Articulated Bus Market Size, Share & Industry Analysis, By Articulation Type (Single-Articulated, and Bi-Articulated), By Propulsion (Conventional and Electric), By Application (Intracity, Intercity, Shuttles Service, and Tour & Charter), By Passenger Capacity (Below 80 passengers, 80–120 passengers, and 120–180+ passengers), and Regional Forecast, 2026-2034

Articulated Bus Market Size and Future Outlook

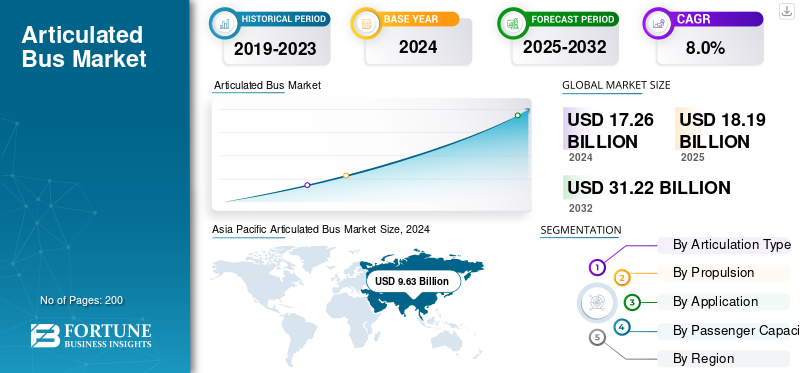

The global articulated bus market size was valued at USD 18.19 Billion in 2025 and is projected to grow from USD 19.65 Billion in 2026 to USD 35.82 Billion by 2034, exhibiting a CAGR of 7.8% during the forecast period. Asia Pacific dominated the articulated bus market with a market share of 55.92% in 2025.

Articulated buses are extended-length passenger vehicles consisting of two or more rigid sections linked by a pivoting joint that allows flexible movement around curves. Typically, 18 meters or longer, these high-capacity buses operate mainly in urban transit and Bus Rapid Transit (BRT) systems, accommodating over 100 passengers per trip. They enhance operational efficiency by reducing congestion and optimizing driver-to-passenger ratios. Widely used for intracity and high-demand corridors, articulated buses balance capacity, maneuverability, and cost-effectiveness compared to deploying multiple standard buses.

The global articulated bus market is experiencing steady growth, driven by rising urbanization, expansion of BRT systems, and public transport electrification initiatives. Municipalities are increasingly adopting articulated configurations for efficient passenger movement in dense city networks, particularly across the Asia Pacific and Europe. Key industry participants include Volvo Buses, MAN Truck & Bus, Daimler Buses, Scania AB, Solaris Bus & Coach, Yutong, BYD, and New Flyer Industries, which focus on advanced propulsion, modular chassis, and electric articulated platforms. Government policies promoting sustainable mass transit and technological advancements in battery systems further support adoption across major metropolitan regions.

U.S. tariff policies have influenced global articulated bus market trends by raising import costs for components, chassis, and electric drivetrains sourced from Asia and Europe. Increased tariffs on steel, aluminum, and electric bus parts have elevated manufacturing expenses, pressuring margins for OEMs and transit authorities. Several suppliers responded by localizing assembly or sourcing materials domestically to mitigate cost fluctuations. However, these tariffs temporarily slowed cross-border supply chains and procurement cycles, particularly for zero-emission articulated buses reliant on imported batteries and electronic systems.

Download Free sample to learn more about this report.

ARTICULATED BUS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 18.19 Billion

- 2026 Market Size: USD 19.65 Billion

- 2034 Forecast Market Size: USD 35.82 Billion

- CAGR: 7.8% from 2026–2034

- Asia Pacific dominated the articulated bus market with a 55.92% share in 2025.

- Single-articulated buses are expected to account for 52.37% of the market in 2026.

- The 80–120 passenger capacity segment is projected to hold 49.27% of the market in 2026.

Asia Pacific

Asia Pacific led the market with USD 10.17 billion in 2025

Europe

Europe reached USD 4.13 billion in 2025 and is projected to grow to USD 4.48 billion in 2026

North America

North America accounted for USD 2.06 billion in 2025

U.S.

