Automotive Clutch Market Size, Share & Industry Analysis, By Type (Friction and Non-friction), By Component (Clutch Disc, Pressure Plate, and Others), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

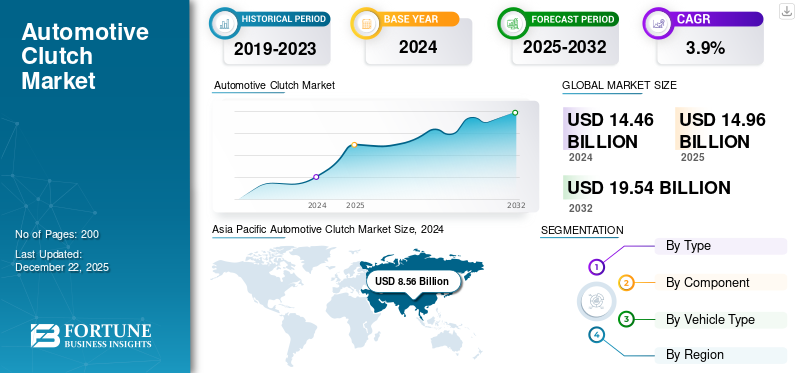

The global automotive clutch market size was valued at USD 14.96 billion in 2025. The market is projected to grow from USD 15.5 billion in 2026 to USD 21.27 billion by 2034, exhibiting a CAGR of 4.04% during the forecast period. Asia Pacific dominated the global market with a share of 59.4% in 2025.

The clutch is a mechanical device that connects and disconnects the engine’s power from the drivetrain. When the clutch pedal is pressed, it disengages the connection between the engine and the wheels, allowing the driver to change gears without damaging the transmission. Releasing the pedal re-engages the engine with the wheels, transferring power and allowing the vehicle to move.

Key players in the market include BorgWarner, Eaton Corporation, Exedy Corporation, Valeo, ZF Friedrichshafen AG, and Haldex. These players compete by developing new products and pricing strategies to strengthen their market presence.

One of the primary drivers of the automotive clutch industry is the steady increase in global vehicle production and sales. As emerging economies such as China, India, and Brazil witness rising disposable incomes and urbanization, there is a growing demand for personal and commercial vehicles. According to industry reports, global vehicle production is anticipated to increase in the coming years as manufacturers strive to meet the demand for combustion engine and electric vehicles (EVs). As the number of vehicles on the road continues to grow, so does the need for clutches, further driving the market’s expansion.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Focus on Fuel Efficiency to Augment Market Growth

Governments globally are implementing stringent regulations to reduce carbon emissions and improve fuel economy. Consumers are also becoming more conscious of their environmental footprint, leading to a higher demand for fuel-efficient vehicles. In response, automotive manufacturers are focusing on improving drivetrain technologies to enhance vehicle efficiency.

Clutches play a vital role in achieving these goals, enabling smoother gear transitions and improving engine performance. As manufacturers seek to develop lighter, more efficient vehicle systems, the demand for advanced clutch technologies that support these systems will surge. The emphasis on fuel efficiency and lower emissions is expected to remain a key driver of growth in the market.

Market Restraints

Transition to Electric Vehicles May Hamper Market Growth

The accelerating adoption of electric vehicles is one of the most significant trends reshaping the industry. As governments globally implement stricter emissions regulations and consumers increasingly prefer environmentally friendly alternatives, traditional internal combustion engine vehicles are gradually being replaced by electric counterparts.

Electric vehicles rely on electric motors for propulsion, which do not require traditional clutch systems. This shift poses a substantial challenge to the automotive clutch market growth, as the demand for conventional clutches may decline significantly. Manufacturers in the automotive clutch sector must adapt by diversifying their product lines and exploring innovative solutions such as traction control systems and integrated e-drives to remain relevant.

Market Opportunities

Increasing Adoption of Advanced Transmission Systems to Support Market Growth

The growing shift toward advanced automatic and semi-automatic transmission systems reshapes the clutch market. Dual-clutch automotive transmissions (DCTs) and continuously variable transmissions (CVTs) are gaining popularity due to their ability to improve engine performance and fuel efficiency. This rise in advanced transmission systems necessitates the development of specialized clutches, thereby boosting market opportunities for manufacturers.

