Automotive Differential Market Size, Share & Industry Analysis, By Type (Open Differential, Limited Slip Differential (LSD), Locking Differential, and Torque Vectoring Differential), By Drive Type (Front-Wheel Drive (FWD), Rear-Wheel Drive (RWD), and All-Wheel Drive (AWD)), By Vehicle Type (Hatchback/Sedan, SUV, Light Commercial Vehicle, and Heavy Commercial Vehicle), By Component (Mechanical, Electro-Mechanical, Electronic, and Others), and Regional Forecast, 2026-2034

Automotive Differential Market Size and Future Outlook

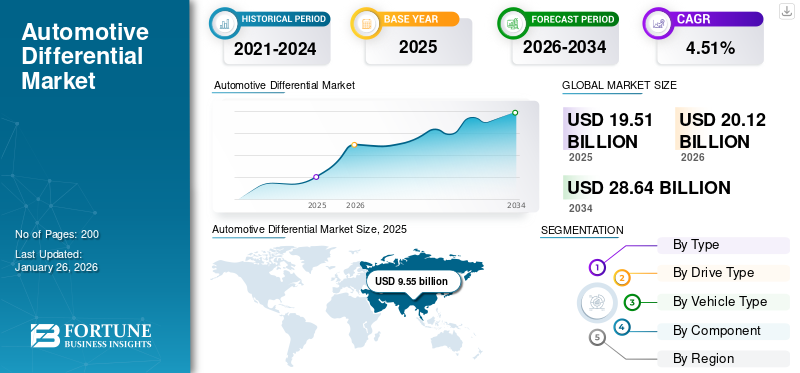

The global automotive differential market size was valued at USD 19.51 billion in 2025. The market is projected to grow from USD 20.12 billion in 2026 to USD 28.64 billion by 2034, exhibiting a CAGR of 4.51% during the forecast period. Asia Pacific dominated the automotive differential market with a market share of 48.7% in 2025.

Differentials play a crucial role in ensuring smooth cornering, stability, and traction by allowing wheels to rotate at different speeds. This market includes a wide range of differential types, such as open, limited-slip, locking, and torque vectoring systems, utilized across passenger cars, light commercial vehicles, and heavy-duty vehicles. Its growth is directly tied to advancements in drivetrain technologies and vehicle performance optimization.

The market encompasses applications in front-wheel drive (FWD), rear-wheel drive (RWD), and all-wheel drive (AWD) configurations. With increasing emphasis on vehicle safety, handling precision, and off-road capability, manufacturers are investing in technologically enhanced differential units to meet the evolving requirements of global automakers.

Major players in the automotive differential market include Dana Incorporated, ZF Friedrichshafen AG, GKN Automotive, Eaton Corporation, BorgWarner, JTEKT Corporation, and American Axle & Manufacturing. These companies focus on expanding their product portfolios through innovations in lightweight materials, electronic differential systems, and integrated driveline solutions.

Download Free sample to learn more about this report.

Automotive Differential Market KEY TAKEAWAYS

- 2025 Market Size: USD 19.51 billion

- 2026 Market Size: USD 20.12 billion

- 2034 Forecast Market Size: USD 28.64 billion

- CAGR: 4.51% from 2026–2034

- Asia Pacific dominated the automotive differential market with a 48.70% share in 2025.

- The open differential segment is projected to hold a 52.79% market share in 2026.

- The front-wheel drive (FWD) segment is projected to account for 51.71% of the market in 2026.

Asia Pacific

Asia Pacific held 48.70% of the global market in 2025, valued at USD 9.55 billion, and is projected to reach USD 9.89 billion in 2026.

Europe

Europe captured 25.40% of global revenue in 2025, with the market valued at USD 4.96 billion and expected to reach USD 5.12 billion in 2026.

North America

North America accounted for USD 3.79 billion in 2025, representing 19.60% of the global market, and is projected to grow to USD 3.88 billion in 2026.

U.S.

U.S. The automotive differential market is projected to reach USD 3.09 billion by 2026.

Japan

Japan The automotive differential market is anticipated to reach USD 1.39 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for All-Wheel Drive (AWD) and Sports Utility Vehicles (SUVs) Accelerates Market Growth

The surge in demand for SUVs and AWD vehicles is one of the most significant growth drivers for the automotive differential market. Consumers increasingly prefer vehicles that offer enhanced safety, stability, and versatility across various terrains. AWD systems depend heavily on differentials, typically a combination of center, front, and rear differentials, to efficiently distribute engine torque among all wheels. This ensures optimal traction and vehicle control, particularly in off-road conditions, slippery roads, or during cornering maneuvers. This trend is directly proportional to a higher adoption rate of advanced differential technologies. The SUV segment, accounting for a growing share of global vehicle sales, especially in Asia Pacific and North America, has pushed OEMs to adopt multi-differential setups to enhance driving dynamics. This development is likely to drive the automotive differential market growth during the forecast period.

