Automotive E-axle Market Size, Share & Industry Analysis, By Electric Vehicle Type (Battery Electric Vehicle, Plug-in Hybrid Electric Vehicle), By Vehicle Type (Passenger Cars, Commercial Vehicles), By Drive Type (All Wheel Drive, Front Wheel Drive, Rear Wheel Drive), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

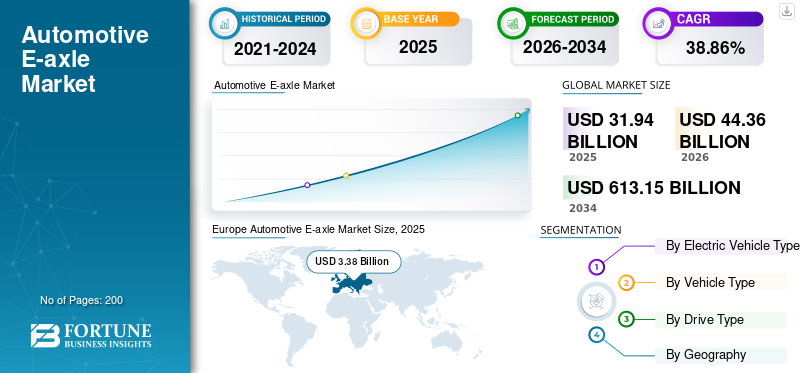

The global automotive e-axle market size was valued at USD 31.94 billion in 2025. The market is projected to grow from USD 44.36 billion in 2026 to USD 613.15 billion by 2034, exhibiting a CAGR of 38.86% during the forecast period. Europe dominated the global market with a share of 46.88% in 2025. The global impact of COVID-19 has been unprecedented and staggering with automotive e-axle witnessing a positive impact on demand across all regions amid the pandemic. Based on our analysis, the global market exhibited a higher growth of 25.4% in 2020 s compared to the average year-on-year growth during 2017-2019. The rise in CAGR is attributable to this market’s demand and growth, returning to pre-pandemic levels once the pandemic is over. The automotive e-axle market in the U.S. is projected to grow significantly, reaching an estimated value of USD 1142.7 million by 2028.

Automotive e-axle refers to a compact electric drive solution that combines the transmission, electric motor, and power electronics into a single unit. This single casing allows for simple integration of several components, a single cooling system for all parts, streamlined packaging, and improved efficiency. It acts as the powertrain of the EV and offers vehicle manufacturers increased performance gains. The aggressive electrification targets set by key OEMs and a greater number of available models will influence the market's growth.

Download Free sample to learn more about this report.

AUTOMOTIVE E-AXLE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 31.94 Billion

- 2026 Market Size: USD 44.36 Billion

- 2034 Forecast Market Size: USD 613.15 Billion

- CAGR: 38.86% from 2026–2034

- Europe dominated the automotive e-axle market with a 46.88% share in 2025.

- The BEV segment held the largest market share due to its lower total cost of ownership, higher efficiency, and reduced maintenance requirements.

- Passenger cars led the market, reaching a value of USD 27.23 billion in 2025.

Europe

Europe led the global market with a value of USD 3.38 billion in 2025, driven by stringent CO₂ emission targets and decarbonization initiatives such as the EU Green Deal and Sustainable Mobility Strategy.

Asia Pacific

Asia Pacific is expected to witness the fastest growth during the forecast period, supported by rapid charging infrastructure deployment, fleet electrification, and declining EV ownership costs.

North America

North America is projected to experience strong growth due to increasing EV adoption, expanding model availability, and supportive federal and state-level policies.

U.S.

Market growth is supported by government initiatives promoting zero-emission vehicles, tax credit programs, and increasing demand for electric SUVs and commercial EVs.

Japan

The automotive e-axle market is expected to reach USD 56.4 billion by 2025.

Read More

Automotive E‑Axle Market Trends

Increasing Collaboration between Key Players in the Value Chain Will Positively Influence Growth

There is an increasing demand for electric vehicles, especially in high-volume emerging economies. However, there is a significant discrepancy between the performance offered and affordability of EVs. Hence, strategic partnerships have increased exponentially between key players in the industry to accelerate electric mobility and achieve mass adoption.

