Automotive Simulation Market Size, Share & Industry Analysis, By Application (Powertrain & Electrification Simulation, ADAS & Autonomous Driving Simulation, Vehicle Dynamics & Handling, & Others), By Vehicle Type (Passenger Cars and Commercial Vehicles), By Vehicle Autonomy Level (Non-Autonomous/Conventional Vehicles, & Others), By Offering (Simulation Software & Licenses, Simulation Platforms & Integrated Tools, Cloud-based Simulation Solutions, AI-enabled Simulation & Digital Twin Solutions, & Others), By Propulsion, By End User, and Regional Forecast, 2026-2034

Automotive Simulation Market Size and Future Outlook

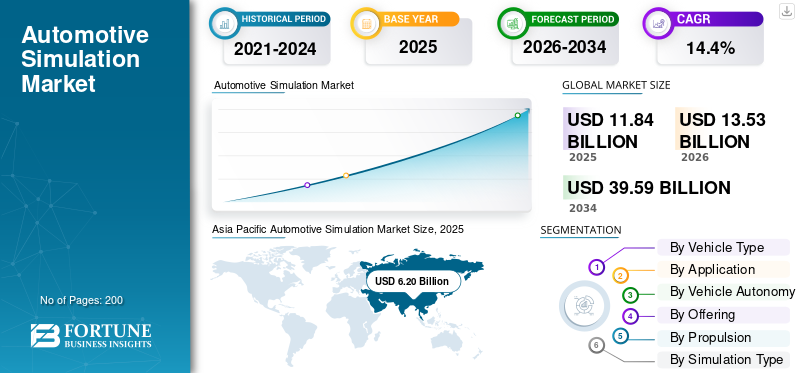

The global automotive simulation market size was valued at USD 11.84 billion in 2025. The market is projected to grow from USD 13.53 billion in 2026 to USD 39.59 billion by 2034, exhibiting a CAGR of 14.4% during the forecast period. Asia Pacific dominated the automotive simulation market with a market share of 52.36% in 2025.

Automotive simulation is the use of virtual models and computational tools to design, test, and optimize vehicle systems, performance, safety, and manufacturing processes before physical prototyping. Market drivers are key factors such as technological advancements, regulatory mandates, cost-efficiency needs, customer demand, and industry competition that stimulate market adoption, investment, and overall growth.

Major players in the market include ANSYS, Siemens, Dassault Systèmes, Altair, MathWorks, PTC, and Autodesk, competing through advanced multiphysics modeling, digital twins, AI integration, cloud platforms, and end-to-end virtual testing and validation solutions.

Download Free sample to learn more about this report.

AUTOMOTIVE SIMULATION MARKET Key Takeaways

- 2025 Market Size: USD 11.84 billion

- 2026 Market Size: USD 13.53 billion

- 2034 Forecast Market Size: USD 39.59 billion

- CAGR: 14.4% from 2026–2034

- Asia Pacific dominated the automotive simulation market with a market share of 52.36% in 2025.

- Commercial vehicles remained the second-largest segment and are projected to expand at a CAGR of 12.9% during the forecast period.

- ADAS & autonomous driving simulation is the fastest-growing application segment, registering a CAGR of 15.6% through 2034.

Asia Pacific

Asia Pacific held the largest market share in 2025 and is the fastest-growing region, supported by strong vehicle production, EV adoption, and increasing investments in autonomous driving technologies.

Europe

Europe represents the second-largest market, expanding at a CAGR of 12.5% over the forecast period. Stringent emission standards, advanced safety mandates, and the strong presence of premium OEMs drive widespread adoption of simulation.

North America

North America held the third-largest share in 2025, supported by strong R&D infrastructure, high technology adoption, and leadership in autonomous and connected vehicle development.

U.S.

The U.S. market in 2026 is estimated at around USD 1.86 billion, accounting for roughly 13.7% of global automotive simulation revenues, fueled by autonomous mobility innovation, AI-driven simulation, and strong cloud-based R&D ecosystems.

Japan

The Japan market in 2026 is estimated at around USD 1.07 billion, accounting for roughly 7.9% of global automotive simulation revenues, supported by advanced OEM R&D, powertrain innovation, and a strong focus on safety validation.