Market Challenges

Increased Competition and Price Pressure on Demand for Automotive Clutches

As the automotive industry becomes increasingly globalized, competition among manufacturers and suppliers continues to intensify. With an influx of low-cost producers, especially from emerging markets such as China and India, established players are combating price pressures that could undermine their profit margins.

Companies capable of leveraging economies of scale are better positioned to offer competitive pricing, forcing others to either reduce their prices or innovate rapidly. This dynamic is pushing clutch manufacturers to optimize production processes, reduce costs, and engage in strategic partnerships or mergers to sustain their market presence. Furthermore, smaller companies often lack the resources to invest in technologies, face elevating challenges in keeping pace with large, more agile competitors.

Automotive Clutch Market Trends

Shift Toward Sustainability to Positively Influence Market Growth

There's an increasing focus on sustainability within the automotive sector, driven by stringent global emission regulations. This shift encourages manufacturers to develop lighter, more efficient clutch systems that consume less energy and produce fewer emissions. Clutches made from recyclable materials and those designed to improve energy efficiency are becoming more popular.

Impact of COVID-19

Disruption in Supply Chains Hampered Market Growth During Initial Stages of Pandemic

Before the pandemic, the market was on an upward trajectory, bolstered by increasing vehicle production and rising demand for passenger and commercial vehicles. The global market thrived on technological advancements and a growing focus on fuel efficiency and performance. With key suppliers affected by lockdowns and restrictions, the production of automotive components, including clutches, saw a swift decline. Raw materials, once readily available, became scarce, leading to project delays and increased operational costs. Manufacturers were forced to rapidly adapt by rethinking their supply chain strategies, leading to the establishment of more localized supply chains designed to mitigate future disruptions.

The COVID-19 pandemic compelled manufacturers to halt production lines temporarily. This downtime translated into lost revenue, layoffs, and uncertainty within the sector. The inability to operate at full capacity resulted in a backlog of orders, further complicating the landscape. Smaller market players in the automotive clutch industry struggled to survive, particularly those relying heavily on just-in-time manufacturing practices. As the industry transitions toward a more sustainable and technologically advanced future, manufacturers must navigate the changes in consumer behavior, supply chain dynamics, and emerging automotive technologies.

Segmentation Analysis

By Type

Non-Friction Clutches Led Market as They Can Handle High Torque Outputs and Power Heavier Vehicles Smoothly

Based on type, the market has been divided into friction and non-friction.

The non-friction segment is expected to account for 54.53% of the market in 2026. Today's engines, particularly downsized, turbocharged units, often produce substantial torque at low RPMs. Furthermore, the increasing popularity of SUVs and larger vehicles has increased the need for systems that can handle greater loads and vehicle weights. While friction clutches can be engineered for high torque, managing the heat generated during the necessary slip can be challenging in heavy-duty or performance applications. Non-friction clutches are well-suited to handle high torque outputs and power heavier vehicles smoothly. Their design allows for robust torque transfer without the direct contact pressure and wear associated with friction surfaces under extreme loads, contributing to durability in demanding applications.

The friction segment captured a market share of 45.7% in 2024, driven by demand in the commercial vehicle sector. These vehicles carry heavy loads and operate under immense stress. Manual transmissions and Automated Manual Transmissions (AMTs), which rely heavily on robust friction clutch systems, are widely preferred due to their ability to handle high torque loads dependably. Friction clutches in these applications are engineered for extreme durability and reliability under demanding conditions. For commercial fleet operators, vehicle uptime is paramount. Manual transmissions and clutch systems are known for their ruggedness and reliability compared to the more complex electronic and hydraulic systems commonly found in passenger vehicles’ automatic transmissions. When maintenance is required, it can often be simpler and quicker, an important advantage in minimizing downtime.

To know how our report can help streamline your business, Speak to Analyst

By Component

Rising Performance Upgrades in Heavy Commercial Vehicles Augmented Clutch Disc Segment Growth

Based on the component, the market is categorized into clutch disc, pressure plate, and others.

