Automotive Logging Devices Market Size, Share & Industry Analysis, By Connectivity Type (Cellular (4G/5G LTE), Satellite, and Bluetooth / Short-range), By Vehicle Type (Passenger Cars, LCVs, and HCVs), By Sales Channel (OEM and Aftermarket), By Application (Compliance, Safety, Fleet Management, Insurance, and Maintenance), and Regional Forecast, 2026-2034

Automotive Logging Devices Market Size and Future Outlook

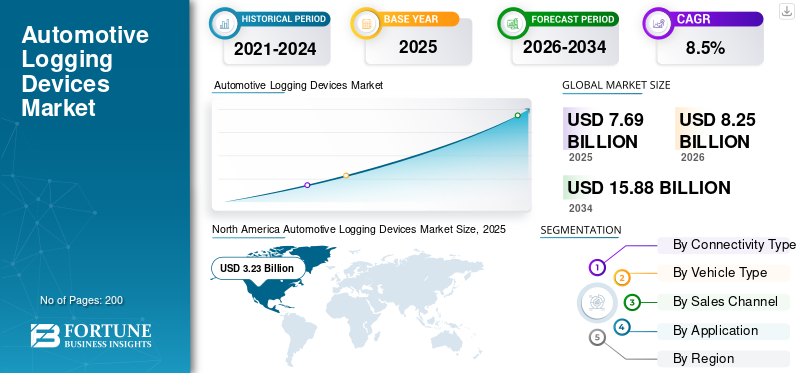

The automotive logging devices market size was valued at USD 7.69 billion in 2025. The market is projected to grow from USD 8.25 billion in 2026 to USD 15.88 billion by 2034, with a CAGR of 8.5% over the forecast period. North America dominated the automotive logging devices market with a market share of 42.% in 2025.

Automotive logging devices are electronic systems installed in vehicles to automatically record driving activity, engine data, vehicle movement, and compliance information. They connect to the engine control module or onboard remote diagnostics port and transmit data through cellular, satellite, or paired connectivity for regulatory reporting, fleet management, safety monitoring, and operational optimization. The market is primarily driven by regulatory mandates such as Electronic Logging Device (ELD) and tachograph requirements, increasing fleet digitization, and the need for real-time operational visibility. Rapid growth in e-commerce logistics, rising focus on fuel efficiency, and the expansion of telematics-based insurance also accelerate product adoption. Additionally, demand for predictive maintenance and upgrades to 4G/5G connectivity is boosting device replacement and subscription-based revenue growth globally. Key players in the market include Geotab Inc., Samsara Inc., Trimble Inc., Verizon Connect, Continental AG (VDO), Motive, EROAD Ltd., and Powerfleet. The market trend is shifting toward integrated hardware and SaaS models, AI-driven analytics, and OEM-embedded telematics systems. Vendors are expanding globally, enhancing 5G connectivity, and bundling compliance, safety, and fleet optimization solutions to increase recurring subscription revenue.

Download Free sample to learn more about this report.

Automotive Logging Devices Market KEY TAKEAWAYS

- 2025 Market Size: USD 7.69 billion

- 2026 Market Size: USD 8.25 billion

- 2034 Forecast Market Size: USD 15.88 billion

- CAGR: 8.5% from 2026–2034

- North America dominated the automotive logging devices market with a 42.0% share in 2025.

- The satellite segment is projected to grow at a CAGR of 10.4% during the forecast period.

- The HCV segment is projected to grow at a CAGR of 9.1% during the forecast period.

Asia Pacific

Fastest-growing region, driven by expanding fleet digitization and rising logistics demand.

North America

Projected to lead the market in 2026, supported by strict ELD regulations and high telematics adoption.

Europe

Projected to reach USD 2.29 billion in 2026, driven by smart tachograph upgrades and freight compliance.

U.S.

Projected to reach USD 2.15 billion in 2026, fueled by ELD mandates and advanced fleet management solutions.