Read More

AUTOMOTIVE SIMULATION MARKET TRENDS

Cloud-Based and AI-Enabled Simulation to Reshape Development Processes

Cloud-based and AI-driven simulation is transforming automotive development workflows. Scalable cloud computing reduces infrastructure costs, while AI accelerates model optimization and testing. These capabilities support remote collaboration, faster iterations, improved accuracy, and quicker time-to-market for advanced vehicle technologies. Cloud-native platforms also improve accessibility for smaller firms, enable elastic scaling for complex simulations, and support global engineering teams working across multiple time zones, strengthening productivity, flexibility, collaboration, innovation speed, and cost efficiency across automotive R&D organizations globally, industry-wide today.

- In January 2026, AI-driven aerodynamic simulation platform AOX was showcased by ADRO Inc. at CES 2026, featuring cloud-based CFD, machine-learning solvers, real-time drag optimization, and scalable workflows, with a public beta launch targeted for H1 2026.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Vehicle Complexity to Bolster Market Growth

Rising vehicle complexity from electrification, software-defined vehicles, ADAS, and autonomous technologies is driving the automotive simulation market growth. OEMs increasingly depend on virtual testing to manage system integration, reduce physical prototyping, shorten development cycles, improve safety validation, and efficiently ensure compliance with evolving global automotive regulations. This approach enables early issue detection, cost control, platform reuse, cross-domain collaboration, faster innovation, reduced recalls, and improved product quality across passenger and commercial vehicle development programs globally for next-generation mobility solutions and sustainable transportation ecosystems.

- In January 2026, NVIDIA launched Alpamayo open AI models, enabling autonomous vehicles to reason contextually using multimodal perception, reinforcement learning, and simulation-trained foundation models, improving decision-making in complex real-world driving scenarios.

MARKET RESTRAINTS

High Implementation Costs and Skill Gaps to Limit Adoption

Automotive simulation requires high upfront investment in software licenses, computing infrastructure, and specialized engineering expertise. Smaller suppliers face budget constraints and limited access to skilled simulation professionals, slowing adoption despite long-term benefits such as cost savings, faster development, and improved design accuracy. These barriers are particularly pronounced in emerging markets, where capital availability, training programs, and digital maturity levels remain uneven across the automotive supply chain, delaying technology diffusion and limiting competitive participation among regional component manufacturers globally.

MARKET OPPORTUNITIES

Digital Twin Integration to Create Lifecycle Optimization Opportunities

Digital twin adoption creates opportunities for automotive simulation across vehicle lifecycles. Virtual environments replicas enable real-time performance monitoring, predictive maintenance, continuous optimization, and data-driven decision-making, helping OEMs and fleet operators improve reliability, reduce downtime, enhance efficiency, and support connected mobility strategies. When integrated with IoT, cloud analytics, and AI, digital twins extend simulation value beyond design into operations, after-sales, and regulatory reporting throughout vehicle ownership, enabling continuous feedback loops, lifecycle intelligence, and long-term performance optimization benefits for manufacturers globally today.

- In January 2026, Siemens introduced a new digital twin software for software-defined vehicles, enabling continuous virtual validation, hardware–software co-development, and real-time lifecycle simulation to accelerate SDV development and reduce integration risks.

MARKET CHALLENGES

Data Validation Complexity to Challenge Simulation Effectiveness

Validating simulation models against real-world conditions remains challenging. Automotive systems generate massive, complex datasets requiring extensive calibration and testing. Inaccurate assumptions or insufficient validation can limit reliability, especially for safety-critical, autonomous, and electrified vehicle applications, impacting confidence in simulation outcomes. Achieving alignment between virtual results and physical behavior demands continuous data updates, sensor accuracy, test correlation, and cross-disciplinary expertise throughout development cycles, increasing development time, validation costs, and engineering complexity for OEMs and suppliers globally across advanced vehicle programs.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

High Software-Intensive Passenger Vehicle Development to Reinforce Passenger Cars Segment Leadership

Based on vehicle type, the market is segmented into passenger cars and commercial vehicles.

The passenger cars segment dominates the market due to high global production volumes, rapid electrification, and rising integration of advanced driver assistance systems and connected features. OEMs increasingly rely on simulation to manage software-heavy architectures, conduct virtual validation, meet stringent safety testing requirements, and comply with regulatory requirements. Frequent model refresh cycles, shorter development timelines, and intense competition in passenger vehicles drive sustained demand for simulation software, digital twins, and virtual testing across design, engineering, and validation stages.

