Asian Food Market Size, Share & Industry Analysis, By Product Type (Instant Noodles, Prepared Meals, Snacks, Sauces & Condiments, and Others), By Food Type (Vegetarian and Non-vegetarian), By Distribution Channel (Hypermarkets/Supermarkets, Convenience Stores, Grocery Stores, Online Sales Channels, and Others), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

KEY MARKET INSIGHTS

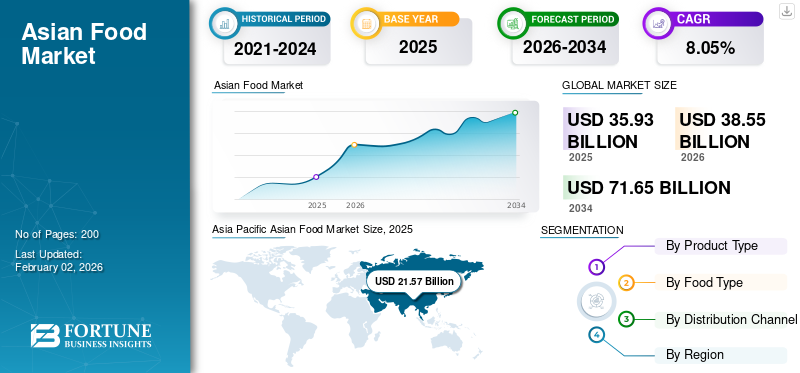

The global Asian food market size was valued at USD 35.93 billion in 2025. The market is projected to grow from USD 38.55 billion in 2026 to USD 71.65 billion by 2034, exhibiting a CAGR of 8.05% during the forecast period. Asia Pacific dominated the asian food market with a market share of 60.04% in 2025.

Asian food comprises a diverse range of products such as rice, noodles, seafood, and meats, made using traditional culinary practices from various Asian countries, including Southeast, Central, and other Asian countries. These products are made from aromatic herbs, spices, and seasonings such as ginger, garlic, lemongrass, and soy sauce to create a wide range of flavors, including sweet, sour, salty, and spicy. Increasing Asian culinary demand across the world is likely to be a key driver of market growth. In addition, the rising tourism sector in Asian countries and key players' promotional activities, such as new product launches, mergers and acquisitions, and partnerships to expand geographical reach, are likely to drive industry growth in the upcoming years.

Ajinomoto Co. Inc., Nissin Food Holdings, Toyo Suisan Kaisha Ltd., Unilever PLC, and Kikkoman Corporation are the major players operating in the industry.

Download Free sample to learn more about this report.

Global Asian Food Industry Key Takeaways

Market Size & Forecast:

- 2025 Market Size: USD 35.93 billion

- 2026 Market Size: USD 38.55 billion

- 2034 Forecast Market Size: USD 71.65 billion

- CAGR: 8.05% from 2026–2034

Market Share:

- Asia Pacific dominated the Asian food market with a 60.04% share in 2025, driven by high consumption of convenient and affordable packaged foods, urbanization, rising purchasing power, and the growing employment of women. Popularity of traditional flavors and authentic taste profiles also continues to strengthen regional demand.

- By product type, instant noodles held the largest market share in 2025, supported by their convenience and widespread global consumption. The snacks segment is projected to record the highest CAGR during the forecast period due to growing international demand.

- By food type, the non-vegetarian segment led in 2024, attributed to high protein content and essential vitamins. Vegetarian products are expected to grow strongly due to rising vegan and plant-based diet adoption in Europe, the U.S., and Asian countries like India and Indonesia.

- By distribution channel, hypermarkets & supermarkets dominated in 2024, offering convenience, variety, and physical access to products. Online channels are expected to witness the fastest growth due to flexibility and home delivery options.

Key Country Highlights:

- China: Rapid growth of prepared meals and high instant noodle consumption support strong market demand.

- Japan: Consumers favor traditional and premium Asian food products, driving industry innovation.

- United States: Increasing penetration of Asian food brands and new product launches expand market presence.

- Europe: Rising popularity of Asian cuisine and cultural migration bolster demand for prepared meals and snacks.

- South America: Urbanization and growing adult population drive consumption of packaged Asian foods.

