Automotive GaN Power Devices Market Size, Share & Industry Analysis, By Device Type (GaN Power Transistors, GaN Power ICs, and GaN Power Modules), By Application (On-Board Chargers (OBCs), DC-DC Converters, Auxiliary/Partial Traction Inverters, and ADAS & Infotainment Power Supplies), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By Voltage Rating (≤200 V, 201–400 V, and 401–650 V), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

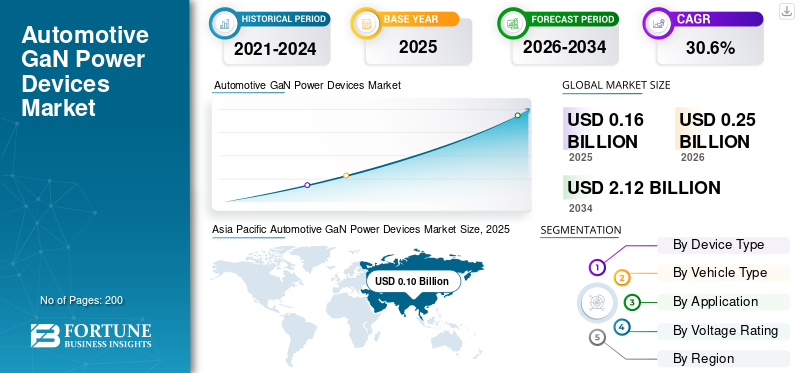

The global automotive GaN power devices market size was valued at USD 0.16 billion in 2025. The market is projected to grow from USD 0.25 billion in 2026 to USD 2.12 billion by 2034, exhibiting a CAGR of 30.6% during the forecast period. Asia Pacific dominated the global automotive GaN power devices market with a market share of 62.5% in 2025.

The global market growth is driven by rising electrification and the need for higher-efficiency, higher-power-density power conversion in vehicles. Growth is strongest in on-board chargers (OBCs) and HV/LV DC-DC converters, where GaN enables faster switching, smaller magnetics, lower losses, and lighter designs. The increasing adoption of software-defined vehicles is also boosting the use of GaN (gallium nitride) in ADAS and infotainment power supply, as compute loads and point-of-load conversion requirements rise. At the same time, automakers and Tier-1s are prioritizing automotive qualification and supply-chain resilience, prompting partnerships between device makers and foundries to scale 200-mm GaN production and improve cost structures.

- For instance, in December 2025, onsemi announced a collaboration with Global Foundries to develop and manufacture next-generation GaN power devices, starting with 650V products, which reinforces capacity expansion and accelerates GaN roadmaps for high-performance power stages relevant to automotive power conversion.

Major players in the global automotive GaN power devices market include Infineon Technologies, STMicroelectronics, Texas Instruments, NXP Semiconductors, Renesas Electronics, ROHM, onsemi, Navitas Semiconductor, and Transphorm. These companies compete through automotive-qualified GaN portfolios, integrated power ICs, scalable manufacturing partnerships, system-level reference designs, and close collaboration with OEMs to enable high-efficiency EV power electronics.

Download Free sample to learn more about this report.

AUTOMOTIVE GAN POWER DEVICES MARKET TRENDS

Automotive-Qualified GaN Moves from Lab to Platform-Ready Power Stages

Automotive GaN is transitioning from evaluation to platform-ready deployment as suppliers introduce more AEC-qualified device families and reference designs, thereby shortening OEM validation cycles. The trend is evident in the push toward integrated GaN power stages (device, driver, and protection) and bidirectional switching architectures that enhance efficiency, reduce component count, and minimize passive magnetics. This enables smaller onboard power units and supports higher electrical loads from centralized compute and zonal architectures. As qualification breadth improves, gallium nitride GaN power devices usage is expanding from niche high-end EV programs toward broader vehicle classes, especially in auxiliary converters and low-voltage domains. In October 2025, Infineon announced the production launch of its CoolGaN Automotive Transistor 100 V G1 family, which is qualified to AEC-Q101.

