Automotive LiDAR Market Size, Share & Industry Analysis, By Technology (Mechanical LiDAR and Solid State LiDAR), By Range (Short-range (≤50 m), Medium-range (50–150 m), and Long-range (>150 m)), By Vehicle Type (Passenger Vehicles and Commercial Vehicles), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026-2034

Automotive LiDAR Market Size

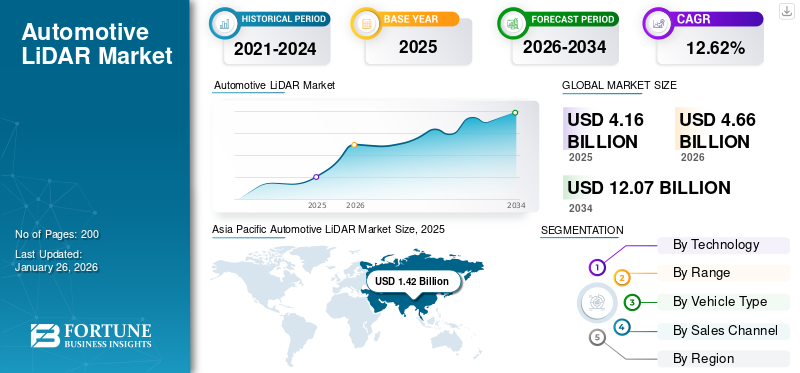

The global automotive LiDAR market size was valued at USD 4.16 billion in 2025 and is projected to grow from USD 4.66 billion in 2026 to USD 12.07 billion by 2034, exhibiting a CAGR of 12.62% during the forecast period. Asia Pacific dominated the medical devices market with a market share of 34.06% in 2025.

Automotive LiDAR (Light Detection and Ranging) is an advanced sensing technology that uses laser pulses to create high-resolution, 3D maps of a vehicle’s surroundings. It plays a critical role in enabling advanced driver-assistance systems (ADAS) and autonomous driving by providing accurate distance measurement, object detection, and real-time environmental perception even in low-light or poor weather conditions.

The automotive LiDAR is experiencing strong growth due to the rising demand for advanced driver-assistance systems (ADAS) and the accelerating development of autonomous vehicles. LiDAR (Light Detection and Ranging) technology provides high-resolution 3D mapping, object detection, and real-time environmental perception, making it a critical component for ensuring safety and reliability in next-generation mobility solutions. Increasing government regulations for vehicle safety, growing investments from automakers and tech companies, and the push for smarter transportation infrastructure are further fueling adoption. Additionally, advancements in solid-state LiDAR, cost reductions, and integration with AI-driven perception systems are making the technology more scalable and commercially viable, driving its rapid expansion across the automotive industry.

The market is dominated by a few key players, including Luminar Technologies, Valeo, Innoviz Technologies, Ouster (merged with Velodyne), Continental AG, Aeva Technologies, Hesai Technology, and RoboSense. These companies lead the market due to their strong partnerships with major automakers, technological innovation, and ability to produce automotive-grade LiDAR sensors at scale.

Download Free sample to learn more about this report.

AUTOMOTIVE LiDAR MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 4.16 billion

- 2026 Market Size: USD 4.66 billion

- 2034 Forecast Market Size: USD 12.07 billion

- CAGR: 12.62% from 2026–2034

- Asia Pacific dominated the automotive LiDAR market with a 34.06% share in 2025.

- The mechanical LiDAR segment is projected to lead the market with a 58.88% share in 2026.

- The medium-range (50–150 m) segment is expected to account for 38.93% of the market in 2026.

North America

North America is witnessing strong growth due to increasing deployment of ADAS technologies and expanding autonomous vehicle development programs.

Europe

Europe continues to advance steadily, driven by premium vehicle demand, strict safety regulations, and ongoing investments in transportation infrastructure.

Asia Pacific

Asia Pacific remains the largest regional market, supported by its dominant position in global vehicle production and rising adoption of autonomous driving technologies.

U.S.

The market is projected to reach USD 0.62 billion by 2026, supported by growing demand for advanced safety systems and connected vehicle technologies.

