Automotive Torsion Beam Market Size, Share & Industry Analysis, By Beam Type (Conventional Torsion Beam and Coupled Torsion Beam (CTBA)), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By Sales Channel (OEM/Factory-Fit and Aftermarket/Replacement), By Material Type (Stamped Steel, High-Strength Steel (HSS/AHSS), and Composite/Hybrid Materials), and Regional Forecast, 2026-2034

Automotive Torsion Beam Market Size and Future Outlook

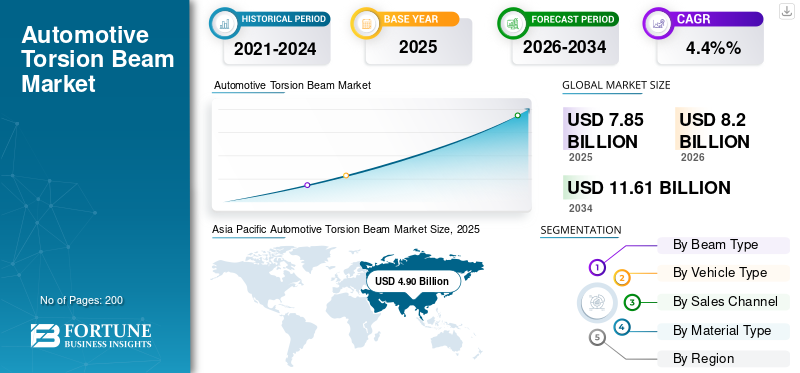

The global automotive torsion beam market size was valued at USD 7.85 billion in 2025. The market is projected to grow from USD 8.20 billion in 2026 to USD 11.61 billion by 2034, exhibiting a CAGR of 4.4% during the forecast period. Asia Pacific dominated the global automotive torsion beam market with a market share of 62.42% in 2025.

Market growth is steadily driven by the high-volume production of compact passenger cars and cost-optimized SUVs, where torsion beams remain a preferred rear-suspension architecture due to their low cost, packaging efficiency, and durability. OEMs are also upgrading designs to improve ride/handling and meet lightweighting targets by increasing the adoption of Coupled Torsion Beam Axles (CTBA) and HSS/AHSS materials, particularly as electrified platforms demand tighter space management and increased stiffness. Tier-1 chassis suppliers, such as Benteler, Gestamp, and Donghee, are expanding their capabilities in twist-beam/CTBA components.

- For instance, in June 2025, BENTELER began construction of a new manufacturing plant in Kenitra, Morocco, where production will include twist beam rear axles (torsion beams) alongside other chassis components supporting new supply capacity and localized delivery for OEM programs.

Download Free sample to learn more about this report.

AUTOMOTIVE TORSION BEAM MARKET Key Takeaways

- 2025 Market Size: USD 7.85 billion

- 2026 Market Size: USD 8.20 billion

- 2034 Forecast Market Size: USD 11.61 billion

- CAGR: 4.4% from 2026–2034

- Asia Pacific dominated the automotive torsion beam market with a 62.42% share in 2025.

- The Coupled Torsion Beam (CTBA) segment is projected to rise at the highest CAGR of 8.4% over the forecast period.

- The aftermarket/replacement segment is projected to grow at a CAGR of 6.1% over the forecast period.

Asia Pacific

The region accounted for the largest market share and remains the fastest-growing regional market, supported by high vehicle production, rising demand for affordable passenger cars and compact SUVs, and electrification-ready platforms.

North America

The market is witnessing steady growth due to strong SUV and light truck production, expanding vehicle exports, supplier localization, and continued demand for cost-efficient rear suspension systems in entry-level vehicles.

Europe

Demand remains strong as automakers continue to adopt lightweight and cost-effective torsion beam systems for compact passenger vehicles, supported by emissions regulations and high production of mass-market models.

U.S.

High SUV penetration, OEM platform optimization, and stable aftermarket demand continue to support moderate and consistent growth in the automotive torsion beam market.