MARKET DYNAMICS

MARKET DRIVERS

Faster, Lighter EV Charging Hardware Accelerates GaN Device Pull

Higher EV volumes and rising charger power levels are intensifying demand for high-efficiency, increasing demand for high-performance, high-frequency switching, where GaN offers strong advantages over silicon in onboard chargers and related converter stages. OEMs and Tier-1s value GaN’s ability to increase power densities, improve overall efficiency, and reduce thermal management burden, directly translating into smaller, lighter onboard power units and potentially improved vehicle range. This driver is strongest in mass-market EV programs that prioritize cost and packaging, especially where GaN enables two-in-one integration of OBC and DC-DC functions. As scale increases, GaN device demand rises in premium models and across high-volume platforms. This is expected to boost the automotive GaN power devices market growth in the coming years. In December 2025, Inovance Automotive and Innoscience announced that their 6.6 kW, 650V GaN OBC had entered mass installation on Changan vehicles.

MARKET RESTRAINTS

Stringent Automotive Stress-Testing Raises Time-to-Market Requirements

Automotive power semiconductors must meet stringent reliability expectations across wide temperature swings, long lifetimes, vibration, humidity, and electrical overstress conditions. For GaN, this restraint manifests as longer qualification timelines, repeated design iterations for packaging and gate-drive robustness, and extended customer validation before the Start of Production (SOP). Even when device performance is compelling, the burden of proving consistent reliability at automotive duty cycles can delay volume ramp, especially for new GaN process nodes and newer suppliers. As a result, adoption often begins in less safety-critical or more modular power blocks (such as OBC/DC-DC) before expanding into broader, higher-risk architectures. In March 2021, the Automotive Electronics Council issued AEC-Q101 Rev E, defining failure-mechanism-based stress-test qualification requirements for discrete semiconductors used in automotive applications.

MARKET OPPORTUNITIES

200-mm GaN Manufacturing Partnerships Open a Cost-Down Runway

A major opportunity lies in the shift toward scaled GaN manufacturing, including 200-mm GaN-on-silicon processes and deeper foundry partnerships, to improve yields, reduce unit costs, and enhance supply assurance for automotive programs. Automotive OEMs, data centers, and Tier-1s typically demand long product lifecycles, multi-source strategies, and predictable capacity; scaling GaN production helps meet these expectations while enabling wider deployment beyond early-adopter EV segments. As costs fall, GaN power devices become more attractive for mid-voltage converters across passenger and commercial vehicles, and for the expanding power needs of zonal ECUs and advanced infotainment/ADAS compute. Greater manufacturing scale also supports the development of more integrated GaN ICs and modules. In December 2024, ROHM and TSMC announced a strategic collaboration to develop and mass-produce automotive GaN power devices.

MARKET CHALLENGES

Scaling Supply While Meeting Automotive Reliability and Cost Targets

A central challenge is achieving simultaneous improvements in cost, capacity, and automotive-grade reliability without sacrificing performance. GaN roadmaps increasingly require advanced processes, tighter defect control, robust packaging, and repeatable qualification across multiple fabs. Meanwhile, OEM design cycles are unforgiving; any late change in process, package, or test flow can trigger re-validation. This creates pressure on suppliers to maintain stable manufacturing while still driving aggressive cost reductions and ramping up volume. The challenge is amplified by competition from mature silicon and entrenched SiC in high voltage traction, forcing GaN makers to prove total system value and long-term supply continuity. In December 2025, onsemi and GlobalFoundries announced a collaboration to develop and manufacture next-generation 650V GaN power products using GF’s 200mm eMode GaN-on-silicon process.

Download Free sample to learn more about this report.