The clutch disc segment leads the market. The segment’s growth is primarily propelled by the massive and ever-growing global fleet of existing manual vehicles reaching their wear-and-tear replacement cycles. Supported by ongoing new manual vehicle sales in key segments and regions, the demand from performance upgrades and heavy-duty applications, and advancements in material technology, the clutch disc remains a critical and in-demand component. The others segment is expected to lead the market, contributing 38.77% globally in 2026.

The pressure plate segment is expected to witness rapid growth during the forecast period. While developed markets such as North America and parts of Europe have significantly shifted toward automatic transmissions (including traditional torque converter automatics, CVTs, and Dual-Clutch Transmissions), manual transmissions remain popular and often more affordable in many emerging economies. Vehicles with manual gearboxes continue to be mass-produced and sold in large numbers in these regions. Economic growth and a rising middle class in these markets are directly contributing to increased demand for vehicles that depend on conventional clutch pressure plates.

By Vehicle Type

Passenger Cars Dominated Market Due to Their Lower Manufacturing Costs

Based on vehicle type, the market is categorized into passenger cars, light commercial vehicles, and heavy commercial vehicles.

The passenger cars segment is anticipated to hold a dominant market share of 60.5% in 2026. In cost-sensitive emerging markets, manual transmissions often remain the standard due to their lower manufacturing costs and perceived simplicity and reliability compared to traditional torque-converter automatics. As the global car parc – the total number of vehicles on the road – continues to grow, particularly in Asia Pacific and Middle East regions, the sheer volume of manual transmission-equipped cars drives strong demand for clutches, both in new vehicle production and, crucially, in the aftermarket segments.

Light commercial vehicle is expected to capture a considerable market share during the forecast period. The rapid growth of online retail has created a massive and efficient logistics network, particularly for the "last mile" delivery. LCVs, ranging from small vans to larger delivery trucks, are essential to the primary vehicles for this crucial stage, operating in dense urban environments and making frequent stops. Construction, maintenance, and utility projects, especially in developing regions and urban centers, require LCVs for transporting materials, tools, and workers to diverse job sites.

Automotive Clutch Market Regional Outlook

By region, the market is divided into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Automotive Clutch Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is expected to capture the largest market share and grow at the highest CAGR over the forecast period. The Asia Pacific market was valued at USD 8.89 billion in 2025, capturing 59.40% of global revenue, and is estimated to reach USD 9.24 billion in 2026. The modern consumer in the region is increasingly tech-savvy, actively seeking vehicles equipped with state-of-the-art features. This demand extends to drivetrain components such as automotive clutches, as drivers prioritize performance, durability, and comfort. In response, manufacturers invest in research and development to create clutches that seamlessly integrate with smart vehicle systems, enhancing overall driving experiences. Additionally, the rising preference for performance vehicles, particularly in markets such as Japan and South Korea, has increased demand for high-performance clutches capable of handling extreme conditions, further intensifying competition across the regional market. The Japan market is anticipated to reach USD 1.47 billion by 2026. The China market is expected to achieve USD 5.25 billion by 2026. The India market is projected to reach USD 0.92 billion by 2026.

North America

North America contributed 17.54% to the global market in 2025, with a valuation of USD 2.62 billion, and is projected to reach USD 2.7 billion in 2026. Following dips during the global pandemic, vehicle miles traveled in North America have largely rebounded. Increased driving activities translate directly into wear and tear on automotive components, including the clutch systems. Stop-and-go traffic, common in many urban and suburban areas, places added strain on clutches, accelerating their degradation and increasing the need for replacement. As economic activity increases and travel resumes, aggregated mileage continues to climb, fueling product demand. The U.S. market is projected to reach USD 1.77 billion by 2026. The UK market is expected to attain USD 0.17 billion by 2026.

The increasing demand for automotive clutches in the U.S. reflects a confluence of shifting consumer preferences, burgeoning performance markets, and transformative technological advancements. As manual and hybrid vehicles gain traction and regulatory pressures heighten, the automotive clutch market is poised for substantial growth. Industry players must stay ahead of trends and invest in innovations to maintain a competitive edge, focusing on quality, performance, and sustainability.