Japan

Demand is supported by the country's strong production of compact and kei vehicles, where torsion beam systems offer space efficiency, reliability, and cost-effective suspension performance.

Read More

AUTOMOTIVE TORSION BEAM MARKET TRENDS

Shift Toward Cost-Optimized and Space-Efficient Rear Suspension Architectures Shapes Product Evolution

Automotive manufacturers are increasingly prioritizing advanced suspension technology systems that strike a balance between cost efficiency, packaging simplicity, and acceptable ride comfort and handling, particularly in high-volume vehicle segments. Torsion beam suspensions continue to gain preference in compact cars and entry-level SUVs as they reduce component count, free up underfloor space, and simplify manufacturing. This trend is further reinforced by electrification, where the placement of batteries and rear packaging efficiency are critical. OEMs are therefore refining torsion beam designs through better geometry, tuning, and material optimization to extend their applicability across a wider range of vehicle platforms without moving to more expensive multi-link systems. In June 2025, BENTELER announced a capacity expansion for twist-beam rear axle production at its new Kenitra facility, designed to support the development of compact and electric vehicle platforms.

MARKET DYNAMICS

MARKET DRIVERS

High Global Production of Compact Passenger Cars and Affordable SUVs Sustains Market Expansion

Sustained demand for affordable mobility across emerging and developed markets continues to drive the production of hatchbacks, sedans, and compact SUVs, directly supporting the adoption of torsion beam technology. These vehicle categories favor torsion beams due to their lower cost, durability, and ease of integration into front-wheel-drive architectures. As automakers strive to maintain competitive pricing while meeting safety, improved fuel efficiency, and efficiency standards, torsion beams remain a proven solution for mass-market platforms. High production volumes in Asia Pacific, parts of Europe, and export-oriented manufacturing hubs further amplify this effect, ensuring consistent OEM demand for torsion beam assemblies and related components. In March 2024, OICA reported that Asia-Oceania remained the largest global vehicle-producing region, reinforcing demand for cost-efficient suspension architectures.

MARKET RESTRAINTS

Increasing Adoption of Multi-Link Suspensions in Premium Segments Limits Addressable Scope

While torsion beams dominate cost-sensitive vehicle segments, their adoption is constrained in premium and performance-oriented models where ride comfort and independent wheel control are prioritized. Multi-link rear suspensions are increasingly standard in higher-end sedans, premium SUVs, and performance vehicles, thereby limiting the penetration of torsion beam suspensions as OEMs move upmarket. This structural shift limits the use of torsion beam technology to specific price bands and vehicle dynamics, as well as architectures, thereby reducing its relevance in luxury segments. As consumer preferences and expectations rise for comfort and enhanced vehicle performance, torsion beams face natural limitations despite continuous incremental improvements. This is hindering the automotive torsion beam market growth. In September 2023, multiple European OEMs confirmed expanded use of multi-link rear suspensions across new premium compact and mid-size vehicle platforms.

MARKET OPPORTUNITIES

Lightweight Materials and Coupled Torsion Beam Designs Create New Value-Growth Potential

Opportunities are emerging through the integration of high-strength steel, advanced high-strength steel, and hybrid material solutions into torsion beam designs. These innovations enable weight reduction, improved stiffness, and better handling characteristics, making torsion beams viable for a broader range of vehicles, including electric and export-oriented models. Coupled torsion beam axles (CTBA) further enhance ride and roll behavior while retaining cost advantages over multi-link systems. This evolution enables suppliers to increase the value per unit, supporting the relevance of torsion beam technology amid tightening emission regulations and efficiency targets. In April 2025, Gestamp highlighted increased use of AHSS in rear axle and torsion beam structures to support lightweight vehicle platforms.

