SUV Market Size, Share & Industry Analysis, By Vehicle Type (Compact, Mid-sized, and Full-sized), By Propulsion (ICE (Less than 1.5L, 1.5L-2L, and More than 2L) and Electric), By Drivetrain (FWD, RWD, and AWD), By Seating Capacity (5 Seater and more than 5 Seater) and Regional Forecasts, 2026-2034

(Offer valid till 15th Aug 2026)

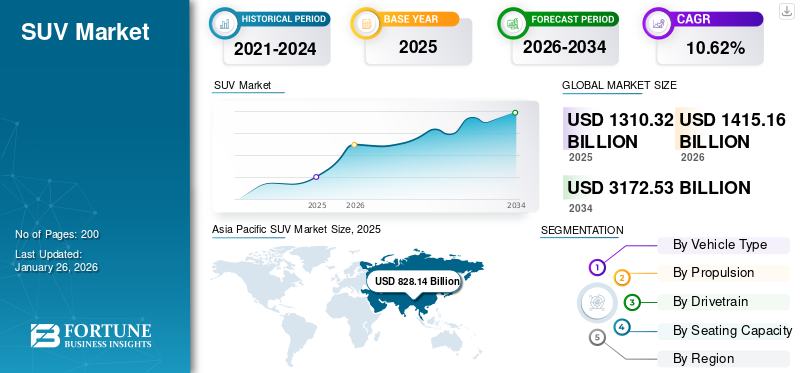

SUV Market Size and Industry Overview

The global SUV market size was valued at USD 1,310.32 billion in 2025 and is projected to grow from USD 1,415.16 billion in 2026 to USD 3,172.53 billion by 2034, exhibiting a CAGR of 10.62% during the forecast period. Asia Pacific dominated the global market, accounting for 63.20% market share in 2025.

The market is driven by evolving consumer preferences toward versatility, higher driving position, and perceived safety advantages, positioning sport utility vehicles as a central pillar of the global passenger vehicle landscape. The SUV market has transitioned from a niche utility-focused segment to a mainstream choice across urban, suburban, and semi-rural environments. This shift has reshaped overall vehicle mix strategies for manufacturers worldwide.

From a structural perspective, the SUV market size reflects broad-based demand across compact, mid-sized, and full-sized categories. Compact SUVs have accelerated penetration in price-sensitive and urban markets, while mid-sized and full-sized SUVs retain strong relevance in regions favoring space, towing capability, and long-distance comfort. Electrification and drivetrain diversification increasingly influence product planning, altering traditional internal combustion engine dominance.

The SUV market growth trajectory is supported by sustained replacement demand, rising household incomes in developing economies, and expanding product portfolios that address multiple price bands. Manufacturers have refined platform architectures to support multiple body styles, improving cost efficiency and accelerating model refresh cycles. This platform-led approach reinforces competitive intensity while maintaining margins.

Regionally, Asia-Pacific and North America represent the strongest volume contributors, though growth dynamics differ. Emerging markets emphasize affordability and fuel efficiency, whereas developed regions prioritize technology, safety systems, and regulatory compliance. Across all regions, the SUV market share continues to expand relative to sedans and hatchbacks, reflecting long-term structural preference shifts rather than short-term cyclical effects.

SUVs are sport utility vehicles designed to combine passenger comfort with higher ground clearance, off-road capability, and versatile cargo space. They range from compact models suitable for urban driving to mid-size and full-size variants built for families, long-distance travel, and off-road adventures. SUVs are available with various propulsion systems, including internal combustion engines (ICE), hybrids, and fully electric powertrains, catering to a wide spectrum of consumer preferences.

The appeal of SUVs comes from their versatility, safety features, spacious interiors, and commanding driving position. Consumers often choose SUVs for their ability to handle diverse road conditions, carry larger loads, and provide comfort for long trips. With electric SUVs, buyers also benefit from lower running costs, zero tailpipe emissions, and advanced connectivity features, without sacrificing utility or performance.

