotive assemblies, pipelines, heavy machinery, shipbuilding structures, and energy infrastructure components. As part of the broader global arc welding equipment industry, these systems support large scale welding operations through inverter-based, energy efficient power sources, digitally controlled welding parameters, automated wire feeding units, and advanced robotic welding system integration to ensure arc stability and repeatable weld penetration across carbon steel and high-strength alloys. The industry is witnessing steady expansion during the forecast period, supported by modernization initiatives, evolving welding technology, compliance with occupational safety and health administration standards, and quality frameworks guided by the American Welding Society, enabling manufacturers and small and medium sized enterprises to enhance productivity and strengthen overall market share.

- For instance, in October 2024, Lincoln Electric expanded its automated welding portfolio with advanced inverter-based power sources designed to support robotic GMAW applications in automotive and heavy fabrication sectors.

- In July 2024, ESAB introduced enhanced digital welding platforms integrating real-time parameter monitoring and connectivity features to improve weld traceability and operational efficiency across industrial fabrication facilities.

Lincoln Electric, ESAB Corporation, Illinois Tool Works (Miller Electric), Fronius International, and Panasonic Connect are among the key players holding a significant share of the market. Their competitive positioning is supported by integrated inverter-driven power platforms, robotic arc welding cells for automotive and structural fabrication, proprietary arc control technologies, advanced consumable portfolios, and the capability to deliver turnkey welding automation solutions across construction, transportation, energy, and heavy industrial manufacturing applications.

Download Free sample to learn more about this report.

ARC WELDING MARKET TRENDS

Shift toward Intelligent Arc Control, Real-Time Monitoring, and Robotic Integration is Transforming Arc Welding Architecture

The demand for arc welding systems is increasingly shaped by OEM requirements for consistent weld quality, parameter traceability, and real-time process validation across automotive, energy, shipbuilding, and heavy fabrication environments with stringent structural and safety compliance standards. These evolving requirements are significantly influencing overall market dynamics, as manufacturers prioritize automation, inverter-based power platforms, and data-enabled welding systems to enhance arc stability, reduce rework rates, and improve long-term joint reliability. Rather than focusing solely on deposition rate and productivity gains, leading suppliers are investing in closed-loop arc control algorithms, adaptive heat input regulation, digital waveform management, and sensor-integrated welding torches capable of capturing voltage, current, and travel speed data in real time. These capabilities support frequent production mix variability and multi-material welding applications, including high-strength steel, stainless alloys, and aluminum structures, while maintaining weld penetration consistency and minimizing distortion across structural assemblies.

- For instance, in September 2024, Fronius International expanded its intelligent inverter platform portfolio with advanced waveform control and connectivity-enabled monitoring solutions to support robotic GMAW applications in automotive body-in-white production.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of Infrastructure, Energy, and Industrial Fabrication Activities to Drive Market Growth

The market is experiencing steady expansion as large-scale infrastructure development, renewable energy installations, oil & gas pipeline projects, and industrial manufacturing modernization initiatives drive fabricators and OEMs to increase welding capacity and invest in advanced arc welding technologies. Structural steel demand across commercial construction, transportation networks, power generation facilities, and heavy machinery production continues to reinforce long-term requirements for high-strength, repeatable welding solutions. Automotive lightweighting programs and the growing adoption of high-strength steel platforms are further accelerating deployment of inverter-based Gas Metal Arc Welding (GMAW) and Flux-Cored Arc Welding (FCAW) systems capable of delivering improved arc stability, controlled heat input, and reduced post-weld rework.

- For instance, in August 2024, Lincoln Electric introduced advanced inverter-driven welding platforms engineered to support high-deposition industrial fabrication and robotic automotive production lines.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Skilled Labor Shortages to Constrain Industry Expansion

Unlike standardized mechanical joining processes, arc welding performance is highly sensitive to base metal composition, thickness variation, and thermal conductivity differences across carbon steel, stainless steel, aluminum, and high-strength alloys. Fluctuations in steel and alloy prices directly influence fabrication project economics, often delaying capital expenditure on new welding power sources and robotic integration systems. Additionally, welding quality remains operator-dependent in manual and semi-automatic applications, and persistent shortages of certified welders across North America and Europe are limiting throughput expansion in construction, shipbuilding, and heavy equipment manufacturing sectors. Differences in Welding Procedure Specifications (WPS), inspection requirements, and project-level qualification standards further increase setup time and integration complexity for large industrial projects. For equipment suppliers, demand variability tied to commodity cycles, infrastructure funding approvals, and energy project timelines can delay order conversions and restrict rapid scaling of production capacity, even during periods of underlying structural demand growth.