MARKET CHALLENGES

Balancing Cost Pressures with Performance Expectations Remains a Structural Challenge

The primary challenge for the torsion beam market lies in balancing aggressive cost targets with rising OEM expectations for comfort, noise isolation, and dynamic performance. As vehicles become heavier due to the addition of safety features and electrification, and efficient driving experience, torsion beam systems must deliver higher stiffness and durability without incurring significant cost increases. Additionally, material price volatility and pressure on Tier-1 suppliers’ margins complicate long-term planning and investment. Failure to meet evolving performance benchmarks may accelerate the substitution of alternative suspension systems in borderline segments, thereby limiting the adoption of torsion beam systems beyond core applications. In November 2024, several automotive suppliers cited steel price volatility as a key factor impacting chassis component cost planning and margin stability.

Download Free sample to learn more about this report.

Segmentation Analysis

By Beam Type

Cost-Optimized Suspension Architecture Sustains Conventional Torsion Beam Dominance

Based on beam type, the market is segmented into conventional torsion beam and coupled torsion beam (CTBA).

The conventional torsion beam segment dominates the global market due to its low manufacturing cost, structural simplicity, and proven durability across high-volume passenger vehicles. OEMs continue to favor this design in hatchbacks, sedans, and entry-level SUVs, where cost control and packaging efficiency are critical. Large-scale adoption across the Asia Pacific and Europe further reinforces volume leadership. Continuous incremental improvements in geometry and tuning enable conventional torsion beams to meet mainstream ride and safety requirements without necessitating a transition to more costly suspension architectures. In March 2024, multiple Asian and European OEMs reaffirmed continued use of conventional torsion beam rear axles in mass-market compact vehicle platforms.

The Coupled Torsion Beam (CTBA) segment is projected to rise at the highest CAGR of 8.4% over the forecast period.

By Vehicle Type

High Production of Compact Passenger Cars Anchors Hatchback and Sedan Segment

Based on vehicle type, the market is segmented into hatchback/sedan, SUV, LCV, and HCV.

Hatchbacks and sedans dominate the market due to their large global production volumes and strong preference for cost-efficient rear suspension layouts. These passenger cars and commercial vehicles prioritize interior space optimization, low curb weight, and affordable pricing, all of which favor the adoption of torsion beam technology. The segment’s dominance is particularly strong in Asia Pacific and Europe, where compact cars remain central to urban mobility and export-oriented manufacturing strategies. In February 2024, OICA data confirmed that compact passenger cars accounted for the majority of vehicle production in the Asia-Pacific region, supporting demand for torsion beam technology.

The SUV segment is projected to grow at a CAGR of 6.2% over the forecast period.

By Sales Channel

OEM/Factory-fit Integration Strengthens Factory-Fit Channel Supremacy

Based on sales channel, the market is segmented into OEM/factory-fit and aftermarket/replacement.

The OEM/factory-fit segment dominates the global automotive torsion beam market share, driven by the direct integration of torsion beams into new vehicle platforms and long-term supply contracts between automakers and suspension suppliers. Most torsion beams are installed during vehicle assembly, closely tied to production volumes and platform architecture decisions. Standardization across global vehicle programs further strengthens OEM dominance, while economies of scale support consistent sourcing from Tier-1 suppliers.

In July 2024, several global OEMs expanded long-term chassis supply agreements to secure factory-fit rear axle components for upcoming compact vehicle platforms.

The aftermarket/replacement segment is projected to grow at a CAGR of 6.1% over the forecast period.

By Material Type

Established Manufacturing Economics Reinforce Stamped Steel Leadership

Based on material type, the market is segmented into stamped steel, high-strength steel (HSS/AHSS), and composite/ hybrid materials.

Stamped steel remains the dominating material segment due to its cost efficiency, high durability, and well-established global supply chain. OEMs and Tier-1 suppliers rely on stamped steel torsion beams for large-scale production, especially in cost-sensitive passenger cars and light SUVs. The material offers predictable performance, ease of welding, and compatibility with existing manufacturing infrastructure, making it the preferred choice for high-volume platforms where affordability and reliability take precedence over aggressive light-weighting objectives.