Rising deployment of 60-ft battery-electric articulated buses by major transit agencies and expanding BRT infrastructure continue to support market growth.

Japan

Growing investments in sustainable urban transportation and demand for high-capacity public transit solutions are supporting the adoption of articulated buses across major metropolitan areas.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rapid Urbanization and the Concomitant Demand for High-Capacity Urban Transit Solutions Drives Market Growth

As cities expand in population and geographic extent, the pressure on existing public transportation networks intensifies. According to the World Bank, growth in African cities alone has prompted six operational Bus Rapid Transit (BRT) systems and ten more under-development systems, which typically deploy articulated buses. Volvo Buses recently introduced fully electric bi-articulated models designed for high-capacity BRT corridors, such as its Brazil-manufactured 28-metre, up-to-250-passenger BZRT chassis now available for global export.

In high-density urban environments, the benefits of articulated buses become manifest, with the capacity to carry significantly more passengers per trip than standard buses (many models exceed 120 passengers) and the ability to operate in dedicated lanes, which help reduce congestion, curb emissions, and optimize operational costs for transit agencies. For example, in Bogota, the introduction of 18-metre articulated electric buses by Zhongtong Bus reflects this pivot.

Cities are increasingly favoring articulated formats as they offer a balance of high throughput with the flexibility of a bus (as opposed to rail) and can be deployed on a relatively shorter lead-time. Urban planning documents show that over 60% of developed cities already integrate articulated buses into their transport systems.

The surge in urban populations and the need for efficient, scalable public-transport capacity are driving articulated bus adoption worldwide. Transit agencies seeking to upgrade trunk corridors, particularly BRT and high frequency routes, are selecting articulated buses as a prime solution to meet higher passenger volumes, tighter emissions constraints, and more demanding urban mobility workflows.

MARKET RESTRAINTS

Complexity and Cost of Infrastructure Adaptation and Vehicle Maintenance to Encumber Market Expansion

A key restraining factor for the global articulated bus market is the complexity and cost of infrastructure adaptation and vehicle maintenance, which can significantly hamper deployment in many regions. Articulated buses require dedicated lane space or wide turning radii, specialized maintenance depots, and in the case of electric articulated models, dependable charging infrastructure. For example, in Australia, when 83 articulated “bendy” buses were withdrawn from service due to structural cracking in the joints, passenger capacity dropped by 30 % on affected routes, demonstrating how mechanical issues can disrupt operations.

Similarly, in India, the city of Bengaluru introduced about 1,700 electric buses since 2021 but reported over 13,000 breakdowns in the last two and half years, many involving battery issues and long repair real time, illustrating how maintenance burdens escalate when infrastructure is inadequate.

These infrastructure and maintenance challenges directly affect transit agencies’ willingness to commit to large articulated bus procurements. When bus bodies are longer (typically 18 m or more), city streets must be widened, stations redesigned, and depot overhead remodeled, leading to increase in upfront costs and operational risk. For instance, NFI Group, reported record order volumes but also a backlog valued at USD 11.7 billion due to supply chain and labor constraints.

Due to these added complexities, higher vehicle cost, specialized servicing, infrastructure upgrades, and uncertainties in reliability, many cities on tighter budgets or those lacking dedicated lanes may opt instead for standard-length buses or mini-BRT rather than articulated models. This slows the articulated bus market’s potential in many emerging and budget-constrained regions, despite the appeal of higher capacity; the risk and cost burden remain too high without strong policy support or financing mechanisms.

MARKET OPPORTUNITIES

Mass Adoption of Zero-Emission Articulated and Bi-Articulated Buses in Rapidly Urbanizing BRT Corridors Generates Several Growth Opportunities

The mass adoption of zero-emission articulated and bi-articulated buses is increasing in rapidly urbanizing Bus Rapid Transit (BRT) corridors, especially in emerging and mid-sized cities worldwide. For example, Volvo Buses recently began series production of its fully electric bi-articulated chassis, 28 meters in length and capable of carrying up to 250 passengers, at its plant in Curitiba, Brazil. In September 2025, The Brazilian city of Goiania announced to introduce 21 of these buses in coming year (16 articulated, 5 bi-articulated) for service on a major BRT route.

