Automotive Powertrain Sensor Market Size, Share & Industry Analysis, By Type (Position Sensor, Speed Sensor, Temperature Sensor, and Others), By Vehicle Type (Passenger Car, LCV, and HCV), By Propulsion Type (ICE and Electric), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

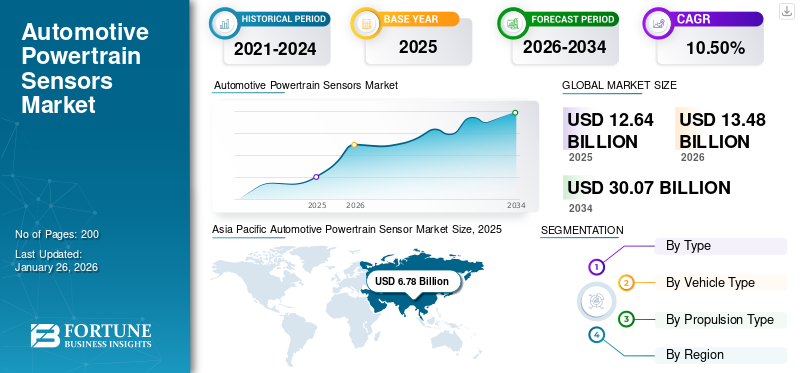

The global automotive powertrain sensor market size was valued at USD 12.64 billion in 2025 and is projected to grow from USD 13.48 billion in 2026 to USD 30.07 billion by 2034, exhibiting a CAGR of 10.50% during the forecast period. Asia Pacific dominated the global market with a share of 53.69% in 2025.

The automotive industry is undergoing a significant transformation, driven by advancements in technology, stringent emission regulations, and a growing demand for fuel efficiency and vehicle performance. Automotive powertrain sensors are devices that monitor and measure various parameters within the powertrain system of a vehicle. The powertrain, which includes the engine, transmission, and drivetrain, is responsible for converting fuel into motion. Automotive powertrain sensors provide real-time data to the vehicle's control systems, enabling precise adjustments to optimize performance, fuel efficiency, and emissions.

Automotive powertrain sensors benefit from optimizing the air-fuel mixture, ignition timing, and Exhaust Gas Recirculation (EGR) to improve fuel efficiency and reduce harmful emissions. By providing accurate, real-time data on engine performance, transmission efficiency, and drivetrain dynamics, powertrain sensors enable vehicles to operate more efficiently, enhancing both performance and safety. The market’s growth is supported by the shift toward hybrid and electric vehicle technologies, which has created substantial demand for sophisticated monitoring systems that can optimize performance and efficiency. Regulatory frameworks focusing on emissions reduction and fuel economy standards are compelling manufacturers to integrate advanced sensor technologies into their powertrain systems. This regulatory pressure, combined with consumer preferences for environmentally conscious vehicles, is driving innovation in sensor applications.

Key players in the market include Robert Bosch, ZF Friedrichshafen, Texas Instruments, Delphi Technologies, Denso Corporation, and Hella GmbH, which compete in the development of new products and pricing.

Download Free sample to learn more about this report.

Automotive Powertrain Sensor Market Trends

Rise of Autonomous Vehicles to Positively Influence Market Growth

The development of autonomous vehicles is another significant trend influencing the automotive powertrain sensor market. Autonomous vehicles rely heavily on sensor data to make real-time decisions, making the integration of advanced technologies crucial for ensuring sensors’ accuracy and reliability. Automakers are developing self-driving capabilities that prioritize ethernet adoption in the platforms. This trend is predicted to reshape the market and drive rapid growth.

For instance, in December 2024, Uber Technologies, Inc. and WeRide launched the launch of their ride-hailing partnership in Abu Dhabi. This initiative showcases availability of Autonomous Vehicles (AVs) on the Uber platform for the first time outside the U.S., and represents the largest commercial robotaxi service operating outside the U.S. and China.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Rising Demand for Electric Vehicles to Augment Market Growth

The automotive industry has undergone a significant transformation, largely driven by the rapid adoption of Electric Vehicles (EVs). The rising demand for electric vehicles is directly linked to the growing demand for advanced and efficient powertrain sensors, an important development driving market growth.

Governments are offering tax rebates, subsidies, and other incentives to encourage the adoption of EVs, which in turn increases the demand for powertrain sensors. Continuous improvements in sensor technology, such as increased accuracy, reliability, and miniaturization, are making powertrain sensors more effective and cost-efficient. Automakers and sensor manufacturers are investing heavily in R&D to develop advanced sensors tailored to the unique requirements of EVs. Additionally, the increasing emphasis on vehicle safety and energy efficiency is driving the demand for high-performance powertrain sensors.