Europe

Europe accounted for USD 2.92 billion in 2025, representing 19.51% of the global market share, and is projected to reach USD 3.01 billion in 2026. Europe held a considerable market share in 2024, remaining a key hub for automotive manufacturing. The region boasts a well-established ecosystem of automakers and suppliers. Recent years have seen a surge in vehicle production and sales, particularly in countries such as Germany, France, and Italy, home to several leading automotive brands. This increase in production naturally leads to a higher demand for clutches, reinforcing Europe’s strong position in the market. The Germany market is forecasted to reach USD 0.72 billion by 2026.

Rest of the World

The Rest of the World region captured 3.55% of the global market in 2025, generating USD 0.53 billion in revenue, and is projected to reach USD 0.55 billion in 2026. The rest of the world is expected to grow at a rapid CAGR during the forecast period. Vehicle manufacturers in Latin America, and Middle East & Africa are increasingly embracing technological innovations to improve vehicle performance. Enhanced clutch performance improves fuel efficiency and reduces emissions, aligning with global sustainability targets. Thus, the demand for high-performance clutches is poised to rise sharply in these regions.

Competitive Landscape

Key Market Players

New Product Developments and R&D Activities to Provide Competitive Edge to Industry Players

Various trends, challenges, and key players shape the competitive landscape of the global automotive clutch market. As the industry responds to changing consumer demands and technological advancements, product manufacturers must remain agile and innovative to maintain their competitive edge. With the growing focus on sustainability, electrification, and advanced technologies, the market is poised for continued growth and transformation in the years to come.

List of Key Automotive Clutch Companies Profiled

- BorgWarner (U.S.)

- Eaton Corporation (Ireland)

- Exedy Corporation (Japan)

- F.C.C. Co., Ltd. (Japan)

- Haldex (Sweden)

- NSK Ltd. (Japan)

- Valeo (France)

- ZF Friedrichshafen AG (Germany)

- Schaeffler AG (Germany)

- Setco (India)

Key Industry Developments

- June 2025 – Eaton Corporation launched a clutch for Asian trucks and expanded its portfolio in South America.

- May 2025 – BorgWarner signed a new DCT clutch deal with a Chinese manufacturer and extended a seven-year contract with a German OEM, enhancing its production presence in Tianjin and Taicang.

- May 2024 – Eaton showcased a comprehensive commercial vehicle clutch portfolio at Automechanika Frankfurt.

- January 2024 – Eaton Corporation added the remanufactured Advantage Line of Clutches to its portfolio.

- October 2023 – Clutch Industries launched the clutch system in the U.S. under the UniClutch brand.

Investment Analysis and Opportunities

Advancement of Materials and Technological Progressions to Generate Opportunities for Market Growth

As the industry moves forward, advanced materials are becoming critical to designing and manufacturing automotive clutches, leading to higher performance, durability, and reduced weight. Carbon composites, characterized by their high strength-to-weight ratio, are increasingly popular in clutch manufacturing. These materials offer superior thermal stability and wear resistance, essential for performance under extreme driving conditions. Ceramics offer outstanding thermal stability and friction properties. Clutches made from ceramic materials can withstand higher temperatures and pressures without degradation, making them ideal for high-performance and racing applications. Integrating smart sensors and IoT capabilities into clutch systems allows for real-time monitoring and analytics, enabling predictive maintenance and optimizing performance.

Report Coverage

The global automotive clutch market report analyzes the market deeply and highlights crucial aspects such as prominent companies, market segmentation, competitive landscape, and technology adoption. Besides this, the market research report provides insights into the automotive clutch market trends and highlights significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.04% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Component

By Vehicle Type

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market size was USD 14.96 billion in 2025 and is anticipated to reach USD 21.27 billion by 2034.

The market will exhibit a CAGR of 4.04% over the forecast period (2026-2034).

By type, the non-friction segment led the market in 2025.

Increasing focus on fuel efficiency is a key factor driving market growth.

Leading companies in the market include BorgWarner, Eaton Corporation, Exedy Corporation, Valeo, ZF Friedrichshafen AG, and Haldex.

Asia Pacific held the largest share of the global market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us