Japan

The market is projected to reach USD 0.20 billion by 2026, driven by the country’s strong automotive manufacturing base and focus on next-generation mobility solutions.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Technological Advancements to Propel Market Growth

The emergence of solid-state automotive LiDAR, MEMS-based LiDAR, and hybrid solutions has significantly improved sensor performance while reducing costs and enhancing durability, making them more suitable for large-scale commercial deployment. Unlike traditional mechanical LiDAR, these newer technologies offer compact designs with fewer moving parts, which lowers manufacturing expenses and increases reliability under harsh driving conditions.

For example, Luminar developed high-performance solid-state LiDAR with extended range capabilities, while Innoviz Technologies focuses on MEMS-based LiDAR solutions designed for mass-market vehicles. Similarly, companies such as Velodyne LiDAR and Quanergy Systems are pioneering hybrid and scalable LiDAR systems that balance performance with affordability. At the same time, continuous progress in miniaturization has made it possible to integrate LiDAR seamlessly into vehicles without compromising design or aerodynamics.

Additionally, improvements in range, resolution, and field of view are expanding LiDAR’s applications from advanced driver assistance systems (ADAS) to fully autonomous driving by enabling more accurate detection of objects, pedestrians, and road environments, even in complex scenarios. Together, these innovations, backed by LiDAR industry leaders, are making LiDAR more scalable, accessible, and practical for mass-market vehicles.

MARKET RESTRAINTS:

Regulatory & Standardization Issues to Restrict Market Expansion

The challenges in automotive LiDAR stem from regulatory uncertainty and a lack of standardized frameworks governing autonomous perception systems. As self-driving and assisted-driving technologies operate in safety-critical environments, governments and regulatory bodies demand rigorous validation, transparency, and conformity to safety features norms before allowing large-scale deployment. However, to date, there is no unified global standard for LiDAR performance, test protocols, fault tolerance, or interoperability with other sensors, which creates ambiguity for OEMs, suppliers, and technology vendors.

- For instance, in the U.S., the National Highway Traffic Safety Administration (NHTSA) regulates vehicle safety via the Federal Motor Vehicle Safety Standards (FMVSS), but these were not originally designed for autonomous systems. Thus, automated vehicles often require exemptions or special interpretations.

- In Europe, certain advanced autonomy functions are being regulated via specific rules such as UN-ECE Regulation 157 on Automated Lane Keeping Systems (ALKS) (a Level 3 capability), which became effective in the EU from January 2022 and has been adopted by 54 contracting parties. However, these regulations address only narrow functional domains (e.g., highway lane keeping) rather than holistic LiDAR sensor behavior across all driving contexts.

Due to this patchwork regulatory landscape, manufacturers must design systems that meet divergent demands across jurisdictions, which increases development cost, slows time to market, and raises compliance risk.

MARKET OPPORTUNITIES:

Autonomous Vehicle Development to Create Lucrative Growth Opportunities

The push toward autonomous vehicles present a major growth opportunity for automotive LiDAR technology, as these systems rely heavily on precise 3D sensing to navigate, detect objects, and make real-time decisions. According to the Autonomous Vehicle Industry Association (AVIA), autonomous vehicles have collectively driven over 44 million miles on U.S. public roads, demonstrating increasing real-world testing and deployment activity.

Moreover, government agencies such as the U.S. Department of Transportation are actively framing policies and regulatory roadmaps (e.g., the “AV 4.0” plan) to support the safe and synchronized integration of automated driving systems.

Together, these trends underscore that as autonomy advances from pilot trials toward commercial rollout, the demand for robust LiDAR systems capable of supporting Level 3-5 automation will rise sharply.

AUTOMOTIVE LIDAR MARKET TRENDS:

Shift toward Solid-state Architecturesand 4D LiDAR Technologies is a Significant Market Trend

The automotive LiDAR is witnessing a shift from conventional mechanical spinning LiDAR to solid-state architectures and 4D LiDAR (which combines range and velocity measurement). Solid-state LiDAR offers enhanced durability (no moving parts), smaller form factors, and lower costs, making it better suited for integration in consumer vehicles. Meanwhile, 4D LiDAR (often implemented via FMCW or related techniques) adds velocity as a measured dimension, enabling more precise object motion detection without additional sensors.