MARKET OPPORTUNITIES

Industrial Automation Modernization and Energy Transition Projects Creating New Demand for Advanced Arc Welding Systems

An emerging opportunity in the arc welding market growth is being driven by industrial automation upgrades and the global energy transition toward renewable power generation, electric mobility, and grid modernization. Manufacturers are increasingly investing in Robotic Gas Metal Arc Welding (GMAW) and inverter-based Flux-Cored Arc Welding (FCAW) systems capable of delivering higher deposition rates, reduced spatter, and digitally monitored weld consistency across wind turbine towers, battery enclosures, electric vehicle chassis, and hydrogen infrastructure components. This shift is expanding demand for welding platforms that integrate adaptive arc control, seam-tracking sensors, and real-time parameter monitoring to improve productivity and minimize rework in high-volume fabrication environments. Suppliers that can deliver energy-efficient inverter technologies, automated welding cells, and application-specific consumables tailored for high-strength steels and lightweight alloys are well positioned to capture incremental demand across automotive electrification, renewable energy structures, and next-generation transportation manufacturing programs.

- For instance, in July 2024, ESAB expanded its digital welding ecosystem with enhanced inverter-based power sources and connectivity-enabled monitoring tools to support automated fabrication lines in renewable energy and electric vehicle component manufacturing facilities.

MARKET CHALLENGES

Compliance with Multi-Industry Quality Standards and Process Qualification Requirements to Add Operational Complexity

Arc welding suppliers face ongoing challenges associated with diverse qualification, inspection, and documentation requirements across automotive, energy, shipbuilding, and heavy industrial manufacturing programs. Welding systems must comply with industry-specific standards such as ISO welding procedure qualifications, pressure vessel codes, pipeline welding certifications, and customer-defined process validation protocols, often requiring customized parameter calibration, consumable testing, and weld performance verification. Variations in joint design, material grades, thickness ranges, and inspection criteria limit full standardization of welding solutions and increase engineering and commissioning time for new production lines.

Segmentation Analysis

By Welding Type

Gas Metal Arc Welding (GMAW / MIG) Segment Led as it Serves as the Primary Production Welding Process across Automotive and Industrial Fabrication Lines

By welding type, the market is segmented into Gas Metal Arc Welding (GMAW / MIG), Gas Tungsten Arc Welding (GTAW / TIG), Shielded Metal Arc Welding (SMAW), Flux-Cored Arc Welding (FCAW), Plasma Arc Welding (PAW), and Submerged Arc Welding (SAW).

Gas Metal Arc Welding (GMAW / MIG) held the largest arc welding market share as it serves as the core production welding process across high-volume automotive manufacturing, structural steel fabrication, transportation equipment assembly, and general industrial applications. Its compatibility with robotic automation platforms, continuous wire feeding capability, stable arc characteristics, and suitability for welding carbon steel, stainless steel, and aluminum components make it the preferred choice for manufacturers seeking productivity, repeatability, and reduced post-weld finishing requirements. As industrial facilities increasingly prioritize automated body-in-white assembly lines, modular fabrication cells, and inverter-based digital power sources, GMAW systems are becoming a strategic investment focus for manufacturers aiming to enhance throughput efficiency while maintaining weld consistency and cost competitiveness across mass production environments.

- For instance, in August 2024, Lincoln Electric expanded its advanced inverter-driven GMAW platform portfolio to support robotic automotive welding lines, while in June 2024, Fronius International enhanced its intelligent MIG welding systems with adaptive arc control features designed for high-speed industrial fabrication applications across Europe and North America.

Flux-Cored Arc Welding (FCAW) is projected to grow at the highest CAGR of 5.6% during the forecast period, driven by rising demand in heavy structural fabrication, shipbuilding, offshore energy platforms, and large-diameter pipeline construction projects. FCAW offers higher deposition rates, improved penetration in thick materials, and better performance in outdoor and wind-prone environments compared to conventional solid-wire processes.

To know how our report can help streamline your business, Speak to Analyst

By Equipment Type

Electrodes & Filler Materials Segment Led Due to Their Recurring Consumption across High-Volume Industrial Fabrication Activities

By equipment type, the market is segmented into welding power sources, welding torches & guns, electrodes & filler materials, and welding accessories.

