Architectural Lighting Market Size, Share & Application Analysis, By Product Type (LED Lighting, Fluorescent Lighting, Incandescent Lighting, Halogen Lighting, Smart Lighting, and Others), By Technology (Wired and Wireless), By Installation Type (New Installation and Retrofit Installation), By Application (Indoor Lighting, Outdoor Lighting, Architectural Lighting, Decorative Lighting, and Others), By End-user (Residential, Commercial, Industrial, Institutional, Hospitality, and Others), and Regional Forecast, 2026 - 2034

KEY MARKET INSIGHTS

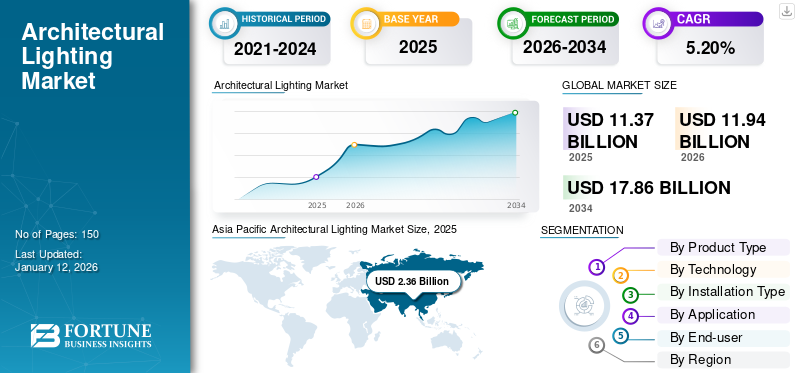

The global architectural lighting market size was valued at USD 11.37 billion in 2025. The market is projected to grow from USD 11.94 billion in 2026 to USD 17.86 billion by 2034, exhibiting a CAGR of 5.20% during the forecast period. Asia Pacific dominated the global architectural lighting market with a share of 24.90% in 2025.

The architectural lighting industry includes designing, producing, and deploying lighting systems that enhance buildings and spaces' aesthetic and functional characteristics. It includes a wide range of products used across residential, commercial, industrial, institutional, hospitality, and other environments. Key drivers of the market include growing demand for energy-efficient solutions, increased adoption of led lighting, and rising focus on creatively integrated building designs.

The COVID-19 pandemic led to temporary disruptions in the market due to supply chain issues and project delays. However, the crisis also accelerated the shift from traditional lighting solutions to smart and contactless lighting solutions, driven by increased concerns around health, safety, and automation.

Key players in the market include Signify Holding, OSRAM GmbH, Cree Lighting, Cooper Lighting LLC, Lutron Electronics, Hubbell, ERCO Lighting, Zumtobel Group, TRILUX Lighting Ltd., Fagerhult, and Acuity Inc.

Download Free sample to learn more about this report.

ARCHITECTURAL LIGHTING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 11.37 billion

- 2026 Market Size: USD 11.94 billion

- 2034 Forecast Market Size: USD 17.86 billion

- CAGR: 5.20% from 2026–2034

- Asia Pacific dominated the global architectural lighting market with a share of 24.90% in 2025.

- The LED lighting segment is expected to account for 38.16% of the market in 2026.

- The wireless segment is anticipated to hold a dominant market share of 52.54% in 2026.

North America

The North America market was valued at USD 3.31 billion in 2025, capturing 34.90% of global revenue, and is estimated to reach USD 3.45 billion in 2026.

Europe

In 2025, Europe held 24.90% of the global market, reaching a valuation of USD 2.36 billion, and is projected to grow to USD 2.49 billion in 2026.

Asia Pacific

The market in Asia Pacific reached USD 2.36 billion in 2025, representing 24.90% of total market revenue, and is projected to reach USD 2.49 billion in 2026.

U.S.

The U.S. market is projected to reach USD 2.01 billion by 2026.

Japan

The Japan market is projected to reach USD 0.57 billion by 2026.

Read More

IMPACT OF ARTIFICIAL INTELLIGENCE (AI)

Artificial intelligence (AI) is transforming the market by facilitating advanced lighting systems that adjust based on user behavior and environmental conditions. AI enhances energy efficiency and user experience through functionalities such as automated lighting controls, occupancy detection, and daylight integration. For instance,

- A recent study by IBM revealed that 74% of companies in the energy and utility sector are adopting AI to address data-related challenges. This adoption is expected to enhance operational efficiency and reduce environmental impact.

These capabilities support the increasing demand for architectural lighting. The rapid integration of AI is expected to drive product innovation, improve operational efficiency, and deliver higher value across the industry.

