Automotive Fuse Market Size, Share & Industry Analysis, By Fuse Type (Blade Fuses, Glass Tube Fuses, Ceramic Fuses, High-Current Fuses, Resettable / PTC Fuses, and Semiconductor Fuses), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By Voltage (Low-Voltage Fuses and High-Voltage Fuses), By Application (Powertrain Systems, Body Electronics, Safety & ADAS Systems, Infotainment & Comfort Systems, and Battery & Charging Systems (EVs)), By Sales Channel (OEM and Aftermarket), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

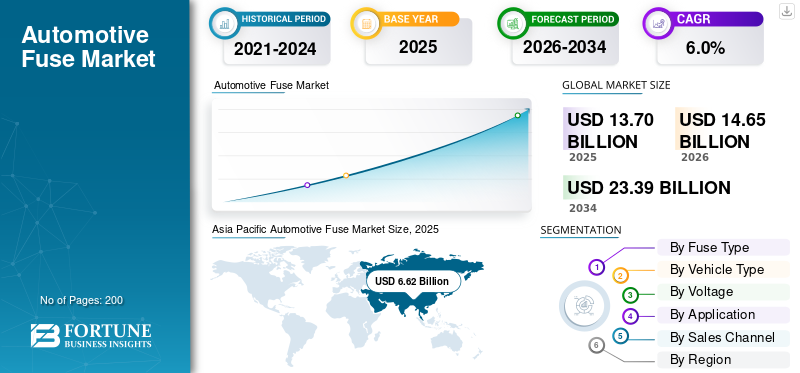

The global automotive fuse market size was valued at USD 13.70 billion in 2025. The market is projected to grow from USD 14.65 billion in 2026 to USD 23.39 billion by 2034, exhibiting a CAGR of 6.0% during the forecast period. Asia Pacific dominated the global market with a market share of 48.32% in 2025.

The market represents manufacturing electrical safety components that protect vehicle circuits from overcurrent, short circuits, and electrical faults. Automotive fuses are essential for maintaining the reliability of modern vehicles, where electronic systems now control critical functions such as lighting, infotainment, power distribution, safety modules, and body electronics. As vehicles become increasingly electrified and connected, fuse reliability has become a core requirement for vehicle safety and performance.

The market is expanding steadily, supported by the growing demand for vehicles with higher electronic content and improved electrical safety. The rise of electrified mobility, including battery electric and hybrid vehicles, has increased internal power loads and circuit complexity. This shift is closely tied to the expansion of EV charging infrastructure, EV charging networks, and DC fast chargers, which place greater electrical demands on onboard vehicle systems. Although fuses are not part of external chargers, they are critical in managing internal power flows that support modern charging technologies.

The adoption of smart charging solutions and integrated vehicle energy management systems will also influence the market’s growth during the forecast period. These developments are particularly relevant for fleet operators, where vehicle uptime, electrical safety, and reliability are critical. Public and private sector support, including investments in the National Electric Vehicle Infrastructure (NEVI), is further accelerating vehicle electrification and indirectly strengthening demand for robust automotive circuit protection.

Key players such as Littelfuse, Eaton, and Mersen are expected to focus on compact fuse designs, improved thermal stability, and compatibility with next-generation vehicle architectures. As the automotive industry continues its transition toward electrification and connected mobility, automotive fuses will remain a foundational component enabling safe and reliable vehicle operation.

Download Free sample to learn more about this report.

Automotive Fuse Market Key Takeaways

- 2025 Market Size: USD 13.70 billion

- 2026 Market Size: USD 14.65 billion

- 2034 Forecast Market Size: USD 23.39 billion

- CAGR: 6.0% from 2026–2034

- Asia Pacific dominated the automotive fuse market with a 48.32% share in 2025.

- The SUV segment is expected to grow at a CAGR of 8.0% over the forecast period.

- The high-voltage fuses segment is expected to grow at a CAGR of 9.9% over the forecast period.

North America

North America reached USD 2.88 billion in 2025.

Asia Pacific

Asia Pacific held the dominant share in 2025, valued at USD 6.62 billion.

Europe

Europe is projected to reach USD 3.54 billion by 2026.

U.S.

The U.S. market reached USD 2.19 billion in 2025.

Japan

The Japan market continues to support growth through strong vehicle production and electronics integration.