Electrodes & filler materials held the largest share of the market, driven by their continuous consumption across automotive manufacturing, structural steel fabrication, shipbuilding, pipeline construction, and heavy machinery production. Unlike capital-intensive welding power sources, consumables require periodic replenishment based on deposition rates, material thickness, and production intensity, resulting in stable and recurring revenue streams. Demand for solid wires, flux-cored wires, stick electrodes, and specialty alloy consumables remains closely linked to infrastructure expansion, industrial output, and energy project execution. As fabrication volumes increase across Asia Pacific and the Middle East, and as manufacturers adopt higher-strength steels and corrosion-resistant alloys, the need for application-specific filler materials with controlled chemistry and enhanced weld integrity continues to reinforce the segment’s dominant market position.

Welding power sources are expected to register the highest growth rate in the market during the study period, expanding at a CAGR of 5.3%, supported by rising adoption of inverter-based technologies and robotic arc welding systems. Manufacturers are increasingly transitioning from conventional transformer platforms to energy-efficient digital power sources equipped with waveform control, arc stability optimization, and real-time parameter monitoring capabilities.

By Automation Type

Semi-Automatic Segment Led Due to Its Extensive Use across Construction, Fabrication, and Industrial Manufacturing Activities

By automation type, the market is segmented into manual, semi-automatic, and automatic/robotic systems.

Semi-automatic systems held the largest share of the market, driven by their widespread adoption across structural steel fabrication, building & construction projects, shipyards, pipeline welding, and medium-scale manufacturing facilities. These systems typically combine inverter-based power sources with continuous wire feeding mechanisms, allowing operators to control torch movement while maintaining stable arc performance and higher deposition rates compared to manual stick welding. Their balance between productivity improvement and capital affordability makes them particularly suitable for contractors, fabrication workshops, and infrastructure projects where flexibility, mobility, and cost efficiency are critical.

Automatic/robotic systems are expected to register the highest growth rate in the market during the study period, expanding at a CAGR of 6.0%, supported by rising labor cost pressures, growing adoption of Industry 4.0 practices, and increasing automotive and heavy equipment production automation. Robotic GMAW cells integrated with seam-tracking sensors, adaptive arc control, and real-time parameter monitoring are gaining traction in high-volume manufacturing environments where repeatability, weld consistency, and take-time optimization are essential.

By End Use

Extensive Deployment across Structural Steel and Infrastructure Projects Led to Building & Construction Segmental Dominance

Based on end use, the market is segmented into automotive, building & construction, shipbuilding, oil & gas, energy & power, heavy machinery & equipment, general fabrication, railways, and aerospace & defense.

Building & construction accounts for the highest share of the market, driven by extensive use of welding processes across commercial buildings, industrial facilities, bridges, transportation infrastructure, and large-scale structural steel frameworks. Structural fabrication activities require high deposition welding for beams, columns, reinforcement structures, and prefabricated modules, making semi-automatic GMAW, SMAW, and FCAW systems critical to daily project execution. Construction environments demand flexible, field-deployable welding equipment capable of operating across variable material thicknesses and outdoor conditions.

The energy & power segment is expected to register a significant growth rate during the study period, expanding at a CAGR of 5.3%, supported by investments in renewable energy infrastructure, grid expansion projects, hydrogen facilities, and power generation upgrades. Fabrication of wind turbine towers, transmission structures, pressure vessels, and energy storage systems requires high-strength weld integrity and process consistency, increasing demand for advanced inverter-based power sources and high-deposition welding consumables.

Arc Welding Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Arc Welding Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific remains the fastest-growing market, revenue valued at USD 7.10 billion in 2025 globally. Market expansion is driven by infrastructure construction, automotive manufacturing growth, shipbuilding output, and energy project development across major economies. China’s demand is closely tied to structural steel fabrication, renewable energy tower production, and large-scale industrial manufacturing. Japan’s market is supported by advanced automotive assembly lines and high robotic gas metal arc welding adoption. South Korea, India, and ASEAN countries are emerging contributors as governments promote manufacturing localization and industrial modernization initiatives.

China Arc Welding Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated at around USD 3.48 billion, representing roughly 19.7% of global sales.

Japan Arc Welding Market

The Japan market in 2026 is estimated at around USD 0.77 billion, accounting for roughly 4.4% of the global sales.

