Artillery Ammunition Market Size, Share, Industry & Russia Ukraine War Analysis, By Munitions Technology (Conventional Munitions, Precision-Guided Munitions (PGMs), Smart Munitions, and Extended-Range Munitions), By Munitions Type (High-Explosive (HE), Armor-Piercing (AP), Cluster Munitions, Smoke/Illumination/Incendiary, and Precision-Guided Munitions (PGMs)), By Caliber (Small, Medium & Large), By Artillery System (Howitzers, Mortars, Rocket Artillery, and Naval Artillery), By Operational Range (Short-Range, Medium Range, & Long Range), By Propulsion Type, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

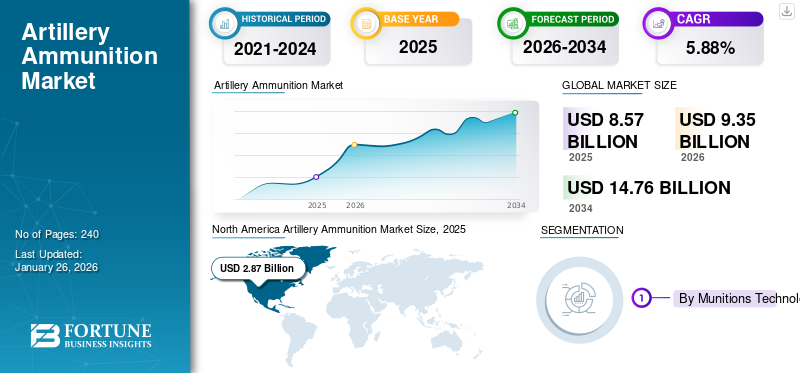

The global artillery ammunition market size was valued at USD 8.57 billion in 2025 and is projected to grow from USD 9.35 billion in 2026 to USD 14.76 billion by 2034, exhibiting a CAGR of 5.88% during the forecast period. North America dominated the artillery ammunition market with a market share of 33.50% in 2025.

Artillery ammunition is projectiles and shells used in large-caliber guns and artillery weapons for fire support, for firing over long distances. The components include the projectile (the shell), propellant to propel it, and a fuse to detonate the shell. They are fired from artillery guns, howitzers, or mortars. These artillery rounds are made to cause damage to targets over long distances, typically outside direct line of sight. The purpose of this weapon system is to suppress, neutralize, or destroy enemy forces, equipment, and installations.

Key players in the market are focused on the development of artillery ammunition with maximum target effect and high accuracy, and range. Moreover, major players are aiming to use various strategies to address the security needs of different countries. For instance, in November 2024, Rheinmetall and Lithuania announced the commencement of construction of a modern artillery ammunition production plant for 155mm artillery ammunition. The facility will be built around 340 hectares and possess an annual production capacity of tens of thousands of 155mm caliber artillery shells. In addition, BAE Systems offers a range of 155mm artillery ammunition, including modular, adaptable ammunition and the BAE Systems' Silver Bullet GPS-based guidance kit. Their "Next Generation Adaptable Ammunition" is designed for ease of manufacture and cost-effectiveness.

Download Free sample to learn more about this report.

Impact of Russia Russia-Ukraine War

Russia-Ukraine War Has Boosted Demand for Reliable Artillery Munitions with Rising Importance of Precision-guided Artillery Systems

The Russia-Ukraine war has significantly impacted the artillery ammunition market by increasing global demand for advanced and reliable artillery munitions. The conflict has highlighted the importance of modern, long-range, and precision-guided artillery systems, prompting many countries to accelerate their procurement and modernization efforts. The war has also exposed vulnerabilities in existing ammunition stockpiles, encouraging countries to accelerate production and stockpiling efforts. Countries involved and allied nations are prioritizing modernization to enhance their firepower capabilities. Russia is rapidly rebuilding its artillery shell stockpile to be three times larger than the U.S. and Europe's combined, while also producing significantly more tanks annually.

Moreover, NATO is supporting Ukraine through its initiatives aiming to enhance the defense production and supply capabilities. For instance, in January 2024, NATO finalized contracts to purchase around 220,000 artillery shells worth USD 1.2 billion, reflecting increased efforts to replenish member states’ ammunition stocks amid ongoing conflicts. These contracts, part of NATO’s Defense Production Action Plan, totaled around USD 10 billion in ammunition purchases, which included missiles and aircraft. Challenges such as the increasing need for artillery ammo production to address the ongoing conflict are expected to drive the product demand.

