Automotive Prognostics Market Size, Share & Industry Analysis, By Offering (Hardware and Software), By Vehicle Type (Hatchback/Sedan, SUV, Light Duty Vehicle, and Heavy Duty Vehicle), By Application (Powertrain Prognostics, Battery Management, Braking System Prognostics, Steering and Suspension Prognostics, and Others), By Propulsion (ICE, HEV, and EV), By Deployment Type (On-Board Deployment and Cloud-Based Deployment), and Regional Forecast, 2026-2034

Automotive Prognostics Market Size

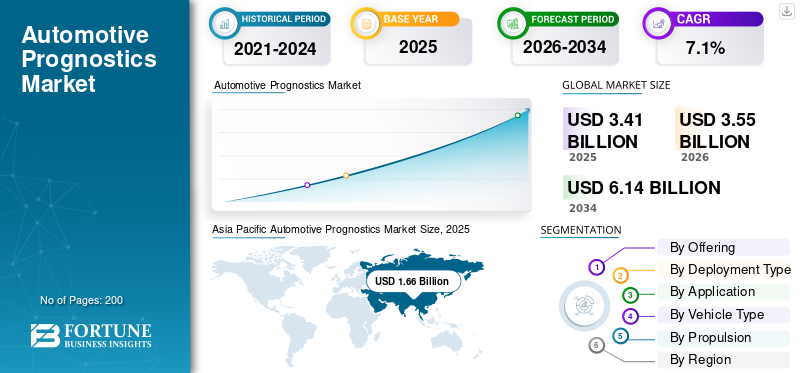

The global automotive prognostics market size was valued at USD 3.41 billion in 2025. The market is projected to grow from USD 3.55 billion in 2026 to USD 6.14 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period. Asia Pacific dominated the global automotive prognostics market with a market share of 48.68% in 2025.

The market refers to technologies and systems that enable the prediction of potential vehicle component failures before they occur. These systems utilize real-time data from sensors, telematics, and electronic control units (ECUs), combined with AI and machine-learning algorithms, to analyze performance trends. By estimating the remaining useful life (RUL) of components, prognostic solutions allow timely maintenance and enhance the overall vehicle reliability, safety, and efficiency. This market includes hardware, software, and cloud-based analytics integrated within connected and intelligent vehicles.

The market is driven by the rapid growth of connected and electric vehicles, increasing demand for predictive maintenance, and advancements in AI-based analytics. OEMs are focusing on reducing unplanned downtimes and warranty costs through the integration of digital health management systems. The rising adoption of telematics, 5G connectivity, and vehicle-to-cloud communication enables real-time monitoring and data-driven maintenance decisions. Additionally, stringent regulations related to vehicle safety, emissions, and operational efficiency are encouraging manufacturers to invest in advanced prognostic solutions.

The automotive prognostics market is moderately consolidated, with major OEMs and Tier-1 suppliers investing in predictive analytics platforms. Key players include Bosch, Continental AG, Siemens Mobility, Delphi Technologies, ZF Friedrichshafen, and Garrett Motion. These companies focus on AI-enabled diagnostic software, cloud-based maintenance platforms, and partnerships with automakers to expand their offerings. Emerging players, such as Uptake Technologies, Noregon Systems, and Pitstop, are introducing machine-learning-based solutions that provide real-time vehicle health insights, thereby strengthening competition and driving innovation.

Download Free sample to learn more about this report.

Automotive Prognostics Market Takeaways

- 2025 Market Size: USD 3.41 billion

- 2026 Market Size: USD 3.55 billion

- 2034 Forecast Market Size: USD 6.14 billion

- CAGR: 7.1% from 2026–2034

- Asia Pacific dominated the automotive prognostics market with a 48.68% share in 2025.

- The SUVs segment held the largest market share in 2025 due to high adoption of predictive maintenance technologies.