India Arc Welding Market

The Indian market in 2026 is estimated at around USD 1.06 billion, accounting for roughly 6.0% of global sales.

North America

The North America market accounted for over USD 3.78 billion in revenue in 2025, supported by a diversified industrial manufacturing base spanning automotive production, structural steel fabrication, energy infrastructure development, and heavy equipment manufacturing across the U.S., Canada, and Mexico. Regional demand is structurally tied to large-scale building & construction activity, pipeline welding operations, renewable energy installations, and automated automotive body-in-white assembly lines that rely extensively on semi-automatic and robotic GMAW systems. Manufacturing facilities across the region increasingly deploy inverter-based power sources integrated with robotic manipulators and real-time parameter monitoring platforms to enhance weld repeatability and reduce rework rates. In addition, a substantial installed base of legacy transformer welding equipment is undergoing gradual replacement with digitally controlled systems featuring adaptive arc control and connectivity-enabled diagnostics.

U.S. Arc Welding Market

The U.S. is expected to dominate the regional market with an estimated revenue of about USD 3.04 billion in 2026, driven by its concentration of automotive manufacturing plants, structural steel fabrication hubs, shipbuilding yards, and defense equipment production facilities. Unlike smaller regional markets, U.S. industrial operations span full-scale production environments requiring synchronized welding automation across chassis assembly, heavy machinery frames, pressure vessels, and energy infrastructure components. Robotic GMAW cells operating within automotive and transportation manufacturing plants form a critical backbone of high-volume welding activity, while semi-automatic and FCAW systems remain widely deployed across construction and pipeline projects. Continuous investments in automation upgrades, inverter-based power platforms, and welding data traceability systems are reinforcing modernization of existing fabrication infrastructure.

Europe

The Europe market is supported by a diversified and industrially mature manufacturing structure spanning automotive production, structural steel fabrication, shipbuilding, rail equipment manufacturing, and energy infrastructure development. Demand for arc welding solutions is closely tied to automotive assembly plants in Germany and Spain, industrial machinery production in Italy, offshore and shipbuilding activities in the Nordics, and energy and transportation infrastructure upgrades across France and Eastern Europe. Unlike highly centralized industrial regions, Europe’s cross-border manufacturing ecosystem requires flexible welding platforms capable of serving distributed fabrication facilities and modular production environments. Stringent quality standards, environmental regulations, and energy-efficiency mandates are accelerating the transition toward inverter-based welding power sources and digitally controlled arc systems with enhanced parameter monitoring and reduced power consumption. Germany, France, Italy, Spain, and the BENELUX region lead regional adoption, supported by strong automotive clusters, advanced industrial automation capabilities, and export-oriented heavy manufacturing programs that reinforce steady demand for high-productivity arc welding technologies.

U.K. Arc Welding Market

The U.K. market in 2026 is estimated at around USD 0.50 billion, representing roughly 2.8% of global sales.

Germany Arc Welding Market

Germany’s market is projected to reach approximately USD 1.08 billion in 2026, equivalent to around 6.1% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by infrastructure megaprojects, oil & gas pipeline development, power generation investments, and gradual industrial diversification initiatives across the GCC and North Africa. Government-backed capital expenditure in energy transmission networks, petrochemical facilities, and structural construction is supporting demand for semi-automatic and submerged arc welding systems used in heavy fabrication and pipeline assembly. The GCC benefits from high-value energy and industrial projects requiring high-deposition welding solutions, while North Africa is witnessing expanding construction and manufacturing activity aligned with export-oriented industrial growth. Across parts of Sub-Saharan Africa, improving industrial capability is encouraging incremental adoption of inverter-based and semi-automatic welding systems.

GCC Arc Welding Market

The GCC market is projected to reach around USD 0.50 billion in 2026, representing roughly 2.8% of the global sales.

South America

The South America arc welding market is supported by expanding infrastructure development, mining activity, automotive production, and energy-related industrial fabrication, particularly in Brazil and Argentina. Brazil represents the primary demand center, driven by structural steel construction, heavy machinery manufacturing, shipbuilding, and oil & gas pipeline projects that rely on semi-automatic and flux-cored arc welding systems. While overall industrial output remains lower than North America and Europe, export-oriented manufacturing and mining equipment fabrication are encouraging steady investment in inverter-based welding power sources and high-deposition consumables. Argentina and select regional economies are gradually modernizing fabrication capabilities to improve weld consistency, enhance productivity, and align with international industrial quality standards.

