Artificial Blood Vessels Market Size, Share & Industry Analysis, By Product Type (Hemodialysis Access Grafts, Peripheral Vascular Grafts, Aortic Grafts, Coronary Vascular Grafts, and Others), By Material (ePTFE Grafts, Polyester Grafts, Polyurethane, Bioengineered/Tissue-Engineered Vascular Grafts, and Others), By Application (Aneurysm Repair, Occlusive Vascular Disease/Bypass Surgery, Hemodialysis Vascular Access, Trauma and Vascular Reconstruction, and Others), By End-user (Hospitals & ASCs, Specialty Cardiac & Vascular Centers, and Others), and Regional Forecast, 2026-2034

Artificial Blood Vessels Market Size and Future Outlook

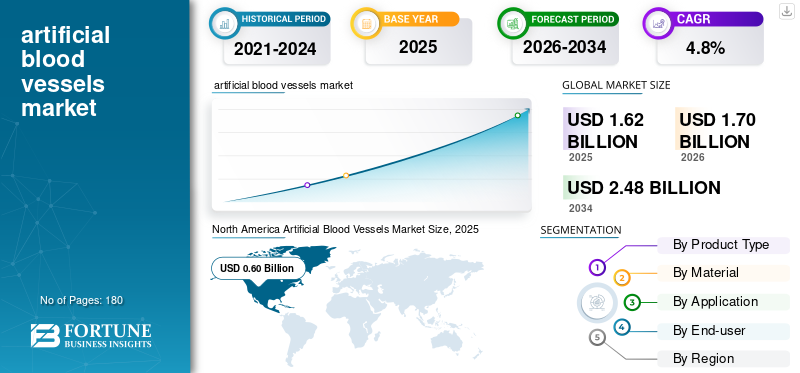

The artificial blood vessels market size was valued at USD 1.62 billion in 2025. The market is projected to grow from USD 1.70 billion in 2026 to USD 2.48 billion by 2034, exhibiting a CAGR of 4.8% during the forecast period. North America dominated the artificial blood vessels market with a market share of 37.03% in 2025.

Artificial blood vessels are man-made vascular conduits used to replace, bypass, or reconstruct damaged blood vessels when native vessels are unsuitable or unavailable. They are used across peripheral bypass procedures, aortic repair, hemodialysis access creation, and selected vascular reconstruction cases. The market is growing due to broad and persistent clinical needs for these products . Cardiovascular diseases remain the leading cause of death worldwide, while peripheral artery disease and aortic disorders continue to create demand for surgical and hybrid interventions. Similarly, a large population of patients with kidney failure still depends on hemodialysis, keeping vascular access procedures clinically relevant. Growth is also supported by better diagnosis, greater procedural volumes in both developed and emerging healthcare systems, and ongoing improvements in graft design, handling, patency, and infection-control features. Together, these factors are sustaining steady adoption of artificial blood vessels across multiple care settings.

Furthermore, W. L. Gore & Associates, Terumo Corporation, Getinge AB, and BD held the largest market share, driven by increased investments and strategic initiatives, including new product launches, collaborations, and partnerships.

Download Free sample to learn more about this report.

Artificial Blood Vessels Market Key Takeaways

- 2025 Market Size: USD 1.62 billion

- 2026 Market Size: USD 1.70 billion

- 2034 Forecast Market Size: USD 2.48 billion

- CAGR: 4.8% from 2026–2034

- North America dominated the artificial blood vessels market with a 37.03% share in 2025.

- The ePTFE Grafts segment is projected to hold a 40.4% market share in 2026.

- The Hospitals & ASCs segment is projected to account for 76.3% of the market in 2026.

North America

North America held 37.03% share in 2025, valued at USD 0.60 billion.

Asia Pacific

Asia Pacific market is projected to reach USD 0.39 billion by 2026.

Europe

Europe market is projected to reach USD 0.50 billion by 2026.

U.S.

Market projected to reach USD 0.57 billion by 2026.

Japan

Market projected to reach USD 0.08 billion by 2026.

