Automotive Ethernet Market Size, Share & Industry Analysis, By Vehicle Type (Passenger Cars and Commercial Vehicles), By Bandwidth Outlook (10 Mbps, 100 Mbps, 1 Gbps, and 2.5/5/10 Gbps), By Application (ADAS, Body & Comfort, Infotainment, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

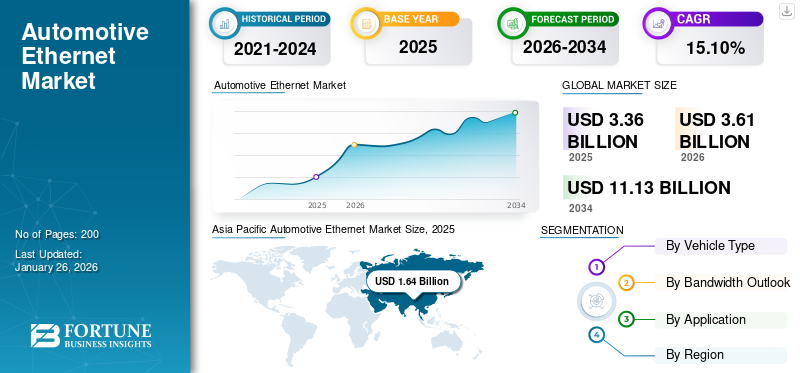

The global automotive ethernet market size was valued at USD 3.36 billion in 2025 and is projected to grow from USD 3.61 billion in 2026 to USD 11.13 billion by 2034, exhibiting a CAGR of 15.10% during the forecast period. Asia Pacific dominated the global market with a share of 48.98% in 2025.

Ethernet is a specialized version of ethernet technology, modified and optimized for utilization in vehicles. Originally developed for computer networking and data communication, ethernet is currently known for high-speed data transmission with reliability and scalability. In the automotive world, it is adapted to meet the unique challenges posed by the automotive environment, including stringent requirements for latency, bandwidth, safety, durability, and cost-efficiency.

Download Free sample to learn more about this report.

Global Automotive Ethernet Market Key Takeaways

- 2025 Market Size: USD 3.36 billion

- 2026 Market Size: USD 3.61 billion

- 2034 Forecast Market Size: USD 11.13 billion

- CAGR: 15.10% from 2026–2034

- Asia Pacific dominated the automotive ethernet market with a 48.98% share in 2025.

- The passenger cars segment is projected to account for 71.90% of the market share in 2026.

- The ADAS segment is expected to hold 42.61% of the global market share in 2026.

Asia Pacific

Asia Pacific generated USD 1.64 billion in revenue in 2025 and is projected to reach USD 1.78 billion in 2026.

Europe

Europe accounted for 25.40% of the global market in 2025 and is expected to reach USD 0.92 billion in 2026.

North America

North America captured 19.43% of global revenue in 2025 and is projected to reach USD 0.70 billion in 2026.

U.S.

The U.S. automotive ethernet market is projected to reach USD 0.59 billion by 2026.

Japan

Japan’s automotive ethernet market is projected to reach USD 0.16 billion by 2026.

Read More

Market Dynamics

Market Drivers

Rising Demand for Advanced In-Vehicle Infotainment Systems to Augment Market Growth

One of the primary drivers for the automotive ethernet market growth is the rising consumer demand for sophisticated in-vehicle infotainment systems. Current consumers expect their vehicles to offer seamless connectivity, entertainment, and real-time information. The ethernet provides the necessary bandwidth to support high-definition video streaming, advanced navigation systems, and interactive media, ensuring a superior user experience. As automakers strive to differentiate their offerings, the integration of automotive ethernet becomes a critical component in delivering cutting-edge infotainment solutions.

Increasing Focus on Vehicle Safety and Advanced Driver Assistance Systems (ADAS) to Propel Market Growth

Safety is a paramount concern for both consumers and manufacturers in the automotive industry. The development and deployment of advanced driver assistance systems (ADAS) rely heavily on real-time data processing and communication. Ethernet enables fast and reliable transfer of data between sensors, cameras, and control units, ensuring that vehicles can make rapid decisions to prevent accidents and enhance driver safety. As regulatory standards for vehicle safety continue to tighten, the adoption of ethernet in the automotive sector is rising, driving the market forward.