Segmentation Analysis

By Device Type

High-Volume Switching Efficiency Drives GaN Power Transistors Leadership

Based on device type, the market is segmented into GaN power transistors, GaN power ICs, and GaN power modules.

GaN power transistors dominate the market due to their broad applicability across onboard chargers, DC-DC converters, and auxiliary inverter stages. Their relatively lower cost, design flexibility, and faster automotive qualification compared with integrated solutions make them the preferred choice for high-volume EV platforms. OEMs favor discrete GaN transistors for scalable architectures, particularly in 400-650 V systems, which support sustained volume growth across passenger vehicles.

- In October 2023, Infineon launched its CoolGaN Automotive Transistor 100 V family, qualified to AEC-Q101, which accelerates the adoption of GaN transistors in automotive power systems.

The GaN Power ICs segment is projected to grow at a CAGR of 35.5% over the forecast period.

By Vehicle Type

Mass-Market Electrification Sustains Hatchback and Sedan Dominance

Based on vehicle type, the market is segmented into hatchback/sedan, SUV, LCV, and HCV.

Hatchback and sedan vehicles dominate GaN power device demand due to their high production volumes and accelerating electrification across mass-market segments. These vehicles extensively utilize GaN-based OBCs and DC-DC converters to optimize efficiency and reduce costs. Strong penetration of efficient and compact and mid-size EVs, particularly in Asia and Europe, ensures consistent GaN volume consumption despite the growing popularity of larger vehicle categories.

- In January 2024, BYD reported strong global sales growth driven largely by compact and mid-size electric sedans, underscoring sustained demand from this vehicle class.

The SUV segment is projected to grow at a CAGR of 32.7% over the forecast period.

By Application

Compact, High-Efficiency Charging Architectures Anchor Demand for On-Board Chargers (OBCs)

Based on application, the market is segmented into on-board chargers (OBCs), DC-DC converters, auxiliary/partial traction inverters, and ADAS & infotainment power supplies.

On-board chargers dominate GaN device demand, as GaN enables higher switching frequencies, reduced magnetics size, improved charging efficiency, and is expected to operate at higher frequencies. OEMs are increasingly deploying GaN in 6.6 kW-11 kW OBCs to reduce weight and thermal losses, while supporting compact vehicle packaging, with satellite communications. This dominance is reinforced by the rising volumes of EVs and the transition toward integrated OBC-DC-DC architectures.

- In November 2023, Renault highlighted next-generation compact OBC designs as a core enabler for EV efficiency improvements, reinforcing the importance of advanced power semiconductors in charging systems.

The ADAS & infotainment power supplies segment is projected to grow at a CAGR of 40.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Voltage Rating

Mid-Voltage Power Density Positions 401-650 V as the Core GaN Range

Based on voltage rating, the market is segmented into ≤200 V, 201-400 V, and 401-650 V.

The 401-650 V segment dominates the automotive GaN power devices market share as it aligns directly with EV onboard chargers and high-efficiency DC-DC converters operating in 400 V and emerging 800 V architectures. GaN’s performance advantages are most pronounced in this range, enabling smaller systems and higher efficiency, which are critical for EV energy management and thermal optimization.

- In December 2024, ROHM and TSMC announced a collaboration to develop and mass-produce automotive GaN power devices, focusing on high-performance voltage ranges suitable for EV efficiency power conversion.

The ≤200 V segment is projected to grow at a CAGR of 35.1% over the forecast period.

AUTOMOTIVE GAN POWER DEVICES MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Automotive GaN Power Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to massive EV production volumes, rapid electrification, and a strong manufacturing base. High adoption of GaN in onboard chargers and DC-DC converters is supported by cost-sensitive mass-market EVs and expanding consumer electronics content. The region benefits from close integration between automakers and semiconductor suppliers, which accelerates the qualification and cost reduction of GaN across both passenger and commercial vehicles.

