Automotive Shock Absorber Market Size, Share & Industry Analysis, By Product Type (Twin-Tube Hydraulic, Gas-Charged Twin-Tube, Mono-Tube, and Others), By Vehicle Type (Two-Wheelers, Passenger Vehicles, Light Commercial Vehicles, and Heavy Commercial Vehicles), By Sales Channel (OEM and Aftermarket) and Regional Forecast, 2026-2034

Automotive Shock Absorber Market Size and Future Outlook

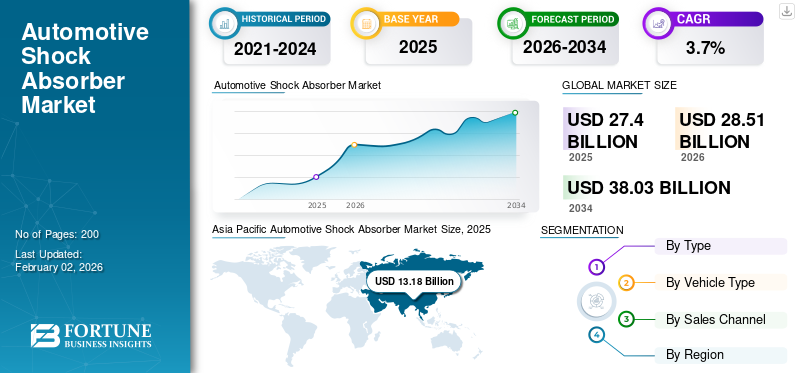

The global automotive shock absorber market size was valued at USD 27.40 billion in 2025. The market is projected to grow from USD 28.51 billion in 2026 to USD 38.03 billion by 2034, exhibiting a CAGR of 3.7% during the forecast period. Asia Pacific dominated the global automotive shock absorber market with a market share of 48.1% in 2025.

Automotive shock absorbers are hydraulic or gas-based components that regulate suspension movement by controlling how a vehicle responds to bumps, vibrations, and uneven road surfaces. They help maintain tire contact, absorb shocks, and manage body motion, which is essential for stable handling across all vehicle types, from a basic passenger car to high-performance or commercial models. Depending on design, manufacturers commonly use twin-tube, gas-charged, or mono-tube formats to meet different performances and durability requirements.

Automotive shock absorbers remain highly relevant because they directly influence overall vehicle safety, comfort, and control. By stabilizing braking, cornering, and steering response, they help reduce wear on tires and suspension joints while ensuring predictable road behavior under different driving conditions. Their importance is growing as consumers increasingly expect smoother rides, greater stability, and refined comfort, especially in regions where vehicles frequently encounter poor road quality or variable climate conditions.

The market is experiencing sustained momentum due to rising demand for SUVs, crossovers, and mid-segment passenger vehicles, particularly in fast-growing regions such as Asia Pacific. Aging vehicle fleets globally are boosting aftermarket replacement rates, while electrification trends are encouraging the development of stronger, better-tuned dampers that can support added battery mass. At the same time, automakers are investing in chassis upgrades to meet stricter safety regulations and improve handling performance. These combined factors are anticipated to drive a steady growth trajectory throughout the forecast period.

Leading manufacturers are focusing on innovation to differentiate their products and meet new suspension challenges. ZF Friedrichshafen AG and KYB Corporation are using advanced technologies such as electronically controlled damping, lightweight piston assemblies, and improved corrosion-resistant materials. Their research efforts center on enhancing reliability, reducing maintenance needs, and offering better adaptability for modern and electric vehicle platforms. As a result, the industry is gradually shifting toward more durable, efficient, and technologically sophisticated shock absorber systems.

Download Free sample to learn more about this report.

AUTOMOTIVE SHOCK ABSORBER MARKET KEY TAKEAWAYS

Market Size & Forecast

Market Size & Forecast

- 2025 Market Size: USD 27.40 Billion

- 2026 Market Size: USD 28.51 Billion

- 2034 Forecast Market Size: USD 38.03 Billion

- CAGR: 3.7% from 2026–2034

Market Share

Market Share

- Asia Pacific dominated the global automotive shock absorber market with a market share of 48.1% in 2025.

