Stainless Steel Market Size, Share & Industry Analysis, By Type (Cold Rolled Flat, Hot Plate & Sheet, Cold Bars & Wire, Hot Bars & Wire Rod, and Others), By Application (Metal Products, Electrical Machinery, Engineering, Construction, Automotive Parts, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

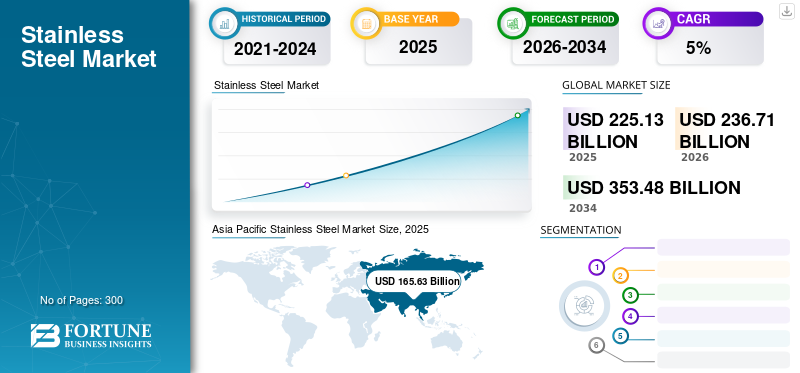

The global stainless steel market size was valued at USD 225.13 billion in 2025 and is projected to grow from USD 236.71 billion in 2026 to USD 353.48 billion by 2034, exhibiting a CAGR of 5.0% during the forecast period. Asia Pacific dominated the stainless steel market with a market share of 73.60% in 2025.

Stainless steel consists of several components that fuse to form a strong alloy. This alloy includes chromium, nitrogen, and molybdenum. Furthermore, this product is environmentally friendly, strong, corrosion-resistant, a neutral alloy, long-lasting, and infinitely recyclable. These properties make steel the perfect choice for several industries, including construction, automotive, and electronics. The rapidly growing automotive industry is driving demand for the product. Furthermore, the corrosion resistance of this recyclable material and increased manufacturing will propel market growth during the forecast period.

The Covid-19 pandemic initially disrupted the market, causing supply chain disruptions and reduced demand from key industries. However, as the global economy recovered, demand for the product rebounded significantly. The resumption of increased construction activity, infrastructure projects, and manufacturing contributed to market recovery and indicated a positive outlook.

Download Free sample to learn more about this report.

Global Stainless Steel Market Overview

Market Size and Forecast:

- 2025 Market Size: $225.13 billion

- 2026 Market Size: $236.71 billion

- 2034 Forecast Market Size: $353.48 billion

- CAGR: 5.0% from 2026 to 2034

Market Share:

- The Asia-Pacific region dominated the stainless steel market with a 73.60% share in 2025. This was driven by rapid infrastructure development, increased steel production, and heightened R&D efforts, particularly in China, the region's largest and fastest-growing market.

- By type, cold-rolled flat steel held the largest share, attributed to its high ductility, excellent surface finish, and wide range of applications in home appliances, furniture, and lockers.

- By application, metal products led in 2023 due to increased usage in metal and medical accessories. However, the construction segment is expected to grow at the fastest CAGR, particularly in urban and impact-resistant structural projects, owing to stainless steel's corrosion resistance and strength.

Key Country Highlights:

- United States: Projected to reach $20.644 billion by 2032, driven by demand for duplex stainless steel in engineering and electronics, supported by cost-effectiveness and resilience.

- China: Continued leadership in global cement consumption and production (projected to reach $13 trillion by 2030), driven by the Belt and Road Initiative and massive domestic construction investment.

- Japan: Rising demand for stainless steel in the automotive and electronics industries, supported by high technology adoption.

- Europe: Market growth is driven by advanced applications in the automotive industry, including exhaust systems, and innovative design practices such as tube hydroforming using austenitic steel.