Japan

Projected to reach USD 0.18 billion in 2026, supported by connected vehicle technologies and regulatory compliance.

Read More

AUTOMOTIVE LOGGING DEVICES MARKET TRENDS

Expanding Regulatory Digitization Accelerates Compliance-Driven Adoption

Governments worldwide are strengthening digital compliance frameworks for commercial transport, increasing adoption of automotive logging devices. Mandatory electronic recording of driving hours, harmonization of cross-border enforcement, and stricter audit trails are pushing fleets to transition from manual logs to certified electronic systems. This regulatory digitization not only increases first-time installations but also creates structured upgrade cycles as standards evolve. As enforcement mechanisms become more technology-centric, fleets are compelled to adopt tamper-resistant, connected devices capable of real-time reporting.

- In August 2023, the European Union mandated the installation of Smart Tachograph Version 2 in newly registered heavy vehicles under the Mobility Package, reinforcing digital monitoring requirements across member states.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rapid Expansion of E-Commerce Logistics Drives Increasing Device Adoption

The sustained expansion of e-commerce and last-mile delivery networks is increasing the number of connected light and heavy commercial vehicles requiring operational visibility, thus driving automotive logging devices market growth. Logistics operators rely on logging devices to monitor route efficiency, fuel usage, driver behavior, and vehicle uptime in high-turnover delivery cycles. As fleets scale, centralized data platforms become essential for optimizing dispatch and decreasing downtime, thereby accelerating hardware-plus-subscription deployments. Growing cross-border freight volumes further reinforce the need for compliance and fleet analytics.

- In April 2024, the U.S. Census Bureau reported continued growth in e-commerce sales, highlighting structural expansion in delivery activity that supports telematics adoption.

MARKET RESTRAINTS

High Upfront Costs and Integration Complexity Constrain Market Growth

Upfront hardware investment, installation expenses, and recurring subscription fees can be significant barriers for small and independent fleet operators. Integration with legacy vehicle systems, data migration challenges, and driver training requirements further complicate adoption. In developing regions, inconsistent enforcement reduces urgency, making cost sensitivity even more noticeable. While large fleets benefit from economies of scale, fragmented operators often delay upgrades until compliance deadlines force them to act. Additionally, connectivity reliability issues in rural areas can limit perceived value, restraining faster penetration across cost-sensitive markets.

MARKET OPPORTUNITIES

Transition Toward AI-Enabled Predictive Fleet Ecosystems Creates Growth Potential

Advancements in artificial intelligence and edge computing are transforming logging devices into intelligent fleet management platforms. Beyond compliance, devices now support predictive maintenance, driver risk scoring, fuel optimization, and insurance analytics. As 5G networks expand, higher data throughput enables real-time video telematics and advanced safety integration, opening new revenue streams. OEM-embedded telematics modules further create opportunities for factory-installed logging solutions.

- In September 2025, Geotab Inc. announced surpassing 5 million connected vehicle subscriptions globally, underscoring expanding demand for data-driven fleet intelligence platforms.

MARKET CHALLENGES

Data Security and Cybersecurity Risks Present Operational Challenges

As logging devices transmit sensitive vehicle and driver data over cellular networks, cybersecurity risks and data privacy concerns are intensifying. Fleet operators must ensure encrypted communication, secure firmware updates, and compliance with regional data protection regulations. Any breach can disrupt fleet operations, damage reputation, and lead to regulatory penalties. Growing reliance on cloud platforms increases exposure to cyber threats, underscoring the need for a robust security architecture.

- In May 2024, the U.S. Cybersecurity and Infrastructure Security Agency (CISA) issued guidance highlighting cybersecurity risks in connected vehicle and telematics ecosystems, reinforcing the importance of secure deployment frameworks.

Segmentation Analysis

By Connectivity Type

Widespread 4G/5G Network Coverage Strengthens Cellular Connectivity Leadership.