- Middle East & Africa: Expanding tourism and changing lifestyles promote adoption of Asian cuisines.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Focus of Companies to Expand Their Production Capacities Propels Market Growth

Increasing interactions with different cultures and nationalities through travel & tourism, social media outreach, and media coverage have expanded the popularity of Asian cuisine across Western countries. Increased product demand, especially for snacks and prepared meals, is likely to foster market opportunities for key manufacturers. As a result, many companies are expanding their production plants into European and American countries. This geographical expansion allows key players to offer effective services and reach out to a larger consumer base in the market. These efforts are expected to significantly reshape the industry outlook and drive growth in the global Asian food market share within the food industry. For instance, in November 2024, CJ Foods, an Asian and Korean cuisine manufacturing company, expanded its global footprint by expanding its production plant in Europe and the U.S. The company plans to open 115,000 square meters in Budapest, Hungary, by the second half of 2026. In the U.S., the company planned to open a new Asian-style food manufacturing facility on a 575,000 square foot site in Sioux Falls, South Dakota.

MARKET RESTRAINTS

Presence of Allergens to Hamper Market Growth

Asian cuisines are primarily made from wheat, soy, fish, and nuts. Soy, wheat, and nuts are primarily considered food allergens in Western countries such as the U.S., the U.K., and Europe. According to the Food Allergy Research & Education report published in April 2024, there were 4.4 million people allergic to wheat, and 1.9 million people are allergic to soy in the U.S. Instant noodles, snacks, sauces, and condiments are primarily made from wheat, soy, and peanuts. Increasing privileges for allergenic foods among consumers will hamper the demand for Asian foods such as instant noodles, snacks, and prepared meals in the global market.

MARKET OPPORTUNITIES

Increasing Tourism in Asian Countries to Change Market Outlook

In the post-pandemic recovery phase, the tourism industry in Asian countries is increasing significantly. The growing appeal of unique cultural & environmental attractions paired with the rise in luxury travel is attracting a growing number of Western travelers to destinations such as Japan, Thailand, Singapore, and India. Efforts to simplify entry requirements, including the implementation of visa-free or visa-on-arrival policies, are making travelling more convenient and leading to an increase in tourist footfall in Asian countries. As a result, visitors are gaining exposure to Asian food habits, helping to familiarize global consumers with Asian ethnic foods. This trend will create more opportunities for the packaged and convenient Asian food products, such as instant noodles, snacks, sauces, fermented products, and others. It will change the industry landscape in the upcoming years and drive the global Asian food market growth with a lucrative growth rate. According to the UV Tourism statistics, Asia Pacific countries received 316 million visitors in 2024, representing an increase of 33% from 2023.

ASIAN FOOD MARKET TRENDS

Increased New Product Launches to Drive Market Growth

Asian snacks, desserts, and instant noodles are gaining popularity among consumers in Western countries due to their distinctive flavors, textures, and visual appeal. As the product demand is increasing across the globe, companies are emphasizing expanding their product range with unique flavors, healthy options, and convenient packaging. Increasing new product launches aimed at broadening product offerings and reaching a wider customer base is likely to drive the global market growth. For instance, in June 2025, Humza, one of the key frozen food brands, launched a premium range of Asian snacks, including samosas, spring rolls, kebabs, sausages, parathas, breaded chicken, frozen vegetables, premium hand-stretched naan breads, and many others in the U.K. and European markets.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Rising Convenient Meal Demand Boosted Consumption of Instant Noodles

Based on product type, the market is classified into instant noodles, prepared meals, snacks, sauces & condiments, and others.

The instant noodles segment held the highest share of the market in 2024. Instant noodles are widely recognized as one of the most popular and convenient meal options globally, contributing to their rapidly growing consumption. According to the World Instant Noodles Association, the global instant noodles consumption reached 123,067 million servings in 2024, an increase of 2.38% from 2023. Additionally, increasing ready-to-cook and ready-to-eat prepackaged food products will drive the segment’s growth.

The snacks segment is anticipated to witness the highest CAGR during the forecast period. Asian snacks such as samosas, chips, rice crackers, mochi, and momos are increasingly becoming popular in Western countries. Additionally, companies are launching new products in the snacks category to drive the segment’s growth.

By Food Type

Non-Vegetarian Segment Led Owing to Its Numerous Benefits

Based on food type, the market is divided into vegetarian and non-vegetarian.