The global SUV market is expanding due to rising consumer demand for versatile vehicles, increasing disposable income in emerging economies, tightening fuel efficiency and emission standards, and a growing interest in electrification. Urbanization and changing lifestyle trends have further reinforced SUV popularity, making them a key segment in the automotive industry.

Automakers are actively innovating in this space to capture market share. Toyota continues to strengthen its SUV lineup with models such as the RAV4 and Highlander, including hybrid variants. Ford has expanded its SUV portfolio globally with vehicles such as the Explorer and Mustang Mach-E electric SUV. Volkswagen offers a range of SUVs from the Tiguan to the ID.4 electric model, targeting diverse consumer needs. Hyundai and Kia are also aggressively pushing hybrid and fully electric SUVs in multiple regions, while luxury vehicle brands such as BMW, Mercedes-Benz, and Audi are introducing premium electric and hybrid SUVs to appeal to environmentally conscious buyers. These moves illustrate the market’s shift from traditional ICE vehicles to electrified offerings while maintaining the SUV’s core characteristics of space, versatility, and performance.

Download Free sample to learn more about this report.

SUV Market KEY TAKEAWAYS

- 2025 Market Size: USD 1,310.32 billion

- 2026 Market Size: USD 1,415.16 billion

- 2034 Forecast Market Size: USD 3,172.53 billion

- CAGR: 10.62% from 2026–2034

- Asia Pacific dominated the SUV market with a 63.20% share in 2025

- The mid-sized SUV segment is projected to account for the largest market share of 41.60% in 2026

- The Internal Combustion Engine (ICE) SUV segment is projected to hold a 58.45% share in 2026

Asia Pacific

Asia Pacific reached USD 828.14 billion in 2025, driven by strong automotive manufacturing and rising SUV demand.

North America

North America reached USD 113.78 billion in 2025, supported by growing demand for larger and electric SUVs.

Europe

Europe reached USD 311.36 billion in 2025, driven by strong demand for hybrid and electric SUVs.

U.S.

U.S. is projected to reach USD 104.33 billion by 2026, fueled by rising demand for mid-sized, full-sized, and electric SUVs.

Japan

Japan is projected to reach USD 91.77 billion by 2026, supported by increasing demand for compact hybrid SUVs.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Advanced Technological Features Enhancing Consumer Appeal

The integration of advanced technological features in SUVs, such as semi-autonomous driving capabilities, enhanced infotainment systems, and advanced safety features, is significantly influencing consumer purchasing decisions. These innovations cater to the growing demand for convenience, connectivity, and safety, making SUVs more attractive to a broader audience.

- For instance, in October 2025, Nissan's 2025 Rogue Platinum model introduced ProPilot Assist for semi-autonomous driving, 3D intelligent viewing systems, and integration with Google and Amazon Alexa services, enhancing the overall driving experience.

The SUV market growth is primarily shaped by a combination of consumer preference shifts, product adaptability, and structural advantages within automotive portfolios. These drivers collectively reinforce the SUV market size expansion across both developed and emerging regions. A key driver is evolving consumer lifestyle preferences. Buyers increasingly favor vehicles that support diverse use cases, including urban commuting, family travel, and recreational activities. SUVs provide elevated driving positions, flexible interiors, and perceived safety advantages. This driver is strongest in suburban and semi-urban markets where multi-purpose mobility is valued.

Another significant driver is the continuous expansion of compact and mid-sized SUV offerings. Automakers have lowered entry price points by optimizing platforms and localizing production. This strategy attracts first-time buyers transitioning from hatchbacks or sedans. Demand is particularly strong in Asia-Pacific and Latin America, where affordability and practicality influence purchasing decisions. Electrification also acts as a growth driver. Electric and hybrid SUVs allow manufacturers to meet emissions regulations while maintaining higher margins compared to smaller vehicle segments. Governments support adoption through incentives and charging infrastructure investment, strengthening SUV market share in Europe and parts of North America.

