Audiology Devices Market Size, Share & Industry Analysis, By Product (Hearing Aids {BTE, ITE, RIC / RITE, CIC / IIC, and Others}, Cochlear Implants, Bone Anchored Hearing Systems, and Diagnostic Devices {Audiometers, Tympanometers, Otoscopes, OAE Analyzers, ABR Systems, and Others}), By Age Group (Pediatrics and Adults), and Regional Forecast, 2026-2034

Audiology Devices Market Overview

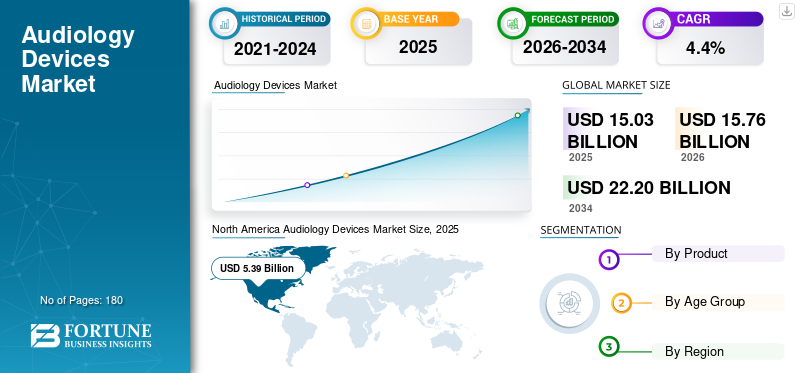

The global audiology devices market size was valued at USD 15.03 billion in 2025. The market is projected to grow from USD 15.76 billion in 2026 to USD 22.20 billion by 2034, exhibiting a CAGR of 4.4% during the forecast period. North America dominated the audiology devices market with a market share of 35.86% in 2025.

Audiology devices include hearing aids, bone conduction implants, cochlear implants, and diagnostic devices such as tympanometers, otoscopes, audiometers, OAE analyzers, and ABR systems. These devices are used to diagnose, screen, treat, and manage hearing loss across the population. The market growth is attributed to the increasing diagnostic rates of hearing loss, aging populations, and increasing access to care.

Furthermore, Sonova, Cochlear Ltd, and Demant A/S held the highest market share due to a diversified portfolio and strategic initiatives to expand their product reach.

Download Free sample to learn more about this report.

AUDIOLOGY DEVICES MARKET TRENDS

Shift toward AI and Connected Care to Emerge as a Key Trend

Currently, there has been an increasing shift from basic amplification toward intelligent, connected hearing ecosystems. An AI-based speech-in-noise improvement, discreet form factors, Bluetooth LE Audio, Auracast, rechargeable batteries, app-based personalization, and remote programming are becoming key differentiators.

These advancements are supporting a better user experience, improved adherence, and broader market penetration, while increasing the focus of key players on introducing such products.

- For instance, Phonak, a Sonova brand, launched its new Infinio hearing-aid portfolio, led by Audéo Sphere Infinio, to improve sound quality and speech clarity in noisy settings with real-time AI.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Prevalence of Hearing Loss and Expanding Access to Hearing Care to Fuel the Market Expansion

Over the past few years, the number of individuals with hearing loss due to conditions such as presbycusis, infections, and others has been increasing. Owing to this, there has been a growing treated population base, including especially older adults and individuals with mild-to-severe hearing impairment. This is encouraging key players to expand the availability of their products globally.

Moreover, increasing access to care is supporting the adoption of treatment products. Such a scenario is anticipated to drive the global audiology devices market growth over the forecast period.

- For instance, according to data from the World Health Organization (WHO) in March 2026, hearing loss becomes more common with age and more than 25% of people over 60 are affected by disabling hearing loss.

MARKET RESTRAINTS

High Device Cost and Reimbursement Gaps to Restrict Market Growth

Despite strong clinical need, the premium prescription hearing aids, cochlear implants, and follow-up care create a higher cost burden for patients and payers, leading to out-of-pocket costs. In many low- and middle-income countries, the reimbursement coverage is limited, which is expected to delay diagnosis and device uptake.

Even in developed markets, price sensitivity is driving the higher demand for OTC and lower-cost models, which, in turn, is expected to hinder market expansion over the forecast period.