The non-vegetarian segment held the highest market share in 2024. Globally, consumers are opting for non-vegetarian foods that contain chicken, pork, and other meats. Meat products contain high protein and an abundance of essential vitamins and minerals such as iron, zinc, and B vitamins, including B12. These nutrients are essential for muscle growth, energy production, and overall health, making non-vegetarian food products most popular among consumers.

The vegetarian segment is expected to exhibit a strong growth trajectory during the forecast period. Emerging vegan and vegetarian diet practices in regions such as Europe and the U.S are likely to drive the demand for vegetarian and plant-based snacks and prepared meals. Furthermore, the growing vegetarian population in Asian countries such as India and Indonesia is likely to propel the segment’s growth during the forecast period.

By Distribution Channel

Hypermarkets & Supermarkets Segment Dominated Due to Its Convenience

Based on distribution channel, the market is fragmented into hypermarkets/supermarkets, convenience stores, grocery stores, online sales channels, and others.

The hypermarkets & supermarkets segment exhibited the largest share of the market in 2024. These sales channels offer a wide variety of products, including categories such as instant noodles, prepared meals, snacks, and condiments. They offer a more convenient shopping experience, allowing users to physically check the quantity, quality, and product appearance before purchase. Thus, the convenience, physical presence, and offerings of multiple product options at a single store are likely to contribute to the segment’s prominence in the market.

Online sales channels such as retail platforms and D2C websites are anticipated to represent the highest CAGR during the forecast period. The online retail channels offer a flexible shopping experience and door delivery option to consumers. Additionally, they offer adequate product details and allow consumers to compare different product options available on the platform, helping consumers make buying decisions more wisely.

Asian Food Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Asian Food Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed 60.04% to the global market in 2025, with a valuation of USD 21.57 billion, and is projected to reach USD 23.15 billion in 2026, driven by the high consumption of convenient and affordable packaged foods across the region. Increasing urbanization, purchasing power among adults, and increasing women's employment rate are significantly driving the convenience prepackaged food products such as prepared meals, snacks, and instant noodles. The traditional flavors, ingredients, and authentic taste profiles of packaged Asian food products continue to appeal to adults and younger consumers, further strengthening demand across the region.

China is one of the leading markets for Asian food products. Instant noodles, in particular, are one of the staple foods among Chinese consumers. According to the World Instant Noodles Association, the consumption of instant noodles reached 43,802 million servings in 2024. Additionally, the rapid growth of the prepared meals industry is contributing significantly to market growth. According to the National Bureau of Statistics of China, the prepared foods market is anticipated to grow average annual rate of 25% till 2026. Therefore, the market is anticipated to grow at a lucrative CAGR during the forecast period.

North America

In 2025, North America represented USD 6.63 billion, accounting for 18.45% of the worldwide market, and is projected to grow to USD 7.11 billion in 2026. Increasing penetration activities by leading brands are likely to drive demand for Asian food products across the region, especially in countries such as the U.S. and Canada. Additionally, Asian companies such as Nissin Foods and Ajinomoto are significantly investing in expanding their product offering to the U.S. and Canadian markets. This strategic move will contribute significantly to the region’s market growth in the coming years.

The U.S. is one of the key markets for the product within North America and globally. Thus, Asian manufacturers are introducing their product lines to strengthen their market presence. For instance, in February 2025, Calbee, a Japanese snack company, introduced authentic Asian style chips in the U.S. market. The products were introduced in multiple flavors, including Umami Salt, Thai-Style Yellow Curry, and others.

Europe

The European market generated USD 4.65 billion in 2025, representing 12.94% of the global market landscape, and is expected to reach USD 5.01 billion in 2026. The European market is anticipated to grow at a considerable rate during the forecast period. The increasing popularity of Asian culture and cuisine across the region is a major factor driving product demand. Increasing tourism and Asian migration into countries are further contributing to the industry's growth. Companies such as CJ CheilJedang and Jollibee Foods Corp are expanding their production plants to European countries such as Germany, Italy, France, and the U.K., which is likely to drive growth in the market during the forecast period.

South America

South America is expected to exhibit steady growth in the market during the forecast period. Growing urbanization and adult population in Brazil, Argentina, and Chile are fueling the popularity of instant noodles, packaged meals, and snacks in the region. Additionally, companies are focusing on entering the market with their existing product lines to tap into new customer segments, which is likely to push the industry growth. The market in Latin America reached USD 1.94 billion in 2025, representing 5.41% of total market revenue, and is projected to reach USD 2.07 billion in 2026.

