Automotive Digital Cockpit Market Size, Share & Industry Analysis, By Component (Digital Instrument Cluster, Infotainment Display, Cockpit Domain Controller (CDC), Head-Up Display (HUD), & Others), By Display Technology (LCD, OLED, LED-Based, & Projection HUD), By Display Size (Below 7 Inches, 7–10 Inches, 10–13 Inches, & Above 13 Inches), By Level of Autonomy (Level 0, Level 1, Level 2, Level 3, Level 4 & Above), By Vehicle Type (Hatchbacks/Sedans, SUVs, Light Commercial Vehicles (LCVs), & Heavy Commercial Vehicles (HCVs)), By Propulsion Type (ICE & Electric), & Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

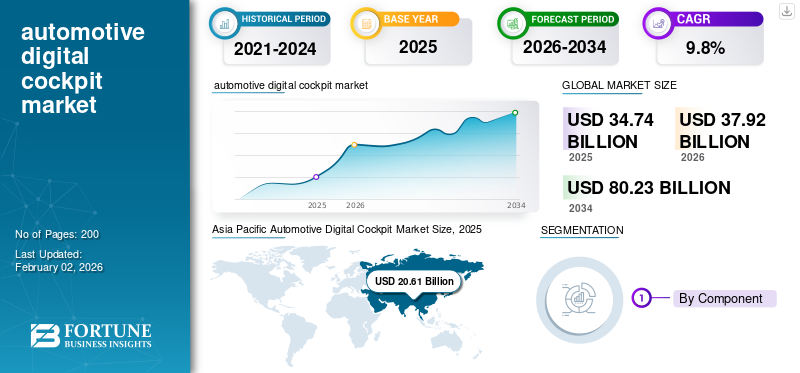

The global automotive digital cockpit market size was valued at USD 34.74 billion in 2025 and is projected to grow from USD 37.92 billion in 2026 to USD 80.23 billion by 2034, exhibiting a CAGR of 9.8% during the forecast period. Asia Pacific dominated the global automotive digital cockpit market with a market share of 59.33% in 2025.

An automotive digital cockpit integrates displays, infotainment, connectivity, ADAS visualization, and centralized computing to deliver an interactive, software-driven driver and passenger experience, replacing traditional analog clusters with intelligent, customizable interfaces. Growing consumer demand for connected, intuitive interfaces, rising adoption of ADAS and autonomous features, shift toward software-defined vehicles, OEM focus on differentiation, and advancements in displays, processors, and HMI technologies drive the market.

Major players in the automotive digital cockpit market include Bosch, Continental, Harman, Aptiv, Visteon, Panasonic, and Hyundai Mobis. These companies compete by advancing high-resolution displays, domain controllers, intuitive HMIs, software platforms, connectivity, and ADAS integration.

Download Free sample to learn more about this report.

Automotive Digital Cockpit Market Key Takeaways

- 2025 Market Size: USD 34.74 billion

- 2026 Market Size: USD 37.92 billion

- 2034 Forecast Market Size: USD 80.23 billion

- CAGR: 9.8% from 2026–2034

- Asia Pacific dominated the automotive digital cockpit market with a 59.33% share in 2025.

- LCD displays held the dominant share due to their cost efficiency and proven reliability.

- Infotainment displays accounted for a significant share owing to rising demand for connected in-vehicle experiences.

Asia Pacific

Asia Pacific leads the market due to strong vehicle production, rapid EV adoption, and increasing cockpit digitalization by regional OEMs.

North America

North America is witnessing steady growth driven by rising adoption of connected infotainment systems, centralized computing, and ADAS-enabled HMIs.

Europe

Europe’s market growth is supported by stringent vehicle safety regulations, electrification trends, and increasing integration of intelligent HMI technologies.

U.S.

The market is expanding rapidly due to strong demand for premium vehicles, advanced infotainment systems, and large in-vehicle display technologies.

Japan

Growth is driven by the presence of major automotive OEMs, continuous innovation in vehicle electronics, and increasing focus on smart cockpit integration.

Read More

MARKET DYNAMICS

Automotive Digital Cockpit Market Growth Drivers

Rising Demand for Connected, Immersive Driving Experiences Fuels Market Growth

Growing consumer expectations for seamless connectivity, AI-driven personalization, and rich infotainment are major drivers. Automakers increasingly integrate multi-display layouts, cockpit domain controllers, and advanced HMIs to differentiate vehicles. In September 2025, Qualcomm Technologies, Inc. announced that its Snapdragon Cockpit Platform powers new all-electric Mercedes‑Benz CLA and Mercedes‑Benz GLC models, delivering AI-driven, high-performance automotive digital cockpits with 5G connectivity, immersive displays, and personalized passenger vehicles' in-car experiences.