Read More

ARTIFICIAL BLOOD VESSELS MARKET TRENDS

Shift Toward Procedure-Specific and More Selective Grafts is Emerging Market Trend

A significant market trend is the shift away from viewing artificial blood vessels as a broad commodity and toward using them as procedure-specific tools chosen for distinct clinical situations. Hospitals and vascular specialists are becoming more selective about graft configuration, wall thickness, support design, and surface properties depending on whether the target procedure is peripheral bypass, dialysis access, or aortic reconstruction. This is raising the value of differentiated products that offer better handling in the operating room and more predictable performance after implantation. Another noticeable trend is the growing overlap between open surgical and endovascular treatment pathways. Even where minimally invasive options expand, artificial graft technologies remain relevant in hybrid care models and in patients with more complex diseases.

Additionally, the market is opting for products backed by strong surgeon familiarity, consistent outcomes, and ease of use rather than novelty alone. Moreover, the increased focus on lifecycle performance, including patency, complication rates, and reintervention burden is also a prominent trend as hospitals pay closer attention to downstream economic outcomes. That is pushing manufacturers to position grafts not only as implantable products but also as solutions that improve procedural confidence and long-term care efficiency.

MARKET DYNAMICS

MARKET DRIVERS

High Procedure Need in Peripheral Vascular Disease, Aortic Repair, and Dialysis Access Drives Market Growth

One of the strongest driver for artificial blood vessels market growth is the steady rise in procedures linked to peripheral vascular disease, aneurysm management, and hemodialysis access. Artificial grafts remain clinically important when surgeons need a reliable conduit and an autologous vessel is unavailable or unsuitable for the target anatomy. In peripheral artery disease, bypass surgery continues to hold a crucial role in limb salvage and severe cases where endovascular treatment may not be enough. In aortic repair, prosthetic graft technologies remain central to open and hybrid treatment pathways.

Hemodialysis access is another major demand engine, as long-term kidney failure management still requires dependable vascular access, including arteriovenous grafts in patients who are not good fistula candidates. This creates a recurring procedural base rather than a one-time episodic market. This combined with aging populations, longer survival among patients with chronic diseases, earlier diagnosis, and broader access to specialty vascular care also drives the market development. Practically, the market benefits from both high-acuity surgical need and chronic-care volume, which gives it a more stable demand profile than many niche device categories.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Preference for Native Vessels and Minimally Invasive Alternatives Limits Market Growth

Despite healthy demand fundamentals, the market faces different restraints, impacting its growth. The most significant restraint is that artificial blood vessels are not the first choice in every vascular procedure. In several settings, surgeons may still prefer autologous veins or arteries due to its familiarity, long-term patency expectations, or lower infection risk in selected patients. In hemodialysis access, clinical practice has favored fistulas when feasible, while grafts are often reserved for patients with unsuitable vasculature or urgent access needs. In peripheral interventions, the continued expansion of endovascular techniques can also reduce the number of cases that progress to open bypass with prosthetic conduits.

In addition, artificial grafts can raise concerns about thrombosis, infection, anastomotic complications, and long-term durability, especially in smaller-caliber applications. These realities do not erase demand, but narrow the addressable market relative to the broader vascular disease burden. Reimbursement pressure and hospital budget scrutiny add another layer of restraint, particularly in price-sensitive markets where surgeons and providers must balance procedural necessity with total treatment cost. As a result, the market growth remains solid, but not unconstrained.

MARKET OPPORTUNITIES

Better Materials and Next-Generation Bioengineered Conduits Can Create Significant Growth Opportunities

A significant market opportunity lies in aligning catheter selection with specific care pathways rather than treating all thoracic drainage as the same commodity. For example, pleural effusion management can benefit from products designed for longer dwell times, patient comfort, and outpatient follow-up. In this area, specialized pleural drainage catheters are growing faster than standard chest tubes.