- The battery management segment is projected to grow at the fastest CAGR of 8.6%, exceeding the overall market CAGR of 7.1%.

North America

North America remains a key market, driven by early adoption of telematics, advanced diagnostics, and predictive maintenance solutions across passenger and commercial vehicle fleets.

Europe

Europe is witnessing steady growth due to rising electric vehicle adoption and increasing implementation of cloud-based prognostic analytics by major automotive manufacturers.

Asia Pacific

Asia Pacific led the global market in 2025 and is expected to maintain its dominance through 2034, supported by strong vehicle production, rapid EV adoption, and increasing deployment of AI-based predictive analytics.

U.S.

The U.S. market is driven by strong fleet-level prognostic adoption, with leading automakers integrating predictive maintenance capabilities into connected vehicle services.

Japan

Japan continues to strengthen its position through advanced telematics infrastructure, connected mobility initiatives, and growing deployment of battery management and prognostic systems in electric vehicles.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Increased Vehicle Connectivity and Telematics Integration to Drive the Market Growth

The rapid expansion of connected vehicle technologies and telematics systems has become one of the most influential drivers of the automotive prognostics industry. Modern vehicles are increasingly equipped with embedded sensors, communication modules, and telematics control units that continuously transmit operational data, including temperature, vibration, and fuel efficiency. The integration of 4G/5G networks, IoT, and vehicle-to-cloud (V2C) communication enables automakers and fleet operators to collect and analyze data in real-time. Such connectivity forms the backbone for implementing predictive analytics and prognostic algorithms, allowing early fault detection and optimized maintenance schedules.

- For instance, in January 2025, ZF launched its AI-driven SCALAR fleet management platform at the Bharat Mobility Global Expo 2025. This solution is designed to optimize commercial vehicle fleet operations by providing real-time data analysis, predictive maintenance, and route optimization for both internal combustion engine (ICE) and electric vehicles.

Such developments are likely to drive the automotive prognostics market growth.

MARKET RESTRAINTS:

Data Privacy and Cybersecurity Concerns May Limit the Market Growth

Data security has emerged as one of the most critical restraints for the market, primarily due to the heavy reliance on real-time data transfer between vehicles, OEM servers, and cloud platforms. Prognostic systems continuously collect sensitive information such as vehicle location, driving behavior, component health, and system performance, which, if compromised, can lead to significant privacy breaches or unauthorized access. As vehicles become increasingly connected, they also become more susceptible to cyberattacks and data manipulation, posing significant risks to both automakers and end-users. The growing complexity of connected ecosystems demands multi-layered cybersecurity frameworks, which add to the overall system cost and development time. In recent years, regulatory bodies have strengthened data protection laws, further complicating global implementation. For instance, Europe’s General Data Protection Regulation (GDPR) and emerging U.S. automotive cybersecurity frameworks mandate stringent control over how vehicle data is collected, stored, and transmitted. These factors may restrain market growth.

MARKET OPPORTUNITIES:

Rising Adoption of Electric and Autonomous Vehicles to Create Lucrative Growth Opportunities

The accelerating transition toward electric and autonomous mobility represents one of the most transformative opportunities for automotive prognostics industry players. Electric vehicles (EVs) rely heavily on predictive maintenance to ensure the optimal performance of batteries, electric drivetrains, inverters, and thermal management systems. Unlike traditional internal combustion engines, EVs require the continuous monitoring of key parameters, including the state of health (SOH), state of charge (SOC), temperature, and voltage balance. Prognostic solutions equipped with advanced AI algorithms can analyze this data to forecast degradation patterns, estimate remaining useful life (RUL), and schedule maintenance before performance drops. This proactive approach enhances battery longevity and also reduces warranty and recall costs for OEMs, a key concern in a competitive EV landscape.