In addition, other countries are also taking the initiative to strengthen Ukraine’s artillery production. Various countries are driving efforts to supply Ukraine with artillery shells, sourcing munitions to meet the urgent defense needs of Ukraine. For instance, in August 2024, Norway approved the transfer of Nammo defense technology to a Ukrainian firm to produce 155mm artillery shells. The transfer is supported financially through Norway’s Nansen Support Programme, with a budget of over USD 7 billion for aid from 2023 to 2027. Such efforts and developments to enhance military support and ammunition supply the expanding market.

Artillery Ammunition Market Trends

Advancement of Artillery Capabilities through Precision Guided Munitions (PGMs)

The traditional design of artillery ammunition relies on an unguided mechanism that follows a definite and fixed trajectory, which offers limited accuracy. Precision-guided munitions use advanced guidance systems to strike a target with greater accuracy. The availability of precision guidance to artillery projectiles has increased the demand for integration of PGMs into artillery systems to improve accuracy, performance, and impact. The use of PGMs in artillery is increasingly being adopted by military forces of various countries for accurate strikes and reduced collateral damage. For instance, in December 2024, the U.S. Navy Force and General Atomics Electromagnetic Systems (GA-EMS) solidified a contract for the extension of the range of LRMP 155mm precision-guided munitions. The LRMP is a 155mm artillery projectile designed to achieve a range exceeding 120 kilometers. The artillery system uses foldable wings and onboard guidance systems for accurate and precise target engagement and maximum damage.

Few manufacturers are developing programs to actively integrate and test Precision Guided Munitions (PGMs) into artillery systems. The main mission behind such programs is to fulfil the increased need for high accuracy and effectiveness in modern defense systems. For instance, in March 2023, BAE Systems test-fired a long-range, sub-caliber artillery round for the U.S. Army's XM1155 program, successfully hitting a target beyond the range of other precision-guided projectiles fired from the same cannon.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increase in Defense Expenditure and Rising Geopolitical Conflicts and Border Tensions to Propel Market Growth

Recent events indicate a rise in geopolitical tensions and conflicts globally. This is driven by factors such as the ongoing conflict in Russia and Ukraine, an increase in tensions between the U.S and China, and rising social and political instability in various regions. Moreover, these tensions and conflicts lead to nations focusing on strengthening their military capabilities by procuring new weapons and technologies. The nations that are experiencing territorial disputes or border threats aim to reinforce their border defense and improve their defensive capabilities by increasing the deployment of advanced ammunition such as artillery systems. Governments of various countries is increasingly partnering with key manufacturers for the procurement of advanced artillery ammunition systems. With the increase in defense budgets, nations are focusing on developing and acquiring advanced ammunition systems with enhanced range, precision, and lethality capabilities. In addition, the surge in defense spending has promoted extensive modernization of artillery systems across the globe.

Countries are investing heavily in modernizing their armed forces to enhance their capabilities and maintain a competitive edge. Particularly, countries are prioritizing the production of advanced artillery systems with the help of various programs to enhance their military capabilities and maintain a strategic advantage in volatile regions. For instance, in March 2024, the European Commission allocated USD 566.6 million from the (Act in Support of Ammunition Production, ASAP) program to bolster ammunition production. This program aims to increase the EU's capacity to produce 2 million artillery shells per year by the end of 2025. Such factors collectively are expected to drive the artillery ammunition market growth during the forecast period.

Market Restraints

High Development Costs of Advanced Systems Hinder Market Growth

As military forces across the globe transition toward the design and manufacturing of advanced artillery ammunition with precision-guided systems and extended range and performance, the cost of development increases significantly. Artillery ammunition supported by a precision-guided system, such as GPS or laser-guided rounds, is significantly more expensive than traditional artillery systems. These smart munitions are manufactured to achieve a high accuracy rate and maximum impact on the target. However, such advanced technology design and integration increase the overall production cost.