Another market opportunity is optimizing post-operative recovery where hospitals are increasingly focused on early mobilization and faster discharge, which creates demand for drainage solutions that are easier to manage, less prone to clogging, and more comfortable for patients. Suppliers that support clinicians with practical education, proper sizing, placement technique, and troubleshooting can reduce complications and strengthen loyalty. Emerging markets offer additional upside as hospital capacity expands and more thoracic and cardiac procedures shift to higher-volume centers. Lastly, product line breadth can be a differentiator as providers often prefer vendors who can reliably supply multiple catheter types and sizes, helping procurement reduce complexity while maintaining clinical flexibility.

MARKET CHALLENGES

Clinical Complexity, Variable Outcomes, and Pricing Pressure to Challenge Market Growth

The market’s biggest challenge is its higher dependence on navigating both clinical complexity and procurement pressure simultaneously. Artificial blood vessels are used in high-stakes procedures where outcomes are significant, yet patient anatomy, comorbidities, infection risk, and vessel quality vary widely. That makes product performance more difficult to standardize than in simpler device categories. A graft that performs well in one indication may not deliver the same value in another, and this complicates adoption, marketing, and pricing strategy. The challenge is even greater in smaller-caliber or infection-prone settings, where complications can quickly affect surgeon preference.

On the commercial side, many hospitals are under pressure to control costs, which can limit premium pricing even when a product offers technical advantages. Emerging markets add another layer of difficulty as access is improving, but reimbursement and procurement pathways may still be inconsistent. In addition, the market lies between mature synthetic platforms and emerging bioengineered concepts, leaving manufacturers with a delicate balance as they must continue supporting proven products while investing in future technologies that may take time to scale. This combination of clinical caution and financial discipline makes the market attractive, but not easy to navigate.

Segmentation Analysis

By Product Type

Wide Adoption of Peripheral Vascular Grafts in Several Applications to Drive the Segment Growth

Based on product type, the market is segmented into hemodialysis access grafts, peripheral vascular grafts, aortic grafts, coronary vascular grafts, and others.

To know how our report can help streamline your business, Speak to Analyst

Peripheral vascular grafts account for a largest artificial blood vessels market share of the market as they are between the intersection of a high disease burden and clear surgical utility. Peripheral artery disease affects a substantial patient population, and severe or complex cases still require bypass procedures when endovascular treatment is not sufficient or durable enough. In these situations, artificial grafts remain an established option, particularly when native conduit quality is poor or unavailable.

Additionally, the hemodialysis access grafts segment is projected to grow at a CAGR of 3.9% during the forecast period.

By Material

ePTFE Grafts Dominate as They Balance Handling, Strength, and Established Clinical Acceptance

By material, the market is classified into ePTFE grafts, polyester grafts, polyurethane, bioengineered/tissue-engineered vascular grafts, and others.

ePTFE grafts hold the largest share as they combine practical surgical handling with long-standing clinical acceptance across peripheral vascular reconstruction and dialysis access. Surgeons value materials that are familiar, easy to suture, and available in a range of configurations suited to different anatomies. Moreover, the segment is projected to hold a 40.4% share in 2026.

Additionally, the bioengineered/tissue-engineered vascular grafts segment is estimated to grow at a CAGR of 9.5% during the forecast period.

By Application

Occlusive Vascular Disease/Bypass Surgery Leads as Surgery Protocols Require Routine, Repeatable Drainage

By application, the market is classified into aneurysm repair, occlusive vascular disease/bypass surgery, hemodialysis vascular access, trauma and vascular reconstruction, and others.

Occlusive vascular disease and bypass surgery represent the largest application segment as they bring together a large patient base, serious clinical consequences, and a continuing need for surgical revascularization. Patients with advanced peripheral artery disease often face pain, tissue loss, non-healing wounds, or limb-threatening ischemia, and these cases can still require bypass even as endovascular therapy expands. Moreover, the segment is projected to hold a 30.7% share in 2026.

Additionally, the aneurysm repair segment is estimated to grow at a CAGR of 5.2% during the forecast period.

By End-user

Hospitals and ASCs Dominate as Thoracic Drainage is Concentrated in the OR, ICU, and Emergency Care

On the basis of end-user, the market is classified into hospitals & ASCs, specialty cardiac & vascular centers, and others.