Based on connectivity type, the market is segmented into cellular (4G/5G LTE), satellite, and Bluetooth/short-range (paired systems).

Cellular connectivity holds highest automotive logging devices market share due to extensive global mobile network coverage, lower hardware costs compared to satellite systems, and seamless integration with cloud-based fleet platforms. Real-time compliance reporting, over-the-air updates, and scalable subscription models further reinforce its leadership. Expanding 5G deployment enhances low-latency data transfer for advanced analytics and video telematics.

The satellite segment is projected to grow at a 10.4% CAGR over the forecast period.

By Vehicle Type

Expanding Fleet-Based Mobility Services Reinforce Passenger Car Segment Dominance

Based on vehicle type, the market is segmented into passenger cars, LCVs, and HCVs.

Passenger cars dominate primarily due to large fleet-operated vehicle volumes in ride-hailing, entry level cars rental, and corporate mobility services. These fleets increasingly deploy logging devices for insurance telematics, driver behavior monitoring, and operational efficiency. Although compliance mandates are stronger for heavy vehicles, the overall numerical strength of the passenger fleet supports higher installed volumes.

- In February 2024, Uber reported over 7 million active drivers globally, highlighting the scale of the fleet of passenger electric vehicles supporting telematics demand.

The HCV segment is projected to grow at a 9.1% CAGR over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Sales Channel

Increasing OEM Telematics Integration Strengthens Factory-Fitted Channel Leadership

Based on sales channel, the market is segmented into OEM and aftermarket.

OEM dominates as automakers increasingly form factor integrate factory-fitted telematics units and digital compliance systems directly into new vehicles. Embedded systems provide better data integration, warranty alignment, cybersecurity management, and lifecycle service contracts, encouraging fleet buyers to prefer OEM-installed solutions. This shift supports recurring revenue through bundled connectivity service type.

- In January 2024, General Motors announced the expansion of its embedded OnStar connectivity services across commercial vehicle platforms, reinforcing OEM-driven telematics integration.

The aftermarket segment is projected to grow at a CAGR of 8.6% over the forecast period.

By Application

Strengthening Regulatory Enforcement Sustains Compliance Application Leadership

Based on application, the market is segmented into compliance, safety, fleet management, insurance, and maintenance.

Compliance remains dominant as electronic logging mandates and tachograph regulations require certified digital recording of driving hours and vehicle activity. Regulatory audits and cross-border freight monitoring sustain continuous demand, particularly in North America and Europe. Compliance-driven installations also create recurring replacement cycles and subscription renewals.

- In December 2024, the European Commission enforced Smart Tachograph retrofit deadlines for cross-border heavy vehicles, reinforcing compliance-led demand.

The fleet management segment is projected to grow at a 9.5% CAGR over the forecast period.

AUTOMOTIVE LOGGING DEVICES MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America Automotive Logging Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America is expected to lead with a share of 41.4% in 2026, in the global market due to strict regulatory enforcement, mature fleet digitization, and high telematics penetration across commercial vehicles. The U.S. ELD mandate has institutionalized electronic logging across interstate carriers, creating a stable installed base and recurring replacement demand. Strong presence of leading vendors, high subscription adoption, and integration of safety and analytics modules further support revenue dominance. This growth remains steady, driven by software upgrades, the expansion of 5G-enabled connectivity, and the integration of AI-based fleet optimization tools across logistics and freight transportation networks.

U.S. Automotive Logging Devices Market

The U.S. market is driven by the Federal Motor Carrier Safety Administration’s ELD mandate, which requires electronic logging for Hours of Service compliance. High freight volumes, large heavy-truck fleets, and widespread SaaS adoption reinforce steady demand. Replacement cycles, cybersecurity upgrades, and advanced fleet analytics integration sustain recurring revenue growth in both OEM and aftermarket channels. The market will be valued at USD 2.15 billion in 2026.