Read More

AUTOMOTIVE FUSE MARKET TRENDS

Shift toward Compact and High-Performance Fuse Designs is the Upcoming Trend

Manufacturers are developing compact fuses with improved thermal resistance to support dense electrical layouts. This trend enhances safety and reliability, supporting overall market share stability during the forecast period.

- Automotive suppliers are developing compact and thermally efficient fuse designs to support space-constrained vehicle electrical architectures.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Electronic Content in Modern Vehicles Accelerates Fuse Demand

The increasing integration of electronic systems in vehicles is a key driver for the global automotive fuse market. Advanced infotainment, safety features, and power management systems require reliable circuit protection. Growth in connected vehicles and electrified platforms further amplifies fuse demand, positively influencing long-term market growth.

- Rising integration of electronic modules in vehicles increases demand for reliable circuit protection components such as automotive fuses.

MARKET RESTRAINTS

Limited Product Differentiation and Pricing Pressure Hinder Industry Growth

Automotive fuses are standardized components, resulting in limited differentiation across suppliers. Intense price competition, especially for high-volume OEM contracts, can compress margins and restrict revenue growth, negatively impacting overall market expansion.

- For instance, standardization of automotive electrical components has intensified price competition among fuse suppliers, limiting margin expansion opportunities.

MARKET OPPORTUNITIES

Electrification and EV Power Management Expansion Offer Growth Opportunities

Vehicle electrification creates opportunities for advanced fuse solutions capable of handling higher loads and compact packaging. Growth in EV charging infrastructure and onboard power electronics supports demand for improved circuit protection designs.

- Growth in electric vehicle platforms is increasing demand for advanced circuit protection solutions capable of handling higher electrical loads.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Volatility

Fluctuations in raw material availability and global supply chain disruptions pose challenges for automotive fuse manufacturers. These issues can delay production schedules and negatively influence market growth.

- For instance, global automotive suppliers continue to face raw material price volatility, impacting cost stability across electrical component manufacturing.

Segmentation Analysis

By Vehicle Type

High Passenger Car Production Volumes Sustain Dominance of Hatchback/Sedan

To know how our report can help streamline your business, Speak to Analyst

On the basis of vehicle type, the market is divided into hatchback/sedan, SUV, LCV, and HCV.

Hatchback and sedan vehicles dominate the automotive fuse market share by vehicle type due to high global production volumes and extensive use of electrical components. These vehicles integrate multiple safety, lighting, and infotainment systems that require reliable circuit protection. Rising electronic content in passenger cars supports stable fuse demand, helping this segment retain a significant market share during the forecast period.

- Passenger cars account for the highest global vehicle volumes, driving sustained demand for standard automotive electrical protection components.

The SUV segment is expected to grow at a CAGR of 8.0% over the forecast period.

By Fuse Type

Standardization and Ease of Installation Makes Blade Fuses the Preferred Fuse Type

On the basis of fuse type, the market is sub-segmented into blade fuses, glass tube fuses, ceramic fuses, high-current fuses, resettable / PTC fuses, and semiconductor fuses.

Blade fuses dominate the market because of their standardized design, ease of installation, and cost efficiency. Automotive manufacturers widely adopt blade fuses across multiple applications, including lighting, infotainment, and body electronics. Their proven reliability and compatibility with modern vehicle architectures continue to drive adoption across OEM platforms.

- Blade fuses remain the most commonly used automotive fuse type due to standardized dimensions and ease of replacement.

The semiconductor fuses segment is expected to grow at a CAGR of 10.0% over the forecast period.

By Voltage

Low-voltage Systems Drive the Highest Fuse Demand Resulting in its Dominance

On the basis of voltage, the market is segmented into low-voltage fuses and high-voltage fuses.

Low-voltage fuses dominate the market as most in-vehicle electrical systems operate within low-voltage ranges. Body electronics, infotainment systems, and control units rely heavily on low-voltage protection. The growing demand for electronic features in modern vehicles further reinforces the dominance of this segment.

- Most vehicle electronic systems operate on low-voltage architectures, requiring extensive use of low-voltage circuit protection devices.

The high-voltage fuses segment is expected to grow at a CAGR of 9.9% over the forecast period.