China Automotive GaN Power Devices Market

China leads global GaN demand, driven by large-scale EV production, widespread deployment of high-efficiency onboard chargers, and rapid adoption of advanced power electronics across mass-market electric sedans and SUVs.

Japan Automotive GaN Power Devices Market

Japan’s growth is supported by hybrid and EV platforms emphasizing compact, reliable power electronics, with GaN adoption focused on DC-DC converters and auxiliary power systems.

India Automotive GaN Power Devices Market

India represents a rapidly growing market, with increasing EV adoption and a focus on cost-efficient, compact power electronics, creating emerging demand for GaN devices in onboard chargers and DC-DC converters.

North America

The North American market is growing steadily, supported by rising EV adoption, increasing integration of high-efficiency onboard chargers, and growing electronics content in vehicles. OEMs focus on higher power density, faster charging, and reduced thermal losses, which support the adoption of GaN in OBCs, DC-DC converters, and ADAS power supplies. Strong R&D activity, early technology adoption, and collaboration between automakers and semiconductor industry suppliers further accelerate the deployment of GaN across passenger and light commercial vehicles.

U.S. Automotive GaN Power Devices Market

The U.S. drives regional demand due to its high EV penetration, strong adoption of high-power onboard chargers, and growing use of advanced ADAS and infotainment systems, which require efficient, compact GaN-based power supplies.

Europe

Europe represents a strong growth region for automotive GaN power devices, driven by stringent emission regulations, high EV penetration, and rapid standardization of EV platforms. Automakers increasingly deploy GaN in onboard chargers and DC-DC converters to improve efficiency and reduce vehicle weight. The region’s focus on compact vehicle design, premium electric vehicles EVs, and energy efficiency, along with a strong semiconductor ecosystem, supports sustained adoption of GaN across multiple vehicle segments.

U.K. Automotive GaN Power Devices Market

The U.K. market benefits from rising EV sales and a strong focus on compact, efficient power electronics in passenger vehicles, supporting the use of GaN in onboard chargers and low-voltage ADAS power systems.

Germany

Germany drives GaN adoption through premium EV platforms and advanced powertrain architectures, with strong emphasis on high-efficiency onboard chargers, integrated power electronics, and automotive-grade semiconductor innovation.

Rest of the World

The Rest of the World market is expanding gradually, supported by increasing EV penetration, improving charging infrastructure, and rising electronics content in vehicles. Adoption of GaN power devices remains limited to early-stage EV programs and premium models, but growing regulatory support and infrastructure investment create long-term growth potential, particularly for onboard chargers and low-voltage power supplies.

COMPETITIVE LANDSCAPE

Key Industry Players

Electrification, Power Density Innovation, and Strategic Manufacturing Alliances Shape GaN Power Device Competition

The global automotive GaN power devices market trends are characterized by intense competition driven by rapid electrification, demand for higher power density, and stringent automotive reliability requirements. Leading semiconductor players, including Infineon Technologies, STMicroelectronics, NXP Semiconductors, Texas Instruments, Renesas, ROHM, onsemi, Navitas Semiconductor, and Transphorm, compete through advanced GaN transistor portfolios, integrated GaN power ICs, and automotive-qualified modules. Competitive differentiation increasingly depends on the breadth of AEC-Q qualification, cost reduction through 200-mm GaN manufacturing, system-level reference designs, and close collaboration with OEMs and Tier-1 suppliers. Strategic partnerships with foundries and packaging specialists are critical to ensure scalable capacity and long-term supply assurance. Companies are also investing in application-specific solutions for onboard chargers, DC-DC converters, and ADAS power supplies to secure platform-level design wins. In December 2024, ROHM and TSMC announced a strategic collaboration to jointly develop and mass-produce automotive-grade GaN power devices, strengthening manufacturing scale and supply stability.

LIST OF KEY AUTOMOTIVE GaN POWER DEVICE COMPANIES PROFILED

- Infineon Technologies AG (Germany)

- STMicroelectronics (Switzerland)

- NXP Semiconductors N.V. (Netherlands)

- Texas Instruments Incorporated (U.S.)

