Automotive 3D Printing Market Size, Share & Industry Analysis, By Offering (Hardware and Software), By Vehicle Type (Hatchback & Sedan, SUV, LCV, and HCV), By Material (Metals, Polymers, Ceramics, and Composites), By Application (Rapid Prototyping & Design Validation, Tooling, Jigs & Fixtures, Production Parts/End-use Manufacturing, and Spare Parts & Aftermarket), By Propulsion Type (ICE and EV), and Regional Forecast, 2026-2034

Automotive 3D Printing Market Size and Future Outlook

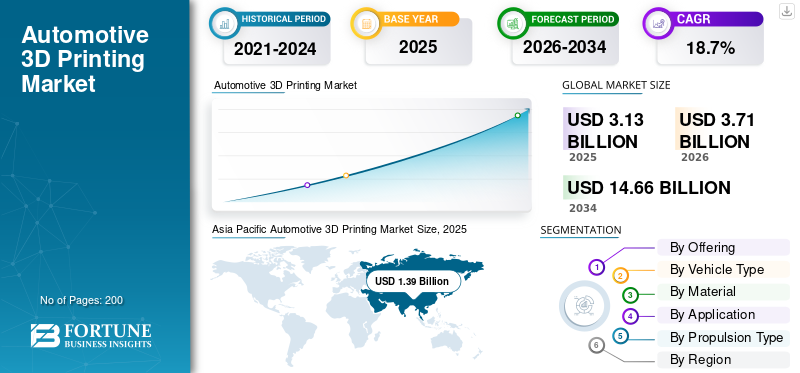

The global automotive 3D printing market size was valued at USD 3.13 billion in 2025. The market is projected to grow from USD 3.71 billion in 2026 to USD 14.66 billion by 2034, exhibiting a CAGR of 18.7% during the forecast period. Asia Pacific dominated the automotive 3d printing market with a market share of 44.41% in 2025.

The automotive 3D printing market refers to the use of additive manufacturing technologies to design, prototype, and produce automotive components and tools. It enables rapid prototyping, lightweight part production, customization, and cost-efficient manufacturing. Automotive OEMs and suppliers adopt 3D printing systems to improve design flexibility, reduce lead times, optimize performance, and support low-volume or complex part manufacturing processes across passenger and commercial vehicles.

Key market drivers include rising demand for rapid prototyping, cost reduction in low-volume production, lightweight and complex part manufacturing, shorter product development cycles, and increased customization. Advancements in 3D printing materials and technologies, along with growing adoption by automotive OEMs for tooling, jigs, and end-use automotive parts, further accelerate market growth.

Major players in the market include Stratasys, 3D Systems, EOS, HP, Desktop Metal, GE Additive, Materialise, Renishaw, and SLM Solutions, competing through advanced additive manufacturing technologies, expanded material portfolios, automation, software integration, and partnerships with automotive OEMs to enable rapid prototyping and end-use part production.

Download Free sample to learn more about this report.

AUTOMOTIVE 3D PRINTING MARKET TRENDS

Integration of 3D Printing with Digital Manufacturing Ecosystems to Shape Market Trends

A key market trend is the integration of additive manufacturing with digital tools such as CAD, simulation software, digital twins, and automotive Industry 4.0 platforms. This integration enables real-time design optimization, predictive performance analysis, and seamless transition from design to production. Automakers are leveraging connected manufacturing environments to improve traceability, quality control, and production efficiency, positioning 3D printing as a core element of smart and digitally enabled automotive factories.

MARKET DYNAMICS

MARKET DRIVERS

Accelerated Product Development and Design Flexibility to Drive Market Growth

Automotive manufacturers increasingly rely on 3D printing to shorten product development cycles and enhance design flexibility. Additive manufacturing allows rapid prototyping, quick design iterations, and early validation of components without the cost and time constraints of traditional tooling. This capability is especially valuable as vehicle architectures evolve with electrification, lightweighting, and aerodynamic optimization. By enabling complex geometries and functional integration, 3D printing supports innovation while reducing development risks, making it a critical driver for faster, more efficient automotive engineering processes.