- In 2024, Subaru and Toyota expanded their AWD lineups with vehicles equipped with advanced differentials, including electronically controlled and automatic limited-slip differentials (LSD), which enhance power distribution and improve handling. Toyota focused on expanding its electronically-controlled AWD systems, particularly for hybrid models, while Subaru improved its hybrid and all-electric AWD offerings.

MARKET RESTRAINTS

Shift Toward Electric Vehicles with Integrated E-Axles May Limit Market Growth

The rapid adoption of electric vehicles (EVs) is creating a technological shift that challenges the traditional differential market. Many EVs use e-axle or in-wheel motor systems, which integrate the motor, power electronics, and differential function into a single unit. This reduces the requirement for separate mechanical differentials. As manufacturers increasingly focus on simplifying EV drivetrains to minimize energy loss and weight, conventional differential manufacturers face declining demand in fully electric segments. For instance, Tesla’s Model S Dual Motor system electronically manages front and rear torque distribution, offering superior traction and dynamic control without mechanical differentials. Thus, the shift toward electric vehicles with integrated e-Axles may limit market growth.

MARKET OPPORTUNITIES

Growth in Off-Highway and Commercial Vehicle Applications to Create Lucrative Growth Opportunities

The expanding off-highway and commercial vehicle sector presents a substantial opportunity for the automotive differential market. Vehicles used in construction, mining, agriculture, and logistics require robust, high-torque differentials to operate efficiently under heavy loads and challenging terrains. These applications demand enhanced traction, load-bearing capability, and durability, driving OEMs and component suppliers to innovate in locking and limited-slip differential technologies. Increasing global investments in infrastructure and mining activities are also contributing to higher demand for heavy-duty trucks, tractors, and earthmoving equipment equipped with advanced drivetrain systems.

- In 2024, Eaton Corporation revealed that it had been chosen by a major electrified vehicle manufacturer to provide its advanced ELocker differential system for an upcoming electric and hybrid vehicle SUV model. This innovative system marks a departure from conventional PHEV configurations, which typically rely on a combination of an internal combustion engine (ICE) and an electric motor to drive all wheels. Instead, the new SUV utilizes an electric motor to power the rear wheels, while the front axle is driven by either an additional electric motor or an optional ICE, offering improved traction, efficiency, and drivetrain flexibility.

AUTOMOTIVE DIFFERENTIAL MARKET TRENDS

Growing Adoption of Smart and Connected Drivetrain Systems is a Significant Market Trend

The increasing digitalization of vehicles is driving a major trend toward the adoption of smart and connected differential systems, transforming traditional mechanical components into intelligent, software-driven modules. Modern vehicles now integrate Electronic Control Units (ECUs), sensors, and communication interfaces that continuously monitor torque distribution, wheel speed, and traction levels. This enables real-time adjustments in differential operation, enhancing vehicle stability, handling precision, and overall safety under dynamic driving conditions. As automakers advance toward autonomous and ADAS-equipped vehicles, these connected differentials are becoming essential for predictive control and energy optimization. This development is expected to drive market growth during the forecast period.

Download Free sample to learn more about this report.

MARKET CHALLENGES

Volatility in Raw Material Prices and Supply Chain Disruptions to Hinder Market Expansion

The automotive differential market faces a significant challenge due to fluctuating raw material prices and ongoing global supply chain disruptions. Differential systems rely heavily on high-grade steel, aluminum, and alloy materials for gears, shafts, and housings. Any volatility in the prices of these materials directly impacts production costs and profit margins for manufacturers. Additionally, the increasing adoption of advanced electronic differential systems has heightened dependency on semiconductors, sensors, and precision components, which remain vulnerable to global shortages and logistics bottlenecks, hampering market growth. For instance, during 2023 and early 2024, several leading suppliers, including Dana Incorporated and Eaton Corporation, experienced production delays and cost escalations due to semiconductor supply issues and rising steel prices. These disruptions affected delivery schedules to OEMs and hindered innovation cycles and new product launches.

Segmentation Analysis

By Type

High Compatibility Across Passenger Cars Leads Open Differential Segment Expansion

On the basis of type, the market is classified into open differential, limited slip differential (LSD), locking differential and torque vectoring differential.

The open differential segment dominates the global market, primarily due to its low cost, mechanical simplicity, and high compatibility across passenger cars, light commercial vehicles, and entry-level SUVs. Open differentials effectively balance torque between wheels under normal driving conditions, making them ideal for vehicles operating on paved roads and moderate terrains. Their design requires minimal maintenance, providing a cost advantage for OEMs targeting high-volume production in emerging markets. This dominance is further reinforced by advancements in materials and lightweight engineering aimed at improving performance, efficiency, and fuel economy. The open differential segment is projected to dominate the market with a share of 52.79% in 2026.

