Automotive Grade Silicon Carbide (SiC) Components Market Size, Share & Industry Analysis, By Component Type (SiC MOSFETs, SiC Diodes, and SiC Power Modules), By Vehicle Type (Passenger Cars and Commercial Vehicles), By Application (Traction Inverters, Onboard Chargers (OBCs), DC-DC Converters, and Auxiliary Power & Energy Management Systems), By Voltage Class (Less than 650V, 650V-1,200V, and Above 1,200V), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

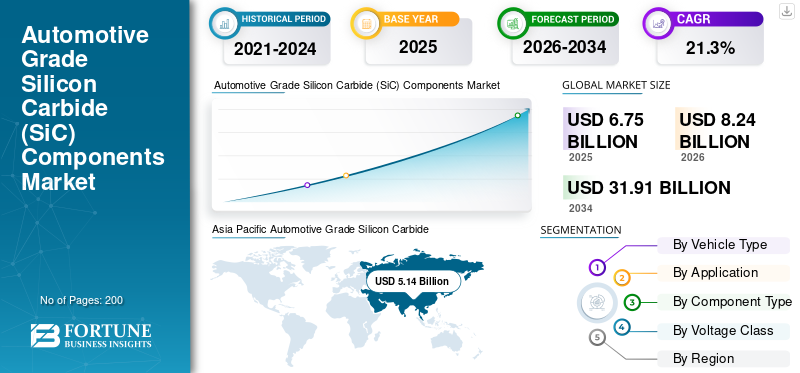

The global automotive grade silicon carbide (SiC) components market size was valued at USD 6.75 billion in 2025. The market is projected to grow from USD 8.24 billion in 2026 to USD 31.91 billion by 2034, exhibiting a CAGR of 21.3% during the forecast period. Asia Pacific dominated the global automotive grade silicon carbide (SiC) components market with a market share of 76.14% in 2025.

Automotive grade silicon carbide components are high-performance semiconductor devices used in vehicles to enable efficient power conversion, faster switching, higher temperatures, and improved range, reliability, and charging performance. Key market drivers include the rising electric vehicle adoption, demand for higher energy efficiency, faster charging, reduced power losses, stricter emission norms, and automakers shifting toward high-voltage, high-performance power electronics.

Major players in the market include Infineon Technologies, STMicroelectronics, Wolfspeed, onsemi, ROHM Semiconductor, and Mitsubishi Electric, competing through advanced SiC wafer technology, high-efficiency power devices, scalability, and automotive-grade reliability.

Download Free sample to learn more about this report.

Automotive Grade Silicon Carbide (SiC) Components Market Key Takeaways

- 2025 Market Size: USD 6.75 billion

- 2026 Market Size: USD 8.24 billion

- 2034 Forecast Market Size: USD 31.91 billion

- CAGR: 21.3% from 2026-2034

- Asia Pacific dominated the automotive grade silicon carbide (SiC) components market with a 76.14% share in 2025.

- The commercial vehicles segment is projected to register the fastest CAGR of 23.0% during the forecast period.

- The onboard chargers segment is projected to grow at a CAGR of 21.3% during the forecast period.

Asia Pacific

Asia Pacific is the largest and fastest-growing regional market, registering a CAGR of 22.3% during the forecast period.

Europe

Europe is the second-largest regional market due to strong EV adoption and stringent emission regulations.

North America

North America is growing steadily due to rising EV adoption and investments in domestic SiC manufacturing.

U.S.

The market is driven by accelerating EV adoption and investments in semiconductor manufacturing.

Japan

The market is supported by increasing EV production and silicon carbide technology adoption.

Read More

AUTOMOTIVE GRADE SILICON CARBIDE (SiC) COMPONENTS MARKET TRENDS

Vertical Integration and Capacity Expansion to Shape Market Evolution

A key market trend is semiconductor manufacturers pursuing vertical integration across SiC wafers, devices, and modules to secure supply chains and improve cost control. Leading players are investing in new fabs, long-term wafer sourcing, and in-house crystal growth. This trend enhances quality consistency, supports rising automotive volumes, and strengthens long-term partnerships with global OEMs and global silicon carbide.

- In May 2024, STMicroelectronics announced plans to build the world’s first fully integrated silicon carbide (SiC) manufacturing facility in Catania, Italy, creating a vertically integrated SiC campus for power devices, substrates, test, and packaging to support automotive and industrial electrification.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Electrification to Drive SiC Power Device Adoption

Accelerating widespread adoption of electric vehicle across passenger and commercial segments is driving the automotive grade silicon carbide (SiC) components market growth. Automakers increasingly adopt SiC MOSFETs and diodes to improve inverter efficiency, extend driving range, enable high voltage, and reduce thermal losses. Government incentives, emission regulations, and OEM investments in dedicated EV platforms further accelerate the large-scale integration of SiC power electronics into next-generation electric powertrains.

