Automotive Graphics Display Controllers Market Size, Share & Industry Analysis, By Product Type (In-Vehicle Infotainment Display Controllers, Center Stack Display Controllers, Instrument Cluster Controllers, Head-Up Display (HUD) Controllers, and Rear Seat Entertainment Controllers), By Vehicle Type (Passenger Cars (Hatchback/Sedan and SUVs) and Commercial Vehicles), By Display Size (Up to 5 Inch, 5-10 Inch, and Above 10 Inch), By Sales Channel (OEM and Aftermarket), and Regional Forecasts, 2026-2034

Automotive Graphics Display Controllers Market Size and Future Outlook

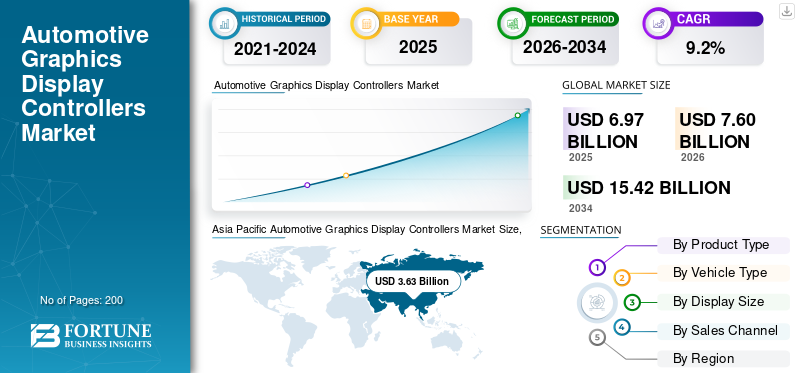

The global automotive graphics display controllers market size was valued at USD 6.97 billion in 2025. The market is projected to grow from USD 7.60 billion in 2026 to USD 15.42 billion by 2034, exhibiting a CAGR of 9.2% during the forecast period. Asia Pacific dominated the automotive graphics display controllers market with a market share of 52.08% in 2025.

The global market covers semiconductor controllers and graphics-processing components that manage visual output inside vehicles. These controllers support infotainment systems, digital clusters, center-stack screens, head-up displays, rear-seat entertainment, navigation visuals, camera feeds, and advanced driver assistance systems (ADAS). In simple terms, they help convert vehicle data into smooth, clear, and responsive graphics for the driver and passengers.

The market is growing as modern vehicles are shifting from mechanical interiors to software-defined digital cockpits. Automakers are adding larger displays, curved screens, multi-screen dashboards, augmented-reality HUDs, and connected user interfaces. This increases demand for high-performance display technologies and controller ICs that can handle faster graphics, better resolution, lower latency, and safer driver interaction.

The automotive graphics display controllers market is strongly linked with growth in passenger cars, SUVs, premium EVs, and connected commercial vehicles. As advanced driver assistance systems expand, visual alerts, camera views, lane guidance, parking assistance, and navigation overlays require stronger display-processing capability. This makes display controllers more important in both comfort and safety functions.

In the future, the market will evolve toward centralized cockpit computing, AI-based interfaces, and multi-domain processors that combine cockpit, infotainment, and ADAS functions. The market also benefits from rising screen adoption in Asia Pacific, North America, Europe, South Korea, and premium markets in South Africa and the Middle East.

Major key players such as Renesas Electronics Corporation, Texas Instruments Incorporated, and Robert Bosch are focusing on integrated cockpit platforms, higher-resolution graphics, and scalable controller architectures to support evolving vehicle digitalization requirements.

Download Free sample to learn more about this report.

AUTOMOTIVE GRAPHICS DISPLAY CONTROLLERS MARKET TRENDS

Growing Adoption of Larger and Curved Displays to Boost Market Growth

A major trend influencing the market is the growing adoption of larger, curved, and pillar-to-pillar cockpit displays in modern vehicles. These screens improve user experience and support the development of the digital interior. However, they also require stronger graphics processing capabilities and display control technologies. The trend supports demand for high-resolution controllers, multi-display synchronization, and advanced cockpit SoCs. Adoption is especially strong in SUVs, luxury cars, and EV platforms across Asia Pacific, Europe, and North America.

- For instance, in 2024, Continental AG, in its Mobility Study, highlighted its Curved Ultrawide Display, featuring a cockpit-wide display interface with hidden control elements to reduce driver distraction.

Market Dynamics

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Digital Cockpit Adoption Drives Demand for the Product

Growing adoption of digital cockpits is a major driver for the automotive graphics display controllers market growth. Automakers are replacing analog dashboards with digital clusters, large center displays, connected infotainment, and ADAS visualization. These systems require controllers that can manage high-resolution graphics, fast response, and multiple displays. As passenger cars, SUVs, and premium EVs add more screens, controller value per vehicle increases, supporting strong market growth.