For instance, Linamar entered into a partnership with Exro Technologies to develop an automotive e-axle (using Exro’s Coil Driver technology) to improve cost optimize integration and performance of Linamar’s e-axle portfolio. Hence, the increased collaboration will accelerate the deployment of EVs and e-axles during the forecast period.

Download Free sample to learn more about this report.

DRIVING FACTORS

Increasing Number of Electric Vehicle Models in Key Regions such as China and the U.S. Will Drive Market Growth

According to the International Energy Agency (IEA) global annual EV outlook report published in April 2021, around 370 electric car models were available in 2020. It represents an increase of 40% year on year. The most significant expansion and various models were observed in the popular SUV segment in 2020. Electric SUVs are witnessing rapid adoption in China and Europe and account for the largest market share in the U.S. For instance, in Europe, the share of electric sports utility vehicles is higher than for the total SUV market.

Hence, these factors will propel the automotive e-axle market growth.

Aggressive OEM Electrification Targets Will Augment Market Growth

According to the IEA, 18 of the 20 largest OEMs (in terms of vehicles sold in 2020), which accounted for around 90% of the total new car registrations worldwide in 2020, have announced plans to boost the availability and production of light-duty electric vehicles. For instance, Volvo plans to sell only electric cars globally from 2030. Ford will sell electric cars only in Europe from 2030. General Motors aims to sell only light-duty electric vehicles by 2035.

Hence, these factors will fuel the demand for automotive e-axles during the forecast period.

RESTRAINING FACTORS

High Cost of Electric Vehicles to Restrain Growth

According to Kelley Blue Book (a subsidiary of Cox Automotive), the average transition price of an electric vehicle is around USD 55,000. Hence, an electric vehicle is equivalent to an entry-level luxury car in terms of pricing. Furthermore, users need to install a Level 2 charging outlet in their home that costs an additional USD 2,500 (to save time and extend battery life) compared to Level 1 charging (cheaper, exponentially longer charging time). Hence, the higher upfront costs for EVs will restrain the market growth.

Automotive E‑Axle Market Segmentation Analysis

By Electric Vehicle Type Analysis

BEV Segment to Hold Largest Share Owing to Lower Total Cost of Ownership (TCO)

By electric vehicle type, the market is segmented into battery electric vehicles (BEV) and plug-in hybrid electric vehicles (PHEV).

The BEV segment held the largest share of the market, which can be attributed to the comparatively lower total ownership costs over the long term, higher efficiency, and lesser maintenance involved. The PHEV segment is anticipated to show substantial growth due to the benefits of faster charging, more range, and reduced carbon footprint.

By Vehicle Type Analysis

Passenger Car Segment to Hold Largest Share Due to Policy Support

By vehicle type, the market is segmented into passenger cars and commercial vehicles.

The passenger car segment is estimated to reach a value of 27.23 billion in 2025, which can be attributed to the significant purchase incentives and subsidies offered in key markets, along with the stringency of emission standards driving large-scale electrification in this segment. The commercial vehicle segment is expected to show exponential growth due to increasing policy support for adopting heavy-duty electric vehicles (HDVs) and rising private sector demand for zero-emission last-mile delivery vehicles.

By Drive Type Analysis

To know how our report can help streamline your business, Speak to Analyst

FWD Segment Dominated in 2020 Propelled by Low Cost and High Efficient Performance

By drive type, the market is segmented into all-wheel drive (AWD), front-wheel drive (FWD), and rear-wheel drive (RWD).

The FWD segment held the largest share of the market in 2020, owing to its low weight, superior traction, and considerably lower cost and complexity in terms of design & setup. The AWD segment is expected to exhibit exponential growth in the market with a share of 15.07% in 2025 as it offers both high-level handling and balance (offered by RWD) and excellent traction (achieved by FWD).