Such examples show that transit agencies are prepared to invest in large articulated buses with advanced electric powertrains, especially where dedicated BRT corridors exist. The synthesis of high passenger throughput and the environmental imperative makes articulated buses especially attractive. Moreover, the manufacturing of these large vehicles is becoming globalized: Volvo’s Brazil-based articulated electric production supports export to high-growth markets worldwide.

As cities aim to reduce emissions, manage rising urban travel demands, and extend capacity without full light-rail investment, the articulated segment gains a strong foothold, creating a major growth path for manufacturers, transit agencies, and infrastructure providers globally.

ARTICULATED BUSES MARKET TRENDS

Adoption of Modular Platform Architectures and High-Power Charging Systems is One of the Significant Market Trends

The product enables faster deployment, lower lifecycle costs, and higher operational flexibility. For example, Kiepe Electric premiered at Busworld Europe 2023 a modular platform concept for bus OEMs that supports 12 m, 18 m, and 24 m articulated formats, including double-articulated models. This system supports up to 800 kW high-power charging, enabling articulated buses to recharge in minutes rather than hours, a major advantage for operators running tight headways in high-demand corridors.

Modular platform usage is being embraced by leading OEMs, BYD launched its B18.b electric articulated bus at Busworld, featuring its eBus Platform 3.0 with cell-to-chassis integration, high battery capacity, and fast charging capabilities. These innovations mean that cities and transit agencies can now select articulated buses that share common components, electronic architecture, and drive-trains across vehicle lengths, reducing procurement complexity and spare-parts cost.

The combination of modular designs plus ultra-fast charging supports 24-hour operations in corridors, raising the appeal of articulated formats for trunk routes. As a result, this trend supports global articulated bus market demand as it lowers the operational and capital cost barriers for deploying large buses, expands the viable use-cases (including bi-artics), and accelerates fleet modernization. With modular platform architecture, transit agencies in various regions can standardize across mixed bus fleets while simplifying articulated bus procurement and maintenance, thereby stimulating broader adoption worldwide.

Download Free sample to learn more about this report.

Segmentation Analysis

By Articulation Type

Single-Articulated Bus Format Dominates as it Maintains Balance Between Capacity and Flexibility

By articulation type, the market is classified into single-articulated and bi-articulated.

The [segment name] segment is expected to account for 52.37% of the market in 2026. The single-articulated bus format (typically around 18 m length with one articulation joint) currently dominates the global market. It strikes a balance between capacity and flexibility; many cities adopt 18-metre articulated vehicles, which can serve high-demand routes without the more extreme infrastructure needs of bi-articulated buses. For example, an 18-metre electric articulated bus from Solaris (the Urbino 18 electric) was recently evaluated in Europe in April 2024, showing strong performance in everyday urban service.

The bi-articulated segment remains more niche. In a recent order by Volvo Buses in Brazil, only 5 of the 21 buses were bi-articulated (the rest single-articulated) for the East-West BRT line in Goiania. The single-articulated type’s dominance helps the segment as it is easier to deploy, requires fewer modifications to stations and lanes, and aligns with many agencies’ upgrade strategies. As more cities transition to higher-capacity, low-emission corridors, demand for single-articulated buses is expected to grow further, driving overall market growth in the articulation-type segment.

By Propulsion

Conventional Segment Dominate the Market due to its Advantages

By propulsion, the articulated buses market is bifurcated into conventional and electric.The conventional segment (diesel, CNG, and other traditional fuels) still leads globally.The fuel powered segment will account for 39.56% market share in 2026. The advantages is structural: depots already have fueling infrastructure, maintenance shops are tooled for powertrain service, parts networks are mature, and operating crews possess deep experience, all of which reduce procurement risk and accelerate speed deployment. Agencies also favor conventional units for route flexibility (long duty cycles and harsh climates), predictable uptime, established resale values, and simpler financing aligned with multi-year replacement programs. For example, Honolulu’s operator recently ordered 35 new 60-ft articulated clean-diesel buses, leveraging existing facilities and training pathways. In fleets undergoing transition, conventional orders continue to backfill retirements, support peak capacity, and stabilize total cost of ownership while charging infrastructure and grid upgrades catch up. This sustains the segment’s dominance by assuring reliable supply and service continuity.