By Application

Body Electronics is the Leading Application as it Generates Highest Demand for Automotive Fuse

On the basis of application, the market is segmented into powertrain systems, body electronics, safety & ADAS systems, infotainment & comfort systems, and battery & charging systems (EVs).

Body electronics dominate fuse demand due to the high number of circuits used in lighting, power windows, climate control, and safety systems. Each function requires individual protection, increasing fuse usage per vehicle. The increased adoption of comfort and convenience features continues to strengthen this segment’s contribution to overall market size.

- Body electronics systems such as lighting, windows, and climate control rely heavily on fuse-based circuit protection.

Battery and Charging Systems (EVs) segment is expected to grow at a CAGR of 9.4% over the forecast period.

By Sales Channel

OEM Sourcing Agreements Ensure Segment Leadership

On the basis of sales channel, the market is segmented into OEM and aftermarket.

The OEM segment dominates due to long-term supply agreements with key players and large-volume procurement. Direct integration of fuses during vehicle assembly ensures consistent demand and stable revenue streams. OEM dominance also reflects the importance of quality certification and compliance in automotive electrical systems.

- Automotive OEMs source fuses directly during vehicle assembly to ensure compliance with quality and safety standards.

The aftermarket segment is expected to grow at a CAGR of 6.8% over the forecast period.

Automotive Fuse Market Regional Outlook

By geography, the global automotive fuse market is categorized into North America, Europe, Asia Pacific, and rest of the world.

Asia Pacific

Asia Pacific Automotive Fuse Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025 at USD 6.62 billion, and will also exhibit the fastest growth rate of 6.5%. The region’s leading position can be attributed to high vehicle production and strong presence of suppliers across China, Japan and South Korea. Rising electronics penetration and electrification initiatives continue to support growth.

- For instance, in 2024, IBEF reported Asia Pacific leads global vehicle production, supporting large-scale adoption of digital instrument clusters across mass-market and premium vehicles.

China Automotive Fuse Market

China’s market is projected to be one of the largest worldwide, with 2025 hitting USD 3.77 billion, representing roughly 27.5% of the global market.

India Automotive Fuse Market

The India automotive fuse market in 2025 reached USD 0.66 billion, accounting for roughly 4.8% of global revenues.

Europe

Europe is projected to record a growth rate of 5.7% in the coming years, which is the second highest among all regions, and reach a valuation of USD 3.54 billion in 2026. Europe’s automotive fuse market growth is expected to be steady due to strict safety regulations and increasing electronic content in vehicles. OEM focus on reliability, efficiency, and compliance sustains demand for circuit protection components.

Germany Automotive Fuse Market

Germany in 2025 achieved USD 0.79 billion, accounting for roughly 5.8% of global revenues.

U.K. Automotive Fuse Market

The U.K. automotive fuse market in 2025 captured USD 0.50 billion, accounting for roughly 3.6% of global sales.

North America

North America reached USD 2.88 billion in 2025 and secured the position of the third-largest region. The regional market is driven by advanced vehicle electronics and steady OEM demand. The U.S. plays a key role, supported by strong innovation in safety systems and electrification. Continued investments in vehicle technology and compliance standards support stable growth across the region.

U.S. Automotive Fuse Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market reached USD 2.19 billion in 2025, representing roughly 16.0% of the global Market.

Rest of the World

The rest of the world market, including Latin America, experiences moderate growth supported by expanding vehicle assembly operations. Improving safety regulations and gradual electronics adoption contribute to rising fuse demand, although growth remains slower than in developed automotive regions.

COMPETITIVE LANDSCAPE

Key Industry Players

OEM Partnerships and Electrification-Driven Product Strategies to Help Gain Advantage

The competitive landscape of the global automotive fuse market is shaped by a group of established multinational manufacturers and specialized circuit protection suppliers. They compete primarily on product reliability, compliance with automotive standards, manufacturing scale, and long-term relationships with OEMs. The market is moderately consolidated, with leading suppliers holding a significant market share through direct supply agreements with global vehicle manufacturers.

To gain competitive advantage, companies are expanding their fuse portfolios to support low-voltage and higher-load applications driven by vehicle electrification. Suppliers are aligning product development with emerging charging technologies and onboard power distribution requirements linked to the growth of global EV charging ecosystems. Strategic investments in R&D enable manufacturers to deliver compact, high-performance fuses that meet the evolving needs of electric and connected vehicles.