In October 2023, leading chassis suppliers highlighted continued reliance on stamped steel for high-volume torsion beam programs supporting global compact vehicle platforms.

The composite/hybrid materials segment is projected to grow at a CAGR of 10.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

AUTOMOTIVE TORSION BEAM MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific is the largest and fastest-growing region for automotive torsion beams, driven by massive vehicle production volumes and strong demand for affordable passenger cars and compact SUVs. Cost sensitivity, urbanization, and expanding middle-class mobility favor torsion beam architectures across multiple countries. OEMs focus on localization, electrification-compatible designs, and scalable platforms, further accelerating adoption and making the region the global growth engine for torsion beam systems.

Asia Pacific Automotive Torsion Beam Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

China Automotive Torsion Beam Market

China dominates regional demand due to its vast production base and strong output of compact SUVs. OEMs favor torsion beams for cost control, while the adoption of CTBA improves ride quality.

Japan Automotive Torsion Beam Market

Japan’s market emphasizes compact and kei vehicles, where torsion beams align with the requirements of space efficiency and reliability. Gradual SUV growth supports incremental demand without major architecture shifts.

India Automotive Torsion Beam Market

India shows strong growth driven by rising hatchback and compact SUV production. Cost-efficient vehicle suspension systems remain critical, making torsion beams highly attractive for volume-driven platforms.

North America

North America’s market is growing steadily, driven by strong SUV and light truck production, as well as increasing vehicle exports, particularly from Mexico. While multi-link suspensions dominate premium segments, torsion beams remain relevant in entry-level SUVs and compact cars. OEM investments in flexible manufacturing, combined with stable demand for cost-optimized rear axles, support consistent growth. The region also benefits from supplier localization strategies and long-term OEM sourcing agreements.

U.S. Automotive Torsion Beam Market

The U.S. market is characterized by high SUV penetration and the selective use of torsion beam suspension in cost-focused trim levels. OEM platform rationalization and steady aftermarket demand support moderate but stable market growth.

Europe

Europe continues to represent a significant market for torsion beam systems, driven by the high production of compact hatchbacks and sedans, particularly in urban-focused mobility segments. OEMs emphasize cost control, weight reduction, and packaging efficiency, thereby sustaining the adoption of torsion beam technology in mass-market vehicles. While premium models are increasingly equipped with multi-link suspensions, volume-driven platforms continue to maintain increasing demand. Regulatory pressure on emissions further supports the use of lightweight torsion beam designs, particularly those made from advanced steels.

U.K. Automotive Torsion Beam Market

The U.K. market benefits from compact car production and export-oriented assembly. Torsion beams remain common in affordable passenger vehicles, supporting stable OEM demand despite overall production volatility.

Germany Automotive Torsion Beam Market

Germany’s market is anchored by high-volume compact models alongside premium vehicles. While luxury segments limit the use of torsion beam, mass-market platforms and export production sustain steady demand.

Rest of the World

The Rest of the World, encompassing South America, the Middle East & Africa, is experiencing moderate growth as local vehicle assembly expands. Cost sensitivity, durability requirements, and simpler vehicle architectures favor the adoption of torsion beam designs. The increasing localization of production and improved road infrastructure support demand, while the gradual growth of SUV penetration enhances market value, despite smaller overall volumes compared to major regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Platform Standardization, Lightweight Engineering, and Supplier Scale Shape Torsion Beam Competitiveness

The global automotive torsion beam market trends are driven by cost optimization, platform standardization, and continuous innovation in materials and design across high-volume vehicle segments. Leading suppliers, including BENTELER, Gestamp, Magna International, ZF, Hyundai Mobis, and American Axle & Manufacturing, compete through scalable torsion beam and CTBA architectures, advanced forming technologies, such as advanced driver assistance systems ADAS and the integration of high-strength steel. Global manufacturing footprints, localized production near OEM plants, and long-term platform supply contracts reinforce competitive strength. Companies focus on improving ride performance through coupled torsion beam designs, reducing weight via AHSS and hybrid solutions, and enhancing durability for electrified platforms. Strategic investments in automation, regional capacity expansion, and close OEM collaboration enable suppliers to balance aggressive cost targets with evolving performance, safety, and efficiency requirements across global vehicle programs.