MARKET RESTRAINTS

Stringent Emission Regulations and Fuel Efficiency Norms to Pose Challenges for Industry Expansion

Governments worldwide are implementing stringent emission regulations and fuel efficiency norms to combat climate change. These regulations pose challenges for traditional internal combustion engine (ICE) SUVs, which typically have larger engines and higher emissions, making compliance more difficult and costly for manufacturers.

- For instance, according to the International Energy Agency (IEA), SUVs accounted for over 20% of the growth in global energy-related CO₂ emissions in recent years, highlighting the environmental concerns associated with their widespread adoption.

Despite sustained SUV market growth, several structural and regulatory constraints continue to moderate expansion across regions and vehicle categories. These restraints affect both demand elasticity and manufacturer cost structures.

Fuel efficiency concerns remain a primary restraint, particularly for internal combustion engine sport utility vehicles. SUVs typically weigh more and have larger frontal areas, resulting in higher fuel consumption compared to passenger cars. Rising fuel price volatility heightens buyer sensitivity, especially in price-conscious markets across Asia-Pacific and Latin America.

Regulatory pressure represents another significant constraint. Governments are tightening emissions and fleet-average efficiency standards, directly impacting SUV market share for larger and higher-displacement models. Compliance requires substantial investment in powertrain optimization, lightweight materials, and electrification. Smaller manufacturers face greater challenges absorbing these costs, limiting competitive diversity.

Urbanization trends also create friction. Congestion, parking limitations, and low-emission zones reduce the practicality of larger SUVs in dense metropolitan areas. This restraint is most evident in European cities and select Asian urban centers, where policy and infrastructure favor compact mobility solutions. Higher ownership costs further restrict adoption. Insurance premiums, maintenance expenses, and tire replacement costs are generally higher for SUVs. These factors influence total cost of ownership calculations for fleet buyers and private consumers alike, slowing purchase decisions.

MARKET OPPORTUNITIES

Shift toward Electrification to Open New Market Opportunities

The shift toward electrification presents significant opportunities for the SUV market. Electric and hybrid SUVs offer eco-friendly alternatives with reduced emissions and lower fuel consumption, appealing to environmentally conscious consumers. This transition is further supported by advancements in battery technology and government incentives promoting clean energy vehicles.

- For instance, in October 2025, BMW's entry-level electric SUV in India has witnessed strong demand, particularly among first-time luxury car buyers, indicating a growing acceptance of electric SUVs in emerging markets.

The SUV market presents multiple opportunity areas as manufacturers adapt portfolios to shifting consumer preferences, regulatory expectations, and technology pathways. These opportunities are unevenly distributed across segments and regions, creating selective growth pockets rather than uniform expansion.

Electrification represents the most significant opportunity. Electric and hybrid sport utility vehicles address regulatory pressure while preserving the body style consumers prefer. Demand is strongest in compact and mid-sized electric SUVs, where range adequacy aligns with urban and suburban usage. This segment supports SUV market growth without relying on larger engine displacement. Emerging markets offer additional upside. Rising disposable income, improving road infrastructure, and aspirational vehicle ownership patterns in Asia-Pacific, the Middle East, and parts of Latin America favor SUVs over traditional sedans. Localized manufacturing and modular platforms improve affordability and expand the addressable market size.

Product innovation creates further openings. Advances in lightweight materials, aerodynamics, and powertrain integration improve efficiency without compromising interior space. Software-defined features, advanced driver assistance systems, and connected services enhance value perception and support premium pricing strategies.

Niche positioning also offers an opportunity. Lifestyle-oriented SUVs targeting off-road capability, performance tuning, or urban luxury attract distinct buyer groups. These niches generate higher margins and strengthen brand differentiation within a competitive SUV market share landscape.

Policy-driven incentives amplify opportunity in specific regions. Subsidies for electric vehicles, charging infrastructure investment, and corporate fleet electrification mandates accelerate adoption. Manufacturers aligning SUV portfolios with sustainability and environmental, social, and governance objectives gain access to institutional buyers and long-term contracts.