- For instance, according to the Hearing Industries Association, in May 2026, on average, a prescription hearing aid is purchased from a hearing professional at a range of USD 1,000 to USD 4,000.

MARKET OPPORTUNITIES

Introduction of Advanced Testing Solutions Products to Create Significant Opportunities

In recent years, there have been significant advances in audiology equipment, including AI-enabled sound processing, app-based fitting, remote care, and consumer-electronics integration. These help reach underpenetrated users and increase awareness of these devices.

This is creating significant opportunities for key players to expand their portfolios through strong innovation and reach patients who may not yet visit audiologists frequently. Such a scenario is expected to support market expansion in the near future.

- For instance, in September 2024, Apple Inc. introduced AirPods 4 with a redesigned fit and brought new hearing health features to AirPods Pro 2, including Hearing Protection, Hearing Test, and Hearing Aid support.

MARKET CHALLENGES

Shortage of Audiologists in Emerging Countries to Challenge Market Expansion

Despite the growing need for audiology devices to address the significant burden of hearing impairment, the adoption of certain products is limited by the scarcity of key professionals. In several developing countries, such as India and Brazil, the ratio of audiologists per capita is below the global standard and recommendations.

Advanced technologies such as cochlear implants require professionally trained audiologists to operate, which emerging countries often lack. As a result, their adoption is delayed or limited in these countries, posing a major challenge for key players seeking to expand their offerings.

- For instance, as of May 2026, the Institute of Health Sciences (IHS), Odisha, reported that India had only 2,500 registered audiologists or 1 per 500,000 people. At the same time, the WHO recommendation suggests 1 per 25,000.

Segmentation Analysis

By Product

Widespread Distribution among End-users to Boost the Hearing Aids Segment Growth

Based on product, the market is segmented into hearing aids, cochlear implants, bone anchored hearing systems, and diagnostic devices. The hearing aids are further sub-segmented into BTE, ITE, RIC/RITE, CIC/IIC, and others. On the other hand, the diagnostic devices segment is subdivided into audiometers, tympanometers, otoscopes, OAE analyzers, ABR systems, and others.

To know how our report can help streamline your business, Speak to Analyst

The hearing aids segment accounted for the largest global market share in 2025 due to their strong healing attributes and high patient acceptance. Hearing aids are non-surgical and widely available at audiology centers, retail chains, clinics, and OTC channels. As a result, their sales are higher, which is anticipated to support the segmental expansion.

- For instance, the European Hearing Instrument Manufacturers Association (EHIMA) collectively sold 22.69 million hearing aids in 2024, marking a 4.0% increase over 2023.

Additionally, the cochlear implants segment is projected to grow at a CAGR of 4.9% during the forecast period.

By Age Group

High Volume of Chronic and Complex Acute Wounds to Drive the Segment Growth

Based on age group, the market is segmented into pediatrics and adults.

In 2025, the adults segment dominated the global audiology devices market share. This segment is expanding with age-related hearing loss, purchasing power, and insurance coverage in select markets. Moreover, an increasing number of older individuals is anticipated to drive the product demand in the coming years. Furthermore, the segment is set to hold a 91.3% share in 2026.

- For instance, according to the National Library of Medicine, 19.1% of India’s population will be over 60 years old by 2050.

In addition, the pediatrics segment is projected to grow at a CAGR of 4.0% over the forecast period.

Audiology Devices Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Audiology Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest market share in 2024, valued at USD 5.13 billion, and reached a valuation of USD 5.39 billion in 2025. The growth is driven by high awareness of hearing loss, strong audiology infrastructure, and the presence of leading manufacturers in the U.S., which is contributing to the greater product availability.

U.S. Audiology Devices Market

In 2026, the U.S. market reached a value of USD 5.23 billion, accounting for approximately 33.2% of the global market.

Europe

The Europe market is projected to record a growth rate of 3.5% during the projection period, the second-highest globally, reaching USD 1.46 billion by 2026. The growth is attributed to well-established healthcare infrastructure, higher diagnosis rates, and established audiology care networks, which are leading to higher adoption of prescription hearing aids and cochlear implants.

U.K. Audiology Devices Market

The U.K. market is expected to reach USD 0.90 billion by 2026, accounting for roughly 5.7% of global revenues.