Prognostic systems in autonomous vehicle can monitor critical systems such as LiDAR sensors, control modules, ADAS units, and electronic braking systems, ensuring uninterrupted functionality and operational safety. As electrification and automation continue to reshape the mobility landscape, the deployment of intelligent prognostic systems will become a strategic differentiator for OEMs seeking to deliver safer, more reliable, and cost-efficient vehicles. This development is anticipated to drive the market growth.

AUTOMOTIVE PROGNOSTICS MARKET TRENDS:

Growing Penetration of Connected and Cloud-Based Platforms is one of the Significant Market Trends

The integration of connected and cloud-based architectures is one of the prominent trends shaping the market. Modern vehicles are increasingly equipped with embedded telematics control units (TCUs), IoT sensors, and vehicle-to-cloud (V2C) communication systems that enable continuous data collection and transmission. This connectivity enables manufacturers to collect real-time data on vehicle health, performance, and environmental conditions, thereby forming the backbone of predictive maintenance. By leveraging cloud computing and edge analytics, automakers can remotely process large volumes of sensor data, detect anomalies, and accurately predict component degradation. This capability is especially critical for global OEMs and fleet operators managing thousands of vehicles, as it enhances scalability and reduces reliance on manual inspections. This development drives the market growth during the forecast period.

- For instance, Volkswagen’s Industrial Cloud and Ford’s Pro Intelligence Platform enable real-time monitoring, remote diagnostics, and over-the-air (OTA) updates across their connected vehicle fleets. These solutions reduce downtime and maintenance costs and also support continuous learning through data feedback loops, improving prediction accuracy over time.

Download Free sample to learn more about this report.

MARKET CHALLENGES:

Complexity in Data Integration and Standardization is a Challenging Factor for the Market

One of the most significant challenges for market expansion is the lack of standardization and data interoperability among OEMs, Tier-1 suppliers, and telematics providers. Every automaker employs unique data architectures, sensor protocols, and diagnostic frameworks, which makes it difficult to create a universal prognostic model applicable across multiple vehicle brands and systems. Integrating diverse data sources from powertrain, braking, and suspension sensors to cloud analytics requires extensive calibration and validation. This complexity limits scalability and increases development timelines for predictive systems. Moreover, the absence of standardized communication protocols restricts collaboration between OEMs and software vendors, delaying industry-wide implementation.

Segmentation Analysis

By Offering

Surging Demand for Sensor-Based Vehicle Monitoring Boosts Hardware Segment Growth

On the basis of segmentation by offering, the market is classified into hardware and software.

The hardware segment holds the largest automotive prognostics market share. Growth in this segment is driven by the rising integration of advanced sensors for powertrain, braking, and battery health monitoring. The increasing adoption of connected vehicles and IoT technologies further enhances the requirement for high-precision data acquisition hardware. Although hardware growth is moderate compared to software, innovations in cost-efficient, durable sensors and onboard diagnostics units continue to expand the hardware ecosystem.

The software segment is set to expand at a CAGR of 7.7%, depicting the fastest growth, over the forecast period.

By Vehicle Type

High Adoption of ADAS and Connected Technologies Positions SUVs as the Leading Vehicle Type

In terms of vehicle type, the market is categorized into hatchback/sedan, SUV, light duty vehicle, and heavy duty vehicle.

The SUVs segment held the largest market share in 2025, owing to their global popularity and higher electronic content compared to compact cars. The segment has also emerged as the fastest-growing segment and its growth is supported by the increased integration of advanced driver-assistance systems (ADAS), complex powertrain architectures, and enhanced connectivity features. Prognostic technologies are widely used in SUVs to monitor suspension, braking, and transmission systems, ensuring safety and comfort in long-distance and off-road conditions. Automakers such as Toyota, Ford, and BMW are embedding predictive health monitoring software into their SUV models to enhance performance reliability

In June 2025, Samsara Inc. announced over a dozen new AI-powered solutions designed to transform safety and efficiency for frontline teams. Powered by Samsara’s open platform, these innovations include AI-driven safety tools, a connected wearable device, advanced routing capabilities, and enhanced maintenance features.