SUV MARKET TRENDS

Growing Preference for Compact and Electric SUVs to Boost Industry Development

There is a noticeable shift in consumer preference toward compact and electric SUVs. These vehicles offer a balance between utility and efficiency, appealing to urban dwellers and environmentally conscious buyers. The compact SUV segment has experienced significant growth, driven by factors such as fuel efficiency, maneuverability, and lower emissions.

- For instance, in February 2025, the Tesla Model Y continues to lead global EV sales, with approximately 1.2 million units sold in 2024, underscoring its popularity among consumers seeking compact electric SUVs.

The SUV market trends indicate a sustained shift toward diversified offerings that balance utility, efficiency, and technology integration. Manufacturers increasingly reposition SUVs as multi-purpose vehicles suitable for daily commuting and extended travel. This repositioning continues to expand the addressable customer base across age groups and income segments. Customer demand trends favor compact and mid-sized SUVs, particularly in dense urban regions. Buyers seek elevated seating, flexible cargo space, and advanced safety features without the operating costs associated with larger vehicles. In parallel, premium SUV demand remains resilient, supported by consumers prioritizing comfort, connectivity, and brand differentiation.

Industry drivers shaping these trends include platform modularization and powertrain flexibility. Automakers deploy shared architectures to launch multiple SUV variants rapidly, reducing development cycles. Competitive trends reflect intensified model proliferation, frequent facelifts, and aggressive feature differentiation to defend SUV market share. Product trends highlight the integration of digital cockpits, advanced driver assistance systems, and connected infotainment as standard offerings. Electrified SUVs, including battery electric and hybrid variants, are increasingly central to portfolio strategies. These products address regulatory pressure while aligning with evolving consumer expectations.

Technology and innovation trends focus on lightweight materials, software-defined vehicle architectures, and improved battery energy density. Over-the-air updates and subscription-based features gain traction, altering revenue models. Regulation and compliance trends, particularly emissions and safety standards, influence powertrain choices and design priorities. Globally, Asia-Pacific drives volume expansion, while Europe emphasizes compliance-led electrification. North America sustains demand for larger SUVs, reinforcing regional differentiation within the SUV market growth outlook.

MARKET CHALLENGES

High Development and Compliance Costs Due to Emission Standards

The implementation of stricter emission standards and fuel economy regulations has increased development and compliance costs for SUV manufacturers. Investing in research and development to meet these standards requires significant financial resources, which can impact profitability and pricing strategies.

- For instance, in March 2024, the U.S. Environmental Protection Agency (EPA) announced the stringent CO₂ and NOx limits for light-duty vehicles, compelling manufacturers to invest in cleaner technologies and more efficient powertrains to avoid substantial penalties.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

Mid-Sized Segment Led Due to Urban Versatility and Fuel Efficiency

To know how our report can help streamline your business, Speak to Analyst

Based on vehicle type, the SUV market is segmented into compact, mid-sized, and full-sized SUVs.

In 2026, the mid-sized SUV segment is projected to dominated the market with a share of 41.60% 2026, owing to its suitability for urban commuting, easier parking, fuel efficiency, and affordability. Manufacturers are increasingly focusing on compact SUVs with advanced features and hybrid/electric options to attract urban buyers.

Mid-sized SUVs form the core volume segment globally. They balance interior space, driving comfort, and performance flexibility. This segment captures family buyers and fleet customers, particularly in North America and China. Electrified variants within mid-sized SUVs are gaining traction as battery packaging becomes more efficient.

- For instance, in 2024, the Toyota RAV4 and Honda CR-V recorded strong sales globally, reflecting high consumer demand for compact SUVs combining practicality with modern technology.

Compact SUVs represent the fastest-expanding segment within the SUV market. Buyers favor compact models for urban usability, lower ownership costs, and improved fuel efficiency. These vehicles benefit from shared platforms with passenger cars, enabling competitive pricing and faster electrification. Compact SUVs dominate first-time SUV purchases in Asia-Pacific and Europe, contributing meaningfully to overall SUV market growth.