Stainless Steel Market Trends

Increased technological development in steel production due to rising CO2 emission rates is a notable trend

Growing technological advancements for producing sustainable stainless steel are driving market growth during the forecast period. Key factors propelling the market include megatrends such as increasing urbanization, population and economic development, mobility, and rising climate change concerns. Furthermore, rising CO2 emissions have prompted many steel producers to develop sustainable alternatives that are durable and recyclable at the end of their lifecycle. For instance, in December 2021, Aperam acquired ELG, a specialist in superalloys and steel recycling. This acquisition aimed to support both companies' CO2 reduction targets and improve their environmental footprint. Therefore, such factors, coupled with increasing consumer preference for steel-based products, are expected to drive significant market growth.

Increased Government Focus on Infrastructure Development

Demand for stainless steel is rising as the real estate and infrastructure sectors seek lightweight yet durable and robust new-generation materials. Infrastructure development projects undertaken by governments in developing countries like China and India have the potential to generate substantial product demand. Infrastructure development is a critical focus for many developing nations, as it is a key driver of economic growth and social development. Countries are investing in various projects, such as transportation, energy, and communications infrastructure, to support growing populations and industries.

According to the World Resources Institute, China is projected to invest nearly $13 trillion in its building and construction sector by 2030, accounting for up to 20% of global construction investment. This high level of investment in the country's building and construction sector presents significant opportunities for the market in the near future.

Download Free sample to learn more about this report.

Growth Factors for the Stainless Steel Market

The Metal's Versatile Properties Driving Market Expansion

Manufacturing serves as a crucial driver for the market, leveraging the metal's versatile properties to meet diverse industrial needs. Stainless steel's corrosion resistance and durability make it ideal for manufacturing machinery and equipment. Manufacturers utilize this steel for components like pumps, storage tanks, and valves to ensure durability and resilience in demanding operational conditions. This demand is intensifying in industries such as chemicals, oil and gas, and food. In these industries, resistance to corrosion is vital for maintaining operational efficiency.

The manufacturing buildings and infrastructure segment makes a significant contribution to the market. Stainless steel's structural strength, aesthetic appeal, and resilience to environmental factors make it an excellent material for constructing components, bridges, and architectural elements. Modern urban infrastructure projects, including skyscrapers and bridges, often rely on stainless steel to ensure structural integrity and longevity.

Rapid Growth in the Automotive Industry Drives Product Adoption

The rapid growth of the automotive industry is driving product consumption. The metal's corrosion resistance, high strength, and heat resistance make it ideal for various automotive components, such as seatbelt springs and hose clamps. According to the World Steel Organization, stainless steel will become common in suspensions, chassis, fuel tanks, bodywork, and catalytic converters in the future. Furthermore, increased technological advancements and rising innovation in the automotive industry Electric Vehicles products. Consequently, rising product demand from automakers will drive the stainless steel market's growth.

Restraints

Availability of alternative products such as aluminum and carbon steel impacting market growth

The availability of alternative products such as aluminum, carbon steel, galvanized steel, and engineered plastics, inhibits product adoption. Furthermore, compared to these alternatives, it is heavy and not water-resistant. These factors limit consumption where lightweight properties are essential. Such factors can suppress market growth and reduce product adoption across various sectors including electronics, engineering, and consumer goods.

Stainless Steel Market Segmentation Analysis

By Type Analysis

The cold-rolled flat segment holds the largest share due to its superior physical properties

On the basis of type, the market is segmented into cold rolled flat, hot plate & sheet, cold bars & wire, hot bars & wire rod, and others.

The Colled Rolled Flat segment is expected to account for 46.20% of the market in 2026. The cold rolled flat segment accounts for the largest share and witnesses the fastest growth in the global market. Cold rolled flat, abbreviated as CRS, is a highly ductile material ideal for applications that require precision. The product offers exceptional properties such as high strength, durability, and excellent surface finish. Therefore, it is highly utilized in home appliances, lockers, file cabinets, and furniture. The segment is expected to record a CAGR of 5.4% during the forecast period.