- Renesas Electronics Corporation (Japan)

- ROHM Semiconductor (Japan)

- ON Semiconductor Corporation (U.S.)

- Panasonic Industry Co., Ltd. (Japan)

- Navitas Semiconductor Corporation (U.S.)

- Transphorm, Inc. (U.S.)

- Mitsubishi Electric Corporation (Japan)

- Power Integrations, Inc. (U.S.)

- Toshiba Electronic Devices & Storage Corporation (Japan)

- Innoscience Technology (China)

- GaN Systems Inc. (Canada)

KEY INDUSTRY DEVELOPMENTS

- In December 2025, onsemi signed a collaboration agreement with GlobalFoundries to develop and manufacture next-generation GaN power devices using GF’s 200mm GaN-on-silicon process, starting with 650V. The move strengthens supply assurance and scale for high-performance GaN devices and integrated power stages targeting EV onboard chargers, DC-DC converters, and other automotive power blocks.

- In December 2025, Inovance Automotive and Innoscience announced their jointly developed 6.6 kW on-board charger, built on Innoscience’s 650V GaN technology, entered mass installation on Changan vehicles. The launch signals the real-volume deployment of GaN in onboard power units, emphasizing higher charging efficiency and power density compared to traditional silicon solutions.

- In October 2025, Infineon announced the production launch of its first 100V CoolGaN Automotive Transistor family and began supplying samples of a pre-production AEC-Q101-qualified range, including high-voltage CoolGaN automotive transistors and bidirectional switches. This expands automotive GaN readiness beyond low-voltage domains toward OBC and HV conversion roadmaps.

- In October 2025, STMicroelectronics introduced STDRIVEG210/STDRIVEG211 half-bridge GaN gate drivers designed to simplify robust GaN switching in low-voltage systems. The launch supports automotive migration toward higher-frequency, higher-efficiency conversion in 48–72V subsystems and auxiliary power electronics, helping designers reduce switching losses and improve transient response and integration.

- In April 2025, Navitas Semiconductor announced that its high-power GaNSafe ICs had achieved automotive qualification under both AEC-Q100 and AEC-Q101. By integrating control, drive, sensing, and protection, the devices target production EV power stages such as onboard chargers and HV-to-LV DC-DC converters, aiming to shorten design cycles and raise system robustness.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 30.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Device Type, By Vehicle Type, By Voltage Rating, By Application, and By Region |

|

By Device Type |

· GaN Power Transistors · GaN Power ICs · GaN Power Modules |

|

By Vehicle Type |

· Hatchback/Sedan · SUV · LCV · HCV |

|

By Voltage Rating |

· ≤200 V · 201–400 V · 401–650 V |

|

By Application |

· On-Board Chargers (OBCs) · DC-DC Converters · Auxiliary / Partial Traction Inverters · ADAS & Infotainment Power Supplies |

|

By Region |

· North America (By Device Type, By Vehicle Type, By Voltage Rating, By Application, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Device Type, By Vehicle Type, By Voltage Rating, By Application, and By Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific (By Device Type, By Vehicle Type, By Voltage Rating, By Application, and By Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Device Type, By Vehicle Type, By Voltage Rating, and By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 0.16 Billion in 2025 and is projected to reach USD 2.12 Billion by 2034.

In 2025, the market value in Asia Pacific stood at USD 0.10 billion.

The market is expected to grow at a CAGR of 30.6% during the forecast period from 2026 to 2034.

The GaN power transistors segment leads the market in terms of device type.

Faster, lighter EV charging hardware accelerates the pull of GaN devices.

Key market players in the market include Infineon Technologies AG, STMicroelectronics, NXP Semiconductors N.V., Texas Instruments Incorporated, and Renesas Electronics Corporation.

Asia Pacific accounted for the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us