Full-sized SUVs remain a smaller but high-margin segment. Demand is strongest in North America and the Middle East, where towing capacity, cabin space, and performance are prioritized. Regulatory pressure and fuel efficiency standards limit growth potential, but premium positioning sustains profitability.

By Propulsion

ICE Segment to Lead due to Lower Upfront Costs

The SUV market is segmented by propulsion into internal combustion engine (ICE) and electric.

While ICE SUVs is projected to dominate with a share of 58.45% in 2026, due to existing infrastructure and lower upfront costs, electric SUVs are rapidly gaining traction due to rising environmental awareness and government incentives for EV adoption. Internal Combustion Engine (ICE) SUVs continue to hold a majority share, particularly in regions with limited charging infrastructure. Internal Combustion Engine (ICE) SUVs continue to hold a majority share, particularly in regions with limited charging infrastructure. Sub-segments include:

- For instance, in 2024, the Hyundai Ioniq 5 electric SUV and the Kia EV6 saw notable adoption in Europe and Asia, highlighting increasing consumer confidence in electric SUVs alongside the continuing dominance of ICE models such as the Toyota RAV4.

Electric SUVs represent the most strategically important growth segment. Battery electric SUVs lead adoption in urban markets, while plug-in hybrids serve transitional demand. Electric propulsion reshapes SUV market trends by lowering operating costs and aligning with emission targets.

By Drivetrain

Front-Wheel Drive Segment Dominates the Market due to its Suitability for Urban Use.

By drivetrain, the SUV market is segmented into front-wheel drive (FWD), rear-wheel drive (RWD), and all-wheel drive (AWD).

Front-wheel drive is poised to dominates the market with a share of 48.56% in 2026, due to its fuel efficiency, lower cost, and suitability for urban and suburban driving conditions. FWD models are easier to handle in everyday traffic and require less maintenance, making them popular among mainstream buyers.

- For instance, the Honda CR-V and Toyota RAV4 FWD variants remain widely adopted in 2024, particularly in regions prioritizing efficiency and affordability. While AWD retains its appeal in premium and off-road models, FWD accounted for the largest share of SUV sales globally.

Front-wheel drive (FWD) dominates compact and mid-sized SUVs due to cost efficiency and sufficient performance for urban use. All-wheel drive (AWD) sees higher adoption in premium, electric, and off-road-oriented SUVs, supporting safety and traction requirements. Rear-wheel drive (RWD) remains limited to performance-focused and luxury platforms.

By Seating Capacity

5-Seater Segment Leads due to its Balance Between Passenger Comfort

By seating capacity, the SUVs are segmented into 5-seater and more than 5-seater.

The 5-seater segment is projected to dominates the market with a share of 60.69% in 2026, due to its balance between passenger comfort, cargo space, and maneuverability, appealing to families and urban commuters. These models provide a practical solution for daily use while maintaining sufficient space for weekend trips or cargo transport. Five-seater SUVs account for the largest volume share, aligning with nuclear family and individual buyer needs. More than five-seater SUVs serve large households and commercial use cases, particularly in emerging markets and fleet operations.

- For example, in 2024, the Honda CR-V and Nissan Rogue 5-seater models continued to lead sales globally, reflecting the preference for standard family-sized SUVs. The 5-seater segment remained the most widely purchased, significantly outpacing larger seating capacity models in overall volume.

SUV Regional Market Insights:

By geography, the SUV market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific SUV Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia-Pacific SUV Market Analysis:

The Asia Pacific region held the dominant SUV market share in 2025 and continued its leadership thereafter. Asia Pacific contributed approximately USD 828.14 billion to the global market in 2025, accounting for 63.20% share, and is expected to reach USD 902.68 billion in 2026. This dominance is supported by strong automotive manufacturing capacity, rapid urbanization, growing consumer demand for compact and mid-sized SUVs, and government incentives promoting both ICE and electric vehicles.