Market Restraints

High Initial Costs Hamper Market Growth

One of the most significant barriers to the ethernet is the high initial costs associated with its deployment. Implementing ethernet technology in vehicles requires the development of a new ecosystem, including specialized hardware, software, and infrastructure upgrades. Automakers and suppliers must invest in designing new Electronic Control Units (ECUs), cables, connectors, and testing tools to integrate ethernet-based systems into modern vehicles. While ethernet is more cost-effective than traditional automotive technologies, such as CAN or MOST, in the long run, the upfront costs associated with it are deterring some businesses, particularly smaller players with limited budgets.

Market Opportunities

Rise of Electric and Autonomous Vehicles to Positively Influence Market Growth

The shift toward electric and autonomous vehicles presents a lucrative opportunity for the market. Electric vehicles (EVs), with their distinct powertrain architectures, benefit from ethernet’s ability to integrate complex systems seamlessly and optimize energy management. Meanwhile, the development and operation of autonomous vehicles rely heavily on data from sensors and cameras, necessitating robust and reliable communication networks that ethernet can provide.

Market Challenges

Security Concerns and Latency Issues Challenges the Product Demand

With the increase in connectivity, vehicles become more vulnerable to cyberattacks. Automotive ethernets, which are integral to vehicle networking, must incorporate strong security measures to prevent unauthorized access and ensure the safety of passengers. Developing and maintaining these security protocols can be complex and costly. A few vehicle systems demand real-time communication with minimal delay. Even though ethernet provides significant bandwidth, ensuring low latency for critical safety systems remains a technical challenge. Designing network architectures that can prioritize and manage data traffic efficiently is a complex task.

Automotive Ethernet Market Trends

Expansion of Autonomous Driving Capabilities to Positively Influence Market Growth in the Future

Higher levels of autonomous driving (Level 3 and above) necessitate immense data processing, with an increasing reliance on sensor fusion from radar, LiDAR, and cameras. The ethernet provides the necessary bandwidth and reliability to transport this data to central processing units, ensuring smooth and real-time operation of autonomous systems. Automakers are developing self-driving capabilities that prioritize ethernet adoption in the platforms. This trend is predicted to reshape the market, contributing toward the rapid market growth.

Download Free sample to learn more about this report.

Impact of COVID-19

Production Delays and Supply Chain Issues Hampered Market Growth During Initial Stages of the COVID-19 Pandemic

The global spread of COVID-19 led to widespread lockdowns, factory closures, and transportation delays. Automotive manufacturers and suppliers faced severe supply chain disruptions as key components required for automotive ethernet systems were less. Semiconductors, which play a pivotal role in ethernet connectivity for in-vehicle networks, were particularly impacted due to chip shortages. Countries, China, South Korea, and Germany, which are crucial hubs for the production of automotive electronics, saw significant production slowdowns due to restrictions and workforce shortages.

These disruptions delayed the deployment of advanced ethernet technologies in new vehicles, pushing back timelines for automotive manufacturers. While global supply chains were on the path to recovery, the aftershocks of the pandemic have encouraged the industry to rethink its reliance on centralized production and explore regionalized supply networks.

The pandemic-induced economic downturn caused a sharp decline in global automotive sales and production. As consumer spending on non-essential goods plummeted, automotive manufacturers reduced their production volumes. This drop in vehicle output had a domino effect on the demand for ethernet technologies, which are integrated into vehicles to facilitate connectivity, data transfer, and advanced driver assistance systems (ADAS).

However, the recovery in automotive production, stimulated by government incentives and constrained demand in key markets, has led to a gradual rebound in the adoption of automotive ethernet systems. Industry players are now recalibrating their strategies to align with the growing consumer preference for connected and intelligent vehicles.

Segmentation Analysis

By Vehicle Type

Growing Demand for Accelerating Connectivity Boosted Adoption of Passenger Cars

On the basis of vehicle type, the market has been segmented into passenger cars and commercial vehicles.

The passenger cars segment is projected to dominate the market with a share of 71.90% in 2026. In recent years, the automotive industry has undergone a transformative shift driven by the increasing complexity of vehicle systems and the push toward more connected and autonomous driving technologies. The core of this evolution is the surging demand for automotive ethernet, a high-speed networking technology that is poised to redefine the connectivity landscape within passenger cars. The demand for in-car entertainment and information systems has been higher. Passengers expect seamless integration with personal devices, high-definition media streaming, and real-time navigation updates, all of which require robust data transmission capabilities.

The commercial vehicles segment is expected to grow at a steady CAGR during the forecast period from 2025 to 2032. Commercial fleets now extensively use telematics solutions for monitoring fuel efficiency, vehicle diagnostics, driver behavior, and route optimization. The ethernet enables reliable and fast data exchange between telematics systems and the cloud, improving overall fleet productivity. It also ensures that real-time updates and diagnostics data can be transmitted without delays, reducing vehicle downtime.