By Drive Type

High Production of Compact and Mid-Segment Vehicles Drives Dominance of Front-Wheel Drive (FWD) Differential Segment

By drive type, the market is segmented into Front-Wheel Drive (FWD), Rear-Wheel Drive (RWD), and All-Wheel Drive (AWD). The Front-Wheel Drive (FWD) segment dominates the global automotive differential market, driven by the widespread production of compact cars, sedans, and small SUVs that primarily use FWD configurations. FWD vehicles offer advantages such as lightweight architecture, better fuel efficiency, and lower manufacturing costs, making them the preferred choice for automakers in cost-sensitive markets. Additionally, FWD systems simplify vehicle design by integrating the engine and transmission on the same axle, reducing drivetrain complexity. The dominance of FWD is reinforced by growing vehicle production in the Asia Pacific region, particularly in China, India, and Japan, where compact and mid-size passenger vehicles hold a major share. The front-wheel drive (FWD) segment is projected to dominate the market with a share of 51.71% in 2026.

By Vehicle Type

SUV Segment Dominates the Market Driven by Rising Demand for AWD and 4WD Vehicles

By vehicle type, the market is segmented into Hatchback/Sedan, SUV, Light-Duty Vehicle, and Heavy-Duty Vehicle.

The SUV segment dominates the global automotive differential market, primarily due to rising consumer preference for spacious, high-performance, and versatile vehicles. SUVs are typically equipped with all-wheel drive (AWD) or four-wheel drive (4WD) systems, both of which require multiple differentials to manage torque distribution between the front, rear, and center axles. This increased mechanical complexity directly contributes to higher differential demand per vehicle compared to sedans or hatchbacks. The growing popularity of SUVs across North America, Europe, and Asia Pacific continues to boost production volumes. For instance, in February 2024, Toyota Motor Corporation reported record SUV sales across global markets, driven by its RAV4 and Highlander models, both featuring advanced differential systems for improved traction and control. The SUV segment is expected to lead the market, contributing 43.64% globally in 2026.

To know how our report can help streamline your business, Speak to Analyst

By Component

Mechanical Components Segment Leads owing to its Widespread Use in Traditional ICE Vehicles

Based on component, the market is segmented into mechanical (gears, case, and bearings), electro-mechanical (clutch and actuator), electronic (sensors and ECU), and others.

The mechanical component segment holds the largest automotive differential market share, primarily due to its widespread use in traditional internal combustion engine (ICE) vehicles and cost-effective driveline designs. Mechanical parts such as bevel gears, bearings, and differential cases remain essential for torque transfer and power distribution across the drivetrain, ensuring durability and high load-bearing capacity. Their proven reliability and lower maintenance costs make them a preferred choice for OEMs, particularly in mass-produced passenger cars and commercial vehicles. Continuous innovation in material strength and lightweight construction further supports segment growth. The mechanical segment will account for 65.83% market share in 2026.

Automotive Differential Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Automotive Differential Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific held 48.70% of the global market, reaching a valuation of USD 9.55 billion, and is projected to grow to USD 9.89 billion in 2026. Asia Pacific holds the largest share of the global automotive differential market, driven by high vehicle production volumes, expanding automotive manufacturing bases, and strong consumer demand for passenger and utility vehicles. Countries such as China, Japan, India, and South Korea serve as key automotive hubs, with established OEMs and Tier-1 suppliers actively investing in advanced drivetrain technologies. The region’s dominance is supported by the increasing production of SUVs, sedans, and light commercial vehicles, which extensively use differential systems for improved traction and fuel efficiency. Additionally, government initiatives promoting domestic manufacturing, such as India’s Make in India and China’s New Energy Vehicle (NEV) policies, are fostering localized production of differentials and driveline components. The Japan automotive differential market is anticipated to reach USD 1.39 billion by 2026, the China automotive differential market is set to attain USD 5.77 billion by 2026, and the India automotive differential market is likely to reach USD 0.89 billion by 2026.

North America

North America accounted for USD 3.79 billion in 2025, representing 19.60% of the global market share, and is projected to reach USD 3.88 billion in 2026. Other regions, including North America, Europe, and the rest of the world, are expanding steadily. North America and Europe represent mature yet innovation-driven markets for automotive differentials. North America benefits from strong demand for SUVs, pickup trucks, and off-road vehicles, particularly in the U.S. and Canada, where performance and towing capabilities are key consumer priorities. Leading automakers such as Ford, General Motors, and Stellantis are integrating advanced torque vectoring and limited-slip differentials in ICE. The United States automotive differential market is expected to reach USD 3.09 billion by 2026.