Middle East & Africa

The Middle East & Africa market was valued at USD 1.14 billion in 2025, capturing 3.16% of global revenue, and is estimated to reach USD 1.22 billion in 2026. The Middle East & Africa region is one of the lucrative markets for Asian food manufacturers. Increasing tourism, paired with consumers' shifting lifestyles, is promoting the adoption of multiple cuisines in countries such as Saudi Arabia, UAE, South Africa, and Kenya. Additionally, companies are expanding their presence to Middle Eastern and African countries to gain a competitive edge, contributing to industry growth.

COMPETITIVE LANDSCAPE

Key Industry Players

New Product Developments and Geographical Expansion Strategies to Increase Sales

The global Asian food market is fragmented, with companies such as Ajinomoto Co. Inc., Nissin Food Holdings, Toyo Suisan Kaisha Ltd., Unilever PLC, and Kikkoman Corporation accounting for a significant share. Companies operating in the global Asian Foods industry are investing significantly in geographical expansion to European and American countries to tap into the rising global demand for Asian Cuisine. Additionally, companies are expanding their product portfolios to cater to changing consumer preferences in the market. Furthermore, companies are involved in strategic partnerships to strengthen their market share. These strategic activities help companies to stay competitive in a dynamic market.

LIST OF KEY ASIAN FOOD COMPANIES PROFILED

- Ajinomoto Co. Inc. (Japan)

- Nissin Food Holdings (Japan)

- Nestle SA (Switzerland)

- Toyo Suisan Kaisha Ltd. (Japan)

- Calbee Group (Japan)

- ITC Limited (India)

- Unilever PLC (U.K.)

- Kikkoman Corporation (Japan)

- Asians Food Products (India)

- ConAgra Brands (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Fine Choice Foods, a North American pioneer in refrigerated Asian-cuisine producing company, expanded its product range by introducing new products such as Pork Gyoza Dumplings with Chili Crisp Oil and Spicy Sriracha Chicken Spring Rolls under its SUMM! Brand.

- May 2025: Snaxfarm, a Thailand-based snacks manufacturing company, expanded its product range by launching coconut-based snacks for younger & health-conscious consumers across Asia Pacific, Europe, and the U.S. The product is available in corn cheese and spicy tomato flavors.

- April 2025: DDC Enterprise, Ltd., a leading multi-brand Asian consumer food company, signed a strategic partnership agreement with Hewen Agricultural Technology Limited, a premium prepared-meal producer, to scale delivery of ready-to-eat (RTE) solutions in E-commerce and direct-to-consumers across Mainland China.

- March 2025: General Mills, an American food manufacturing company, introduced its first ramen noodles under its brands, Old El Paso and Totino’s. Newly launched products are available in four flavors: Old El Paso Ramen Noodles – Fajita, Old El Paso Ramen Noodles – Beef Birria, Totino’s Ramen Noodles – Cheese Pizza, and Totino’s Ramen Noodles – Buffalo-Style Chicken Pizza.

- September 2024: Authentic Asia, one of the prepared meals brands, launched a new innovative line of single-serve frozen meals with authentic flavors of Asia, restaurant-quality ingredients, and at-home convenience in the U.S. The new product is available in Thai Style Coconut Curry Chicken, Thai Basil Stir-Fried Beef, Drunken Noodles, Sichuan-Inspired Chicken, Orange Chicken, Korean-Inspired Beef Noodles, and Kimchi Fried Rice categories.

REPORT COVERAGE

The global Asian food market report provides market size and forecast for all the segments. It includes details on the market dynamics and trends expected to drive the market during the forecast period. It offers information about the key regions, key industry developments, new product launches, and details on key countries' partnerships, mergers, and acquisitions. The global market analysis also covers a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.05% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Food Type

|

|

|

By Distribution Channel

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 35.93 billion in 2025 and is projected to reach USD 71.65 billion by 2034.

The market is expected to exhibit a CAGR of 8.05% during the forecast period (2026-2034).

The instant noodles segment led the market by product type.

The increasing focus of companies to expand their production capacities is a key factor driving market growth.

Ajinomoto Co. Inc., Nissin Food Holdings, Toyo Suisan Kaisha Ltd., Unilever PLC, and Kikkoman Corporation are the key market players in the industry.

Asia Pacific dominated the market in 2025.

Increased new product launches are the major factors that are expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us