- In August 2024, Ford and Formlabs showcased how Ford used in-house SLA/SLS 3D printing to speed up iterative prototyping for the all-electric Explorer (e.g., mirrors, handles, charging port, and dashboard components), cutting prototype turnaround from days to hours and enabling more design iterations earlier in development.

MARKET RESTRAINTS

Lack of Standardization Across Materials and Processes to Restrain Market Growth

The market is restrained by the limited standardization of materials, printing processes, and qualification methods. Variations in printer technologies, material properties, and build parameters make it difficult for OEMs to ensure consistent performance across suppliers and production sites. This lack of uniform standards increases validation time, complicates supplier integration, and slows large-scale deployment, particularly for components requiring strict quality and performance consistency.

MARKET OPPORTUNITIES

Expansion of End-Use Part Manufacturing to Unlock New Growth Opportunities

Beyond prototyping, automotive OEMs are increasingly exploring 3D printing for end-use and functional part production. The 3D printing technology enables low-volume manufacturing, on-demand spare parts, and localized production, reducing inventory and logistics costs. This opportunity is particularly strong for customized interior components, lightweight structural parts, and replacement parts for legacy vehicle models. As materials become stronger, more durable, and meet higher certification standards, the shift from prototyping to serial production drives automotive 3D printing market growth.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Quality Consistency and Certification Requirements to Challenge Market Growth

Ensuring consistent quality and meeting stringent automotive certification standards remain a major challenge for the market. Variability in print outcomes, material behavior, and post-processing can impact part reliability and repeatability. Automotive applications demand high safety, durability, and regulatory compliance, particularly for structural or safety-critical components. Addressing these challenges requires robust process controls, standardized testing protocols, and close collaboration between printer manufacturers, material suppliers, and OEMs.

Segmentation Analysis

By Offering

Advanced Printers and Materials Adoption to Sustain Hardware Segment Dominance

Based on offering, the market is classified into hardware and software.

The hardware segment dominates the market due to high demand for industrial-grade printers, metal and polymer materials, and post-processing systems. Automotive OEMs and tier suppliers invest heavily in printers for prototyping, tooling, and low-volume production. Continuous upgrades in printer speed, build size, and material compatibility, along with capital-intensive purchasing cycles, sustain higher revenue contribution from hardware across automotive manufacturing facilities.

Software is the fastest-growing segment. It is expected to grow at a CAGR of 20.2% during the forecast period. The growing use of design optimization, simulation, workflow management, and digital twins is driving software adoption, especially as OEMs integrate 3D printing into connected, Industry 4.0 manufacturing environments.

By Vehicle Type

Rising Preference for SUVs and Complex Component Design to Drive SUV Segmental Dominance

In terms of vehicle type, the market is categorized into hatchback & sedan, SUV, LCV, and HCV.

The SUV segment dominates the market due to higher design complexity, greater part volumes per vehicle, and increased customization requirements. SUVs integrate larger interior components, lightweight structural parts, and functional prototypes, driving extensive use of additive manufacturing. Strong global demand for SUVs across electric and ICE platforms further accelerates prototyping, tooling, and low-volume part production, reinforcing sustained dominance.

The hatchback & sedan segment held the second-largest market share in 2025 and is expected to grow with a CAGR of 18.8% during the forecast period. Continuous platform refreshes, the electrification of compact cars, and cost effective prototyping needs sustain steady adoption of 3D printing across mass-market passenger vehicles.

To know how our report can help streamline your business, Speak to Analyst

By Material

Design Flexibility, Cost Efficiency, and Rapid Prototyping Needs to Propel Polymers Segmental Dominance

Based on material, the market is segmented into metals, polymers, ceramics and composites.

The polymers segment dominates the market due to its extensive use in rapid prototyping, tooling, interior components, and functional testing. Polymer materials offer cost advantages, faster print speeds, and greater design flexibility than metals and ceramics. Automotive OEMs widely use polymers for concept validation, lightweight parts, and customized components, making them the preferred material across both passenger and commercial vehicle development programs.

Metals is the fastest growing segment. It is expected to grow at a CAGR of 19.2% during the forecast period. Growing adoption of lightweight structural components, powertrain parts, and end-use applications, especially in electric vehicles, is driving accelerated demand for metal additive manufacturing.