IMPACT OF RECIPROCAL TARIFFS

Reciprocal tariffs have notably impacted the market by increasing the cost of imported raw materials and finished lighting products. For instance,

- The imposition of U.S. tariffs on imported components is projected to raise production costs by approximately 4 to 6%, with notable implications for the consumer electronics segments.

These tariffs have disrupted global supply chains, leading to long lead times and higher production costs for manufacturers. As a response, many companies are re-evaluating their sourcing strategies and discovering local or regional supply options to mitigate risk. Thus, these increased costs are passed on to end users, possibly affecting project budgets and slowing market growth in certain regions.

ARCHITECTURAL LIGHTING MARKET TRENDS

Soaring Need for Energy-efficient and Sustainable Lighting Drives Market Growth

The increasing demand for energy-efficient and sustainable lighting solutions drives the market. Rising environmental concerns and the tightening of energy regulations encourage architects and developers to prioritize lighting systems that reduce energy consumption and carbon emissions. Light Emitting Diode (LED) technologies, smart lighting controls, and daylight integration have become essential tools in achieving these sustainability objectives. For instance,

- In September 2024, according to the International Energy Agency, buildings account for 30% of global energy consumption and 25% of greenhouse gas emissions. Implementing smart technologies can reduce office energy use by up to 70%, supporting Architecture, Engineering, Construction, and Operations (AECO) professionals in achieving cost-efficiency and sustainability objectives.

In addition to regulatory compliance, energy-efficient lighting supports long-term cost savings and improves building performance, making it a smart choice for commercial and residential projects. Furthermore, green building certification programs, such as LEED and BREEAM, are increasingly influencing the adoption of sustainable lighting practices. This growing focus on sustainability is also driving product innovation and shaping purchasing decisions across the market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Smart Lighting Integration with Building Automation Systems Leads the Market

Integrating smart lighting systems with building automation technologies fuels the architectural lighting market growth. These systems allow centralized control, real-time monitoring, and automated lighting adjustment based on occupancy, daylight levels, and user preferences. This integration improves energy efficiency, user comfort, and operational flexibility in modern buildings.

Moreover, IoT and wireless communication advancements have accelerated the adoption of smart lighting solutions across various sectors. These lighting systems are combined into building management platforms to optimize performance and reduce maintenance costs. The rising demand for smart building solutions is expected to further boost the market considerably. For instance,

- Ekinex S.p.A. estimates that the global Smart Lighting market will grow from USD 13.4 billion in 2020 to over USD 30 billion by 2025, representing a CAGR of 18%, a strong indicator of noteworthy market expansion.

Market Restraints

High Initial Costs and Integration Challenges to Limit Market Expansion

Deploying advanced lighting systems often requires substantial upfront investment that restrains the market. This financial barrier can slow adoption, especially among small & medium-sized projects with limited budgets. Integrating smart lighting technologies with existing building automation systems demands specialized technical expertise. These challenges can lead to longer installation times and higher labor costs, further impacting project feasibility. As a result, these factors hinder market penetration and limit the widespread deployment of architectural lighting solutions.

Market Opportunities

Rising Demand for Human-centric Lighting Creates New Market Opportunities

The rising demand for human-centric lighting (HCL) solutions presents a significant opportunity to expand the architectural lighting market. For instance,

- According to our data, the global human-centric lighting market was USD 3.53 billion in 2024 and is anticipated to reach USD 4.23 billion in 2025. It is projected to grow to USD 22.07 billion by 2032, witnessing a CAGR of 26.6% during the forecast period.

HCL systems are engineered to mimic natural light patterns, helping to regulate daily rhythms and promote physical and mental well-being. The demand for such solutions continues to grow with increased awareness about the impact of lighting on health and productivity across various environments.

This approach enhances user satisfaction, improves performance, and reduces absenteeism in professional settings. Such lighting solutions also support sustainability goals by optimizing energy usage and reducing environmental impact. With growing end-users’ focus on occupant health, human-centric lighting is expected to play a vital role in accelerating market growth.

SEGMENTATION Analysis

By Product Type

LED Lighting Dominates Due to Superior Energy Efficiency and Cost-effectiveness

Based on product type, the market is divided into LED lighting, fluorescent lighting, incandescent lighting, halogen lighting, smart lighting, and others.

The LED lighting segment is expected to account for 38.16% of the market in 2026. It is expected to grow at the highest CAGR due to its superior energy efficiency, longer lifespan, and declining costs, making it the preferred choice for new and retrofit projects. For instance,

- According to the UNFCCC, LED lamps consume 75% less energy than traditional incandescent bulbs. They also use 50% less energy than compact fluorescent lamps (CFLs), highlighting their efficiency in reducing energy consumption.