- In December 2025, China’s electric vehicle maker Leapmotor announced plans to boost the annual sales to more than 4 million units within the next decade, aiming for 1 million sales by 2026 and expanding globally with a Stellantis partnership and new premium models.

MARKET RESTRAINTS

High Manufacturing Costs to Restrain Market Expansion

Automotive grade silicon carbide components face cost-related restraints due to expensive substrates, complex crystal growth, lower wafer yields, and limited foundry capacity. Compared to traditional silicon devices, SiC requires specialized equipment and longer production cycles. These factors increase component prices, limiting adoption in entry-level vehicles and price-sensitive markets, especially where EV manufacturing costs competitiveness remains a critical purchasing consideration.

MARKET OPPORTUNITIES

Expansion of High-Voltage Architectures to Create New Growth Opportunities

The industry shift toward 800V and higher voltage EV architectures creates strong opportunities for SiC component suppliers. SiC devices perform efficiently at higher voltages and temperatures, enabling ultra-fast charging, lighter powertrains, and compact system designs. As premium EV features cascade into mass-market vehicles, the demand for scalable, automotive-grade SiC solutions is expected to broaden significantly.

- In June 2023, ZF unveiled its 800-volt electric drive system in the EVbeat concept car, integrating a high performance electric motor, inverter, and reduction gearbox. The system delivers higher efficiency, compact packaging, and improved torque density for next-generation electric vehicles.

MARKET CHALLENGES

Capital Intensive Investments in Capacity Expansion to Create Challenges for Market Expansion

Meeting rapidly rising automotive demand presents a major challenge for the silicon carbide market, as capacity expansion requires long lead times and capital-intensive investments. Any delays in wafer availability, yield optimization, or fab ramp-ups can disrupt OEM production plans. Balancing demand growth with reliable, automotive-grade supply remains critical for sustaining market confidence and long-term adoption.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

High EV Passenger Car Parc and Frequent Charging Requirements to Propel Passenger Cars Segment Dominance

Based on vehicle type, the market is segmented into passenger cars and commercial vehicles.

The passenger cars segment dominates the market due to the rapidly expanding global electric passenger vehicle parc and high charging frequency. The widespread urban adoption, home and public charging reliance, and growing ride-hailing EV fleets drive consistent demand for network operations, maintenance, software management, and uptime support. Government incentives, dense urban charging deployment, and OEM-backed charging ecosystems further sustain recurring service revenues and long-term contracts for passenger car-focused charging networks.

- According to the IEA, the global electric car sales exceeded 17 million in 2024, growing over 25%, with the additional 3.5 million vehicles sold in 2024 alone surpassing total the global electric car sales recorded in 2020.

The commercial vehicles segment is the fastest growing, registering a CAGR of 23.0% over the forecast period. The segmental growth is driven by fleet electrification, depot-based charging, uptime-critical operations, and rising demand for managed charging, predictive maintenance, and network optimization services across logistics, transit, and delivery fleets.

By Application

High Demand in Drivetrain Efficiency and Power Conversion to Drive Traction Inverters Segmental Demand

Based on application, the market is segmented into traction inverters, onboard chargers (OBCs), DC-DC converters, and auxiliary power & energy management systems.

The traction inverters segment dominates the market due to their critical role in power conversion and drivetrain efficiency. Rising EV production, increasing adoption of high-voltage architectures, and the shift toward SiC-based inverters drive continuous demand. Frequent software updates, thermal management support, thermal conductivity, diagnostics, and performance optimization services sustain recurring operational and support revenues across OEM and fleet-operated electric vehicles globally.

- In November 2025, Magnachip announced the expansion of its industrial IGBT business by leveraging advanced semiconductor traction inverter IGBT technology developed with Hyundai Mobis. The partnership aims to grow high-performance IGBT applications in EV traction, industrial, AI, and renewable energy systems market, with mass production slated for 2026.

The onboard chargers segment is the second-largest segment in the market and is poised to grow at a CAGR of 21.3% over the forecast period. The segment is driven by rising AC charging usage, residential installations, bidirectional charging adoption, and the need for ongoing firmware updates, maintenance, and compatibility support across diverse charging infrastructure.