MARKET RESTRAINTS

High System Costs and Integration Complexity Restrict Wide-scale Adoption

Despite rising demand, expensive displays, processors, and centralized controllers, combined with integration challenges across infotainment, advanced driver assistance systems, and telematics, act as key restraints. Legacy vehicle architectures struggle to support sophisticated digital ecosystems, increasing engineering burdens. These constraints overlap with opportunities in standardized platforms but slow adoption in cost-sensitive markets, limiting mass deployment beyond premium segments.

Automotive Digital Cockpit Market Opportunities

Software-Defined Vehicle Architecture Unlocks New Monetization Opportunities

As vehicles shift to software-defined architectures, OEMs gain opportunities to deliver subscription services, OTA upgrades, app ecosystems, and personalized cockpit features. This creates recurring revenue streams and enhances lifecycle value. It positions automotive digital cockpits as core enablers of future mobility experiences. In January 2025, Elektrobit unveiled its SDV roadmap at CES, showcasing open-source solutions spanning cloud-to-cockpit development, enabling scalable software architectures, faster deployment cycles, and enhanced integration for next-generation automotive digital ecosystems.

MARKET CHALLENGES

Escalating Cybersecurity Risks Challenge the Reliability of Connected Cockpits

As automotive digital cockpits integrate cloud services, V2X, and OTA capabilities, cybersecurity becomes a major challenge. Protecting displays, ECUs, and user data from attacks requires robust encryption, intrusion detection, and safety compliance. This challenge overlaps with trends in centralization and opportunities in software-defined vehicles, highlighting the tension between innovation, connectivity, and secure system design.

Automotive Digital Cockpit Market Trends

Rapid Convergence of ADAS, Infotainment, and Instrument Clusters Drives Cockpit Centralization

A key trend is the fusion of multiple domains, instrument clusters, infotainment, navigation, climate, and ADAS visualization into a single high-performance computing unit. This reduces wiring, weight, and latency while enabling rich UI integration. In January 2024, Qualcomm and Bosch showcased a new central vehicle computer for advanced digital cockpits, integrating high-performance processing, AI, and ADAS support to enable next-generation software-defined vehicle experiences. Thus, the rapid convergence of ADAS, infotainment, and instrument clusters drives cockpit centralization to propel the automotive digital cockpit demand.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

Expanding Connectivity Ecosystem Drives Infotainment Display Dominance

Based on component, the market is segmented into digital instrument clusters, infotainment displays, cockpit domain controllers, head-up displays, and others. Infotainment displays dominate due to OEM focus on immersive HMI, larger multi-screen layouts, advanced head units, centralized controls, smartphone integration, and continuous OTA-enabled feature enhancements. Their role as the primary interaction hub strengthens adoption across all vehicle categories, supported by falling display costs and rising consumer expectations for connectivity, demand for seamless, personalized in-vehicle digital experiences. In January 2025, Hyundai India planned to launch an Android Automotive-based infotainment system in 2027, enabling deeper connectivity, improved UI/UX, integrated apps, and enhanced automotive digital cockpit capabilities across upcoming models.

By Display Technology

Enhanced Affordability and Maturity Sustain LCD Leadership in Automotive Cockpits

Based on display technology, the market is segmented into LCD, OLED, LED-based, and projection HUDs. LCD dominates due to its cost efficiency, proven reliability, wide temperature tolerance, and large-scale manufacturability aligned with OEM budgets. Its adaptability across instrument clusters, infotainment displays, and secondary screens further reinforces adoption, especially in high-volume vehicle segments where price-performance balance remains a primary purchasing criterion for automotive digital cockpit integration. Exceptional brightness, contrast, slimness, and energy efficiency accelerate Mini-LED and Micro-LED adoption. In January 2025, AUO and BHTC unveiled a next-generation smart cockpit concept featuring advanced LED, Mini-LED, and Micro-LED display technologies, delivering higher brightness, improved contrast, and immersive automotive HMI experiences.

By Vehicle Type

Versatile Cabin Space and Premium Features Propel SUV Digital Cockpit Leadership

Based on vehicle type, the market is segmented into hatchbacks/sedans, SUVs, LCVs, and HCVs. SUVs hold the largest automotive digital cockpit market share due to their global sales strength, larger cabin layouts supporting multi-display configurations, and faster adoption of advanced infotainment, ADAS visualization, and connected services. OEMs increasingly prioritize premium digital experiences in SUVs, making them the central platform for showcasing next-generation cockpit architectures and software-defined vehicle capabilities across mainstream and luxury segments. Rising consumer preference for tech-rich, spacious vehicles accelerates SUV cockpit feature upgrades. In March 2025, Mazda unveiled the new CX-5, featuring an upgraded digital cockpit with advanced displays, improved HMI responsiveness, enhanced connectivity, and driver-centric interfaces designed to elevate safety, comfort, and in-vehicle user experience.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion

Cost Efficiency and Established Architectures Sustain ICE Leadership in Digital Cockpit Integration

Based on propulsion type, the market is segmented into ICE and electric. ICE vehicles dominate due to their significantly larger global production base, proven electrical architectures, and steady cockpit feature upgrades across mass-market segments. OEMs continue integrating advanced displays, connectivity, and HMI enhancements into ICE platforms, ensuring broad adoption even as electrification accelerates. Their affordability and mature supply chains further reinforce widespread digital cockpit penetration. EVs, including plug-in hybrid electric vehicles (PHEVS) and battery electric vehicles (BEVS), are rapidly adopting high-end automotive digital cockpits driven by centralized computing and software-defined vehicle architectures. In January 2025, Suzuki selected Qt to power digital cockpits for its upcoming mainstream EVs, enabling faster HMI development, enhanced graphics performance, scalable UI frameworks, and improved user experience across next-generation electric models.

By Level of Autonomy

Widespread ADAS Adoption Strengthens Level 2 Dominance in Digital Cockpit Deployment

Based on the level of autonomy, the market is segmented into level 0, level 1, level 2, level 3, and level 4 & above. Level 2 dominates as it represents the broadest global deployment of semi-autonomous features, requiring advanced digital cockpits for lane-keeping visualization, adaptive cruise displays, driver monitoring, and real-time sensor feedback. Automakers integrate richer HMI, larger screens, and centralized computers to support these functions, making Level 2 the most commercially scaled autonomy stage driving cockpit enhancement. In January 2025, Toyota announced expanded global deployment of its Level 2 driver-assist platform, integrating enhanced sensors, upgraded HMI, and automotive digital cockpit alerts to improve lane-keeping, adaptive cruise performance, and overall driving safety. Higher automation demands sophisticated visualization, AI-driven HMI, and centralized computing, accelerating cockpit innovation in emerging L4+ platforms, especially in electric vehicles and hybrid electric vehicles (HEVS.

By Display Size

Increased Feature Complexity Drives Strong Adoption of 7–10 Inch Cockpit Displays

Based on display size, the market is segmented into below 7 inches, 7-10 inches, 10-13 inches, and above 13 inches. The 7-10 inch segment dominates as it balances cost, usability, and dashboard integration across mass-market vehicles. This size range supports navigation, infotainment, ADAS visualization, and smartphone mirroring without significantly raising system cost. Its compatibility with both entry-level and mid-range models makes it the most widely adopted format in global automotive digital cockpit strategies. Luxury and EV platforms increasingly adopt large cinematic displays, driving a high growth rate for screens above 13 inches. In April 2025, Škoda confirmed the new Kodiaq’s India launch, highlighting its upgraded 13-inch touchscreen infotainment unit, delivering enhanced clarity, improved user interaction, and a more premium, feature-rich digital cockpit experience for drivers.

Automotive Digital Cockpit Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific Automotive Digital Cockpit Market Analysis

Asia Pacific dominates and grows fastest due to massive vehicle production, strong EV penetration, and aggressive digitalization by Chinese, Japanese, and Korean OEMs. High consumer demand for connected features, falling display and semiconductor costs, and government-supported smart mobility ecosystems accelerate cockpit adoption. Local suppliers’ rapid innovation in displays, domain controllers, and AI-based HMI further boosts scalability. The region’s large volume base and competitive pricing make it the global center of digital cockpit expansion. In March 2025, Geely began consolidating its in-house automotive digital cockpit R&D teams to accelerate development of larger, high-resolution display systems, enabling unified screen architectures and improved efficiency across next-generation vehicle platforms.

Asia Pacific Automotive Digital Cockpit Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America Automotive Digital Cockpit Market Analysis

North America’s automotive digital cockpit market grows steadily as OEMs accelerate adoption of connected infotainment, centralized compute, and ADAS-enhanced HMIs. Strong consumer demand for premium features, higher penetration of SUVs and pickups, and rapid integration of software-defined vehicle platforms support expansion. Regulatory focus on camera-based driver monitoring systems and safety visualization further strengthens cockpit upgrades, propelling the automotive digital cockpit market growth.

The U.S. leads North America’s digital cockpit advancement due to its high adoption of premium vehicles, fast-growing EV ecosystem, and strong demand for large displays and rich infotainment experiences. Automakers prioritize OTA-enabled interfaces, AI-based personalization, and ADAS visualization to differentiate offerings. Technology partnerships with software, semiconductor, and cloud providers further accelerate cockpit innovation.