By Application

Intracity Segment Dominates due to Increasing Passenger Traffic

By application, the market is segregated into intracity, intercity, shuttle services, and tour & charter.

The Intracity segment will account for 48.44% market share in 2026. Intracity use (urban bus services inside cities) is the dominant application for articulated buses. This is due to high passenger volumes, bus rapid transit (BRT) systems, and urban trunk corridors are perfect use-cases for articulated buses; they maximize capacity and efficiency in dense networks. The dominance of this segment supports growth because, as urban populations rise, more cities build or upgrade their trunk routes with articulated buses rather than standard buses or smaller vehicles. Agencies thus favor articulated buses for main city lines, which enhances procurement volume and supports overall market expansion.

To know how our report can help streamline your business, Speak to Analyst

By Passenger Capacity

80–120 Passengers Segment Dominates owing to Ability to meet Urban Transit Requirements

By passenger capacity, the market is classified into below 80 passengers, 80–120 passengers, and 120–180+ passengers. 80–120 passenger capacity band (typical for standard 18-metre articulated buses) is the dominating segment globally. The 80–120 passengers segment is expected to account for 49.27% of the market in 2026. These buses align with the majority of urban transit requirements, delivering high passenger throughput within typical bus lane infrastructure. For example, Solaris’s studies of its 18-metre articulated electric buses show they are optimized for this capacity band.

As most transit agencies operate in this capacity range, needing more than standard 12-m buses but less than ultra-high capacity, this segment witnesses the greatest volume. Its dominance supports segment growth as it represents the sweet spot for articulated deployments. As cities expand or upgrade, many choose this capacity band to balance cost, infrastructure, and throughput.

ARTICULATED BUS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Articulated Bus Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific represented USD 10.17 Billion, accounting for 55.92% of the worldwide market, and is projected to grow to USD 11.02 Billion in 2026. Asia Pacific dominates the articulated bus market, driven by China’s scale and rising South/Southeast Asian tenders. China reports 554,000 new-energy buses, accounting for 81.2% of its public bus fleet, reflecting deep electrification that increasingly includes 18–28 m vehicles for megacity corridors. Manufacturers are pushing ultra-high-capacity options. Yutong unveiled a 26-m double-articulated pure-electric bus and Volvo began series production of its 28-m electric articulated/bi-articulated BZRT chassis in Brazil for export, validated in Latin America but highly relevant to APACs BRT megacities.

India, meanwhile, launched a national tender for 10,900 e-buses under the PM E-Drive scheme, expanding big-city trunk capacity. These developments sustain APAC’s leadership: manufacturing depth, strong policy support, and dense urban corridors translate into persistent articulated procurements that shape global supply chains, component localization, and cost curves.

Europe

Europe recorded a market size of USD 4.13 Billion in 2025, capturing 22.69% of the global market share, and is projected to reach USD 4.48 Billion in 2026. Europe is the fastest-growing region for articulated buses due to scale electrification and multi-city procurement frameworks. Berlin’s BVG issued a follow-on order for 270 Solaris Urbino 18 e-articulated under a framework permitting up to 700 e-artics over eight years, one of the Europe’s largest articulated electrification programs. Additional momentum comes from steady municipal orders, with regional market data showing ~4,000 e- bus sales across Europe in the first three quarters of 2024, a 25% year-over-year increase. As cities enforce low-emission zones and expand BRT-like priority measures, 18-m articulated BEVs deliver capacity, depot compatibility, and lifecycle cost benefits, accelerating fleet replacements and establishing exportable deployment models that elevate global volumes.

North America

The North America market accounted for USD 2.06 Billion in 2025, representing 11.31% of the global industry, and is expected to reach USD 2.2 Billion in 2026. North America’s articulated bus demand is centered on large-city BRT and trunk routes, with electrification steadily lifting replacement needs. In the U.S., zero-emission transit bus adoptions reached 7,028 by July 2024, underscoring agencies’ readiness to specify 60-ft battery electric articulated models for high-demand corridors. New York MTA recently expanded its order to 72 battery-electric 60-ft New Flyer articulated buses within a broader 265-bus procurement.