Smart lighting holds the second largest share as it offers enhanced control, customization, and integration capabilities, supporting the rising demand for smart building solutions and energy management.

By Technology

Wireless Segment Leads Owing to Ease of Installation and IoT Compatibility

Based on technology, the market is divided into wired and wireless.

The wireless segment is anticipated to hold a dominant market share of 52.54% in 2026 and is projected to grow at the highest CAGR due to its ease of installation, flexibility, and compatibility with IoT and smart building systems. These solutions reduce infrastructure costs and enable scalable lighting networks, making them attractive for new and retrofit installations.

The wired segment holds a significant share owing to its reliability, stable connectivity, and suitability for large-scale lighting installations where consistent performance is essential.

By Installation Type

New Installation Segment Holds the Largest Market Share, Driven by Urbanization and Construction Growth

By installation type, the market is bifurcated into new installation and retrofit installation.

In 2026, the new installation segment is projected to lead the market with a 60.07% share and is expected to grow fastest during the study period, owing to the ongoing urbanization and construction of commercial and residential buildings. New projects incorporate the latest technologies, driving the adoption of energy-efficient and smart lighting systems.

The retrofit installation segment maintains a significant share due to the vast existing building stock requiring upgrades to improve energy efficiency, comply with regulations, and enhance lighting quality without complete rebuilds.

By Application

Indoor Lighting Segment Dominates as it Plays a Crucial Role in Enhancing Functionality and Aesthetics

Based on application, the market is divided into indoor lighting, outdoor lighting, architectural lighting, decorative lighting, and others.

Indoor lighting dominates the market due to its widespread use by end-users, where lighting considerably impacts functionality and aesthetics. The critical role of interior lighting in enhancing user comfort and energy management contributes to its leading position.

Outdoor lighting is expected to grow at the highest CAGR, driven by increasing investments in urban infrastructure, public safety, and smart city initiatives that require advanced, energy-efficient, and adaptive exterior lighting solutions.

To know how our report can help streamline your business, Speak to Analyst

By End-user

Commercial Sector Leads Fueled by Sustainability Mandates

Based on end-user, the market is divided into residential, commercial, industrial, institutional, hospitality, and others.

The commercial segment leads the market and is projected to grow at the highest CAGR due to the extensive adoption of energy-efficient and smart lighting to reduce operational costs and improve occupant experience. Large-scale projects and growing sustainability mandates in commercial buildings are further driving the segment’s growth.

The residential segment holds the second-largest share as homeowners increasingly seek energy-saving, smart lighting solutions that offer convenience, personalization, and improved home aesthetics.

ARCHITECTURAL LIGHTING MARKET REGIONAL OUTLOOK

By region, the market is studied across North America, Asia Pacific, Europe, Middle East & Africa, and South America.

Asia Pacific

Asia Pacific Architectural Lighting Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The market in Asia Pacific reached USD 2.36 billion in 2025, representing 24.90% of total market revenue, and is projected to reach USD 2.49 billion in 2026. Asia Pacific dominates the market and is expected to witness the highest CAGR due to rapid urbanization, industrialization, and infrastructure development across countries such as China, Japan, India, and South Korea. Increasing government initiatives promoting energy efficiency and green building practices drive demand for advanced lighting solutions in commercial and residential sectors. Additionally, the rising adoption of smart lighting technologies and favorable regulatory frameworks further support market expansion in the region. Additionally, a growing middle-class population and increasing construction activities contribute to the robust growth. The Japan market is projected to reach USD 0.57 billion by 2026, the China market is projected to reach USD 0.72 billion by 2026, and the India market is projected to reach USD 0.47 billion by 2026.

North America

The North America market was valued at USD 3.31 billion in 2025, capturing 34.90% of global revenue, and is estimated to reach USD 3.45 billion in 2026. The region benefits from well-established construction and renovation activities, high sustainability awareness, and regulatory compliance, such as LEED certification. Moreover, ongoing investments by the U.S. in smart city initiatives and infrastructure upgrades continue to support steady market growth. The U.S. market is projected to reach USD 2.01 billion by 2026. For instance,

- In May 2025, Phase One of Illuminate CLE was inaugurated in Cleveland's Public Square as a permanent, architecturally integrated lighting installation. The project highlights a combination of design and technical expertise.