Europe

The Europe market was valued at USD 4.96 billion in 2025, capturing 25.40% of global revenue, and is estimated to reach USD 5.12 billion in 2026. In Europe, the automotive differential market is driven by vehicle electrification, premium car production, and stringent emission standards. Major automakers such as BMW, Audi, and Mercedes-Benz are increasingly adopting torque vectoring systems to enhance efficiency and handling. Strong R&D focus and government incentives further accelerate regional market growth. The Rest of the World (RoW), including Latin America, the Middle East, and Africa, is witnessing growth driven by expanding vehicle assembly operations and the rising adoption of commercial vehicles for industrial and infrastructure applications. The United Kingdom automotive differential market is estimated to reach USD 0.68 billion by 2026, while the Germany automotive differential market is forecast to reach USD 0.99 billion by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Key Players Focus on Strategic Collaborations to Support the Development of Next-Generation ICE Powertrains

The automotive differential market is dominated by leading Tier-1 suppliers such as Dana Incorporated, ZF Friedrichshafen AG, GKN Automotive, Eaton Corporation, American Axle & Manufacturing (AAM), and BorgWarner Inc. These companies maintain strong partnerships with major global OEMs, including Toyota, Ford, BMW, and Volkswagen, enabling them to deliver customized and high-performance driveline solutions. Their product portfolios encompass a wide range of differential systems, ranging from open and limited-slip types to advanced torque vectoring and electronic differentials.

Key market players are strategically aligning with the ongoing electrification and digitalization trends, transforming the automotive industry. Their focus lies in strengthening supply chains and investing in lightweight materials, along with advanced intelligent control unit integration technologies, to support the development of next-generation hybrid and internal combustion engine (ICE) powertrains.

LIST OF KEY AUTOMOTIVE DIFFERENTIAL COMPANIES PROFILED:

- American Axle & Manufacturing, Inc. (AAM) (U.S.)

- BorgWarner Inc. (U.S.)

- Dana Incorporated (U.S.)

- Eaton Corporation plc (Ireland)

- ZF Friedrichshafen AG (Germany)

- GKN Automotive (GKN PLC) (U.K.)

- Hyundai WIA Corporation (South Korea)

- JTEKT Corporation (Japan)

- Schaeffler Technologies AG & Co. KG (Germany)

- Linamar Corporation (Canada)

KEY INDUSTRY DEVELOPMENTS:

- In July 2025, BorgWarner announced that it had secured a new Electric Cross Differential (eXD) contract with a leading Chinese OEM, marking a significant expansion of its torque management portfolio in Asia. The eXD system is designed to improve traction, cornering stability, and driving safety by electronically managing torque distribution between the left and right wheels.

- In April 2025, Dana Incorporated showcased its latest fully integrated drive and motion systems at Bauma 2025, one of the largest global exhibitions for construction and industrial machinery. The company highlighted its Spicer drivetrain solutions tailored for internal combustion engine (ICE) equipment, featuring high-durability axles, transmissions, and differential systems engineered for improved efficiency and power delivery.

- In May 2024, Eaton Corporation announced it had been selected by a major global automaker to supply its advanced ELocker electronic locking differential system for an upcoming plug-in hybrid SUV (PHEV).

- In February 2024, Mazda Motor Corporation introduced an innovative asymmetric limited-slip differential (LSD) on its 2024 MX-5 Miata Club trim, enhancing handling dynamics and cornering stability. The new LSD features a cam-based mechanism that varies locking torque depending on whether the car is accelerating or decelerating, providing stronger lockup during braking and smoother rotation during acceleration. This innovation aims to improve driver feedback, traction control, and cornering balance, maintaining the lightweight sports car’s renowned handling precision.

- In January 2022, OHV introduced slip differentials for 2WD & 4WD Mercedes-Benz Sprinter-based vans, suited for both platforms, NCV3 (2007-2018) and VS30 (2019+) chassis. The new differentials are mainly designed for the uplifting and building of community and also for the fleet services with a goal to improve the off-road and inclement weather ability.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.51% from 2026-2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Type

By Drive Type

By Vehicle Type

By Component

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 19.51 billion in 2025 and is projected to reach USD 28.64 billion by 2034.

In 2025, the market value stood at USD 9.55 billion.

The market is expected to exhibit a CAGR of 4.51% during the forecast period (2026-2034).

The SUV segment led the market by vehicle type.

Rising demand for All-Wheel Drive (AWD) and Sports Utility Vehicles (SUVs) accelerate market growth.

The automotive differential market is dominated by leading Tier-1 suppliers such as Dana Incorporated, ZF Friedrichshafen AG, and GKN Automotive.

Asia Pacific dominated the market with a share of 48.7% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us