Hospitals and ASCs account for the largest share of end users as artificial blood vessels are implanted in settings that require operating-room infrastructure, imaging support, anesthesia capabilities, perioperative monitoring, and access to multidisciplinary teams. Aortic procedures, peripheral bypass surgeries, vascular reconstruction, and dialysis access creation are typically handled in organized surgical environments where patient selection, sterile technique, and post-operative management can be tightly controlled. Furthermore, the segment is set to hold 76.3% share in 2026.

In addition, the specialty cardiac & vascular centers segment is projected to grow at a CAGR of 6.9% during the forecast period.

Artificial Blood Vessels Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Artificial Blood Vessels Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest revenue share in 2024, at USD 0.57 billion, and reached USD 0.60 billion in 2025. North America is expected to grow steadily due to its high procedural base in peripheral vascular surgery, aortic repair, and dialysis access creation. The U.S. remains the core demand center due to its large volume of patients with peripheral artery disease, chronic kidney disease, diabetes, and other cardiovascular risk factors that often progress to vascular intervention. The region also benefits from strong hospital infrastructure, broad access to vascular specialists, and faster adoption of premium graft technologies, such as reinforced and specialty-coated synthetic conduits.

U.S. Artificial Blood Vessels Market

In 2026, the U.S. market is forecasted to represent USD 0.57 billion, capturing 33.4% of total global revenue.

Europe

Europe is expected to achieve a 3.9% growth rate in the coming years, the second-highest market globally, reaching USD 0.50 billion by 2026. Europe is projected to expand at a stable pace, supported by its aging population, established reimbursement systems, and sustained demand for vascular reconstruction procedures across major countries such as Germany, France, the U.K., Italy, and Spain. The region has a strong base of tertiary hospitals and cardiovascular centers that routinely perform peripheral bypass, aneurysm repair, and dialysis-related vascular access procedures. Demand for this product is also supported by the relatively high diagnosis and treatment rates for chronic vascular disorders compared to many developing markets.

U.K. Artificial Blood Vessels Market

The U.K. market is projected to reach USD 0.07 billion by 2026, accounting for 4.1% of the global market revenue.

Germany Artificial Blood Vessels Market

Germany's market is forecasted to reach about USD 0.11 billion by 2026, representing roughly 6.4% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is predicted to be valued at USD 0.39 billion, ranking as the third-largest globally. Asia Pacific is likely to be the fastest-growing region, as it combines a large patient pool with expanding healthcare capacity. Countries such as China and India are seeing a rising incidence of diabetes, hypertension, chronic kidney disease, and other conditions that increase the need for vascular access and bypass procedures. Similarly, Japan and Australia continue to contribute from the high-value end of the market through advanced surgical care and stable adoption of vascular graft products. Growth is also supported by ongoing investments in hospital infrastructure, increased availability of cardiovascular and vascular surgery services, and improved diagnostic rates in urban healthcare systems.

Japan Artificial Blood Vessels Market

Japan is projected to generate approximately USD 0.08 billion in revenue by 2026, contributing nearly 4.5% to the global market.

China Artificial Blood Vessels Market

China’s market is forecast to reach approximately USD 0.12 billion by 2026, contributing about 7.2% to global revenues.

India Artificial Blood Vessels Market

India is forecast to contribute approximately USD 0.05 billion to the market by 2026, corresponding to about 3.0% of global revenues.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are anticipated to witness moderate market growth, with Latin America expected to reach around USD 0.09 billion by 2026. Latin America is expected to grow from a smaller base, mainly driven by improved access to vascular surgery, increased dialysis capacity, and the rising burden of diabetes and cardiovascular disease. Brazil and Mexico remain the main revenue contributors as they have the largest procedure volumes, more developed hospital systems, and a greater concentration of vascular specialists than the rest of the region. The Middle East & Africa region is projected to show steady growth, supported by gradual expansion in specialty care, rising awareness of vascular disease, and increasing investment in hospital capacity in selected countries. The GCC countries are likely to account for the largest share of regional growth as they have comparatively stronger healthcare spending, more advanced cardiovascular centers, and better access to imported vascular graft products.