Europe

In 2025, Europe held 24.90% of the global market, reaching a valuation of USD 2.36 billion, and is projected to grow to USD 2.49 billion in 2026. The widespread adoption of LED and smart lighting technologies in commercial, residential, and public infrastructure fuels market demand. Furthermore, the region’s mature construction market and focus on green building certifications continue to bolster investments in architectural lighting. The UK market is projected to reach USD 0.59 billion by 2026, while the Germany market is projected to reach USD 0.51 billion by 2026.

Middle East and Africa (MEA) and South America

In 2025, the Middle East & Africa market stood at USD 0.77 billion, representing 8.10% of global demand, and is projected to grow to USD 0.79 billion in 2026. The Middle East & Africa (MEA) and South America regions are expected to experience slower growth in the market due to economic uncertainties and a slower pace of infrastructure development. Limited awareness and adoption of advanced lighting technologies and smart systems also restrain market expansion.

Rest of the World

Latin America maintained a strong presence in the global market, reaching USD 0.67 billion in 2025, accounting for 7.10% share, and is expected to reach USD 0.68 billion in 2026.

Competitive Landscape

KEY MARKET PLAYERS

Key Players Focus on Launching New Products to Strengthen their Market Position

Players are launching new products to enhance their market positioning by leveraging technological advancements, addressing diverse consumer needs, and staying ahead of competitors. They prioritize portfolio enhancement and strategic collaborations, acquisitions, and partnerships to strengthen their product offerings. Such strategic product launches help companies maintain and grow their market share in a rapidly evolving landscape.

Long List of Companies Studied (including but not limited to)

- Signify Holding (Netherlands)

- OSRAM GmbH (Germany)

- Cree Lighting (U.S.)

- Cooper Lighting LLC (Ireland)

- Lutron Electronics (U.S.)

- Hubbell (U.S.)

- ERCO Lighting (Germany)

- Zumtobel Group (Austria)

- TRILUX Lighting Ltd. (Germany)

- Fagerhult (Sweden)

- Acuity Inc. (U.S.)

- Bega (Germany)

- Vode Lighting (U.S.)

- Luxit (U.S.)

- Arturo Alvarez (Spain)

- Delta Light (Belgium)

- iGuzzini (Italy)

- Soraa (U.S.)

- Seoul Semiconductor (South Korea)

- And more..

KEY INDUSTRY DEVELOPMENTS

- May 2025- Pinnacle Architectural Lighting and Anthology Woods launched the Renew linear lighting series. The product line merges high-performance illumination with sustainable FSC-certified wood materials, showcasing technical precision and environmental stewardship.

- April 2025- Lucent Lighting introduced the Mix85 luminaire range, focusing on quality, innovation, and sustainable design practices. The product ensures high lighting performance with a minimal environmental footprint.

- January 2025- U.S. Architectural Lighting released the QBIX Architectural Sconce Series. The line features configurable optics and dual-directional lighting to enhance visual aesthetics and functionality across various architectural applications.

- December 2024- Häfele introduced an Architectural Lighting Range comprising nine series personalized to various lighting applications and design requirements. The range includes downlights, spotlights, and wall washers, enabling flexible lighting solutions across interior spaces.

- September 2024- Signify introduced its WiZ Smart Lighting range to the Indonesian market. The plug-and-play solution offers users 16 million color options and a dynamic white-to-color spectrum, catering to the growing demand for smart and customizable home lighting.

REPORT COVERAGE

The architectural lighting market report focuses on key aspects such as leading companies, product types, and product applications. Besides, the report offers insights into the market trend analysis and highlights vital application developments. In addition to the factors above, the report encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

|

Study Period |

2021-2034 |

|

|

Base Year |

2025 |

|

|

Estimated Year |

2026 |

|

|

Forecast Period |

2026-2034 |

|

|

Historical Period |

2021-2024 |

|

|

Unit |

Value (USD Billion) |

|

|

Growth Rate |

CAGR of 5.20% from 2026 to 2034 |

|

|

Segmentation |

By Product Type

By Technology

By Installation Type

By Application

By End-user

By Region

|

|

|

Companies Profiled in the Report |

|

|

Frequently Asked Questions

The market is projected to reach USD 17.86 billion by 2034.

In 2026, the market size stood at USD 11.94 billion.

The market is projected to grow at a CAGR of 5.20% during the forecast period.

By application, the indoor lighting segment leads the market.

The increasing demand for energy-efficient and sustainable lighting solutions is a key factor driving market growth.

Signify Holding, OSRAM GmbH, Cree Lighting, Cooper Lighting LLC, and Lutron Electronics are the top players in the market.

Asia Pacific dominated the global architectural lighting market with a share of 24.90% in 2025 and is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us