- For instance, in January 2024, Qualcomm’s CES press kit highlighted Snapdragon Digital Chassis, cockpit AI, and software-defined vehicle solutions for next-generation in-car experiences.

MARKET RESTRAINTS

Centralized Vehicle Computing May Reduce Standalone Controller Demand

A key restraint affecting the market is the shift toward centralized compute architectures. In older cockpit designs, separate controllers were used to manage individual screens and functions. However, in newer vehicles, a single high-powerful SoC can support infotainment, cluster, ADAS views, and multiple displays. With this architecture, system efficiency improves, which may reduce the number of discrete display controller units per vehicle. As a result, unit volume growth for standalone display controllers could moderate, even as screen content complexity and display quality continue to improve.

- For instance, in January 2024, Bosch and Qualcomm introduced a centralized single-SoC platform capable of supporting both cockpit and ADAS functionalities with a unified vehicle computing system.

MARKET OPPORTUNITIES

Augmented-Reality HUDs to Create Premium Growth Opportunities

Augmented-reality HUDs create a strong opportunity for the graphics display controller market as they need advanced rendering, precise image placement, and real-time driver information. These systems display navigation, speed, warnings, and advanced driver assistance systems data directly within the driver’s field of vision, enhancing both convenience and driving safety. As premium vehicles and EVs adopt windshield-wide displays, controller ASPs are expected to increase, especially in Europe, North America, and Asia Pacific.

- For instance, in January 2025, BMW introduced Panoramic iDrive with an optional 3D Head-Up Display showing navigation and automated-driving information in the driver’s view.

MARKET CHALLENGES

Rising Software Complexity to Hinder Market Development

The market faces rising challenges associated with increasing software complexity and stringent safety requirements. Display controllers now handle safety-relevant information, ADAS alerts, camera views, and driver warning systems. As a result, any system delay, display distortion, or processing failure can negatively affect user trust and vehicle safety. Therefore, suppliers must meet automotive-grade reliability, cybersecurity, functional safety, and long validation cycles, increasing development cost and slowing adoption among smaller OEMs.

- For instance, in December 2025, Renesas expanded its R-Car Gen 5 platform around multi-domain SoCs for SDV, ADAS, infotainment, and gateway applications.

Automotive Graphics Display Controllers Market Segmentation Analysis

By Product Type

In-Vehicle Infotainment Display Controllers Dominate Due to Their Growing Usage in Vehicles

On the basis of product type, the market is segmented into in-vehicle infotainment display controllers, center stack display controllers, instrument cluster controllers, Head-Up Display (HUD) controllers, and rear seat entertainment controllers.

In-vehicle infotainment display controllers dominate this market as infotainment screens are now common across entry, mid-range, and premium vehicles. These controllers support navigation, smartphone connectivity, media, vehicle settings, voice assistants, and connected services. Their high penetration across passenger cars and commercial vehicles makes them the largest product category, while rising screen size and software-defined cockpit features continue to lift product demand.

- For instance, in January 2024, HARMAN expanded its Ready product portfolio with Samsung synergies to improve connected, automotive-grade in-cabin experiences.

The Head-Up Display (HUD) controllers segment is expected to grow at a CAGR of 12.8% over the forecast period.

By Vehicle Type

Passenger Cars Segment Dominates Owing to Its High Global Production

On the basis of vehicle type, the market is segmented into passenger cars (hatchback/sedan and SUVs) and commercial vehicles.

The passenger cars segment dominates the global market, accounting for the majority of global vehicle production while increasingly adopting advanced cockpit electronics, connected infotainment systems, and advanced driver assistance systems. Within passenger cars, SUVs represent the leading sub-segment due to their higher integration of large displays, digital clusters, HUDs, and premium infotainment packages. Compared with hatchbacks and sedans, SUVs carry higher electronics value and larger cockpit screens, making them the most valuable contributor to display controller demand.

- For instance, in September 2025, BMW debuted its 2026 iX3 SUV featuring a 43-inch Panoramic iDrive windshield display and a 17.9-inch infotainment screen.

The commercial vehicle segment is expected to grow at a CAGR of 8.1% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Display Size

5-10 Inch Segment Dominates due to its Widespread Usage in Mass-Market Infotainment Screens

On the basis of display size, the market is segmented into up to 5 Inch, 5-10 Inch, and above 10 Inch.

The 5-10 inch display size dominates as it is widely used in mass-market infotainment screens, center stacks, and digital clusters. This display range offers an effective balance between cost efficiency, screen visibility, packaging flexibility, and functional performance, making it suitable for compact cars, sedans, SUVs, and fleet vehicles. While above-10-inch displays are growing faster, 5-10-inch screens remain the largest installed base across global vehicle production.