By Application

Accelerated Design Iteration and Reduced Development Timelines to Drive Rapid Prototyping Dominance

Based on application, the market is segmented into rapid prototyping & design validation, tooling, jigs & fixtures, production parts/end-use manufacturing and spare parts & aftermarket.

Rapid prototyping & design validation segment dominate the market as OEMs and suppliers prioritize faster product development and early-stage testing. Additive manufacturing enables quick iteration of complex components, functional testing, and design optimization without expensive tooling. This application is critical as automakers adapt to electrification, lightweighting, and frequent model updates, ensuring consistent demand across passenger and commercial vehicle programs.

The production parts/end-use manufacturing segment is the fastest-growing over the forecast period. It is expected to grow at a CAGR of 20.0% during the forecast period. Improvements in material strength, process reliability, and certification support increasing adoption for low-volume and customized automotive components.

By Propulsion Type

Established Manufacturing Base and Continuous Model Refresh Cycles to Drive ICE Segmental Dominance

Based on propulsion type, the market is segmented into ICE and EV.

The ICE segment dominates with the largest automotive 3D printing market share, due to its vast global vehicle parc and well-established manufacturing ecosystems. Automakers extensively use 3D printing for prototyping engine components, transmission parts, tooling, and fixtures across ICE platforms. Frequent facelifts, regulatory-driven efficiency improvements, and cost optimization programs sustain consistent additive manufacturing demand, reinforcing the segment’s larger revenue share compared to emerging propulsion technologies.

The EV segment is the fastest-growing and is expected to grow with a CAGR of 19.5% over the forecast period. Rapid EV platform development, lightweighting requirements, battery component prototyping, and customization needs are accelerating the adoption of 3D printing across electric vehicle programs.

Automotive 3D Printing Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive 3D Printing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market and is the fastest growing region due to its large automotive production base, especially in China, Japan, South Korea, and India. Rising investments in EV manufacturing, cost-efficient prototyping, and localized component production fuel adoption. Strong presence of automotive OEMs, tier suppliers, and increasing government support for advanced manufacturing technologies, further accelerate demand, positioning the region as both the volume and growth leader.

China Automotive 3D Printing Market

China leads the automotive 3D printing adoption due to high vehicle production volumes, fast EV platform refresh cycles, and a dense supplier ecosystem. It is set to reach USD 0.96 billion in 2026 and will grow at a CAGR of 19.6% during the forecast period. OEMs and Tier-1s increasingly use additive manufacturing for rapid prototyping, battery-related component development, tooling aids, and low volume functional parts. Growing local availability of printers, materials, and service bureaus supports faster deployment across plants, reinforcing China’s dominant share.

India Automotive 3D Printing Market

India is the fastest-growing market as OEMs, startups, and suppliers adopt 3D printing to reduce development time and prototyping costs while supporting localization. It is likely to reach USD 0.15 billion in 2026 and will grow at a CAGR of 21.2% during the forecast period. Increasing use in jigs/fixtures, interior prototypes, and functional testing is accelerating as EV programs expand and engineering centers scale. Wider adoption by contract manufacturers and service providers further improves accessibility, driving rapid growth from a smaller base.

Europe

Europe holds the second-largest market share and is expected to grow at a CAGR of 18.9% over the forecast period. The region benefits from advanced automotive engineering, strong R&D intensity, and early adoption of additive manufacturing. Leading OEMs focus on lightweighting, sustainability, and precision manufacturing, driving steady use of 3D printing for prototyping, tooling, and end-use parts across premium and electric vehicle platforms.

Germany Automotive 3D Printing Market

Germany dominates Europe due to deep engineering capabilities and strong integration of additive manufacturing in product development and industrial workflows. It is expected to grow at a CAGR of 18.5% during the forecast period. OEMs and suppliers use 3D printing extensively for design validation, tooling, and increasingly for high-value, low-volume production parts particularly in premium and performance vehicles. The emphasis on precision, quality assurance, and digital manufacturing ecosystems sustains steady demand and continuous technology upgrades.