Market Restraints

High Initial Costs to Hamper Market Growth

One of the most significant barriers to the automotive powertrain sensor market growth is the high initial costs associated with its deployment. The cost of advanced powertrain sensors can pose a challenge for some manufacturers, particularly in emerging markets. These sensors often incorporate cutting-edge technology and high-quality materials to ensure reliability and durability. Additionally, their development and manufacturing processes are complex and require significant investment in Research and Development (R&D) and specialized manufacturing equipment, factors that drive up the cost of production. As a result, high costs can deter automotive manufacturers and consumers from adopting advanced powertrain sensors, particularly in cost-sensitive markets.

Market Opportunities

Integration of Advanced Technologies to Positively Influence Market Growth

The integration of Artificial Intelligence (AI) and Machine Learning (ML) with powertrain sensors is opening new avenues for enhancing vehicle performance and predictive maintenance. These technologies improve the accuracy and efficiency of sensors, leading to better fuel economy and reduced emissions. AI and ML algorithms can analyze data from powertrain sensors to predict potential failures before they occur. This predictive maintenance reduces downtime and repair costs and enhances vehicle reliability and safety. Additionally, IoT enables powertrain sensors to communicate with other vehicle systems and external networks. This connectivity facilitates the collection and analysis of vast amounts of data, which can be used to optimize vehicle performance, enhance diagnostics, and enable new services. This development is expected to drive market growth during the forecast period.

Segmentation Analysis

By Type

Growing Technological Advancement Boosted Position Sensor Segment Growth

On the basis of type, the market is segmented into position sensor, speed sensor, temperature sensor, and others.

The position sensor segment is anticipated to hold a dominant market share of 41.90% in 2026. The integration of advanced technologies such as capacitive, inductive, and magnetic sensing methods has enhanced the accuracy and reliability of position sensors, driving segment growth.

For instance, in February 2023, Continental introduced a new high-speed e-motor rotor position sensor. The high-speed inductive e-motor Rotor Position Sensor (eRPS) detects the exact position of the rotor in a synchronous electric machine, which helps increase efficiency and enables smoother operations.

By Vehicle Type

Rising Adoption of EVs Encouraged Passenger Car Segment Growth

Based on vehicle type, the market is divided into passenger car, LCV (Light Commercial Vehicle), and HCV (Heavy Commercial Vehicle).

The passenger car segment is anticipated to hold a dominant market share of 80.03% in 2026. The high volume of passenger car sales directly correlates with the increased demand for powertrain sensors, which are essential for optimizing engine performance and ensuring compliance with emissions regulations. Additionally, the increasing adoption of electric vehicles is also contributing to the growth of the passenger car segment within the powertrain sensor market.

By Propulsion Type

Electric Segment is Expected to Depict Fastest Growth Due to Increased Investment in EV Infrastructure

Based on the propulsion type, the market is divided into ICE and electric.

The electric propulsion type segment is expected to grow at the fastest rate during the forecast period. As governments and private sectors invest heavily in EV infrastructure, including charging stations and battery technology, the demand for powertrain sensors will continue to rise. These investments support the broader adoption of electric vehicles, creating a favorable environment for sensor manufacturers.

Automotive Powertrain Sensor Market Regional Outlook

The global market regions are segmented into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Powertrain Sensor Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region captured 53.69% of the global market in 2025, generating USD 6.78 billion in revenue, and is projected to reach USD 7.29 billion in 2026, due to high automobile production levels, driven by strong demand from China, India, and Japan. The region's rapid industrialization, urbanization, and increasing disposable incomes are propelling the demand for vehicles equipped with advanced powertrain sensors. This development is expected to continue driving the market growth during the forecast period. China leads global EV production, significantly contributing to the demand for powertrain sensors tailored for electric and hybrid vehicles. The Japan market is projected to reach USD 1.1 billion by 2026, the China market is projected to reach USD 4.3 billion by 2026, and the India market is projected to reach USD 0.66 billion by 2026.

Europe

Europe holds a substantial share of the automotive powertrain sensor market, driven by stringent emission regulations and a strong presence of major automotive manufacturers. The region promotes cleaner technologies and the adoption of electric vehicles through incentives and subsidies, further increasing the demand for specialized powertrain sensors. Germany, France, and the U.K. are at the forefront of this trend. Continuous improvements in sensor accuracy and integration capabilities further enhance their attractiveness to manufacturers in the region. The UK market is projected to reach USD 0.25 billion by 2026, and the Germany market is projected to reach USD 1.06 billion by 2026. In 2025, the Europe market stood at USD 3.14 billion, representing 24.82% of global demand, and is projected to grow to USD 3.38 billion in 2026.