- For instance, in January 2024, TI introduced new automotive chips at CES to support smarter and safer vehicles, strengthening electronics used around modern cockpit systems.

The above 10 Inch segment is expected to grow at a CAGR of 12.2% over the forecast period.

By Sales Channel

Rising Integration of ADAS Screen in Vehicles Boosted OEM Segment Growth

On the basis of sales channel, the market is segmented into OEM and aftermarket.

The OEM segment captured the major automotive graphics display controllers market share, as graphics display controllers are integrated into vehicle electronics platforms during vehicle development. Automakers select controllers based on display architecture, safety requirements, software compatibility, and long-term supply needs. Infotainment systems, clusters, HUDs, and ADAS displays are mostly factory-installed, which significantly strengthens OEM demand. In comparison, aftermarket demand remains relatively limited and is primarily associated with replacement units, retrofits, and infotainment upgrades.

- For instance, in January 2024, Bosch and Qualcomm demonstrated their cockpit-ADAS integration platform, showing how OEMs can use centralized electronics for factory-built digital cockpit architectures.

The aftermarket segment is expected to grow at a CAGR of 9.7% over the forecast period.

Automotive Graphics Display Controllers Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Automotive Graphics Display Controllers Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share, reaching USD 3.63 billion in 2025 and also maintained its leading share in 2024 with USD 3.30 billion. The growth is attributed to large vehicle production, rapid EV adoption, and strong digital cockpit demand in China, Japan, India, and South Korea. China’s high-volume new energy vehicle market drives large displays and connected cockpit adoption, while Japan and South Korea support advanced electronics and supplier ecosystems. India is also contributing to regional market expansion as digital infotainment systems and connected displays become increasingly common across affordable and mid-range passenger vehicle models.

- For instance, in January 2025, China’s auto production reached 31.282 million units in 2024, while NEV sales exceeded 10 million units and crossed 40% share.

China Automotive Graphics Display Controllers Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues standing at around USD 2.21 billion, representing roughly 31.7% of global sales.

India Automotive Graphics Display Controllers Market

The Indian market in 2025 stood at around USD 0.37 billion, accounting for roughly 5.3% of global revenues.

North America Automotive Graphics Display Controllers Market

North America is estimated to reach USD 1.58 billion in 2026 and secure the position of the second-largest region in the market. North America will remain a high-value region because the U.S. has strong SUV, pickup, premium vehicle, and connected infotainment demand. The U.S. market favors large center displays, ADAS visualization, and subscription-ready cockpit software. Canada and Mexico support production-linked demand, while Mexico is important for OEM manufacturing and electronics integration.

U.S. Automotive Graphics Display Controllers Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market stood at around USD 0.94 billion in 2025, representing roughly 20.9% of global sales.

Europe

Europe is projected to record a growth rate of 7.9% in the coming years. The market is expected to reach a valuation of USD 1.29 billion by 2026. Europe will grow steadily as premium OEMs expand digital clusters, HUDs, and cockpit-wide displays. Germany, France, the U.K., Italy, and Spain support demand through premium brands, safety regulations, and connected vehicle platforms. Growth is also supported by EV launches and software-defined vehicle programs, although high vehicle costs and slower replacement cycles may limit product adoption.

Germany Automotive Graphics Display Controllers Market

Germany’s market in 2025 stood at around USD 0.46 billion, accounting for roughly 6.6% of global revenues.

U.K. Automotive Graphics Display Controllers Market

The U.K.’s market in 2025 stood at around USD 0.14 billion, accounting for roughly 2.4% of global revenues.

Latin America

Latin America is expected to witness moderate growth, led primarily by Brazil and Argentina. Demand is being supported by rising infotainment penetration in locally produced vehicles and the gradual adoption of digital instrument clusters in higher trims. However, factors such as price-sensitive consumers, slower premium vehicle adoption, and limited local semiconductor ecosystems continue to restrict the region’s overall market share compared with Asia Pacific, Europe, and North America.

Middle East & Africa

The Middle East & Africa will grow at a smaller base during the forecast period. Demand in the UAE is supported by strong sales of premium imported vehicles equipped with large displays and advanced infotainment. South Africa contributes through local vehicle assembly and demand from the commercial vehicle fleet. Although growth across many regional markets remains gradual due to price-sensitive consumers, premium SUVs, and connected vehicle adoption support value expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Compete on Chip Performance to Gain Competitive Edge

The competitive landscape of the global automotive graphics display controller market is shaped by semiconductor companies, automotive electronics suppliers, display technology firms, and cockpit platform developers. Competition is moving beyond standalone display controllers toward integrated cockpit SoCs platforms, multi-display processors, domain controllers, and software-defined vehicle platforms to support next-generation connected and intelligent vehicle ecosystems.