North America

North America represents the third-largest market, supported by early technology adoption and a strong presence of additive manufacturing solution providers. OEMs and suppliers in the U.S. and Canada actively use 3D printing for rapid prototyping, tooling, and the production of customized components. Ongoing investments in EV development, digital manufacturing, and Industry 4.0 integration sustain moderate but consistent growth across the region.

U.S. Automotive 3D Printing Market

The U.S. dominates North America with the broad adoption of 3D printing across OEMs, Tier suppliers, and service bureaus. It is expected to grow at a CAGR of 17.4% during the forecast period. Demand is driven by rapid prototyping, tooling, and fixtures for assembly lines, as well as by growing end-use production of customized or low-volume components. Continued investment in EV platforms, software-driven manufacturing, and distributed production models supports stable expansion and deeper integration of additive manufacturing into mainstream operations.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, shows gradual growth driven by expanding automotive assembly operations and increasing awareness of additive manufacturing benefits. Adoption is primarily focused on prototyping, tooling, and aftermarket spare parts to reduce lead times and import dependency. While market penetration remains limited, rising industrialization and localized manufacturing initiatives support long-term growth potential.

COMPETITIVE LANDSCAPE

Product Portfolio Expansion, Strategic Partnerships, and End-to-End Solutions Aid Players to Gain Competitive Advantage

The automotive 3D printing market is moderately competitive, with global additive manufacturing leaders and specialized technology providers focusing on innovation-led differentiation. Key players in the market, such as Stratasys, 3D Systems, EOS, HP, Desktop Metal, and GE Additive, compete by enhancing printer speed, build volume, accuracy, and material compatibility. Continuous advancements in metal and polymer printing technologies enable suppliers to address diverse automotive applications, ranging from rapid prototyping and tooling to low-volume production and functional components, strengthening their competitive positioning.

Competitive intensity is further driven by collaborations between 3D printing companies and automotive OEMs to develop application-specific and scalable solutions. Market participants increasingly offer integrated ecosystems combining hardware, materials, software, and post-processing to improve workflow efficiency and customer retention. Investments in service networks, localized production support, and aftermarket capabilities allow companies to differentiate their offerings while meeting automotive requirements for quality consistency, cost optimization, and faster time-to-market.

LIST OF KEY AUTOMOTIVE 3D PRINTING COMPANIES PROFILED

- Stratasys (U.S.)

- 3D Systems (U.S.)

- HP Inc. (3D Printing Division) (U.S.)

- EOS GmbH (Germany)

- Desktop Metal (U.S.)

- GE Additive (U.S.)

- Materialise (Belgium)

- Renishaw (U.K.)

- SLM Solutions (Germany)

- Carbon (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Hawk Ridge Systems added a broad suite of Stratasys industrial 3D printers to its portfolio, supporting automotive tooling and end-use parts production with expanded certified materials.

- February 2026: Stratasys published its 2026 additive manufacturing predictions, emphasizing increased use of 3D printing for automotive assembly aids, end-of-arm tooling, and service parts, driven by demand for flexibility and smarter production processes.

- November 2025: Stratasys announced a strategic investment and agreement with Tritone Technologies to enter metal and ceramics 3D printing, enhancing automotive metal part capabilities.

- April 2025: HP showcased its 3D printing ecosystem at RAPID + TCT, emphasizing sustainability and industrial adoption.

- December 2024: 3E EOS expanded additive manufacturing capabilities using Stratasys technology, adding multiple F3300 printers to enhance prototyping and production support across aerospace, defense, and automotive sectors.

- June 2024: HP unveiled breakthrough polymer and metal 3D printing innovations at Formnext, accelerating automotive production readiness.

- April 2024: Renishaw and Materialise announced a workflow integration partnership to increase efficiency and productivity on metal AM systems, optimizing build preparation and throughput.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 18.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, By Propulsion Type, By Vehicle Type, By Material, By Application, and By Region |

| By Offering |

|

| By Vehicle Type |

|

| By Material |

|

| By Application |

|

| By Propulsion Type |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.13 billion in 2025 and is projected to reach USD 14.66 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.39 billion.

The market is expected to exhibit a CAGR of 18.7% during the forecast period of 2026-2034

The ICE segment led the market by propulsion type.

Accelerated product development and design flexibility are the key factors driving the market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us