To know how our report can help streamline your business, Speak to Analyst

By Component Type

Rising Adoption in Onboard Chargers and Traction Inverters to Boost SiC MOSFETs Segmental Expansion

By component type, the market is divided into SiC MOSFETs, SiC diodes, and SiC power modules.

The SiC MOSFETs segment dominates the market due to their widespread use in traction inverters, onboard chargers, and DC-DC converters. Automakers increasingly prefer SiC MOSFETs for their superior switching speed, lower power losses, and high-temperature performance. The growing EV penetration, transition to 800V platforms, and demand for improved driving range ensure sustained, large-scale adoption across passenger and commercial electric vehicles.

- In December 2025, Toshiba developed new 1200 V silicon carbide (SiC) MOSFETs for automotive traction inverters, offering improved efficiency and performance. These devices target next-generation electric vehicles, supporting higher power density and enhanced thermal reliability for EV powertrain systems.

The SiC power modules segment is the fastest-growing segment, expanding at a CAGR of 22.9% over the analysis period. The segment growth is driven by the OEM demand for compact, integrated solutions that simplify system design, improve thermal management, and support higher power densities, power semiconductor, in next-generation electric powertrains.

By Voltage Class

Shift toward High-Voltage EV Platforms and Fast-Charging Capability Augments 650V–1,200V Segment Growth

By voltage class, the market is categorized into less than 650V, 650V–1,200V, and above 1,200V.

The 650V–1,200V voltage segment dominates the market due to its strong alignment with modern EV powertrain requirements. This range is widely used in traction inverters, DC fast-charging systems, and high-power onboard chargers. The increasing adoption of 800V architectures, demand for faster charging, improved efficiency, and reduced system losses continue to drive the segment’s dominance and accelerated growth.

- In December 2025, Volkswagen unveiled a new electric model integrating XPeng’s 800V electrical architecture, enabling ultra-fast charging and a driving range of up to 425 miles. This highlights VW’s strategy to enhance EV performance, efficiency, and competitiveness through advanced Chinese-developed EV technologies.

The less than 650V segment holds the second-largest market share and is poised to depict a CAGR of 19.2% over the forecast period. The growth of the segment is supported by its continued use in auxiliary power electronics, low-power DC-DC converters, and legacy EV platforms, particularly in cost-sensitive and hybrid vehicle applications.

Automotive Grade Silicon Carbide (SiC) Components Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Grade Silicon Carbide (SiC) Components Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and is the fastest-growing market, registering a CAGR of 22.3% over the forecast period. The regional market is driven by strong EV production in China, Japan, and South Korea. Government subsidies, local semiconductor manufacturing investments, and the rapid adoption of high-voltage EV platforms accelerate demand. The presence of major SiC suppliers, expanding charging infrastructure, and aggressive electrification targets across passenger and commercial vehicles further reinforces regional leadership and sustained high-growth momentum.

- In 2024, over 6.4 million units of BEVs were sold in China, as per the IEA. The sales of EVs grew around 18.5%, as compared to 2023 sales, which were reported at around 5.4 million units.

Europe

Europe represents the second-largest automotive grade silicon carbide (SiC) components market share, supported by stringent emission regulations, strong EV penetration, and early adoption of 800V architectures. Leading OEMs increasingly integrate SiC components to enhance efficiency and fast-charging capability. Robust investments in battery-electric platforms, coupled with regional semiconductor capacity expansion and policy-driven electrification mandates, ensure steady demand growth across passenger cars, commercial vehicles, and public transport electrification initiatives.

- In September 2025, Volvo aimed to switch its upcoming EX90 electric SUV to an 800-volt electrical system, enabling faster charging, improved efficiency, and better high-power performance, aligning the model with next-generation EV architectures and premium market expectations.

North America

The market growth in North America is driven by rising EV adoption, increasing investments in domestic SiC manufacturing, and the electrification of pickup trucks and commercial fleets. OEMs focus on high-performance EVs and fast-charging capability supports SiC adoption in traction inverters and power modules. Government incentives, infrastructure funding, and the reshoring of semiconductor supply chains further strengthen long-term demand and technology adoption across the U.S. and Canada.

U.S. Automotive Grade Silicon Carbide (SiC) Components Market

The U.S. market is driven by accelerating electric vehicle adoption, strong federal incentives, and major investments in domestic semiconductor manufacturing. Automakers increasingly deploy SiC devices in high-performance EVs, pickup trucks, and commercial fleets to enable fast charging and improved efficiency.

- In February 2025, Texas Instruments announced plans to invest over USD 60 billion for foundational semiconductor manufacturing in the U.S., expanding long-term domestic capacity to support automotive, industrial, and electronics demand while strengthening supply chain resilience.