Europe Automotive Digital Cockpit Market Analysis

Europe’s automotive digital cockpit market growth is driven by strict safety regulations, rapid electrification, and strong OEM emphasis on intelligent HMI, cybersecurity, and multi-display integration. Premium brands accelerate early adoption of advanced cockpit domain controllers, AR head-up display HUD, and AI-driven interfaces. The region’s sustainability mandates and digital-first mobility strategies further push centralized architectures. In February 2025, Nissan debuted the all-new LEAF featuring an upgraded digital cockpit with advanced displays, enhanced connectivity, intuitive HMI, and integrated driver-assist visualizations to elevate user experience alongside its extended 622 km range.

Rest of the World

The rest of the world shows moderate but rising growth, primarily supported by increasing adoption of connected infotainment and cost-optimized digital cockpit platforms in Latin America, the Middle East, and Africa. Growing SUV sales, improving network infrastructure, and gradual EV introduction enhance cockpit feature penetration. In October 2024, Zeekr launched the 7X in the UAE, featuring a sophisticated digital cockpit with expansive displays, AI-driven interfaces, seamless connectivity, and advanced driver-assist visualization to elevate the premium in-car user experience.

COMPETITIVE LANDSCAPE

Key Industry Players:

Software-Defined Architectures, HMI Innovation, and Strategic Alliances Shape Digital Cockpit Competitiveness

The automotive digital cockpit market is defined by rapid advancements in high-performance computing, intelligent HMI design, and deep OEM and supplier collaboration. Leading players such as Bosch, Continental, Harman, Aptiv, Visteon, Panasonic, and Hyundai Mobis compete through sophisticated domain controllers, immersive multi-display systems, AI-driven personalization, and robust cybersecurity. Companies strengthen competitiveness by expanding global software centers, leveraging OTA platforms, optimizing costs through modular architectures, and forming strategic alliances with cloud, semiconductor, and UI technology partners. In September 2025, Qualcomm and Harman collaborated to integrate generative AI into automotive systems, enhancing digital cockpit intelligence, enabling personalized HMI, predictive assistance, and advanced in-vehicle user experiences for next-generation vehicles.

Top Key Companies in the Automotive Digital Cockpit Market

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Visteon Corporation (U.S.)

- Harman (U.S.)

- Panasonic Automotive Systems (Japan)

- Denso Corporation (Japan)

- Aptiv PLC (Ireland)

- LG Electronics (South Korea)

- Hyundai Mobis (South Korea)

- FORVIA (France)

- Marelli (Japan)

- Desay SV Automotive (China)

- Alps Alpine Co., Ltd. (Japan)

- Qualcomm (U.S.)

- BlackBerry QNX (Canada)

- PATEO CONNECT+ (China)

- ThunderSoft (China)

- Neusoft Corporation (China)

- Elektrobit Automotive (Germany)

- Valeo (France)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Volkswagen opened its EV-only development center in China, featuring advanced digital cockpit R&D capabilities. The facility focuses on high-performance computing, large integrated displays, AI-driven HMI, and software-defined cockpit architectures tailored for next-generation electric vehicles developed specifically for the Chinese market.

- January 2025: BlackBerry QNX introduced a fully virtualized automotive digital cockpit system at CES. The solution integrates infotainment, instrument cluster, and safety domains, enabling higher reliability, rapid development, and seamless consolidation for next-generation software-defined vehicles.

- January 2025: Qualcomm signed a multi-year collaboration with Google to integrate generative AI into digital cockpit platforms. The partnership enables advanced on-device AI processing, real-time personalization, multimodal interfaces, and enhanced driver-assist visualization powered by Snapdragon Automotive platforms and Google’s AI ecosystems for next-generation vehicles.

- September 2024: Maruti Suzuki revealed details of the upcoming e-Vitara, highlighting its upgraded digital cockpit with a large touchscreen, advanced connected features, and improved driver-information display. The system integrates enhanced HMI responsiveness and EV-specific visualization to support efficient energy management and user interaction.

- January 2024: Stellantis revealed that its India engineering teams are developing AI-powered digital cockpits featuring intelligent HMI, real-time personalization, voice-driven interfaces, and predictive assistance. The systems leverage advanced machine-learning models and centralized compute platforms to enhance user experience across future Stellantis vehicles globally.

REPORT COVERAGE

The global automotive digital cockpit market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and automotive digital cockpit market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Display Technology, Vehicle Type, Propulsion, Level of Autonomy, Display Size, and Region |

| By Component |

|

| By Display Technology |

|

| By Vehicle Type |

|

| By Propulsion |

|

| By Level of Autonomy |

|

| By Display Size |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 34.74 billion in 2025 and is projected to reach USD 80.23 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 20.61 billion.

The market is expected to exhibit a CAGR of 9.8% during the forecast period.

The SUVs segment led the market in terms of vehicle type.

Rising demand for connected, immersive driving experiences fuel market growth.

Major players in the automotive digital cockpit market include Bosch, Continental, Harman, Aptiv, Visteon, Panasonic, and Hyundai Mobis.

Asia Pacific held the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us