China, Japan, and South Korea are leading the charge, with major OEMs such as Toyota, Hyundai, and Honda driving SUV sales through a combination of locally produced models and global partnerships. The Japan market is projected to reach USD 91.77 billion by 2026, the China market is projected to reach USD 391.86 billion by 2026, and the India market is projected to reach USD 132.14 billion by 2026.

- For instance, in 2024, the Kia Sportage and Nissan X-Trail recorded significant sales across the Asia Pacific region, reflecting strong consumer preference for practical, fuel-efficient, and technologically advanced SUVs.

Asia-Pacific represents the fastest-expanding SUV market, driven by rising incomes, urbanization, and shifting consumer aspirations. Compact and mid-sized SUVs dominate volume growth, particularly in China and India. Electrification accelerates unevenly, influenced by national policy support and infrastructure readiness. Local manufacturers increasingly compete with global brands, intensifying pricing pressure and reshaping regional SUV market share dynamics.

Japan SUV Market:

Japan’s SUV market favors compact and efficient models suited to dense urban environments. Hybrid SUVs maintain strong penetration due to fuel efficiency and regulatory alignment. Battery electric SUVs grow gradually, constrained by charging infrastructure and consumer caution. Domestic manufacturers emphasize reliability, safety, and hybrid optimization, maintaining steady SUV market growth within a mature automotive ecosystem.

China SUV Market:

China is the largest and most dynamic SUV market globally, driven by urban demand, policy support, and domestic manufacturing scale. Electric SUVs play a central role in market expansion, supported by incentives and rapid infrastructure deployment. Local brands gain share through competitive pricing and technology integration. Regulatory direction strongly influences product cycles and accelerates SUV market electrification.

Europe SUV Market Analysis:

The market in Europe reached USD 311.36 billion in 2025, representing 23.76% of total market revenue, and is projected to reach USD 328.94 billion in 2026. The European SUV market is shaped by emission regulations, urban density, and evolving consumer priorities. Compact and mid-sized SUVs dominate demand, while full-sized models remain niche. Electrification is central to competitive positioning, with battery electric and plug-in hybrid SUVs expanding rapidly. Policy-driven emission targets influence product planning, compressing margins for internal combustion platforms while accelerating investment in efficient, modular vehicle architectures.

Europe followed Asia Pacific in market share, driven by urbanization, high demand for compact and electric SUVs, and stringent emission regulations encouraging EV adoption. Countries such as Germany, France, and the U.K. are witnessing growth in both premium and mid-sized SUV segments, supported by incentives for hybrid and electric models and expanding charging infrastructure. The UK market is projected to reach USD 74.11 billion by 2026, and the German market is projected to reach USD 63.42 billion by 2026.

Germany SUV Market:

Germany reflects a technology-driven SUV market characterized by premium positioning and engineering depth. Domestic manufacturers lead innovation in electric and performance-oriented SUVs. Demand favors compact and mid-sized models aligned with urban mobility and environmental compliance. Regulatory scrutiny on emissions and lifecycle sustainability drives rapid electrification. Export-oriented production strengthens Germany’s influence within the broader European SUV market landscape.

United Kingdom SUV Market:

The United Kingdom SUV market emphasizes compact and electric SUVs, reflecting urban congestion and policy incentives. Buyers prioritize efficiency, safety, and connectivity over size. Electrification adoption outpaces several European peers due to regulatory clarity and infrastructure investment. Competitive differentiation centers on price accessibility and total cost of ownership, shaping SUV market trends toward smaller, technology-rich vehicle configurations.

North America SUV Market Analysis:

In 2025, North America held 8.68% of the global market share, reaching a valuation of USD 113.78 billion, and is projected to grow to USD 122.1 billion in 2026. North America secured the third position, with the U.S., Canada, and Mexico showing robust demand for mid-sized and full-sized SUVs. Consumer preference for larger vehicles, combined with strong dealership networks and rising adoption of electric SUVs such as the Ford Mustang Mach-E and Tesla Model Y, contributed to overall market growth. The U.S. market is projected to reach USD 104.33 billion by 2026.