- Aftermarket segment is expected to grow at a CAGR of 2.9% over the forecast period.

- Passenger Vehicles accounted for the largest market share.

Key Regional Highlights

Key Regional Highlights

North America

North America recorded steady growth due to its large SUV and pickup truck fleet, along with strong aftermarket replacement demand.

Europe

Europe held the second-largest market share, supported by premium vehicle production, stringent safety regulations, and increasing adoption of advanced damping technologies.

Asia Pacific

Asia Pacific led the market and is expected to remain the fastest-growing region, driven by high vehicle production volumes, expanding passenger vehicle fleets, and rising demand for ride comfort and safety.

China

China remains a key growth engine within Asia Pacific, supported by its position as the world’s largest automotive manufacturing hub.

Rest of the World

Rest of the World markets are witnessing moderate expansion due to increasing vehicle ownership, infrastructure development, and demand for durable suspension systems.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Global Light-Vehicle Production Growth Boosts Automotive Shock Absorber Demand

Rising light-vehicle production directly increases OEM fitment and future replacement volumes for shock absorbers. OICA data show global motor vehicle output rebounding past 90 million units in 2023, and sustained recovery in major markets supports growing demand for suspension components over the forecast period.

- For instance, according to International Energy Agency, in 2023, almost 14 million electric cars were sold all over the globe, adding a large new base requiring future damping replacements.

MARKET RESTRAINTS

Alternative Suspensions Resulting in Diluted Conventional Damper Content to Hinder Market Demand

Growing use of air springs, active suspension, and integrated chassis systems can reduce reliance on traditional stand-alone dampers in some vehicle classes. As these architectures proliferate in premium segments, they can cap potential market share gains for conventional shock absorber designs.

- For instance, a 2024 review on Active Suspension Systems for Road Vehicles notes that advanced air-spring and active-suspension architectures (e.g. air suspension, adaptive suspension) are increasingly viable alternatives to conventional shocks reducing demand pressure for traditional shock absorbers in vehicles opting for such systems.

MARKET OPPORTUNITIES

Rapid EV Rollout Creates Demand for Specialized Dampers

Rapid EV growth opens prospects for advanced shock absorber technologies tailored for battery mass, torque delivery and regenerative braking dynamics. With nearly one in five cars sold in 2023 being electric, suppliers investing in EV-focused designs can secure outsized value growth.

- For instance, modern EVs with heavy battery packs and altered weight distribution are accelerating demand for enhanced suspension solutions. A 2025 article cites active/adaptive suspension as a key enabler for EV ride comfort and stability under battery load.

MARKET CHALLENGES

Challenges in EV Suspension to Balance Weight, NVH, and Efficiency to Hinder Market Growth

Heavier battery packs and different torque characteristics increase suspension and NVH stress in EVs can hamper the automotive shock absorber market growth. Engineers must deliver durable damping, acceptable cost, and optimized ride/handling while managing tire and energy losses, under tightening noise-vibration-harshness expectations and volatile raw material prices.

- For instance, the U.S. IIHS reported in 2024 that EVs weigh 600-1,000+ pounds more than comparable gasoline cars, increasing braking, handling, and suspension load challenges.

AUTOMOTIVE SHOCK ABSORBER MARKET TRENDS

Smart Dampers Converge with Centralized Vehicle Control to be the Prominent Market Trend

Suspension is increasingly linked to centralized ADAS and chassis-domain controllers, with electronically controlled dampers adjusting in real time based on sensor data. Systems like BMW’s Electronic Damper Control demonstrate how damping maps integrate with driving modes and stability functions for refined dynamics.

- For instance, adaptive suspension systems like Magneti Marelli’s MagneRide (magnetorheological dampers) continue expanding across premium and performance vehicles showing industry shift toward suspension that adapts in real time to road and load conditions.