By Bandwidth Outlook

Favorable Trends Associated with Autonomous and Semi-Autonomous Driving Bolstered 100 Mbps Segment Growth

Based on the bandwidth outlook, the market is divided into 10 Mbps, 100 Mbps, 1 Gbps, and 2.5/5/10 Gbps.

The 100 Mbps segment is projected to dominate the market with a share of 39.37% in 2026. The road toward fully autonomous vehicles necessitates the integration of numerous interconnected systems, each generating and processing vast amounts of real-time data. While gigabit Ethernet standards (such as 1 Gbps+) may be needed for certain high-performance tasks, 100 Mbps networks still fulfill a wide range of less data-intensive but equally critical functions. Many OEMs prefer to deploy a mix of bandwidth solutions depending on specific application requirements, with 100 Mbps serving as a cost-effective and reliable option.

The 1 Gbps segment will grow at the fastest CAGR during the forecast period. Modern vehicles are no longer isolated systems; they are connected to the cloud, infrastructure, and other vehicles (V2X communication). From over-the-air (OTA) updates to in-car entertainment and real-time traffic navigation, connected cars rely on high-bandwidth networks to provide seamless user experiences. A 1 Gbps ethernet backbone provides the speed needed to support these innovations, thus becoming a viable option for businesses operating in the market.

To know how our report can help streamline your business, Speak to Analyst

By Application Analysis

ADAS Segment to Lead the Market Due to Its Data-Intensive Operations and Scalability

Based on the application, the market is divided into ADAS, body & comfort, infotainment, and others.

The ADAS segment is projected to dominate the market with a share of 42.61% in 2026. ADAS relies on data-based components, such as high-definition cameras and radars. Processing and sharing the information in real-time across vehicle subsystems is non-negotiable for the efficient functioning of these systems. The ethernet provides the high-speed connectivity needed to enable these communication flows seamlessly. It offers a scalable option for OEMs (Original Equipment Manufacturers) and system suppliers. With the ongoing progression toward higher automation levels (Level 3–5 autonomy), the need for larger bandwidth and faster data transfer is increasing. Ethernet provides the flexibility to adapt to these future demands without requiring significant overhauls to vehicle architecture.

The body & comfort segment held a significant market share. The rising adoption of advanced body and comfort features such as climate control, seat adjustment systems, lighting, and automated door functionalities. These systems require reliable and efficient communication networks, which automotive Ethernet provides by enabling high-speed data transmission and reducing wiring complexity. This development drives the market growth.

Automotive Ethernet Market Regional Outlook

The global market regions are segmented into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Ethernet Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific contributed 48.98% to the global market in 2025, with a valuation of USD 1.64 billion, and is projected to reach USD 1.78 billion in 2026. The shift toward electric mobility is accelerating across the Asia Pacific region. Many governments, including those in China, Japan, and South Korea, are actively promoting EV adoption through subsidies, tax incentives, and infrastructure investments. EVs rely heavily on advanced electronic systems for battery management, connectivity, and energy efficiency, making ethernet essential for their operation. The Japan market is projected to reach USD 0.16 billion by 2026, the China market is projected to reach USD 1.08 billion by 2026, and the India market is projected to reach USD 0.2 billion by 2026.

Asia Pacific is home to some of the world’s largest automotive markets, including China, India, Japan, and South Korea. Growing vehicle ownership, population density, and urbanization have contributed to a surge in demand for personal vehicles as well as commercial fleets. As more automakers in the region seek to integrate advanced technologies into their products, automotive ethernet has become a critical enabler of next-generation features.

North America

North America will grow at a steady pace during the forecast period. The inclination toward self-driving cars has heavily influenced North America's automotive landscape. Companies in North America and the U.S., such as Tesla, Waymo, and GM’s Cruise, are spearheading efforts to develop Level 4 and Level 5 autonomous vehicles. Autonomous driving requires real-time communication between multiple sensors, cameras, LiDAR systems, and central computing units. Automotive Ethernet provides the bandwidth and reliability necessary to support these complex ecosystems, making it a vital technology for autonomous innovation. The U.S. market is projected to reach USD 0.59 billion by 2026. In 2025, North America represented USD 0.65 billion, accounting for 19.43% of the worldwide market, and is projected to grow to USD 0.7 billion in 2026.