Hot plate & sheet is also referred to as structural steel and is projected to be the second-largest segment in the market. The segment is likely to hold 36% of the market share in 2025. This type of steel could be cut and welded to manufacture more complicated products. It is mainly used in drums, containers, automobile panels, general fabrication, and trailer cladding.

Increasing demand for cold bars & wire in engineering applications due to their excellent mechanical properties, will propel the segment growth. Hot bars & wire rods, also called annealed bars and normalized bars, are gaining rapid traction in the electrical & electronics industry owing to their excellent tensile strength.

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Metal products lead due to increased adoption in cookware and medical accessories

On the basis of application, the market is divided into metal products, electrical machinery, engineering, construction, automotive parts, and others.

The Metal Products segment is anticipated to hold a dominant market share of 34.71% in 2026. The metal products segment held the highest stainless steel market share. Growing consumer disposable income and rising adoption of metals in utensils and medical accessories, driving high demand and contributing to overall market growth during the study period.

Engineering steel products generally include exhaust systems, ship containers, cable trays, and pipelines. Increasing demand for oil & gas and transportation products will boost growth in the segment.

The construction segment is growing at the highest CAGR in the market. The segment led the market share by 13% in 2024. Stainless steel products are utilized in modern construction due to their great strength and corrosion resistance. It is also used in modern construction, including exterior cladding for large structures and high-impact structures, and can be found in interior applications such as countertops, backsplashes, and railings. In motor vehicle parts, product demand is rising owing to rapid innovation in the automotive industry coupled with increasing consumer expenditure. Steel is a reliable, versatile solution, which makes it an ideal choice in electrical machinery. In the electronic industry, stainless steel, particularly grades, such as type 316 S and 304 SS is highly adopted due to its excellent properties.

Regional Insights

Based on geography, the market is studied across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific Stainless Steel Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The Asia Pacific market generated USD 165.63 billion in 2025, representing 73.60% of the global market landscape, and is expected to reach USD 175.04 billion in 2026. The rapid infrastructure development and increasing technological advancement in steel have fueled market growth in Asia Pacific. China holds the highest market share in this region and is the fastest-growing country. The increasing production of steel, rising research & development activities, and the growing construction industry are some prominent factors fueling product demand in China. The market in China is likely to be USD 117.6 billion in 2025. On the other hand, Japan is likely to hit USD 11.14 billion and India is projected to reach USD 14.66 billion in 2025.

[kwilcokq5v]

Europe

In 2025, Europe represented USD 33.65 billion, accounting for 14.90% of the worldwide market, and is projected to grow to USD 34.71 billion in 2026. In Europe, the high demand for the product is associated with rapid growth in the automotive industry and technological advancements. Around 45%-50% of steel is used in automotive exhaust systems. In addition, several firms are employing innovative processes for complex designs, including tube hydroforming with austenitic steel. Hence, such factors will fuel market growth in Europe. The Italy market size is likely to hit USD 14.87 billion in 2025, while Germany is projected to hold USD 4.14 billion and France is expected to hit USD 2.87 billion in 2025.

North America

North America recorded a market size of USD 19.24 billion in 2025, capturing 8.50% of the global market share, and is projected to reach USD 20.04 billion in 2026. In North America, market growth is majorly attributed to the increasing demand for duplex series of steel in electronic and engineering applications, owing to its cost-effective property. The U.S. market size is estimated to be USD 15.44 billion in 2025.

Latin America and Middle East & Africa

In 2025, Latin America held 1.70% of the global market, reaching a valuation of USD 3.92 billion, and is projected to grow to USD 4.09 billion in 2026. In Latin America, Brazil and Mexico are the leading countries. The rising consumption of metal products in the medical and transportation industries will boost market growth in this region.