Key players are also strengthening their presence in North America and Asia, where vehicle electrification and public charging expansion are accelerating. Collaboration with OEMs, Tier-1 suppliers, and infrastructure stakeholders involved in charging services helps fuse manufacturers integrate their products early in vehicle design cycles. Additionally, suppliers increasingly tailor solutions for commercial fleets, addressing reliability requirements specific to fleet operators and high-utilization vehicles.

Overall, competition in the automotive fuse market is increasingly defined by technological alignment with electrification trends, operational efficiency, and the ability to support future-ready vehicle electrical systems in a rapidly evolving mobility landscape.

- For instance, Littelfuse expanded its automotive circuit protection portfolio to support evolving vehicle electrical architectures, reinforcing long-term supply partnerships with global OEMs.

LIST OF KEY AUTOMOTIVE FUSE COMPANIES PROFILED

- Littelfuse, Inc. (U.S.)

- Eaton Corporation (Ireland)

- Mersen (France)

- Bel Fuse Inc. (U.S.)

- Schurter Holding AG (Switzerland)

- Panasonic Corporation (Japan)

- SIBA GmbH (Germany)

- Vicfuse (China)

- Conquer Electronics (Taiwan)

- AEM Components (U.S.)

KEY INDUSTRY DEVELOPMENTS

- August 2025: SCHURTER launched the ALO high-performance EV fuse series, covering up to 1000 VDC and currents up to 900A with multiple mounting options. The new series targets protection for PDUs, battery disconnect units, and powertrain electronics where compactness and mechanical robustness are critical.

- July 2025: Mersen published an updated overview of its e-mobility solutions, highlighting high-speed fuse protection for EV platforms and charging ecosystems. The communication underscores ongoing portfolio expansion around battery protection and high-power electrification needs.

- May 2025: Littelfuse launched the Nano^2 415 SMD fuse with a 1500A interrupting rating at 277V, positioning it for space-constrained electronics that still face high fault-current risks. The release supports OEMs shifting from legacy through-hole protection to compact surface-mount designs.

- April 2025: Eaton announced a new line of advanced pyro fuses for EV architectures, including a dual-trigger version intended to improve safety and reliability during high-energy fault isolation. This reflects increasing focus on fast, deterministic disconnection in high-voltage battery

- March 2025: Littelfuse released the AEC-Q200-qualified 823A Series, a high-voltage (1000 Vdc) SMD fuse aimed at EV power systems such as BMS, battery disconnect units, and high-voltage DC-DC converters. The product targets tighter packaging requirements while maintaining automotive reliability expectations.

REPORT COVERAGE

- The global automotive fuse market analysis provides an in-depth study of market size & forecast by all segments. It includes details on market dynamics and trends that are expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.0% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, Fuse Type, Voltage, Application, Sales Channel, and Region |

|

By Fuse Type |

· Blade Fuses · Glass Tube Fuses · Ceramic Fuses · High-Current Fuses · Resettable / PTC Fuses · Semiconductor Fuses |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · LCV · HCV |

|

By Voltage |

· Low-Voltage Fuses · High-Voltage Fuses |

|

By Application |

· Powertrain Systems · Body Electronics · Safety & ADAS Systems · Infotainment & Comfort Systems · Battery and Charging Systems (EVs) |

|

By Sales Channel |

· OEM · Aftermarket |

|

By Geography |

· North America (By Fuse Type, Vehicle Type, Voltage, Application, Sales Channel, and Country) o U.S. o Canada o Mexico · Europe (By Fuse Type, Vehicle Type, Voltage, Application, Sales Channel, and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Fuse Type, Vehicle Type, Voltage, Application, Sales Channel, and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Fuse Type, Vehicle Type, Voltage, Application, Sales Channel, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 13.70 billion in 2025 and is projected to reach USD 23.39 billion by 2034.

In 2025, Asia Pacific’s market value stood at USD 6.62 billion.

The market is expected to exhibit a CAGR of 6.0% during the forecast period of 2026-2034.

The hatchback/sedan segment led the market by vehicle type.

Rising electronic content in modern vehicles is driving the global automotive fuse market.

Littelfuse, Eaton Corporation, Bel Fuse, and Schurter Holding are some of the top players in the market.

Asia Pacific dominated the market by holding the largest share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us