Germany Audiology Devices Market

The Germany market is projected to reach USD 1.29 billion by 2026, accounting for approximately 8.2% of the global revenue.

Asia Pacific

By 2026, the Asia Pacific market is expected to reach USD 2.51 billion, ranking third globally. The growth is supported by a large untreated hearing-loss population, rising healthcare expenditure, and growing awareness in China, India, Japan, Australia, and Southeast Asia.

- For instance, according to the National Medical Journal of India, 3% of the country's population is living with hearing loss as of May 2026, underscoring the need for hearing solutions.

Japan Audiology Devices Market

The Japan market is estimated to generate USD 0.59 billion in revenue by 2026, capturing nearly 3.8% of the global market.

China Audiology Devices Market

The China market is expected to reach approximately USD 0.93 billion by 2026, representing nearly 5.9% of global revenues.

India Audiology Devices Market

The India market is expected to reach approximately USD 0.28 billion by 2026, accounting for around 1.8% of the global market revenue.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are expected to showcase moderate growth, with the Latin America market is predicted to reach USD 1.73 billion by 2026. The growth of these regions is mainly driven by improving healthcare access and the expansion of private audiology clinics.

GCC Audiology Devices Market

By 2026, the GCC market is estimated to reach approximately USD 0.68 billion, representing around 4.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Companies’ Strategic Initiatives and Diversified Portfolios to Strengthen their Market Positions

In 2025, Sonova, Cochlear Ltd, and Demant A/S held the majority of the global market share. These industry participants have strong brand reputation and well-established distribution worldwide. Further, they compete with an advanced product portfolio of hearing aids, cochlear implants, and diagnostic devices.

Moreover, key players are deploying strategic initiatives, such as partnerships and acquisitions, to expand their product reach. In addition, these companies are focusing on geographical expansion through new facility launches and distribution agreements to enhance market share.

LIST OF KEY AUDIOLOGY DEVICES MARKET COMPANIES PROFILED

- Cochlear Ltd (Australia)

- Sonova (Switzerland)

- Demant A/S (Denmark)

- WS Audiology A/S (Denmark)

- MED-EL Medical Electronics (Austria)

- GN Store Nord A/S (Denmark)

- Rudolf Riester GmbH (Germany)

- INVENTIS S.r.l. (Italy)

- Echodia (France)

- Path Medical GmbH (Germany)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Cochlear Ltd announced the FDA approval of the Cochlear Nucleus Nexa System, described as the world’s first smart cochlear implant system.

- February 2025: GN Store Nord A/S introduced ReSound Vivia, described as its most intelligent hearing portfolio and an AI-powered hearing aid family.

- August 2024: Sonova launched Audéo Infinio and Audéo Sphere Infinio, including real-time AI-based speech-from-noise separation technology.

- April 2024: Cochlear Ltd received FDA clearance to lower the indicated age for the Cochlear Osia System from 12 years to 5 years for selected hearing-loss conditions.

- September 2023: GN Store Nord A/S launched ReSound Nexia, including non-rechargeable RIE models and a rechargeable microRIE.

- February 2023: Demant A/S expanded its HearLink portfolio with new hearing aids powered by AI sound technology and SoundProtect, designed to reduce wind, handling, and transient noise.

- September 2022: Sony Corporation and WSA entered a partnership to jointly develop and supply OTC self-fitting hearing aids, starting with the U.S. market.

REPORT COVERAGE

The report provides a comprehensive analysis of all covered segments, along with an assessment of key drivers, trends, opportunities, restraints, and challenges in the audiology devices market. It further includes insights into technological advancements, the prevalence and incidence of hearing loss, key industry developments, company market share analysis, and detailed profiles of leading market participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.4% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Age Group, and Region |

| By Product |

|

| By Age Group |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 15.03 billion in 2025 and is projected to reach USD 22.20 billion by 2034.

In 2025, the North America market value stood at USD 5.39 billion.

The market is expected to grow at a CAGR of 4.4% over the forecast period of 2026-2034.

The hearing aids segment led the market in terms of product in 2025.

The key factors driving the market are the rising prevalence of hearing loss and expanding access to hearing care.

Sonova, Cochlear Ltd, and Demant A/S are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us