Middle East & Africa accounted for USD 2.69 billion in 2025, representing 1.20% of the global market share, and is projected to reach USD 2.81 billion in 2026. The expansion of production capacities and industrial facilities by various firms is expected to increase construction activities in the Middle East & Africa. The growing construction industry in the Middle East and Africa is anticipated to surge market growth significantly. The Saudi Arabia is expected to be USD 1.95 billion in 2025.

Key Industry Players

Key players maintain their positions using acquisition and product innovation strategies

The market is consolidated and competitive. Major global players such as ArcelorMittal S.A., Nippon Steel Corporation, Posco, Outokumpu Oyj, and Acerinox S.A. are investing heavily in advancing technologies to enhance product output. Market leaders are using superior operational efficiency and innovative technological development as growth strategies. Furthermore, market players are focusing on acquisitions and expansion efforts to strengthen their market share.

Top List of Stainless Steel Companies:

- Acerinox S.A (Spain)

- Aperam S.A. (Luxembourg)

- ArcelorMittal S.A. (Luxembourg)

- Baosteel Group Corporation (China)

- Jindal Stainless Group (India)

- Nippon Steel Corporation (Japan)

- Outokumpu Oyj (Finland)

- POSCO (South Korea)

- Acciai Speciali Terni S.P.A (Italy)

- Yieh Corporation (Taiwan)

Key Industry Developments:

- February 2024 - Acerinox signed an agreement to acquire Haynes International. The acquired company is a major U.S. developer, manufacturer, and marketer of technologically advanced high-performance alloys. This acquisition strengthens Acerinox's position in the high-performance alloy segment.

- June 2023 - Outokumpu partnered with Nordic Steel to introduce sustainable stainless steel to Norway. Outokumpu's Circle Green is the world's most sustainable stainless steel, with carbon dioxide emissions up to 92% lower than the industry average. This agreement advances both companies' environmental strategies and enables Nordic Steel to be the first in Norway to offer these solutions to customers.

- March 2023 - A Memorandum of Understanding (MOU) was signed between Outokumpu and Fortum to explore decarbonizing Outokumpu's steel production through the development of Small Modular Reactors (SMRs). This agreement enabled the company to access the potential for SMR construction in Finland.

- May 2022 - Jindal Stainless became a supplier to Alstom for developing a technically advanced, state-of-the-art train for the region's rapid transit system. Jindal Stainless will supply Alstom with approximately 2 kilotons of 301LN stainless steel grade with a 2J finish to build 210 train sets. Several components are being developed using this steel, including sidewall skins, brackets, end walls, sole bars, cost rails, roofs, and underframes.

- December 2021 - Aperam acquired Elg, a recycler of stainless steel and superalloys, at an enterprise value of $358.3 million. This acquisition strengthened the company's leadership position in environmental, social, and governance (ESG) within the industry. It improved the input mix, expanded raw material supply, and supported the company's CO₂ reduction goals.

Report Highlights

This report provides a detailed analysis of the market, focusing on key aspects such as major companies, types, and applications. It also covers quantitative data in terms of volume and value, market data research methodology, and insights into market dynamics and trends. The report highlights significant industry developments and the competitive landscape. In addition to the above factors, this report includes various market growth drivers in recent years.

[3uphzxscyx]

Report Scope and Segmentation

|

Attributes |

Details |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR 5.0% from 2026 to 2034 |

|

Unit |

Value (USD billion), Volume (kilotons) |

|

Segmentation |

By Type

|

|

By application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global size was USD 225.13 billion in 2025 and is projected to reach USD 353.48 billion by 2034.

The market will exhibit a CAGR of 5.0% over the forecast period of 2026-2034.

By application, the metal products segment led the market in 2025.

The increasing demand from automotive and construction industry is the key factor driving market growth.

Nippon Steel Corporation, Outokumpu Oyj, ArcelorMittal, and Acerinox S.A are the leading players in the market.

- 2021-2034

- 2025

- 2021-2024

- 300

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us