Such high pricing creates difficulties for countries with limited defense budgets to procure or produce such ammunition on a large scale. Moreover, such high production cost also hinders the ability to maintain and keep inventory of large stockpiles of ammunition, which is essential during prolonged conflicts or war-like situations. Therefore, this may lead to countries investing in the production of old and less effective artillery to manage their defense expenditure. Thus, overall high development cost is expected to hamper the growth of the market during the forecast period.

Market Challenges

Strict International Regulations and Export Controls Pose a Significant Challenge

The regulations related to the production and cross-border export act as a challenge for the market. These regulations, including international arms control treaties and stringent export licensing processes, significantly impact production and global trade. Moreover, the concerns about illicit or disapproved manufacturing of ammunition and the Arms Trade Treaty (ATT) add to the challenges in the market. Numerous countries adopt stringent regulations and export licensing procedures for artillery ammunition, which require permits and authorization for each transaction.

For instance, in 2024, the U.S. Department of Commerce’s Bureau of Industry and Security (BIS) announced an interim final rule (IFR) amending the Department’s licensing policy for exports of firearms, ammunition, and related components under its jurisdiction. The U.S. Bureau of Industry and Security (BIS) has increased scrutiny of firearm and ammunition exports to prevent diversion to foreign criminals, gangs, terrorists, or other malicious actors. In addition, the production of traditional artillery ammunition can involve toxic chemicals, raising environmental concerns and potentially leading to further restrictions on manufacturing processes and exports. Therefore, stringent regulations and the need to comply with safety standards are expected to lead to higher production costs for ammunition manufacturers, creating challenges for the growth of the market.

Market Opportunities

Increase in Development of Rocket-Assisted and Ramjet Propelled to Drive Market Growth Opportunities

There is an increase in the development of rocket-assisted artillery ammunition, driven by the need for increased range, accuracy, and lethality in modern weapon systems. Adoption of such a system is due to its ability to engage targets at longer distances, exceeding the capabilities of a traditional artillery round. The system makes use of a small motor to propel the round ahead. Moreover, the modern rocket-assisted artillery uses precision guidance systems to enhance the accuracy and overall performance of the artillery ammunition system. Many countries are investing in the development and production of these advanced ammunition types to enhance their artillery capabilities.

Moreover, there is a rise in the integration of ramjet engines in artillery ammunition to meet the evolving needs of modern warfare. Ramjet technology enables sustained high-speed flight, which only enhances the shell’s kinetic impact and improves the accuracy of the system. Many manufacturers are focusing on integrating ramjet technology into artillery shells for enhanced range, speed, and precision. For instance, in May 2025, Nammo revealed a 155mm artillery shell equipped with a solid-fuel ramjet engine. The advanced system has a range of 150 km, and it exceeds all the capabilities of traditional artillery systems. In addition, other companies such as are also designing artillery rounds installed with ramjet technology. For instance, in May 2025, Tiberius Aerospace provides TRBM 155HG 155mm artillery round announced the launch of its first defense product, the Sceptre TRBM 155HG, a 155mm ramjet-powered artillery round designed for long-range precision strike missions up to 150 km. Therefore, such developments and advancements in the traditional artillery ammunition to achieve extended range is expected to present opportunities for the growth of the market during the forecast period.

Segmentation Analysis

By Munitions Technology

Conventional Segment Held Largest Share Due to Suitability and Affordability

On the basis of munitions technology, the market is classified into conventional munitions, Precision-Guided Munitions (PGMs), smart munitions, and extended-range munitions.

The conventional munitions segment held the largest market share of 54.48% in 2026. The segment is experiencing growth due to its widespread adoption in the military and armed forces industry globally. These munitions are a suitable option for the military forces as they are cost-effective and affordable for bulk production or stockpiling. They are compatible with most existing artillery systems; therefore, they are used extensively by military forces without modification and alteration.

The Precision-Guided Munitions (PGMs) segment is expected to grow fastest during the forecast period. The segment is growing owing to the increase in importance of advanced artillery systems equipped with inertial navigation systems in modern warfare and warlike situations. They are used by the forces to achieve mission goals with fewer rounds and enhanced operational efficiency. Moreover, the increase in advancement in guidance technologies and their integration in artillery rounds to improve the performance and accuracy of the system is expected to drive the growth of the segment. For instance, in 2024, at MSPO 2024, Poland's Defense unveiled its new 155mm Precision Guided Ammunition with laser guidance, capable of hitting targets up to 20 km away, enhancing Poland’s artillery capabilities. The munitions are designed for use with Krab and Kryl howitzers, with proven reliability beyond 8 km.