To know how our report can help streamline your business, Speak to Analyst

By Application

Powertrain Prognostics Segment Dominates Driven by Rising Demand for Performance and Reliability Optimization

Based on application, the market is segmented into powertrain prognostics, battery management, braking system prognostics, steering and suspension prognostics, and others.

The powertrain prognostics segment accounts for a dominant share of the market, driven by the need to enhance performance, efficiency, and reliability of critical vehicle components such as engines, transmissions, and drivetrains. With the growing complexity of internal combustion and hybrid systems, OEMs are increasingly adopting predictive maintenance tools to detect issues such as gear wear, fuel system inefficiencies, and lubricant degradation before failure occurs. Advanced sensor integration and AI-driven analytics have enabled real-time condition monitoring, reducing downtime and warranty costs.

For instance, in January 2024, Bosch announced a partnership with Here Technologies and Daimler Truck on an advanced driver assistance system (ADAS) with predictive powertrain control for commercial vehicles to enhance efficiency and reduce emissions.

The battery management segment is set to exhibit the fastest growth at a CAGR of 8.6% over the forecast period.

By Propulsion

ICE Segment Maintains a Strong Market Presence Owing to the Large Global Fleet of Conventional Vehicles

Based on propulsion, the market is segmented into ICE, EV, and HEV

The ICE segment continues to hold a dominant market share, driven by the vast global fleet of gasoline and diesel-powered vehicles that still dominate production in developing regions. Prognostic systems in ICE vehicles focus on monitoring key components such as engines, exhaust systems, fuel injectors, and transmissions to detect early signs of wear or malfunction. Stricter emission standards and rising maintenance costs have encouraged OEMs to deploy predictive analytics to enhance performance and reduce downtime.

January 2024: Mercedes-Benz announced the new MBUX Virtual Assistant at CES 2024, highlighting its use of generative AI for a more intelligent user experience, including health and service recommendations.

The EV segment is poised to emerge as the fastest-growing segment with a CAGR of 7.6% over the analysis period.

By Deployment Type

Adoption of Edge Computing and Advanced ECUs Strengthens Growth of On-Board Deployment Solutions

Based on deployment type, the market is segmented into on-board deployment and cloud-based deployment.

The on-board deployment segment leads the automotive prognostics market, focusing on systems integrated directly into the vehicle’s electronic control units (ECUs) and telematics modules. These systems process diagnostic and predictive data locally, providing real-time fault detection without the need for continuous cloud connectivity. This deployment model is especially beneficial in regions with limited internet infrastructure or data security restrictions. Growth is supported by the adoption of edge computing and advanced ECUs, enabling faster in-vehicle decision-making and reduced latency.

- Bosch integrates powerful AI directly into vehicles and uses robust vehicle computers that combine different functions on a single system-on-chip (SoC) to enable real-time, on-board decision-making.

The cloud-based deployment segment is anticipated to exhibit the fastest growth at a CAGR of 7.4% during the forecast period.

Automotive Prognostics Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Prognostics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region dominates the global automotive prognostics industry and is expected to maintain its leadership through 2034, driven by high vehicle production volumes, rapid electrification, and the strong adoption of connected mobility solutions. Countries such as China, Japan, South Korea, and India are investing heavily in automotive digitalization and AI-based predictive analytics. China’s expanding EV ecosystem and Japan’s advanced telematics infrastructure have made the region a hub for battery management and cloud-based prognostic systems.

- For instance, in August 2024, BYD and Huawei announced a significant agreement for BYD to incorporate Huawei's advanced autonomous driving system, Qiankun, in its Fangchengbao premium off-road EV brand (specifically the Bao 8 SUV). While this collaboration centers on smart driving features and does not involve predictive maintenance platforms, it exemplifies the growing integration of digital and AI-based automotive technologies in the region, further supporting the market's growth.