North America

North America will grow at a steady pace during the forecast period. The increasing sales of EVs in the U.S. reflect a growing shift toward sustainable transportation solutions. This trend is further boosting the need for advanced powertrain sensors capable of monitoring critical vehicle parameters. The U.S. market is projected to reach USD 1.43 billion by 2026. North America contributed approximately USD 2.09 billion to the global market in 2025, accounting for 16.50% share, and is expected to reach USD 2.15 billion in 2026.

Rest of the World

In 2025, Rest of the World represented USD 0.63 billion, accounting for 4.98% of the worldwide market, and is projected to grow to USD 0.66 billion in 2026.

Competitive Landscape

Market Players are Focusing on Development of Advanced Sensor Technologies to Gain Competitive Advantage

Leading companies operating in the market include Robert Bosch., ZF Friedrichshafen, NXP Semiconductor N.V., and Analog Devices Inc.

Technological advancements in sensor technology, such as the development of MEMS (Micro-Electro-Mechanical Systems) sensors, are enhancing the accuracy and reliability of powertrain sensors. These innovations are also helping to reduce the cost of sensors, making them more accessible to a wider range of vehicle types.

Continental AG is a German company that offers a wide range of automotive products and services. The company's powertrain sensor portfolio includes sensors for engine management, transmission, and exhaust systems. Known for its advanced sensor technologies and integrated solutions, the company has a strong presence in Europe and North America. The company is recognized as a key player in the market, with a strong focus on innovation and customer satisfaction.

List of Key Automotive Powertrain Sensor Companies

- Robert Bosch (Germany)

- ZF Friedrichshafen (Germany)

- Texas Instruments (U.S.)

- Continental AG (Germany)

- Delphi Technologies (U.K.)

- PVB Piezotronics(China)

- Valeo (France)

- Balluff Automation (Germany)

- Denso Corporation (Japan)

- Thyssenkrupp (Germany)

- Hella GmbH (Germany)

- NXP Semiconductors (Netherlands)

Key Industry Developments

- November 2024 – Continental Automotive Technologies has entered into a partnership with NOVOSENSE Microelectronics, a specialist in high-performance analog and mixed-signal semiconductor solutions, to jointly develop automotive-grade sensor technologies aimed at enhancing vehicle safety systems. The collaboration between the two companies focuses on creating advanced sensing solutions that will contribute to improved safety standards in automotive applications.

- October 2024 – Honeywell introduced two new solutions to optimize Electric Vehicle (EV) safety for drivers and enhance manufacturing for gigafactories. The technologies developed by Honeywell Process Solutions and Honeywell Sensing Solutions, support the company’s strategic alignment with three powerful megatrends, including the global energy transition.

- February 2023 – Continental announced the expansion of its sensor portfolio to cater to the fast-growing electric vehicle market with the introduction of a new innovative sensor. The high-speed inductive e-motor Rotor Position Sensor (eRPS) detects the actual position of the rotor in a synchronous electric machine, which helps to increase efficiency and allows smoother operations. Compared to existing resolver sensors, the eRPS is more compact and 40% lighter.

- December 2022 – Honeywell signed a strategic alliance with Nexceris, the developer of Li-ion Tamer lithium-ion gas detection solutions, to enhance the safety of electric vehicles (EVs). Under this partnership, Honeywell and Nexceris will co-develop sensor-based solutions to help prevent conditions that lead to thermal runaway in EV batteries, a hazardous phenomenon that causes extremely high temperatures within the battery cell and can result in fires.

- May 2022 – Continental introduced new sensors to protect the batteries of electrified vehicles. These additions to its extended sensors portfolio are tailored to support both road safety and electrification.

Report Coverage

The global automotive powertrain sensor market report analyzes the market in-depth and highlights crucial aspects such as prominent companies, market segmentation, competitive landscape, and technology adoption. Besides this, the market analysis provides insights into the market trends and highlights significant industry developments. In addition, the report encompasses several factors contributing to the market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.50% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Vehicle Type

By Propulsion Type

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market was valued at USD 12.64 billion in 2025 and is anticipated to reach USD 30.07 billion by 2034.

The market will exhibit a CAGR of 10.50% during the forecast period (2026-2034).

By vehicle type, the passenger car segment dominated the market in 2025.

Rising demand for electric vehicles is a key factor driving market growth.

Leading companies operating in the market include Robert Bosch., ZF Friedrichshafen, NXP Semiconductor N.V., and Analog Devices Inc.

Asia Pacific dominated the global market with a share of 53.69% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us