Europe

Europe demonstrates strong, stable growth, reaching a value of USD 2.16 billion in 2025 and expected to reach at USD 2.29 billion by 2026, supported by tachograph regulations and cross-border freight compliance requirements. The transition to Smart Tachograph Version 2 and retrofit deadlines across member states have created structured upgrade demand. Europe benefits from established commercial transport corridors, advanced regulatory enforcement, and the increasing integration of telematics with emission-monitoring and safety systems. While relatively mature compared to Asia Pacific, steady modernization of fleet infrastructure and expansion of digital compliance for light commercial vehicles continue to drive incremental revenue growth.

U.K. Automotive Logging Devices Market

The U.K. market is shaped by tachograph compliance for commercial vehicles and strong logistics activity supporting domestic and cross-border freight. Post-Brexit regulatory alignment with EU transport standards continues to sustain digital logging adoption. Fleet modernization initiatives, rising e-commerce delivery volumes, and increasing deployment of integrated safety and telematics solutions support the market growth. The market is expected to value at USD 0.25 billion by 2026.

Germany Automotive Logging Devices Market

Germany is a major European logistics hub, with a high commercial vehicle density and strong enforcement of digital tachographs. The market is expected to grow with a CAGR of 7.6% over the forecast period. The country’s advanced automotive ecosystem supports OEM-installed telematics integration. Demand is further reinforced by export-driven freight movement and the modernization of fleet management infrastructure across industrial transport networks.

Asia Pacific

Asia pacific market is the fastest-growing, exhibiting a CAGR of 11.4% over the forecast period, driven by expanding regulatory frameworks, rising logistics demand, and accelerating fleet digitization across emerging economies. Large commercial vehicle populations and increasing enforcement of vehicle tracking standards are propelling adoption. Rapid urbanization, growth in cross-border trade, and rising 4G/5G penetration further stimulate device deployment. Compared to mature Western markets, the Asia Pacific offers significant first-time adoption potential, resulting in higher CAGR throughout the forecast period.

China Automotive Logging Devices Market

China’s market is expected to grow with a CAGR 10.7% during the forecast period, supported by extensive freight activity, strong government oversight of transport monitoring, and rapid expansion of digital infrastructure. Large-scale logistics networks and increasing focus on safety and operational transparency are boosting telematics adoption. The integration of connected vehicle platforms with logistics management systems increases demand for advanced logging devices.

Japan Automotive Logging Devices Market

Japan maintains steady growth, expected to reach a value of USD 0.18 billion by 2026, driven by advanced fleet management practices and regulatory compliance requirements for commercial transport. High technological readiness and widespread connected vehicle integration support OEM-driven deployments. Aging driver demographics also encourage the adoption of digital monitoring systems for safety and operational efficiency.

India Automotive Logging Devices Market

India is witnessing rapid adoption, predicted to have a share of 20.7% in 2026, driven by AIS-140 vehicle-tracking requirements and the expanding logistics and e-commerce sectors. Growing enforcement of transport digitization policies and increasing fleet formalization are accelerating the installation of logging devices. Cost-effective cellular-based solutions dominate, supporting scalable adoption across large commercial vehicle populations.

Rest of the World

The Rest of the World region shows moderate but improving growth, supported by gradual regulatory reforms and growing awareness of the benefits of fleet optimization. Adoption is uneven across Latin America, the Middle East & Africa market, largely influenced by enforcement intensity and infrastructure readiness. Rising cross-border trade, modernization of public transport fleets, and growing telematics penetration in oil & gas and mining logistics contribute to steady expansion. However, the overall share remains lower than in other regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Compliance-Driven Innovation, SaaS Integration, and Strategic Partnerships Shape Automotive Logging Devices Competition