Other Regions

North America and Europe are the secondary markets for automotive prognostics, driven by the early adoption of telematics, advanced diagnostics, and stringent safety and emission standards. The U.S. leads in fleet-level prognostic adoption, as OEMs such as Ford, General Motors, and Volvo Trucks incorporate predictive maintenance into their connected services.

In contrast, Europe’s growth is fueled by rising EV adoption and OEMs such as Volkswagen and BMW deploying cloud-based analytics. Meanwhile, in the rest of the world, Latin America and the Middle East and Africa remain in the early adoption stage, limited by digital infrastructure. However, the market in these regions is gradually evolving with the expansion of fleet telematics.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Predictive Technology Providers Form Strategic Alliances to Enhance their Market Positions

The automotive prognostics market is led by prominent Tier-1 suppliers and technology firms such as Bosch Mobility Solutions, Continental AG, ZF Friedrichshafen AG, Siemens Mobility, Delphi Technologies (BorgWarner), and Garrett Motion Inc. These companies are pioneering advanced predictive maintenance and vehicle health management platforms in collaboration with leading OEMs including Toyota, Ford, General Motors, BMW, and Volkswagen. Their offerings span hardware components and AI-driven software platforms that enable real-time data analytics, predictive diagnostics, and over-the-air (OTA) updates to ensure optimized vehicle performance and uptime.

Key market players are strategically leveraging AI, cloud computing, and digital twin technologies to strengthen their competitive positioning in the era of connected and electric mobility. Partnerships between OEMs and cloud service providers such as AWS, Microsoft Azure, and Google Cloud are accelerating the development of scalable prognostic ecosystems. Companies are also expanding through mergers, R&D investments, and connected fleet solutions to address the growing demand for predictive maintenance in EVs, hybrids, and commercial fleets.

LIST OF KEY AUTOMOTIVE PROGNOSTICS COMPANIES PROFILED:

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- ZF Friedrichshafen AG (Germany)

- Siemens Mobility (Germany)

- Garrett Motion Inc. (Switzerland)

- Denso Corporation (Japan)

- Magna International Inc. (Canada)

- NXP Semiconductor N.V. (Netherlands)

- Infineon Technologies AG (Germany)

- HCL Technologies Limited (India)

- SAP (Germany)

- Cummins Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- In September 2025, ZF Friedrichshafen AG launched its Predictive Vehicle Health Monitoring Solution, capable of monitoring drive-products in real-time on delivery vehicles and detecting stress peaks early to prevent unplanned downtime.

- In March 2025, Platform Science and Cummins Inc. partnered to launch Vehicle Health Intelligence in the Virtual Vehicle Marketplace, allowing fleets to register online and access real-time engine health diagnostics and OTA updates.

- In November 2024, Infineon Technologies and Aurora Labs announced an AI-powered automotive predictive maintenance system, integrating Aurora’s AI technology with Infineon’s microcontrollers to enable the real-time monitoring of critical automotive systems (steering, braking).

- In January 2024, Mercedes-Benz announced the new MBUX Virtual Assistant at CES 2024, highlighting its use of generative AI for a more intelligent user experience, including health and service recommendations.

- In May 2023, BMW Group deployed an AI supported Smart Maintenance system at its Regensburg plant which monitors conveyor systems and proactively identifies faults, preventing 500 minutes of downtime annually.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.1% from 2025-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Offering, By Vehicle Type, By Application, By Propulsion, By Deployment Type, and By Region |

| By Offering |

|

| By Vehicle Type |

|

| By Application |

|

| By Propulsion |

|

| By Deployment Type |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.41 billion in 2025 and is projected to reach USD 6.14 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.66 billion.

The market is expected to exhibit a CAGR of 7.1% during the forecast period of 2026-2034.

The SUV segment led the market by vehicle type in 2025.

Increased vehicle connectivity and telematics integration is a key factor driving the market growth.

Asia Pacific dominates the market with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us