- In January 2026, Qualcomm showcased CES innovations for BMW, highlighting Snapdragon Digital Chassis, AI-driven simulation, virtual validation, and connected compute platforms to accelerate software-defined vehicle development and in-vehicle intelligence deployment.

Commercial vehicles represent the second-largest segment, expanding at a CAGR of 12.9% over the forecast period. Growth is driven by electrification of trucks and buses, stricter emission norms, and increasing use of simulation for durability, powertrain optimization, and autonomous logistics applications.

By Application

Increasing EV Adoption Propels Powertrain & Electrification Simulation Dominance

Based on application, the market is segmented into powertrain & electrification simulation, ADAS & autonomous driving simulation, vehicle dynamics & handling, safety & crash & structural simulation, and thermal & NVH & aerodynamics simulation.

Powertrain & electrification simulation holds the largest automotive simulation market share due to accelerating EV adoption, tightening emission regulations, and the need to optimize batteries, motors, inverters, and thermal systems. OEMs and suppliers rely heavily on simulation to improve energy efficiency, extend driving range, reduce development costs, and validate compliance across multiple global markets, making it a core application throughout vehicle development programs.

- In January 2026, Anritsu showcased electrification testing solutions at CES 2026, featuring high-voltage powertrain simulation, battery emulation, EMC testing, and validation tools supporting EV, ADAS, and software-defined vehicle development.

ADAS & autonomous driving simulation is the fastest-growing application, expanding at a 15.6% CAGR over the forecast period. Growth is driven by rising investments in autonomy, safety mandates, the complexity of sensor fusion, and the need for large-scale virtual scenario testing.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Autonomy Level

Widespread ADAS Adoption and Regulatory Mandates to Anchor Semi-Autonomous Vehicles Segment Leadership

By vehicle autonomy level, the market is divided into non-autonomous/conventional vehicles, semi-autonomous vehicles (ADAS, level 1–2), and highly autonomous vehicles (level 3 & above).

Semi-autonomous vehicles (ADAS, level 1–2) dominate the market due to their high penetration across passenger and commercial vehicles. Mandatory safety features such as AEB, lane keeping, and adaptive cruise control drive continuous simulation demand for system validation, sensor calibration, and functional safety compliance, supporting steady usage across OEMs and Tier-1 suppliers.

Highly autonomous vehicles (level 3 & above) are the fastest-growing segment, expanding at a CAGR of 18.8% over the forecast period. Growth is fueled by robotaxi programs, autonomous logistics, complex scenario validation, and increasing reliance on virtual testing to reduce real-world deployment risks.

- In January 2026, Lucid, Nuro, and Uber debuted a robotaxi at CES 2026, integrating Level 4 autonomous software, sensor fusion, simulation-trained AI models, and electric vehicle platforms for urban mobility deployment.

By Offering

Core Role of Virtual Validation and Engineering Workflows to Sustain Simulation Software & Licenses Dominance

By offering, the market is categorized into simulation software & licenses, simulation platforms & integrated tools, cloud-based simulation solutions, AI-enabled simulation & digital twin solutions, and engineering & consulting & support services.

Simulation software and licenses dominate the market as OEMs and suppliers depend on established tools for vehicle design, multiphysics analysis, virtual testing, and regulatory validation. These solutions form the backbone of engineering workflows, supporting powertrain, structural, safety, and electronics simulations across all development stages, ensuring consistent demand and high renewal rates.

AI-enabled simulation and digital twin solutions are the fastest-growing offering, expanding at a CAGR of 17.0% over the forecast period. Growth is driven by real-time analytics, predictive capabilities, lifecycle optimization, and integration of artificial intelligence and machine learning with cloud-based simulation platforms.

- In January 2026, NVIDIA detailed Alpamayo for autonomous vehicle development, combining simulation-trained foundation models, multimodal perception, generative AI, and scalable virtual testing to improve reasoning, safety validation, and deployment readiness.

By Propulsion

Established Vehicle Base and Mature Development Frameworks to Anchor ICE Segment Leadership

By propulsion, the market is bifurcated into ICE and electric.