- For instance, companies such as Aeva are developing automotive-grade 4D LiDAR systems (e.g., their “Atlas” series) that measure distance and velocity for every point.

- In addition, firms such as RoboSense are producing solid-state LiDAR products tailored for automotive ADAS and autonomy applications.

MARKET CHALLENGES:

Technical Limitations in Automotive LiDAR to Hamper Market Growth

The automotive LiDAR perception systems face significant limitations in real-world operation, especially under adverse environmental conditions. According to an SAE technical study, LiDAR sensor performance degrades on average by 13.88 % for static objects and 16.16 % for dynamic objects when operating in rain, snow, or cloudy weather, underscoring how weather can erode detection accuracy.

Moreover, automotive LiDAR is susceptible to interference from ambient light, multipath reflections, occlusions, and limited signal-to-noise ratios in long-range or low-reflectivity scenarios. To address such variability, the SAE International formed an Active Safety System LiDAR Performance Task Force aimed at developing standardized methods and test procedures to evaluate LiDAR object-detection performance uniformly.

Download Free sample to learn more about this report.

Segmentation Analysis

By Technology

Reliability on Mechanical LiDAR Contributed to the Segment’s Growth

On the basis of technology, the market is classified into mechanical LiDAR and solid state LiDAR.

To know how our report can help streamline your business, Speak to Analyst

The mechanical LiDAR segment is expected to continue to dominate the market with a share of 58.88% in 2026, as it is a mature, proven technology that delivers wide field-of-view (FOV), full 360° scanning coverage, robust range, and high point-cloud density. Many early autonomous vehicle and ADAS implementations have relied on mechanical LiDAR (e.g., spinning LiDAR units) as they reliably scan the full surroundings, which is critical for high-speed driving and complex urban environments. According to surveys of sensor fusion and autonomous perception systems, mechanical LiDAR is identified as the “most popular long-range environment sensor” despite its drawbacks (e.g., moving parts, higher cost, and wear). As many certifications and performance benchmarks were developed using mechanical LiDAR architectures, deploying alternative technologies such as solid-state or MEMS LiDAR often faces hurdles in meeting existing performance expectations under varied real-world conditions. Consequently, OEMs and Tier-1 suppliers tend to prefer the known reliability of mechanical LiDAR when designing early autonomous systems.

Solid-state LiDAR is expected to register robust growth, driven by its cost efficiency, compact design, and increasing adoption across automotive and industrial applications. The segment is also fueled by the rising demand for high-performance sensing solutions.

By Range

Optimal Balance-to-Cost-ratio Boosted the Medium-range (50-150m) Segment Growth

In terms of range, the market is categorized into short-range (≤50 m), medium-range (50-150 m), and long-range (>150 m).

The medium-range (50-150m) segment captured the largest share of the market in 2024. In 2026, the segment is anticipated to dominate with a 38.93% share. The segment leads many automotive LiDAR deployments as it strikes an optimal balance between range, cost, resolution, and practical vehicle application requirements. In urban and suburban driving scenarios where most vehicles operate, LiDAR doesn’t always need to witness extremely far ahead (as in highway scenarios), but it must reliably detect obstacles, pedestrians, and vehicles several tens of meters away to enable safe decision-making, braking, and maneuvering. The 50-150 m band, therefore, provides sufficient coverage for most real-world ADAS and conditional autonomy tasks while avoiding the expense, size, and complexity of ultra-long-range systems. Moreover, many OEMs and ADAS standards are designed around this sweet spot range, so medium-range LiDAR sensors tend to hit required specifications more cost-effectively.

For Example:

- VanJee WLR-760 - A high-line automotive-grade LiDAR (192-line) which could be used in medium to longer range sensing setups. The long-range (>150 m) segment is expected to witness a robust CAGR of 14.3%, supported by significant technological advancements and expanding applications across commercial and passenger vehicles.

By Vehicle Type

Increasing Demand for Advanced Technology to Boost Passenger Vehicles Segment Growth.