REGIONAL ANALYSIS

Europe

Europe Automotive E-axle Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe held the largest market share and is valued at USD 3.38 billion in 2025. Factors such as increasing stringency of CO2 emission targets and the implementation of decarbonization strategies such as the EU Sustainable and Smart Mobility Strategy and Action Plan and the EU Green Deal will propel the market growth in this region. Europe is projected to exhibit a CAGR of 32.5%.

Asia Pacific

Asia Pacific is anticipated to exhibit exponential growth in the market during the forecast period. The market in China is expected to grow at a steady CAGR of 33.3%. Rapid deployment of charging infrastructure, aggressive electrification of heavy-duty fleets and public transportation, and decrease in the total cost of ownership of EVs will drive the growth of the market in this region. The automotive e-axle market in Japan is expected to reach an estimated value of USD 56.4 billion in 2025.

North America

North America is expected to exhibit good growth in the market during the forecast period. Initiatives at a state level for stronger EV deployment and available EV models (particularly in the SUV segment) continue to increase in the U.S. Moreover, the government has also announced intentions to revise tax credit programs at a federal level to encourage zero-emission vehicle adoption and support domestic manufacturers. These factors will propel the demand for e-axles in this region.

KEY INDUSTRY PLAYERS

Diverse Product Portfolio to Strengthen Leading Position of Dana Limited in Market

Early investment in strategic partnerships, extensive R&D investments, and a comprehensive product portfolio has enabled Dana Limited to strengthen its leading position as a key player in the market. Based on vehicle type, the company offers an industry-leading six different e-axles. In September 2021, the company launched the eS9000r e-axle for various Class 7 & 8 medium and heavy-duty vehicles that will further advance the adoption of electric mobility in the commercial vehicle segment. Hence, these factors will propel the leading position of Dana in the market.

LIST OF KEY COMPANIES PROFILED:

- Dana Limited (Ohio, U.S.)

- Robert Bosch GmbH (Gerlingen, Germany)

- GKN Automotive Limited (London, U.K.)

- Nidec Corporation (Kyoto, Japan)

- ZF Friedrichshafen AG (Friedrichshafen, Germany)

- Continental AG (Hanover, Germany)

- Schaeffler AG (Herzogenaurach, Germany)

- AxleTech (Meritor, Inc.) (Michigan, U.S.)

- Linamar Corporation (Guelph, Canada)

- Magna International Inc. (Aurora, Canada)

KEY INDUSTRY DEVELOPMENTS:

- October 2021 – Nidec announced the implementation of Ni200Ex, the company’s 200kW, e-axle traction motor system, in the ZEEKR 001, an EV produced by Geely Automobile Group, one of the largest auto manufacturers in China

- July 2021 – Schaeffler started the production of its 2in1 electric axles at its facility in Taicang, China. Following the adoption of this product in China, this e-axle will also be used by a major European auto manufacturer.

REPORT COVERAGE

The global automotive e-axle market report covers a detailed analysis of the industry and focuses on key aspects, such as leading companies, product types, and leading applications of the product. Besides this, the study offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report delivers an in-depth automotive e-axle study analysis of several factors that have contributed to its growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2034 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Volume (Thousand Units) & Value (USD Billion) |

|

Segmentation |

By Electric Vehicle Type

|

|

By Vehicle Type

|

|

|

By Drive Type

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global Automotive E-axle Market size was USD 31.94 billion in 2025 and is projected to reach USD 613.15 billion by 2034.

In 2025, the Europe Automotive E-axle Market value stood at USD 3.38 billion.

The Automotive E-axle Market will register a CAGR of 38.86% over the forecast period (2026-2034).

The passenger cars segment is expected to lead this market during the forecast period.

Increasing investments by key players to develop technologically advanced electric axle drive systems, key tier-1 suppliers, and OEMs collaborating to take advantage of growth opportunities in the electric mobility supply chain and the rapid transition from internal combustion engine-based vehicles (ICE vehicles) to electric vehicles are expected to drive the global e-axle market growth.

Dana Limited, Robert Bosch GmbH, and Nidec Corporation are the major players in the global market.

Europe held the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us