The global automotive logging devices market trends are characterized by regulatory-driven demand, rapid evolution of SaaS platforms, and increasing integration of AI-enabled fleet intelligence. Leading players such as Geotab Inc., Samsara Inc., Trimble Inc., Motive, Verizon Connect, Continental AG (VDO), EROAD Ltd., and Powerfleet compete through certified compliance solutions, scalable cloud platforms, advanced driver analytics, and multi-network connectivity capabilities. Companies differentiate themselves by bundling hardware with subscription-based fleet management, safety monitoring, and predictive maintenance services to boost recurring revenue. Competitive intensity is further shaped by OEM telematics integration, 5G upgrades, and cybersecurity-focused device architectures. Vendors are expanding globally through strategic alliances with telecom operators, semiconductor providers, and enterprise software firms to improve real-time data collections processing and support cross-border compliance.

LIST OF KEY AUTOMOTIVE LOGGING DEVICES COMPANIES PROFILED

- Geotab Inc. (Canada)

- Samsara Inc. (U.S.)

- Trimble Inc. (U.S.)

- Omnitracs LLC (U.S.)

- Verizon Connect (U.S.)

- Teletrac Navman (U.S.)

- Continental AG (VDO) (Germany)

- Garmin Ltd. (Switzerland)

- Zonar Systems, Inc. (U.S.)

- TomTom Telematics (Netherlands)

- EROAD Ltd. (New Zealand)

- MiX Telematics Ltd. (South Africa)

- Inseego Corp. (U.S.)

- Intangles Lab Pvt. Ltd. (India)

- Fleet Complete (Canada)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Daimler Truck North America (DTNA) announced a strategic partnership with Class 8 to help Freightliner owner-operators and small fleets improve compliance and planning through connected services. The rollout targets newer Cascadia models first, signaling an OEM ecosystem expansion in which third-party compliance/logging tools integrate into factory-connected truck programs.

- February 2026: FMCSA’s ELD program updates confirmed Forward Thinking Systems’ Field Warrior ELD (BYOD) as usable for recording and transferring hours-of-service data, reflecting ongoing regulatory oversight of compliant logging solutions. Such official list updates can directly influence purchasing decisions for fleets that must use registered devices for audits and enforcement.

- February 2026: Geotab Inc. introduced the GO Anywhere asset-tracking family, including a tracker that blends cellular and satellite connectivity to maintain visibility in coverage dead zones. The product expansion highlights how logging-device ecosystems are extending into trailers, equipment, and mixed-fleet assets to reduce downtime and losses.

- January 2026: Motive launched AI Dashcam Plus, upgrading edge compute (processor/AI capacity), stereo vision, and hands-free communications in a unified in-cab device. While safety-focused, the launch matters for logging ecosystems as fleets increasingly bundle video, driver events, and compliance records into a single, connected hardware stack.

- November 2025: Motive and GEICO announced a partnership to improve commercial fleet safety and offer potential insurance savings to policyholders who use Motive AI Dashcams and telematics. The collaboration highlights how insurance programs are increasingly tied to logged driving events and risk signals, boosting the adoption of connected logging and safety hardware.

REPORT COVERAGE

The automotive logging devices market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on market research dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, strategic partnerships, mergers & acquisitions. The market forecast provides a comprehensive competitive landscape, including the most significant global market share, emerging opportunities, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.5% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Connectivity Type, By Vehicle Type, By Sales Channel, By Application, and By Region |

| By Connectivity Type |

|

| By Vehicle Type |

|

| By Sales Channel |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.69 billion in 2025 and is projected to reach USD 15.88 billion by 2034.

In 2025, the Europe market value stood at USD 2.16 billion.

The market is expected to grow at a CAGR of 8.5% from 2026 to 2034.

The aftermarket segment led the market in the sales channel segment.

Regulatory mandates such as ELD and tachograph requirements, increasing fleet digitization, and the need for real-time operational visibility are driving market momentum.

Key market players include Geotab Inc., Samsara Inc., Trimble Inc., Verizon Connect, Continental AG (VDO), Motive, and EROAD Ltd.

North America accounted for the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us