Leading companies are investing in high-performance graphics, functional safety, AI acceleration, low-power designs, and scalable architectures. Renesas Electronics Corporation, Qualcomm Technologies Inc., NVIDIA Corporation, and NXP Semiconductors compete on chip performance, automotive-grade reliability, software ecosystem, and support for infotainment, cluster, HUD, and ADAS visualization. Tier-1 suppliers such as Bosch, Continental, Denso, Panasonic Automotive, Visteon, Harman, and Hyundai Mobis focus on complete cockpit systems that combine screens, processors, sensors, and software.

Strategic partnerships are becoming important as automakers seek to reduce the number of ECUs, lower development complexity, and more flexible vehicle platform architectures. Semiconductor firms are therefore collaborating with Tier-1 suppliers and software companies to offer ready-to-integrate cockpit solutions. These partnerships help OEMs reduce time-to-market and develop common platforms across multiple vehicle type categories.

Display technology specialists such as LG Display, Samsung Display, BOE Technology Group, and AUO Corporation are playing an increasingly influential role in shaping market competition through the development of larger, thinner, curved, OLED, and transparent automotive displays. These technologies increase the graphics-processing requirements of automotive controllers and strengthen demand for advanced display solutions.

- For instance, in January 2024, Qualcomm and Bosch showcased a central vehicle computer allowing digital cockpit and ADAS functions to operate on one Snapdragon Ride Flex SoC.

LIST OF KEY AUTOMOTIVE GRAPHICS DISPLAY CONTROLLERS COMPANIES PROFILED

- Renesas Electronics Corporation (Japan)

- Texas Instruments Incorporated (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- NVIDIA Corporation (U.S.)

- NXP Semiconductors N.V. (Netherlands)

- STMicroelectronics N.V. (Switzerland)

- Infineon Technologies AG (Germany)

- Analog Devices, Inc. (U.S.)

- ROHM Semiconductor (Japan)

- Socionext Inc. (Japan)

- MediaTek Inc. (Taiwan)

- Samsung Electronics Co., Ltd. (South Korea)

- Continental AG (Germany)

- Robert Bosch GmbH (Germany)

- Denso Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Hyundai Mobis formed a Quad Alliance with ZEISS, SCHOTT, and other partners to develop and mass-produce holographic windshield displays for vehicles. This technology enables full-windshield projection of driving data, navigation, and infotainment content, transforming the entire glass surface into an interactive display and supporting next-generation immersive cockpit environments.

- January 2026: Visteon and Mahindra expanded their collaboration to integrate SmartCore Pro digital cockpit technology into Mahindra’s upcoming XUV7X0 SUV platform. The system consolidates infotainment, instrument cluster, telematics, and surround-view processing into a centralized architecture, improving performance, scalability, and software-defined vehicle capabilities for next-generation passenger vehicles.

- November 2025: HARMAN achieved the first HDR10+ Automotive certification for its Ready Display product. The certification improves in-car visual quality through adaptive brightness and color adjustment.

- October 2025: NXP launched the i.MX 952 applications processor for automotive HMI, AI vision, and in-cabin perception. The processor supports smarter cockpit interfaces and sensor-fusion-based interior functions.

- September 2025: Visteon and FUTURUS partnered to co-develop next-generation HUD systems for global automakers. The collaboration targets advanced head-up display and augmented-reality cockpit applications.

- September 2025: AUMOVIO unveiled a compact 3D head-up display using mirrorless AR-HUD technology. The design reduces installation space by up to 50% versus conventional HUDs.

- September 2025: Hyundai Mobis showcased its Holographic Windshield Display on the Kia EV9 at IAA Mobility 2025. The technology turns the windshield into a screen for navigation, driving data, and media UI.

REPORT COVERAGE

The global automotive graphics display controllers market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 9.2% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Vehicle Type, Display Size, Sales Channel, and Region |

| By Product Type |

|

| By Vehicle Type |

|

| By Display Size |

|

| By Sales Channel |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 6.97 billion in 2025 and is projected to reach USD 15.42 billion by 2034.

In 2025, the market value stood at USD 3.63 billion.

The market is expected to exhibit a CAGR of 9.2% during the forecast period.

The passenger cars segment leads the market by vehicle type.

Rising digital cockpit adoption is the key factor driving the market.

Renesas Electronics Corporation, Texas Instruments Incorporated, Robert Bosch, and Continental AG are some of the top players in the market.

Asia Pacific dominated the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us