At the same time, agencies continue adding high-capacity articulated buses to elevate service quality. Richmond’s GRTC introduced new 60-ft buses for the Pulse BRT, with additional vehicles entering service through year-end. New Flyer supports over 35,000+ heavy-duty buses in service across North America, including 1,900 zero-emission units, useful for fleet standardization and parts commonality. As electrified artics spread beyond early leaders to mid-size metros, North America’s segment growth reinforces the global market with proven 18-m BRT use-cases, interoperable charging standards, and increasingly maturing maintenance ecosystems.

Rest of the World

In 2025, Rest of the World held 10.08% of the global market, reaching a valuation of USD 1.83 Billion, and is projected to grow to USD 1.95 Billion in 2026. Growth in the Rest of the World is led by Latin American BRT hubs and selective Middle East/Africa deployments. The region has become a bellwether for bi-articulated operations on ultra-busy corridors. Volvo is validating 28-m electric bi-articulated buses in Curitiba, Bogotá, and Mexico City, while Mexico City’s Metrobús has unveiled the world’s first regular electric bi-articulated service on a corridor carrying approximately 1.8 million daily riders, demonstrating that high-capacity zero-emission operations are feasible today.

Complementary fleet additions, such as BYD e-buses on CDMX Line 4, serving ~120,000 passengers/day, help build operating experience and charging ecosystems that downstream articulated orders can leverage.

Brazil’s role as a production/export base for large Volvo e-artics is improving supply access across LATAM. While fiscal volatility can moderate the pace, the demonstrated throughput benefits of 18–28 m buses on BRT spines underpin steady regional demand.

COMPETITIVE LANDSCAPE

Key Industry Players

High-Capacity Transit Innovation and Robust International Production Base of Key Companies Drive Competitive Edge

Volvo Buses is recognized as one of the leading global manufacturer in the articulated bus market due to its extensive legacy in high-capacity transit innovation, robust international production base, and strong presence in Bus Rapid Transit (BRT) systems worldwide. The company has consistently advanced articulated and bi-articulated platforms with an emphasis on safety, efficiency, and electrification. Its BZL Electric Articulated and BZRT Bi-Articulated chassis, produced in Brazil and Sweden, demonstrate Volvo’s technological leadership, with the 28-meter BZRT capable of carrying up to 250 passengers, the largest electric bus of its class. Volvo’s dominance is reinforced by successful deployments across Latin America, Europe, and Asia, particularly in Curitiba and Bogotá, where its buses serve millions daily. Continuous innovation in modular electric drivetrains, high-capacity passenger design, and durable chassis engineering has positioned Volvo as the benchmark for articulated bus reliability, efficiency, and sustainability in the global market.

Solaris Bus & Coach has built a strong European leadership in electric articulated buses. Its flagship Urbino 18 Electric has been widely adopted by major operators such as BVG Berlin, RATP Paris, and Warsaw’s ZTM. The model integrates advanced battery systems, regenerative braking, and a modular architecture supporting up to 140 passengers. Solaris’s focus on zero-emission innovation, lightweight composite materials, and high passenger comfort has earned it repeated large-scale contracts, including a framework for up to 700 articulated e-buses for Berlin’s BVG in 2024. Through consistent R&D and a reputation for operational reliability, Solaris has firmly established itself as Europe’s leading articulated electric bus specialist and a global industry frontrunner in high-capacity transit.