Europe

Europe held a considerable market share in 2024. Europe has been at the forefront of promoting smart mobility, with extensive investments in connected and autonomous vehicle technologies. Autonomous vehicles rely heavily on advanced sensor systems, cameras, radar, and LiDAR, all of which produce massive amounts of data that need to be processed and transmitted in real time. Ethernet in the automotive sector, with its high bandwidth and low latency capabilities, has emerged as the ideal solution to ensure seamless communication between various sensors, on-board systems, and external networks. The UK market is projected to reach USD 0.12 billion by 2026, and the Germany market is projected to reach USD 0.18 billion by 2026. The Europe market generated USD 0.85 billion in 2025, representing 25.40% of the global market landscape, and is expected to reach USD 0.92 billion in 2026.

Rest of the World

The rest of the world is expected to grow at a rapid CAGR during the forecast period. Car buyers in the Middle East & Africa region, particularly in affluent areas such as the Gulf Cooperation Council (GCC) countries, are seeking vehicles with enhanced infotainment and connectivity features. The ethernet is crucial for supporting high-definition video, audio, and internet connectivity within the vehicle, meeting the entertainment demands of modern consumers.

Competitive Landscape

Key Market Players

The market is consolidated and has a large number of brands that hold a strong foothold. These players have adopted various strategies, such as product differentiation & development, contracts, acquisitions, and collaborations, to gain a competitive advantage.

List of Key Automotive Ethernet Companies Profiled

- Broadcom Inc. (U.S.)

- Microchip Technology Inc. (U.S.)

- Marvell Technology, Inc. (U.S.)

- NXP Semiconductors N.V. (Netherlands)

- Texas Instruments Inc. (U.S.)

- Cadence Design Systems, Inc. (U.S.)

- Keysight Technologies Inc. (U.S.)

- STMicroelectronics NV (Switzerland)

- Analog Devices Inc. (Switzerland)

- Realtek Semiconductor Corp. (Taiwan)

Key Industry Developments

- March 2024 – ENNOVI introduced an automotive 10Gbps+ Ethernet Connector Solution. The Automotive Ethernet Connector designs have a standardized USCAR interface. ENNOVI-Net has press-fit pins as opposed to through-board solder pins. This patent-pending innovation thereby completely avoids the need for soldering. The Automotive Ethernet Connector ENNOVI-Net design solution allows for customization to accommodate specific board- and connector interface positioning, enabling integration into final applications.

- March 2024 – Analog Devices, Inc. (ADI) and the BMW Group announced their collaboration on the early adoption of ADI's E²B technology, which utilizes 10BASE-T1S Ethernet to the Edge bus within the automotive sector. This technology is essential for facilitating new zonal architectures in automotive design and aligns with trends such as software-defined vehicles. The BMW Group is positioned to be a pioneering original equipment manufacturer (OEM) in implementing this technology, specifically applying ADI's E²B in the design of ambient lighting systems for future BMW vehicles.

- February 2024 – AVIVA Links, Inc. announced the industry’s first family of multi-gigabit asymmetrical Ethernet devices based on the Automotive SerDes Alliance Motion Link Ethernet (ASA-MLE) draft specification. The new products include Ethernet PHYs, Switches, CSI-2 bridge ICs, and Zonal Aggregators, all of which are optimized for ultra-high bandwidth asymmetric video and control links.

- April 2023 – GRANITE RIVER LABS INC. launched the 10BASE-T1S Automotive Ethernet Test Standards. This networking technology is designed to address the challenges of data transmission in automotive environments by utilizing twisted-pair cables that can effectively transmit data at speeds of 10 Mbps. It operates efficiently even in noisy and highly electromagnetic conditions, which are common in automotive applications.

- November 2021 – Elektrobit launched the industry-first automotive Ethernet switch firmware for in-vehicle communications.

Report Coverage

The global automotive ethernet market report analyzes the market in-depth and highlights crucial aspects such as prominent companies, market segmentation, competitive landscape, and technology adoption. Besides this, the market analysis provides insights into the market trends and highlights significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 15.10% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type

By Bandwidth Outlook

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market size was USD 3.61 billion in 2026 and is anticipated to reach USD 11.13 billion by 2034.

The market will exhibit a CAGR of 15.10% over the forecast period (2026-2034).

By vehicle type, the passenger cars segment dominated the market in 2025.

Favorable trends associated with autonomous and connected vehicles to augment the market growth

Leading companies operating in the market include Broadcom Inc., Microchip Technology Inc., NXP Semiconductor N.V., Texas Instruments Inc., STMicroelectronics NV, and Analog Devices Inc.

Asia Pacific dominated the global market with a share of 48.98% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us