Based on vehicle type, the market is segmented into passenger vehicles and commercial vehicles.

The passenger vehicle segment is expected to dominate the market with a share of 69.2% in 2026, as OEMs are beginning to integrate LiDAR as standard or widely optional hardware on mass-market EVs and advanced ADAS-equipped models, driving much larger unit volumes than niche robo-taxi or commercial fleets. The passenger car segment combines the largest global vehicle volumes with growing demand for higher-level driver assistance (and OEM marketing of safety/autonomy features). Chinese volume producers (BYD, Li Auto, and several Tier-1s) are already shipping LiDAR at scale, pushing prices down and enabling broad adoption. As a result, passenger vehicles account for the majority share of LiDAR units shipped today and are forecast to remain the primary growth engine for LiDAR revenues through the remainder of this decade.

- According to the Society of Indian Automobile Manufacturers (SIAM) in FY 2024-25, Passenger Vehicle (PV) domestic sales in India reached their highest ever at 4.30 million units, marking a 2 % growth over FY 2023-24.

The commercial vehicle market is poised for steady expansion, driven by strong economic activity, growth in e-commerce logistics, and supportive government policies for fleet modernization.

By Sales Channel

Growing Commitment of OEMs toward Enhancing Safety Capabilities to Encourage Segment Growth

Based on sales channel, the market is segmented into OEM and aftermarket.

Original Equipment Manufacturers (OEMs) are expected to dominate the market with a share of 69.08% in 2026, owing to their deep involvement in vehicle design, rigorous safety requirements, and long product life cycles. This dominance is reinforced by industry production trends.

- According to OICA, in 2024, world motor vehicle production reached 92.5 million units, continuing a pattern of annual growth in vehicle output.

The aftermarket segment is expected to witness significant growth, as aftermarket players increasingly focus on offering ADAS functionalities, thereby indirectly fueling the expansion of the automotive LiDAR.

Automotive LiDAR Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Automotive LiDAR Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed 34.06% to the global market in 2025, with a valuation of USD 1.42 billion, and is projected to reach USD 1.62 billion in 2026, bolstered by its overwhelming role in global vehicle production. According to OICA data, Asia remained the world’s largest vehicle-producing region in 2024, accounting for approximately 59% of global vehicle output. For instance, according to OICA, in 2024, the Asia Pacific accounted for 54.9 million of total vehicle sales. The increase in the number of vehicle production is indirectly boosting the LIDAR market in the region. China is expected to dominate the Asia Pacific market due to the rising demand for autonomous vehicles in the country. The Japan market is projected to reach USD 0.20 billion by 2026, the China market is projected to reach USD 0.73 billion by 2026, and the India market is projected to reach USD 0.42 billion by 2026.

Europe and North America

Other regions, such as Europe and North America, are anticipated to witness a notable growth in the coming years. In 2025, North America represented USD 1.1 billion, accounting for 26.42% of the worldwide market, and is projected to grow to USD 1.22 billion in 2026. The North America automotive LiDAR market is expected to dominate, driven by the aggressive adoption of advanced driver assistance systems (adas) and autonomous vehicle programs. The U.S. is expected to lead the North American region due to the growing demand for advanced features and enhanced road and vehicle safety. The U.S. market is projected to reach USD 0.62 billion by 2026.

The Europe market generated USD 0.98 billion in 2025, representing 23.48% of the global market landscape, and is expected to reach USD 1.09 billion in 2026. Europe continues to advance steadily, driven particularly by the premium and high-safety vehicle segments. The growth is further fueled by stringent government regulations and significant public infrastructure investments. The UK market is projected to reach USD 0.28 billion by 2026, and the Germany market is projected to reach USD 0.34 billion by 2026.

Rest of the World

Rest of the World contributed approximately USD 0.67 billion to the global market in 2025, accounting for 16.00% share, and is expected to reach USD 0.73 billion in 2026. Over the forecast period, the Rest of the world, involving Latin America and the Middle East & Africa regions, would witness a moderate Automotive LiDAR market growth. A key growth driver is the increasing vehicle production and sales, particularly in emerging economies where rising disposable incomes and the gradual shift toward electrification and premium vehicles are creating demand for advanced safety and driver-assistance systems.