LIST OF KEY ARTICULATED BUS COMPANIES PROFILED

- Zhengzhou Yutong Bus Co., Ltd. (China)

- BYD Co., Ltd. (China)

- New Flyer Industries / NFI Group (Canada)

- Volvo Buses (Sweden)

- EvoBus / Mercedes-Benz (Daimler) (Germany)

- MAN Truck & Bus SE (Germany)

- Scania (Volkswagen Group) (Sweden)

- IVECO Bus (Iveco Group) (Italy)

- Solaris Bus & Coach (Poland)

- VDL Bus & Coach (Netherlands)

- Alexander Dennis Limited (ADL)

- Van Hool NV (Belgium)

- Otokar (Turkey)

- CRRC Corporation Limited (China)

- Xiamen King Long United Automotive (King Long) (China)

KEY INDUSTRY DEVELOPMENTS

- In October 2025, Karsan received a tender to supply 42 of its e-ATA 18-metre articulated buses for operation in Bari, Italy. Delivery of these vehicles, will be carried out in collaboration with Italian dealer Kmobility, from June 2026.

- In August 2025, Volvo Buses, in collaboration with GreenMob Capital, deployed 21 electric buses, 16 articulated and 5 bi-articulated, across the city of Goiania, Brazil. These represent the world’s first fully electric bi-articulated units in regular operation. Each bus delivers exceptional passenger capacity and zero-emission performance tailored for Bus Rapid Transit (BRT) networks. The project showcases Latin America’s rapid shift toward electrified public transport, supported by innovative financing and local partnerships. Volvo’s participation cements its leadership in large-capacity e-mobility solutions, combining Scandinavian technology with Brazilian operational needs to advance cleaner, quieter, and more efficient urban transportation solutions.

- In June 2025, IVECO BUS confirmed a major order from De Lijn, the public transit company of Flanders, for 100 18-meter articulated electric buses. The order forms part of a broader fleet electrification program and strengthens the region’s transition to zero-emission public transport. These buses would feature advanced battery systems, accessibility-focused interiors, and fast-charging capability. The partnership builds on a framework agreement and demonstrates confidence in IVECO’s E-WAY H2 technology. For IVECO, this deal reinforces its strong European footprint, while for De Lijn it represents a decisive step toward sustainable, high-capacity transit serving dense urban corridors across Belgian cities.

- In May 2025, Spanish bodybuilder Castrosua partnered with Chinese EV leader BYD to co-develop a new articulated electric bus platform for European markets. The collaboration integrates Castrosua’s custom bus body engineering with BYD’s proven electric chassis and battery systems. The forthcoming model targets operators seeking sustainable, high-capacity mobility solutions for urban routes. This partnership symbolizes Spain’s growing role in Europe’s e-mobility ecosystem and leverages BYD’s global technology leadership. By combining localized production expertise with advanced EV technology, both companies aim to accelerate adoption of articulated e-buses tailored for EU standards and operator requirements.

- In December 2023, Solaris Bus & Coach and Berliner Verkehrsbetriebe (BVG) expanded their collaboration through a framework agreement allowing up to 700 articulated electric buses over eight years. Under this contract, BVG recently confirmed a batch of 270 Urbino 18 electric buses featuring Solaris High Energy batteries and dual charging modes. The deal represents one of Europe’s largest electric articulated-bus procurements. It emphasizes BVG’s commitment to sustainable fleet transition and Solaris’s dominance in the electric-bus market. The cooperation enhances Berlin’s public transport decarbonization while setting a new benchmark for large-scale zero-emission bus adoption across the continent.

REPORT COVERAGE

The global articulated bus market report provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market forecasts a detailed competitive landscape with information on the market share, growing opportunities, and profiles of key players in the automotive market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Articulation Type, By Propulsion, By Application, By Passenger Capacity, and By Region. |

| By Articulation Type |

|

| By Propulsion |

|

| By Application |

|

| By Passenger Capacity |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 18.19 billion in 2025 and is projected to reach USD 35.82 billion by 2034.

In 2025, the market value stood at USD 10.17 billion.

The market is expected to expand at a CAGR of 7.8% during the forecast period (2026-2034).

The single-articulated segment lead the market by articulation type.

Rapid urbanization and the concomitant demand for high-capacity urban transit systems are the key factors driving market growth.

Top players in the Articulated Bus include Volvo Buses, MAN Truck & Bus, Daimler Buses, Scania AB, Solaris Bus & Coach, Yutong, and BYD.

Asia Pacific dominates the market.

North America, Europe, Asia Pacific, and the rest of the world are considered in the RD.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us