The ICE segment holds the largest market share due to the vast global installed base of internal combustion vehicles and its mature development ecosystem. OEMs continue to use simulation extensively for engine optimization, emission compliance, thermal management, NVH analysis, and fuel efficiency improvements. Ongoing regulatory updates, incremental powertrain enhancements, and long production cycles sustain consistent simulation demand across ICE vehicle programs worldwide.

Electric is the fastest-growing segment, expanding at a CAGR of 18.9% over the forecast period. Growth is driven by rapid EV adoption, battery innovation, thermal optimization needs, and heavy reliance on simulation to reduce development time and cost.

- In 2025, according to IEA, global electric car sales are projected to exceed 20 million units, representing more than 25% of total worldwide passenger car sales, reflecting accelerating EV adoption across major automotive markets.

By Simulation Type

Early-Stage Validation and Cost-Efficient Testing to Sustain Software-in-the-Loop Dominance

By simulation type, the market is sub-segmented into model-in-the-loop (MiL), software-in-the-loop (SiL), hardware-in-the-loop (HiL), system-level simulation, and full vehicle/virtual prototyping.

Software-in-the-Loop (SiL) holds a dominant market share due to its cost efficiency, flexibility, and early-stage validation capabilities. OEMs and suppliers extensively use SiL to test control algorithms, software logic, and system interactions before physical hardware availability. Its ability to enable rapid iterations, defect detection, and scalable testing across powertrain, ADAS, and body electronics programs reinforces sustained adoption.

- In January 2025, Stellantis partnered with dSPACE to accelerate cloud-based vehicle development, leveraging scalable simulation, virtual validation, and software-in-the-loop testing to speed software-defined and electrified vehicle programs.

Hardware-in-the-Loop (HiL) is the fastest-growing simulation type, expanding at a CAGR of 16.6% over the forecast period. Growth is driven by increasing ECU complexity, safety-critical validation requirements, and the need for real-time testing under near-production conditions.

By End User

Integrated Vehicle Development and Regulatory Compliance Needs to Anchor Automotive OEMs Segment Leadership

By end-user, the market is subdivided into automotive OEMs, tier-1 suppliers, engineering & simulation service providers, autonomous mobility & technology companies, and research institutes & academia.

Automotive OEMs account for the largest market share, as simulation is deeply embedded across vehicle design, validation, and homologation processes. OEMs rely on simulation to manage multi-domain complexity, reduce physical prototypes, ensure safety compliance, and accelerate time-to-market across ICE, electric, and autonomous vehicle programs globally.

- In January 2026, Hyundai announced plans to use VR simulators in vehicle development, enabling immersive human–machine interaction testing, virtual ergonomics validation, and simulation-driven evaluation of ADAS, interiors, and driving dynamics.

Autonomous mobility and technology companies represent the fastest-growing end-user segment, expanding at a 16.9% CAGR over the forecast period. Growth is driven by heavy investment in virtual scenario testing, AI model training, and large-scale validation of autonomous systems.

Automotive Simulation Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Simulation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the largest share in 2025 and is the fastest-growing region, driven by large-scale vehicle production in India, China, Japan, and South Korea. Rapid electrification, rising adoption of ADAS, and strong government support for EVs are accelerating simulation adoption. OEMs increasingly rely on virtual validation to manage cost pressures, shorten development cycles, and comply with evolving safety and emission regulations. Growing investments in autonomous driving, software-defined vehicles, and local engineering capabilities further strengthen regional market growth momentum.

- According to the IEA, China accounted for nearly 60% of global new electric car registrations in 2023, with electric vehicles exceeding 35% of domestic car sales, up from 29% in 2022 and surpassing the national 2025 NEV adoption target ahead of schedule.

China Automotive Simulation Market

The Chinese market in 2026 is estimated at around USD 4.20 billion, accounting for roughly 31.1% of global automotive simulation revenues, driven by EV scale-up, ADAS penetration, and strong government-backed digital engineering initiatives.

Japan Automotive Simulation Market

The Japan market in 2026 is estimated at around USD 1.07 billion, accounting for roughly 7.9% of global automotive simulation revenues, supported by advanced OEM R&D, powertrain innovation, and a strong focus on safety validation.