To know how our report can help streamline your business, Speak to Analyst

By Munitions Type

High-Explosive (HE) Segment to Lead Due to Its Widespread Use in Anti-Personnel Operations, Anti-Structure Missions, and Area Denial

On the basis of munition type, the market is classified into High-Explosive (HE), Armor-Piercing (AP), Cluster Munitions, Smoke/Illumination/Incendiary, and Precision-Guided Munitions (PGMs).

The High-Explosive (HE) segment is expected to account for 41.63% of the market in 2026. The segment is witnessing growth as it is widely adopted for neutralizing the enemy personnel, fortification, and other applications. It is used across almost every artillery-capable military force across the globe. Numerous defense forces, such as the army, navy, are adopting high-explosive artillery ammunition for anti-structure and area denial operations. For instance, in September 2024, the Indian Navy plans to enhance its defense capabilities by introduction of High-Explosive Pre-Fragmented artillery shells, which are designed to target and neutralize drone swarms. Such developments create more demand for advanced high-explosive ammunition tailored to modern war threats such as drones, which is expected to stimulate the growth of the market.

The Precision-Guided Munitions (PGMs) segment is estimated to grow at the fastest CAGR over the forecast period. The segment growth reasons are an increase in the need for modernization of defense weapons and ammunition, and a huge investment in guided artillery systems to maintain precision in long-range artillery ammunition. Defense forces of various countries are investing in the development of extended-range precision artillery with the help of guidance systems. For instance, in December 2024, General Atomics Electromagnetic Systems (GA-EMS) was awarded a contract by the U.S. Navy through Advanced Technology International (ATI) to develop the Long Range Maneuvering Projectile (LRMP) Common Round. The LRMP is a highly advanced 155mm artillery projectile equipped with onboard guidance systems designed to significantly extend the range of traditional artillery systems.

By Caliber

Medium Artillery Calibers (105 - 155 mm) Segment Holds Largest Share Due to Its Widespread Platform Compatibility and Extensive Use

On the basis of caliber, the market is classified into small artillery calibers (below 105 mm), medium artillery calibers (105 - 155 mm), and large artillery calibers (above 155 mm).

Medium artillery calibers (105 - 155 mm) hold the largest share in the market as they are versatile and compatible with a wide range of artillery systems, such as towed, self-propelled, and rocket artillery. Most NATO and allied countries have standardized on 155mm artillery systems for interoperability and procurement on a large scale. Moreover, countries such as the U.S., Russia, and China aim to maintain large stockpiles of medium caliber ammunition, which is expected to fuel the demand for replenishment. Numerous armies are establishing production plants for the manufacturing of 155mm artillery munitions. For instance, in April 2025, the U.S. Army and General Dynamics Corporation opened a new facility in Camden, Arkansas, to load, assemble, and pack 155mm high-explosive artillery munitions, enhancing production capacity. This move aims to strengthen the U.S. industrial base and ensure the timely delivery of key munitions to soldiers.

The small artillery calibers (below 105 mm) segment is estimated to be the fastest-growing, driven by rising demand for lightweight and highly mobile artillery systems, accounting for an 80.12% market share in 2026. There is a rise in the need for small-caliber artillery ammunition in modern and rapid deployable forces. The military forces are requiring precise and portable artillery ammunition in modern warfare and counterinsurgency operations, and tactical support, which is fueling the growth of the segment. For instance, in 2024, Rheinmetall announced a contract with Switzerland to produce 81mm mortar ammunition, with delivery by the end of 2025. The contract includes the manufacturing of MX2-KM mortars and various cartridges.

By Artillery System

Howitzers Segment to Hold Largest Share Due to Increased Utilization in Fire Control Systems

On the basis of the artillery system, the market is classified into howitzers, mortars, rocket artillery, and naval artillery.