Rest of the World

The rest of the world market is gradually expanding, supported by emerging EV adoption in Latin America, the Middle East, and parts of Africa. Government pilot programs, improving charging infrastructure, and declining EV costs encourage initial demand for SiC-based power electronics. The growth remains moderate but is expected to accelerate as regional electrification policies mature and imports of high-voltage EV platforms increase.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus on Electrification, High-Voltage Architectures, and Supply Chain Integration to Gain Competitive Edge

The automotive grade silicon carbide components market is shaped by rapid EV electrification, high-voltage architectures, and the shift toward energy-efficient power electronics. Major players in the market include Infineon Technologies, STMicroelectronics, Wolfspeed, onsemi, ROHM Semiconductor, and Mitsubishi Electric compete through wafer capacity expansion, vertically integrated manufacturing, and automotive-grade reliability. Companies focus on SiC MOSFET innovation, power module integration, and long-term OEM supply agreements. Strategic fab investments, yield optimization, and partnerships with automakers help secure supply chains and strengthen competitive positioning globally.

- In October 2024, Wolfspeed launched 1200V silicon carbide six-pack power modules designed for e-mobility propulsion systems, delivering higher efficiency, increased power density, and improved thermal performance to support next-generation electric vehicle traction inverters and high-voltage architectures.

LIST OF KEY AUTOMOTIVE GRADE SILICON CARBIDE (SiC) COMPONENTS COMPANIES PROFILED

- Infineon Technologies AG (Germany)

- STMicroelectronics (Switzerland)

- Wolfspeed, Inc. (U.S.)

- onsemi (U.S.)

- ROHM Semiconductor (Japan)

- Mitsubishi Electric Corporation (Japan)

- Bosch Semiconductor (Germany)

- Renesas Electronics Corporation (Japan)

- Toshiba Electronic Devices & Storage (Japan)

- Fuji Electric Co., Ltd. (Japan)

- Littelfuse, Inc. (U.S.)

- Microchip Technology Inc. (U.S.)

- United Silicon Carbide (Qorvo) (U.S.)

- GeneSiC Semiconductor (U.S.)

- Semikron Danfoss (Germany)

KEY INDUSTRY DEVELOPMENTS

- In December 2025, Infineon achieved a milestone with 200 mm SiC technology, enhancing production scalability and enabling higher-volume manufacturing of SiC power devices for automotive and industrial applications.

- In September 2025, Wolfspeed commercially launched its 200 mm silicon carbide materials portfolio, unlocking industry-scale SiC production to support broader adoption in EV power electronics and high-efficiency systems.

- In May 2025, Nexperia launched automotive-qualified 1200 V SiC MOSFETs in D2PAK-7 packaging, with low RDS (on), enhanced thermal stability, and AEC-Q101 certification for EV traction inverters, onboard chargers, and DC-DC applications.

- In September 2024, STMicroelectronics unveiled a new generation of silicon carbide (SiC) power technology for EV traction inverters, offering smaller, efficient 750 V and 1200 V products to broaden SiC adoption in mid-size and compact electric vehicles.

- In September 2023, CDIL Semiconductors became the first Indian company to begin production of silicon carbide devices, aiming to address surging EV and power management demand domestically.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 21.3% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, By Application, By Component Type, By Voltage Class, and By Region |

|

By Vehicle Type |

· Passenger Cars · Commercial Vehicles |

|

By Application |

· Traction Inverters · Onboard Chargers (OBCs) · DC-DC Converters · Auxiliary Power & Energy Management Systems |

|

By Component Type |

· SiC MOSFETs · SiC Diodes · SiC Power Modules |

|

By Voltage Class |

· Less than 650V · 650V–1,200V · above 1,200V |

|

By Geography |

· North America ( By Vehicle Type, By Application, By Component Type, By Voltage Class, and By Country) o U.S. o Canada o Mexico · Europe (By Vehicle Type, By Application, By Component Type, By Voltage Class, and By Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type, By Application, By Component Type, By Voltage Class, and By Country) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World (By Vehicle Type, By Application, By Component Type, By Voltage Class) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.75 billion in 2025 and is projected to reach USD 31.91 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 5.14 billion.

The market is expected to exhibit a CAGR of 21.3% during the forecast period of 2026-2034.

The passenger cars segment leads the market in terms of vehicle type.

Rapid electrification is a key factor set to drive SiC power device adoption, propelling industry growth.

Infineon Technologies, STMicroelectronics, Wolfspeed, onsemi, ROHM Semiconductor, and Mitsubishi Electric are the leading companies in the market.

Asia Pacific holds the largest share in the market.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us