India Automotive Simulation Market

The Indian market in 2026 is estimated at around USD 0.80 billion, accounting for roughly 5.9% of global automotive simulation revenues, driven by rapid EV adoption, localization of engineering, and cost-focused virtual development strategies.

Europe

Europe represents the second-largest market, expanding at a CAGR of 12.5% over the forecast period. Stringent emission standards, advanced safety mandates, and the strong presence of premium OEMs drive widespread adoption of simulation. European automakers leverage simulation for electrification, light weighting, NVH optimization, and autonomous system validation. Continuous R&D investments, digital twin deployment, and collaboration with leading simulation software providers support steady regional growth despite economic uncertainties.

- In January 2026, RFpro in the U.K. launched an autonomous vehicle simulator enabling RF propagation modeling, sensor-level validation, and virtual drive testing to improve the accuracy of ADAS and autonomous system development and verification.

Germany Automotive Simulation Market

The German market in 2026 is estimated at around USD 0.73 billion, accounting for roughly 5.4% of global automotive simulation revenues, supported by premium OEMs, stringent regulations, electrification programs, and digital twin deployments.

U.K. Automotive Simulation Market

The U.K. market in 2026 is estimated at around USD 0.16 billion, accounting for roughly 1.2% of global automotive simulation revenues, driven by autonomous testing programs, motorsport-led engineering expertise, and software-centric vehicle development.

North America

North America held the third-largest share in 2025, supported by strong R&D infrastructure, high technology adoption, and leadership in autonomous and connected vehicle development. OEMs and technology companies extensively use simulation for ADAS validation, AI training, and powertrain optimization. Growing investments in software-defined vehicles, electric mobility, and cloud-based simulation platforms continue to drive demand across the U.S. and Canada.

- In January 2026, Stratasys enabled Subaru to cut tooling development time by more than 50% using a T25 high-speed head for the F770 printer, accelerating rapid prototyping, fixture simulation, and manufacturing validation workflows globally.

U.S. Automotive Simulation Market

The U.S. market in 2026 is estimated at around USD 1.86 billion, accounting for roughly 13.7% of global automotive simulation revenues, fueled by autonomous mobility innovation, AI-driven simulation, and strong cloud-based R&D ecosystems.

Rest of the World

The rest of the world shows steady market growth, driven by gradual automotive digitalization in Latin America, the Middle East, and Africa. Expanding vehicle assembly operations, increased regulatory alignment, and rising adoption of simulation to reduce development costs support demand. Growing interest in EVs, localized engineering capabilities, and partnerships with global simulation vendors further contribute to long-term regional market development.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Simulation Platforms, AI Integration, and Ecosystem Partnerships Define Competitive Intensity

The market is moderately consolidated, dominated by global software and engineering solution providers with strong R&D capabilities. Key players such as ANSYS, Siemens, Dassault Systèmes, Altair, MathWorks, PTC, and Autodesk compete through multiphysics simulation platforms, digital twin technologies, AI-enabled solvers, and cloud-based delivery models. Companies focus on expanding end-to-end capabilities, integrating AI and data analytics, and strengthening industry partnerships. Strategic acquisitions, cloud alliances, and sector-specific solutions help vendors address growing electrification, ADAS, and autonomous vehicle simulation requirements worldwide.

- In March 2025, VI-grade launched a next-generation real-time simulation platform with AutoHawk Extreme, enabling high-fidelity vehicle dynamics, hardware-in-the-loop testing, and accelerated virtual validation for ADAS and autonomous vehicle development.

LIST OF KEY AUTOMOTIVE SIMULATION COMPANIES PROFILED

- ANSYS (U.S.)

- Siemens Digital Industries Software (Germany)

- Dassault Systèmes (France)

- Altair Engineering (U.S.)

- MathWorks (U.S.)

- PTC (U.S.)

- Autodesk (U.S.)

- MSC Software (Hexagon AB) (Sweden)

- ETAS (Robert Bosch GmbH) (Germany)

- dSPACE (Germany)

- IPG Automotive (Germany)

- AVL List GmbH (Austria)

- ESI Group (France)

- Vector Informatik (Germany)

- Synopsys (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Mobileye announced plans to acquire Mentee Robotics, integrating physical AI, vision-based autonomy, simulation-trained models, and embodied intelligence to accelerate autonomous driving technologies and robotic decision-making capabilities.