GCC Artificial Blood Vessels Market

By 2026, the GCC is expected to generate approximately USD 0.03 billion in the market, accounting for nearly 2.0% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Product Innovation to Reinforce the Market Position of Prominent Players

The market is moderately consolidated, with a mix of large multinational vascular device companies and a smaller group of specialized players competing across peripheral vascular grafts, aortic grafts, and hemodialysis access grafts. Competition is shaped less by price alone and more by product reliability, surgeon familiarity, clinical performance, graft material, and breadth of indication coverage. Established companies such as W. L. Gore & Associates, Terumo Corporation, Getinge AB, BD, LeMaitre Vascular, and B. Braun SE benefit from strong hospital relationships, broad geographic reach, and well-recognized graft platforms, which give them an advantage in large procurement contracts and repeat institutional demand.

Moreover, other key players, such as Artivion, Inc., Braile Biomédica, Japan Lifeline, and LifeNet Health, compete through ongoing technological developments, the growing demand for improved healthcare infrastructure, and efforts to improve procedural outcomes.

LIST OF KEY ARTIFICIAL BLOOD VESSELS COMPANIES PROFILED

- L. Gore & Associates (U.S.)

- Terumo Corporation (Japan)

- Getinge AB (Sweden)

- BD (U.S.)

- LeMaitre Vascular (U.S.)

- Braun SE (Germany)

- Artivion, Inc. (U.S.)

- Braile Biomédica (Brazil)

- Japan Lifeline (Japan)

- LifeNet Health (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Terumo Aortic, a global medical device company dedicated to developing solutions for aortic disease, and Bentley, a leading global manufacturer of balloon-expandable covered stents, announced their partnership in a clinical study in the U.S.

- February 2025: Humacyte, Inc. announced the commercial launch of Symvess (acellular tissue engineered vessel-tyod) for use in adults as a vascular conduit for extremity arterial injury when urgent revascularization is needed to avoid imminent limb loss, and when autologous vein graft is not feasible.

- December 2024: Humacyte, Inc. announced that the U.S. Food and Drug Administration (FDA) has granted full approval for SYMVESS (acellular tissue-engineered vessel-tyod) for use in adults as a vascular conduit for extremity arterial injury when urgent revascularization is needed to avoid imminent limb loss, and when an autologous vein graft is not feasible.

- December 2024: Artivion, Inc. announced that the U.S. Food and Drug Administration (FDA) has granted a Humanitarian Device Exemption (HDE) for use of the AMDS Hybrid Prosthesis ("AMDS") in acute DeBakey Type I dissections in the presence of malperfusion.

- October 2023: Getinge AB announced commercial availability of the iCast covered stent system in the U.S. for the treatment of iliac arterial occlusive disease.

- July 2023: Terumo Aortic announced that the Japanese Pharmaceuticals and Medical Devices Agency (PMDA) has granted approval of the Thoraflex Hybrid Frozen Elephant Trunk (FET) device for commercial sale in Japan for the treatment of patients with complex aortic arch disease.

- June 2023: NAMSA, a world-leading MedTech Contract Research Organization (CRO) offering global end-to-end development services, and Terumo Aortic announced that they have entered into a strategic outsourcing partnership to assist with the acceleration and commercialization of Terumo Aortic’s innovative aortic disease products.

REPORT COVERAGE

The report provides an in-depth analysis of all market segments, highlighting key drivers, trends, opportunities, restraints, and challenges. It also provides insights into technological advancements, key industry developments, company market share analysis, and profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.8% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type,Material, Application, End-user, and Region |

| By Product Type |

|

| By Material |

|

| By Application |

|

| By End-user |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.62 billion in 2025 and is projected to reach USD 2.48 billion by 2034.

In 2025, the North America market value stood at USD 0.60 billion.

The market is expected to exhibit a CAGR of 4.8% during the forecast period of 2026-2034.

The peripheral vascular grafts segment led the market by product type.

The key factors driving the market are rising high procedure needs in peripheral vascular disease, aortic repair, and dialysis access.

W. L. Gore & Associates, Terumo Corporation, Getinge AB, and BD are some of the major players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us