Download Free sample to learn more about this report.

![]() Segmentation Analysis

Segmentation Analysis

By Product Type

Twin-Tube Hydraulic Segment Dominate as They are Widely Prevailing in Everyday Road Vehicles

On the basis of product type, the market is segmented into twin-tube hydraulic, gas-charged twin-tube, mono-tube, and others.

Twin-tube hydraulic shock absorbers dominate because they are widely used on mainstream passenger cars, SUVs, and light trucks. They offer a cost effective balance of comfort, control and durability, making them the default choice for high-volume OEM applications and many replacement parts.

- For instance, Monroe and other technical sources describe twin-tube shocks as the most common design for everyday passenger vehicles l.

Others segments is expected to grow at a CAGR of 6.4% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Passenger Cars Dominate Due to Their Everyday Usage for Daily Commuting

On the basis of vehicle type, the market is segmented into two-wheelers, passenger vehicles, light commercial vehicles, and heavy commercial vehicles.

Passenger cars dominates the segment as they form the largest share of the global vehicle fleet and annual production. Their widespread use for daily commuting, coupled with rising consumer demand for comfort and safety, drives continuous OEM fitment and recurring replacement cycles.

- For instance, OICA data show global motor vehicle output reached 93.5 million units in 2023, with passenger cars representing the bulk of production.

Two-wheeler segment is expected to grow at a CAGR of 3.4% over the forecast period.

By Sales Channel

Aftermarket Leads Due to High Requirement Arising from Aging Fleets and Replacement Cycles

On the basis of sales channel, the market is segmented into OEM and aftermarket.

- The aftermarket dominates the market because vehicles typically undergo one or more suspension overhauls during their life. For example, ACEA reports EU cars now average 12.3 years, supporting strong long-term demand for replacement shocks and related components,

implying multiple replacement opportunities as owners seek to maintain consumer demand for comfort and safety.

Aftermarket segment is expected to grow at a CAGR of 2.9% over the forecast period.

Automotive Shock Absorber Market Regional Outlook

By geography, the automotive shock absorber market is categorized into North America, Europe, Asia Pacific, and Rest of the World.

Asia Pacific

Asia Pacific dominates the global automotive shock absorber market share and is also expected to remain the fastest-growing region in the forecast period, supported by high vehicle production volumes that exceed million units annually and expanding passenger car fleets. Asia Pacific is projected to maintain the highest market share throughout the forecast period on the account of strong manufacturing ecosystems, rising disposable incomes, and increasing consumer demand for comfort and safety make the region a key market for both OEM and aftermarket suppliers. Rapid urbanization, diverse driving environments, and ongoing technological advancements continue to accelerate the demand for shock absorbers, while local manufacturers broaden coverage across multiple market segments. For instance, China produced over 26 million vehicles in 2023, accounting for more than one-third of global output according to the China Association of Automobile Manufacturers (CAAM). This massive concentration of OEM manufacturing directly drives the region’s outsized demand for shock absorbers, as every new vehicle requires factory-installed dampers and generates a long-term aftermarket base.

Asia Pacific Automotive Shock Absorber Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe

Europe follows as the second-largest region, driven by premium and performance vehicle production and a strong focus on advanced shock absorber technologies. Stringent safety standards and a mature automotive ecosystem encourage continuous research and development, particularly in adaptive and lightweight damper systems. The region’s emphasis on sustainability also shapes material choices as manufacturers seek alternatives to traditional raw material inputs.

North America

North America exhibits steady but slower growth, supported by a sizable light-truck and SUV fleet and consistent aftermarket replacement cycles. In the U.S., the market is reinforced by an aging vehicle parc and dominance of pickups and SUVs, which experience higher suspension wear and support steady aftermarket-driven shock absorber demand. The region benefits from stable growing demand, though it is comparatively less dynamic than Asia Pacific and Europe due to slower platform turnover.