North America represents a structurally strong SUV market, driven by consumer preference for larger vehicles, higher disposable incomes, and established road infrastructure. The region shows balanced demand across compact, mid-sized, and full-sized SUVs. Regulatory pressure increasingly shapes powertrain strategies, accelerating electrified SUV adoption. Competitive intensity remains high, with domestic and global manufacturers emphasizing technology integration, safety features, and electrification to protect SUV market share.

United States SUV Market:

The United States dominates regional SUV demand, supported by fuel affordability, lifestyle preferences, and widespread suburban mobility. Mid-sized and full-sized SUVs account for a substantial share of new vehicle sales. Electric SUVs gain momentum in coastal and urban states, supported by policy incentives and charging expansion. Automakers focus on platform scalability and advanced driver assistance systems to sustain SUV market growth amid regulatory tightening.

Latin America SUV Market Analysis:

Latin America’s SUV market shows steady expansion, led by compact and mid-sized models. Affordability and fuel efficiency shape purchasing decisions. Electrification remains limited but emerging, primarily through hybrid offerings. Economic volatility and infrastructure gaps moderate the adoption pace. Global manufacturers prioritize localized production and cost optimization to capture incremental SUV market growth across key economies.

Middle East & Africa SUV Market Analysis:

The Middle East & Africa SUV market is driven by terrain suitability, climate conditions, and preference for durable vehicles. Full-sized SUVs retain relevance, particularly in Gulf countries. Electrification adoption remains early-stage, constrained by infrastructure and fuel economics. Market growth depends on economic diversification efforts, regulatory evolution, and gradual consumer exposure to alternative powertrains.

Over the forecast period, markets in the Rest of the World, including Latin America and the Middle East & Africa, are expected to grow gradually. While adoption of SUVs is increasing due to rising disposable incomes and urban development, sales volumes are smaller compared to APAC, Europe, and North America. Key markets such as Brazil, Mexico, Saudi Arabia, and the UAE are gradually expanding SUV penetration, particularly in mid-sized and compact segments.

Rest of the World

The Rest of the World market accounted for USD 57.03 billion in 2025, representing 4.35% of the global industry, and is expected to reach USD 61.43 billion in 2026.

SUV Industry Competitive Landscape

Key Industry Players

Major Players Focus on Collaborations and Technological Innovation to Strengthen Their Market Position

The global SUV market exhibits a moderately concentrated structure, with leading automakers, EV specialists, and regional brands competing through innovation, strategic partnerships, and electrification initiatives. Key players are focusing on expanding SUV portfolios, integrating advanced technologies, and launching electric variants to attract shifting consumer preferences while maintaining global market share.

Toyota Motor Corporation, Ford Motor Company, and Volkswagen Group are among the top players shaping this market. Toyota continues to expand its SUV lineup with models such as the RAV4 and Highlander, including hybrid versions. Ford has strengthened its presence with the Explorer, Escape, and Mustang Mach-E electric SUV, targeting both traditional and electrified segments. Volkswagen is pushing advanced models such as the Tiguan and ID.4 electric SUV, combining versatility with electrification to meet diverse regional demand. These automakers maintain leadership through R&D, global distribution networks, and technology-driven offerings.

The SUV market is highly competitive, shaped by scale advantages, platform strategies, and rapid powertrain diversification. Global incumbents dominate volume, while new entrants challenge established cost and technology assumptions. Competitive positioning increasingly depends on electrification readiness, supply-chain resilience, and regional adaptability rather than size alone.

Large multinational automakers such as Toyota Motor Corporation and Volkswagen Group leverage broad SUV portfolios spanning compact to full-sized segments. Their strengths lie in platform standardization, manufacturing efficiency, and global distribution. However, legacy internal combustion exposure creates margin pressure as emission regulations tighten. These players respond through modular electric platforms and hybrid-heavy transition strategies.