The howitzers segment will remain the dominant component in the global market due to its increased deployment by modern armed forces for indirect fire support and long-range targeting beyond the direct line of sight, supporting a wide range of ammunition types, accounting for a 54.24% market share in 2026. They are extensively used in both towed and self-propelled configurations. Moreover, numerous countries modernize and strengthen their military artillery capabilities through the procurement of howitzers for national defense. For instance, in 2024, Rheinmetall announced a USD 152.8 million contract with Germany to supply 22 PzH 2000 self-propelled howitzers and chassis for the German Bundeswehr. The order involves delivering 155 mm weapon systems, replacing systems previously supplied to Ukraine.

The rocket artillery segment is estimated to grow at the fastest CAGR over the forecast period. The segment is growing due to the increase in demand for long-range and quick strike capabilities. Rocket artillery systems are designed to provide rapid and large firepower over long distances. Rising adoption in emerging military powers is driving increased partnership contracts of defense forces of various countries with the rocket artillery system manufactures. For instance, in August 2024, Elbit Systems secured a USD 270 million contract to supply rocket artillery to an unnamed international client. The contract will be carried out over a period of four years.

By Operational Range

Medium Range Segment Holds Largest Share Due to Optimal Range Accuracy and Tactical Versatility

On the basis of operational range, the market is classified into short-range (below 20 km), medium range (20 - 50 km), and long range (above 50 km).

The medium range (20 - 50 km) segment holds the largest share in the market as it is a preferred choice of range for most army forces across the globe. The medium range artillery system offers suitable range, reach, and accuracy for conventional and common battlefield. It is increasingly used in various tactical applications such as counter-battery and immediate target suppression.

The long range (above 50 km) segment is estimated to be the fastest-growing as there are advances in precision-guided munitions, extended-range artillery shells, and a rise in emphasis on deep-strike capabilities. There is an increase in the adoption of long-range artillery systems as the military forces across the globe are investing heavily in developing long-range artillery ammunition to achieve increased impact and improve strike capabilities.

By Propulsion Type

Ballistic Segment Holds Largest Share Due to Its Ability to Provide Maximum Damage, Effectiveness, and Versatility

On the basis of propulsion type, the market is classified into ballistic, rocket-assisted, ramjet-propelled, and hybrid propulsion.

The ballistic segment holds the largest share in the market due to its utilization in conventional artillery systems across the global military forces, and its effectiveness around various targets such as personnel, vehicles, and structures. The ballistic rounds are dependent on simple and unguided propulsion, equipped with an explosive charge system. Thus, they are cost-effective and easy to manufacture and store in large quantities. Moreover, ballistic artillery rounds are suitable for medium-range indirect fire and suppression applications.

The rocket-assisted segment is estimated to be the fastest-growing segment as there is an increase in demand for enhanced range, improved accuracy, and heightened safety through advanced artillery munitions. Rocket-assisted projectiles (RAPs) utilize a rocket motor to propel the shell beyond the range of traditional artillery. Moreover, there is a trend to use RAPs with precision guidance systems, such as laser guidance or smart fuses, to improve accuracy at extended ranges. Countries collaborate with artillery system manufacturers for enhancing fire support capabilities with long-range, precision rocket systems. For instance, in 2024, Diehl Defence and Elbit Systems Land signed an agreement to collaborate on rocket artillery ammunition for the PULS and EuroPULS launchers, addressing Europe's growing demand for advanced rocket capabilities. The partnership will focus on delivering rockets and training munitions tailored to European and German military requirements. The EuroPULS launcher, developed jointly with KNDS Deutschland, aims to meet NATO standards.