Rest of the World

The Rest of the World shows moderate expansion, reflecting rising motorization rates and infrastructure development. While volumes remain smaller, these markets demonstrate rising demand for durable, cost-efficient shock absorber technologies suited to challenging road conditions.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and OEM Integration Shape Competition in the Global Market

The global automotive shock absorber market is moderately consolidated, with long-established suspension system manufacturers, performance damping specialists, and emerging regional suppliers competing through material innovation, tuning precision, and OEM integration. Companies are focusing on enhancing durability, reducing weight, and improving ride quality to meet the evolving needs of SUVs, electric vehicles, and varied driving conditions across global markets. Product differentiation increasingly relies on advanced valving systems, corrosion-resistant coatings, and optimized manufacturing processes designed to support both premium and cost-effective applications.

Leading participants such as ZF Friedrichshafen AG, KYB Corporation, Tenneco (Monroe), and Bilstein play a central role in shaping market standards. ZF continues to invest in electronically adjustable damping platforms and intelligent chassis systems that enhance comfort and handling. KYB Corporation strengthens its position through new electronically controlled shock technologies and expanded OEM programs, while Monroe focuses on long-life dampers engineered for higher durability and consistent performance across millions of operating cycles. Regional players in Asia Pacific are also increasing their presence, offering competitively priced solutions while improving product quality and distribution capabilities.

- For example, KYB recently announced expanded OE-fit electronically controlled damper applications for major Japanese and European automakers, highlighting how technological upgrades and platform-specific calibration have become essential drivers of competitive advantage in the shock absorber industry.

LIST OF KEY AUTOMOTIVE SHOCK ABSORBER COMPANIES PROFILED

- KYB Corporation (Japan)

- ZF Friedrichshafen AG (Germany)

- DRiV Automotive Inc. (U.S.)

- Hitachi Astemo Ltd. (Japan)

- Thyssenkrupp Bilstein (Germany)

- HL Mando (South Korea)

- Magneti Marelli (Italy)

- Astemo, Ltd. (Japan)

- Fox Factory Inc. (U.S.)

- Meritor Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Bilstein reported that its DampTronic IIsemi-active damper technology has been redesigned from small-series applications to full mass production for a Bavarian premium OEM. The continuously variable damper aims to reconcile sporty dynamics with high ride comfort and is now being rolled out in larger volumes.

- January 2025: An aftermarket report described Hitachi Astemo’s presence at Automechanika Shanghai 2024, where it showcased Honda-branded parts and, for the first time, modified motorcycle shock absorbers and braking systems. High-performance front and rear shocks were highlighted for safety and performance gains in two-wheeler applications.

- August 2024: KYB America launched complete shock assemblies for vehicles using rear shock mounts, combining shock, mount and boot in one pre-assembled unit. The plug-and-play design aims to reduce installation time, improve durability and support growing aftermarket demand for quick, OE-quality replacement solutions.

- June 2024: DRiV (Tenneco) announced a major expansion of its Monroe steering and suspension range, adding around 750 new part numbers and increasing coverage by roughly 20%. The investment includes digital catalogues, tech support and anti-counterfeit measures, strengthening Monroe’s position in the global replacement shock and suspension market.

- January 2024: Monroe Intelligent Suspension confirmed that its CVSA2/Kinetic H2 system equips the 2024 McLaren 750S. The hydraulically interconnected, semi-active damping and roll-control technology is designed to deliver high agility and stability while preserving day-to-day ride comfort in one of the latest high-performance supercars.

REPORT COVERAGE

The global automotive shock absorber market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Vehicle Type, Sales Channel and Region |

| By Product Type |

|

| By Vehicle Type |

|

| By Sales Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 27.40 billion in 2025 and is projected to reach USD 38.03 billion by 2034.

In 2025, the market value stood at USD 13.18 Billion.

The market is expected to exhibit a CAGR of 3.7% during the forecast period.

The twin-tube hydraulic segment led the market by product type.

Growing adoption of advanced suspension systems driving the growth for automotive shock absorber market.

KYB Corporation, ZF Friedrichshafen AG, HL Mando, and Magneti Marelli are the prominent players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us