COMPETITIVE LANDSCAPE

Key Industry Players:

Industry Participants Focus on Strategic Partnerships to Meet Diverse Industry Needs

The market is highly competitive and fragmented, with a large number of start-ups, specialized LiDAR technology providers, and established automotive suppliers all vying for partnerships with automakers. Numerous players are offering diverse LiDAR technologies such as mechanical, solid-state, MEMS, and flash LiDAR, each suited to different use cases (ADAS, autonomous driving, mapping, etc).

Luminar and Innoviz stand out for securing OEM production contracts with global brands such as Volvo, Mercedes-Benz, and BMW, while Valeo and Continental benefit from their Tier-1 supplier status and proven reliability in mass production. Meanwhile, Chinese players such as Hesai and RoboSense dominate in cost-effective, high-volume production, and firms such as Aeva and Ouster lead in advanced sensor architectures and mergers that expand market reach. Overall, dominance in this market stems from cutting-edge technology, OEM integration, cost efficiency, and large-scale production capability.

LIST OF KEY AUTOMOTIVE LiDAR COMPANIES PROFILED:

- Luminar Technologies, Inc. (U.S.)

- Valeo S.A. (France)

- Innoviz Technologies Ltd. (Israel)

- Continental AG (Germany)

- Aeva Technologies, Inc. (U.S.)

- Ouster, Inc. (U.S.) (merged with Velodyne LiDAR)

- Hesai Technology Co., Ltd. (China)

- RoboSense (Suteng Innovation Technology Co., Ltd.) (China)

- Quanergy Systems, Inc. (U.S.)

- Cepton, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- May 2025: Innoviz Technologies Ltd., a leading Tier-1 supplier of high-performance, automotive-grade LiDAR sensors and perception software, has announced an expanded collaboration with Volkswagen Autonomous Mobility. The partnership aims to accelerate the integration of InnovizTwo LiDAR units into the ID. Buzz AD, Volkswagen’s Level 4 autonomous shuttle.

- April 2025: Mercedes-Benz entered into a new agreement with Luminar Technologies to co-develop and integrate Luminar’s latest LiDAR system into its future vehicle models. The partnership with the German automotive giant marks Luminar’s first agreement involving its smaller and more efficient Halo LiDAR sensors, coming at a time when automakers worldwide are accelerating efforts to develop safer autonomous vehicles.

- December 2024: Aeva, a leading company in next-generation sensing and perception technology, announced its participation in CES 2025 in Las Vegas. During the event, Aeva unveils and demonstrates its new, high-resolution 4D long range LiDAR sensor designed for automotive applications. The company also presented a preview of Torc’s autonomous Freightliner Cascadia commercial vehicle, which is equipped with Aeva’s 4D LiDAR technology, and highlighted a new in-cabin LiDAR collaboration.

- April 2024: Marelli, a leading global mobility technology supplier, and Hesai Group, a world leader in automotive LiDAR, announced a collaboration to combine Marelli’s advanced headlamp design with Hesai’s next-generation LiDAR technology.

- March 2024: Stellantis Ventures, the corporate venture arm of Stellantis N.V., announced an investment in SteerLight, a company developing a new generation of high-performance LiDAR (Light Detection and Ranging) sensing technology.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The automotive LiDAR market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTES | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.62% from 2026-2034 |

| Unit | Value (USD Billion) |

| By Technology |

|

| By Range |

|

| By Vehicle Type |

|

| By Sales Channel |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 4.16 billion in 2025 and is projected to reach USD 12.07 billion by 2034.

In 2025, the market value stood at USD 1.62 billion.

The market is expected to exhibit a CAGR of 12.62% during the forecast period (2026-2034).

The mechanical LiDAR segment leads the market by technology.

The key factors driving the market are increasing consumer and regulatory emphasis on vehicle safety.

Luminar Technologies, Inc. (U.S.), Valeo S.A. (France), Innoviz Technologies Ltd. (Israel), Continental AG (Germany), and Aeva Technologies, Inc., are some of the prominent players in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us