Artillery Ammunition Market Regional Outlook

On the basis of region, the market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Artillery Ammunition Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America region captured 33.50% of the global market in 2025, generating USD 2.87 billion in revenue, and is projected to reach USD 3.12 billion in 2026. Countries in the region aim to assign a huge budget for expanding the production of artillery rounds. For instance, in May 2024, U.S. Congress doubled the funding to USD 6 billion for the purchase and production of 155mm artillery shells to replenish stocks depleted by supplies to Ukraine. Moreover, the U.S. market is growing due to increased military procurement, modernizing inventories, and supporting ongoing conflicts such as Ukraine. In addition, the Canada Army is planning to spend more than USD 6 billion to acquire new self-propelled howitzers and ground-based long-range rockets. Thus, such an increase in investment to enhance the artillery shell manufacturing is expected to drive the market growth. Furthermore, there is a rise in the integration of GPS and other laser guidance systems to transform traditional artillery. The U.S. market is projected to reach USD 2.97 Billion by 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 2.69 billion in 2025, accounting for 31.42% share, and is expected to reach USD 2.97 billion in 2026. Europe is witnessing growth in the market owing to various reasons, such as an increase in defense spending and the initiatives launched for military readiness. Moreover, various countries are advancing their artillery capabilities through production expansion. For instance, in March 2024, the European Union announced that it had allocated USD 567.3 million to boost the ammunition production capacity to 2 million shells annually by the end of 2025. Moreover, in June 2025, the U.K. government announced it to invest USD 2.02 billion to build six new factories to increase the production of domestic artillery production. The new production plant will support a full production cycle for both 155mm and 105mm shells. Such efforts to expand production capacities and investment in new technologies are expected to propel the growth of the market. The UK market is projected to reach USD 0.42 Billion by 2026, while the Germany market is projected to reach USD 0.6 Billion by 2026.

Asia Pacific

In 2025, Asia Pacific generated USD 1.95 billion, contributing 22.72% to global market revenue, and is projected to grow to USD 2.13 billion in 2026. The Asia Pacific region is experiencing robust growth, which is driven by an increase in geopolitical tension across the globe and a rise in defense modernization efforts. Geopolitical tensions, particularly in China, India, and South Korea, are prompting countries to enhance their artillery capabilities. India and China are significantly expanding their artillery capabilities to meet the evolving security needs of the military and assert their influence in a rapidly changing security environment. Moreover, China is prioritizing the integration of various technologies in artillery rounds to create an advanced artillery fleet. The Japan market is projected to reach USD 0.16 Billion by 2026, the China market is projected to reach USD 0.83 Billion by 2026, and the India market is projected to reach USD 0.51 Billion by 2026.

For instance, in April 2023, the Chinese military tested an AI-powered laser-guided artillery shell has an AI chip that is capable of processing speeds greater than current GPS-guided artillery shells. In addition, Indian companies are partnering with international artillery ammo manufacturers to begin the production of artillery systems. For instance, in May 2025, India's Reliance Defense announced a partnership with Rheinmetall to start a large-scale ammunition production. With this collaboration, Reliance's production facility is expected to produce 200,000 artillery shells, 10,000 tons of explosives, and 2,000 tons of propellants. Thus, such initiatives to promote the large-scale production of artillery shells in various countries in the region is expected to fuel the regional market growth.

Latin America and Middle East & Africa

The market is growing at a moderate rate in Latin America and the Middle East & Africa region. The Latin America market generated USD 0.56 billion in 2025, representing 6.54% of the global market landscape, and is expected to reach USD 0.6 billion in 2026. The industry is significantly influenced by various reasons such as internal security concerns, border tensions, and regional instability. Countries in the Latin America region are focusing on the modernization of weapons and equipment to enhance their military capabilities. For instance, in May 2024, Brazilian Army's Logistics Command awarded a contract to Elbit Systems Land as part of the VBCOAP 155mm SR program for the supply of self-propelled 155mm howitzers. The VBCOAP 155 mm SR program plans to purchase 36 artillery systems for the Brazilian Army by 2034.

Moreover, the countries in the Middle East & Africa region are experiencing increased interest in upgrading their military forces with artillery systems and extended-range ammunition. Middle East & Africa recorded a market size of USD 0.29 billion in 2025, capturing 3.37% of the global market share, and is projected to reach USD 0.3 billion in 2026. In addition, the defense sector in the region is aiming to collaborate with different artillery rounds manufacturers to promote self-reliance in defense production. For instance, in February 2024, Saudi Defense Industry announced a partnership with KNDS to design and develop the SABIR guided artillery ammunition, a strategic step aligned with Saudi Vision 2030. Such developments to increase the domestic production of artillery shells and reduce reliance on imports are expected to propel the growth of the market in the region.