- January 2026: Omega Simulation launched OMEGALAND v4, a dynamic digital twin platform that enables real-time physics simulation, IoT data ingestion, AI analytics, and lifecycle optimization for complex automotive systems globally.

- October 2025: Sumitomo Riko leveraged ANSYS AI technology to accelerate automotive component simulation over tenfold, enabling faster design optimization, materials modeling, and manufacturing process validation with reduced development cycles.

- March 2025: NVIDIA highlighted its automotive ecosystem for physical AI, combining simulation-trained foundation models, Omniverse-based digital twins, and accelerated computing to enable safe development of autonomous and intelligent vehicle systems.

- March 2025: ANSYS showcased advanced simulation solutions at CES, including AI-enhanced solvers, digital twins, and cloud-based multiphysics platforms that support electrification, ADAS validation, and software-defined vehicle development.

- February 2025: ESI Group launched BM-Stamp, advancing predictive automotive stamping simulation with physics-based forming analysis, material behavior modeling, and digital twin workflows to reduce tooling iterations and manufacturing defects.

- July 2024: Luminar launched Sentinel software for automakers, integrating lidar perception, proactive safety logic, and simulation-based validation to support highway autonomy, collision avoidance, and scalable deployment across vehicle platforms.

- April 2024: Applied Intuition and Luminar partnered to accelerate ADAS development by integrating lidar hardware, perception software, and simulation-driven validation to improve sensor fusion accuracy and autonomous driving safety.

- January 2024: Stellantis launched a virtual development tool to accelerate automotive software creation, leveraging cloud-based simulation, software-in-the-loop testing, and continuous integration to speed validation of software-defined vehicle architectures.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.4% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Application, By Vehicle Type, By Vehicle Autonomy Level, By Offering, By Propulsion, By Simulation Type, By End User, and By Region |

|

By Vehicle Type |

· Passenger Cars · Commercial Vehicles |

|

By Application |

· Powertrain & Electrification Simulation · ADAS & Autonomous Driving Simulation · Vehicle Dynamics & Handling · Safety & Crash & Structural Simulation · Thermal & NVH & Aerodynamics Simulation |

|

By Vehicle Autonomy Level |

· Non-Autonomous/Conventional Vehicles · Semi-Autonomous Vehicles (ADAS, Level 1–2) · Highly Autonomous Vehicles (Level 3 & Above) |

|

By Offering |

· Simulation Software & Licenses · Simulation Platforms & Integrated Tools · Cloud-based Simulation Solutions · AI-enabled Simulation & Digital Twin Solutions · Engineering & Consulting & Support Services |

|

By Propulsion |

· ICE · Electric |

|

By Simulation Type |

· Model-in-the-Loop (MiL) · Software-in-the-Loop (SiL) · Hardware-in-the-Loop (HiL) · System-Level Simulation · Full Vehicle/Virtual Prototyping |

|

By End User |

· Automotive OEMs · Tier-1 Suppliers · Engineering & Simulation Service Providers · Autonomous Mobility & Technology Companies · Research Institutes & Academia |

|

By Region |

· North America (By Application, By Vehicle Type, By Vehicle Autonomy Level, By Offering, By Propulsion, By Simulation Type, By End User, and By Country) o U.S. o Canada o Mexico · Europe (By Application, By Vehicle Type, By Vehicle Autonomy Level, By Offering, By Propulsion, By Simulation Type, By End User, and By Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Application, By Vehicle Type, By Vehicle Autonomy Level, By Offering, By Propulsion, By Simulation Type, By End User, and By Country) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World (By Application, By Vehicle Type, By Vehicle Autonomy Level, By Offering, By Propulsion, By Simulation Type, and By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 11.84 billion in 2025 and is projected to reach USD 39.59 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 6.20 billion.

The market is expected to exhibit a CAGR of 14.4% during the forecast period of 2026-2034.

The passenger cars segment leads the market in terms of vehicle type.

Increasing vehicle complexity to boost market expansion.

Key players in the market include ANSYS, Siemens, Dassault Systèmes, Altair, MathWorks, PTC, and Autodesk, among others.

Asia Pacific held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us