LIST OF KEY AUTOMOTIVE TORSION BEAM COMPANIES PROFILED

- ZF Friedrichshafen AG (Germany)

- Schaeffler Group (Germany)

- Benteler International AG (Austria)

- Magna International Inc. (Canada)

- American Axle & Manufacturing Holdings, Inc. (AAM) (U.S.)

- Hyundai Mobis (South Korea)

- Gestamp Automoción S.A. (Spain)

- Marelli Holdings Co., Ltd. (Japan)

- JTEKT Corporation (Japan)

- Thyssenkrupp Automotive Technology (Germany)

- Multimatic Inc. (Canada)

- Sogefi S.p.A. (Italy)

- Tata AutoComp Systems Ltd. (India)

- Mubea – Muhr und Bender KG (Germany)

- Yorozu Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- In November 2025, Perodua’s upcoming EV display coverage reported that the model features a rear torsion beam layout, along with a battery package and compact platform proportions. The disclosure is notable as it indicates continued OEM preference for torsion beams in value-focused electrified vehicles where packaging efficiency, manufacturability, and durability are prioritized for mass adoption in emerging-market mobility.

- In September 2025, ZF Chassis Systems Duncan announced an expansion into a new large facility in Spartanburg County, South Carolina, to scale production of precision axle assemblies. The move signals continued investment in the axle-module manufacturing footprint and higher output capacity, which supports OEM demand for standardized rear-axle architectures and localized chassis supply.

- In June 2025, BENTELER officially broke ground on a new automotive components plant in Kenitra, Morocco, positioning the site to manufacture chassis parts, including twist-beam (torsion beam) rear axles for a major OEM. The project strengthens localized supply capability, cost competitiveness, and export-ready production of rear axle assemblies for high-volume vehicle programs.

- In October 2024, the Slovak government and Hyundai Mobis signed an MoU to build a new EV parts plant in Novaky, Slovakia, backed by incentives. While focused on EV components, the investment strengthens Hyundai Mobis’ European manufacturing base for chassis-related modules and supports localization strategies for future vehicle platforms.

- In September 2024, SAIC-GM-Wuling’s Bingo SUV specifications were highlighted to include a hydroformed closed torsion beam rear suspension, as reported in connection with its market rollout. The configuration illustrates how OEMs maintain the attractiveness of torsion-beam architectures for electric vehicles EVs and compact SUVs by utilizing forming techniques that enhance stiffness and packaging while preserving cost efficiency compared to multi-link systems.

REPORT COVERAGE

The global automotive torsion beam market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It contains details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The automotive torsion beam market forecast offers a comprehensive competitive landscape, encompassing the largest market share, emerging opportunities, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAIS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.4% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Beam Type, By Vehicle Type, By Sales Channel, By Material Type, and By Region |

| By Beam Type |

|

| By Vehicle Type |

|

| By Sales Channel |

|

| By Material Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.85 billion in 2025 and is projected to reach USD 11.61 billion by 2034.

In 2025, the market value stood at USD 4.90 billion.

The market is expected to grow at a CAGR of 4.4% during the forecast period of 2026-2034.

The OEM/Factory-Fit segment leads the market in terms of sales channel.

High global production of compact passenger cars and affordable SUVs sustains market expansion.

Top players in the market include ZF Friedrichshafen AG, Schaeffler Group, Benteler International AG, Magna International Inc., and American Axle & Manufacturing Holdings, Inc

Asia Pacific accounted for the largest share of the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us