Competitive Landscape

Key Market Players

Key Players Focus on the Investment in Artillery Ammunition and Strategic Partnerships to Enhance Their Market Presence

The artillery ammunition market is highly competitive, driven by a rise in global defense budgets, technological advancements, and the increasing importance of artillery ammunition in the military sector. Some of the top players in the industry are such as Rheinmetall, BAE Systems, Lockheed Martin Corporation, Hanwha Aerospace, General Dynamics Ordnance, Tactical Systems, and others, are collaborating with the defense industries of various countries across the globe. Moreover, leading companies maintain their dominance and increase their market share through investment in ammunition production facilities, development of advanced propellants, and integration of various technologies such as ramjet engines, artificial intelligence, and inertial navigation systems into artillery systems. In addition, market players are also competing with each other by developing advanced, extended-range, and more precise artillery munitions. Moreover, they are also focusing on producing tailored artillery solutions and the components to match the requirements of the specific customer country.

LIST OF KEY ARTILLERY AMMUNITION COMPANIES PROFILED

- BAE Systems plc (U.K)

- Rheinmetall AG (Germany)

- Lockheed Martin Corporation (U.S.)

- Hanwha Aerospace (South Korea)

- General Dynamics Corporation (U.S.)

- Nammo AS (Norway)

- Elbit Systems Ltd. (Israel)

- Thales Group (France)

- KNDS (Netherlands)

- Denel SOC (South Africa)

- Poongsan Corporation (South Korea)

- CBC Global Ammunition (U.S.)

- Rostec(Techmash) (Russia)

- ST Engineering (Singapore)

- Arsenal JSCo (Russia)

- Munitions India Ltd. (India)

- Ukroboronprom (Ukraine)

- Roketsan (Turkey)

- IMI Systems (Israel)

- NORINCO (China)

- CSG Defense (Czech Republic)

- Arsenal JSco (Bulgaria)

- Leonardo S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS

- In April 2025, BAE Systems, a key player in the market, secured a USD 162 million contract to produce major structures for the M777 lightweight howitzer, with initial deliveries set for 2026. The first major structures will be produced at BAE Systems’ new multi-million-pound artillery development and production facility in Sheffield, U.K.

- In April 2025, South Korea’s Hanwha Aerospace announced a USD 253 million contract with India for a second batch of 100 K9 Vajra-T self-propelled howitzers, with the new units expected to be 60% locally manufactured in India.

- In January 2025, Rheinmetall secured a USD 23.90 million contract to supply tens of thousands of 155mm M107 artillery shells, with plans to boost production capacity to 1.1 million shells annually by 2027 amid rising global demand.

- In June 2024, Nexter, a part of KNDS, announced plans to significantly increase its propellant powder production capacities in partnership with Norwegian firm Nammo and Lithuanian company Valsts Aizsardzibas Korporacija (VAK). This initiative is supported by a USD 46.6 million grant from the European Commission under the ASAP (Act in Support of Ammunition Production) plan, aimed at strengthening artillery ammunition supplies for Ukraine.

- In February 2024, Nexter was awarded a major contract by the French Army Procurement Agency (DGA) to supply 109 of our CAESAr NG Mk II 155mm self-propelled howitzers. The total value of this contract is approximately USD 398.35 million.

REPORT COVERAGE

The report provides a detailed analysis of the sector and focuses on important aspects such as key players, technology, application, and propulsion, depending on various regions. Moreover, the research report offers deep insights into the market trends, competitive landscape, market competition, and market status, and highlights key industry developments. Additionally, it encompasses several direct and indirect factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 6.7% from 2025 to 2032 |

|

Segmentation |

By Munitions Technology

|

|

By Munitions Type

|

|

|

By Caliber

|

|

|

By Artillery System

|

|

|

By Operational Range

|

|

|

By Propulsion Type

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 8.57 billion in 2025 and is projected to reach USD 14.76 billion by 2034.

Registering a CAGR of 5.88%, the market will exhibit significant growth during the forecast period.

By munitions technology, the conventional munitions segment led the market.

BAE Systems plc (U.K.), Rheinmetall AG (Germany), Lockheed Martin Corporation (U.S.), Hanwha Aerospace (South Korea), General Dynamics Corporation (U.S.), and Nammo AS (Norway) are some of the leading players in the market.

The key factors driving the market are increased defense expenditure and rising geopolitical conflicts and border tension.

- 2021-2034

- 2025

- 2021-2024

- 240

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us