North American manufacturers, including Ford Motor Company, maintain strong positioning in mid-sized and full-sized SUVs. Brand equity and dealer networks support resilience, particularly in utility-focused segments. Weaknesses include slower cost competitiveness in electric SUVs and dependence on regional demand cycles. Strategic focus centers on software integration, connected features, and selective electrification of high-margin models.

Asian competitors have reshaped competitive dynamics. Hyundai Motor Group competes through aggressive electrification, flexible platforms, and rapid model refresh cycles. Its strength lies in balancing price, technology, and design across regions. Meanwhile, BYD disrupts the SUV market through vertically integrated battery supply, cost leadership, and fast electric SUV scaling, though brand perception remains uneven outside Asia.

Pure-play electric manufacturers, led by Tesla, influence competitive benchmarks despite narrower portfolios. Their advantages include software-driven differentiation and charging ecosystems, offset by limited model diversity.

LIST OF KEY SUV COMPANIES PROFILED

- Toyota Motor Corporation (Japan)

- Volkswagen Group (Germany)

- Mercedes-Benz (Germany)

- Hyundai Motor Company (South Korea)

- General Motors (U.S.)

- Great Wall Motor (China)

- Ford Motor Company (U.S.)

- Mahindra & Mahindra (India)

- BYD Company Ltd (China)

- Renault Group (France)

SUV Industry Key Developments:

- March 2024: Toyota Motor Corporation expanded its global electric SUV lineup, accelerating modular battery platform deployment to support emission compliance and strengthen electric SUV penetration across North America, Europe, and Asia-Pacific markets.

- July 2024: Volkswagen Group advanced its next-generation electric SUV architecture, integrating unified software systems to improve scalability, over-the-air updates, and lifecycle efficiency across multiple SUV brands.

- November 2024: Hyundai Motor Group launched a new mid-sized electric SUV platform, targeting cost reduction and faster production ramp-up through shared components and in-house battery management optimization.

- February 2025: Ford Motor Company restructured its SUV development roadmap, prioritizing high-margin hybrid and electric SUVs to balance regulatory compliance with profitability in North American and European markets.

- May 2025: BYD expanded overseas electric SUV manufacturing capacity, strengthening supply chain localization and accelerating global SUV market growth through competitively priced, battery-integrated vehicle platforms.

REPORT COVERAGE

The global SUV market analysis provides an in-depth study of market size and forecast by all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.62% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, Propulsion, Drivetrain, Seating Capacity, and Region |

|

By Vehicle Type |

· Compact · Mid-sized · Full-sized |

|

By Propulsion |

· ICE o Less than 1.5L o 1.5L-2L o More than 2L · Electric |

|

By Drivetrain |

· Four-Wheel Drive · Rear-Wheel Drive · All-Wheel Drive |

|

By Seating Capacity |

· 5 seater · More than 5 seater |

|

By Geography |

· North America (By Vehicle Type, Propulsion, Drivetrain, Seating Capacity, and Country) o U.S. o Canada o Mexico · Europe (By Vehicle Type, Propulsion, Drivetrain, Seating Capacity, and Country) o U.K. o Germany o France o Italy o Rest of Europe · Asia Pacific (By Vehicle Type, Propulsion, Drivetrain, Seating Capacity, and Country) o China o Japan o South Korea o India o Rest of Asia Pacific · Rest of the World |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1,415.16 billion in 2026 and is projected to reach USD 3,172.53 billion by 2034.

In 2024, the market value stood at USD 828.14 billion.

The market is expected to exhibit a CAGR of 10.62% during the forecast period of 2026-2034.

The mid-sized segment led the market by SUV type.

Advanced technological features enhancing consumer appeal are driving the growth of the SUV market.

Toyota Motor Corporation, Volkswagen Group, Hyundai Motor Company, and Ford Motor Company are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us