Brazil Arc Welding Market

The Brazil market is projected to reach around USD 0.60 billion in 2026, representing roughly 3.4% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Advantage Driven by Technological Differentiation, Automation Capability, and Global Distribution to Strengthen Market Position

The arc welding market is moderately consolidated, with competitive positioning shaped less by overall portfolio width and more by technological differentiation, automation integration capability, consumable expertise, and long-term relationships with industrial OEMs and fabrication contractors. Leading players such as Lincoln Electric, ESAB Corporation, Illinois Tool Works (Miller Electric), Fronius International, and Panasonic Connect maintain strong market positions by delivering advanced inverter-based power sources, robotic arc welding cells, and application-specific consumable solutions tailored to automotive, energy, shipbuilding, and heavy fabrication environments. Their competitive strength is reinforced by proprietary arc control technologies, global service networks, and integrated automation capabilities that ensure weld consistency, productivity optimization, and operational reliability across high-volume manufacturing operations.

Competitive differentiation is increasingly driven by a supplier’s ability to support robotic integration, provide digitally connected welding platforms with real-time parameter monitoring, and deliver high-performance filler materials optimized for advanced alloys and high-strength steels rather than by equipment scale alone. As manufacturers prioritize automation, energy efficiency, and weld quality traceability, arc welding leaders are strengthening software integration, regional manufacturing footprints, and aftermarket consumable supply chains to protect installed-base positions and elevate switching barriers for new entrants.

- For instance, in February 2025, Lincoln Electric expanded its advanced robotic welding automation solutions to support high-volume automotive and structural fabrication applications.

- Similarly, in April 2025, ESAB enhanced its digital inverter welding platforms with connectivity-enabled monitoring features designed to improve process control and production efficiency across industrial manufacturing facilities.

LIST OF KEY ARC WELDING COMPANIES PROFILED IN REPORT

- Lincoln Electric Holdings, Inc. (U.S.)

- ESAB Corporation (U.S.)

- Illinois Tool Works Inc. (U.S.)

- Fronius International GmbH (Austria)

- Panasonic Connect Co., Ltd. (Japan)

- Kemppi Oy (Finland)

- Kobe Steel, Ltd. (Japan)

- Daihen Corporation (Japan)

- The Linde Group (U.K.)

- Air Liquide (France)

KEY INDUSTRY DEVELOPMENTS

- June 2025: ESAB Corporation signed a definitive agreement to acquire EWM GmbH, a German producer of heavy industrial welding equipment and automation systems, significantly expanding ESAB’s global equipment capabilities and welding automation footprint.

- February 2025: Lincoln Electric launched the Ranger® Air 330MPX multi-function engine drive, a versatile welder incorporating Stick, TIG, MIG, and flux-cored arc welding capabilities with integrated air compressor and power generation features enhancing on-site welding productivity for industrial and construction applications.

- October 2025: Lincoln Electric reported strong Q3 2025 sales growth, driven in part by increased demand for welding consumables and industrial automation solutions in structural fabrication and energy sectors.

- September 2025: A new submerged arc welding machine was inaugurated at BHEL’s Trichy complex to improve welding productivity and support delivery of power plant components, reflecting investment in heavy fabrication welding solutions in India.

- August 2025: Miller Electric Mfg. announced its latest lineup of welding and safety innovations at FABTECH 2025 in Chicago, featuring new high-efficiency welding consumables and air quality solutions aimed at improving operator safety and productivity in industrial welding environments.

REPORT COVERAGE

The global arc welding market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Welding Type, Equipment Type, Automation Type, End Use, and Region |

| By Welding Type |

|

| By Equipment Type |

|

| By Automation Type |

|

| By End Use |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value to stand at USD 17.68 billion in 2026 and is projected to reach USD 25.70 billion by 2034.

In 2025, the North Americas market value stood at USD 3.78 billion.

The market is expected to exhibit a CAGR of 4.8% during the forecast period (2026-2034).

By end-use industry, the building & construction segment leads the market.

Rising infrastructure development, expanding automotive production, growing energy & power investments, and increasing adoption of welding automation technologies are key factors driving the arc welding market.

Lincoln Electric Holdings, Inc., ESAB Corporation, Illinois Tool Works Inc., Fronius International GmbH, Panasonic Connect Co., Ltd. are the top players in the market.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us