Automotive Wiper Market Size, Share & Industry Analysis, By Blade Type (Conventional Wiper Blades, Flat Wiper Blades, and Hybrid Wiper Blades), By Material (Rubber, Silicon, and Other Composites), By Vehicle Type (Hatchback/Sedan, SUV, LCV, and HCV), By Sales Channel (Aftermarket and OEM), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

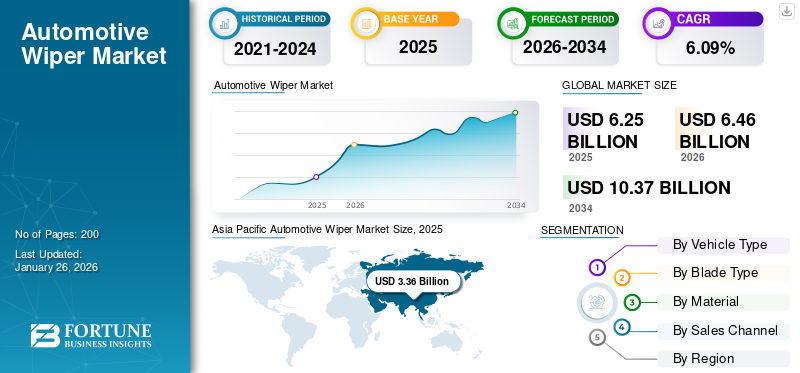

The global automotive wiper market size was valued at USD 6.25 billion in 2025. The market is projected to grow from USD 6.46 billion in 2026 to USD 10.37 billion by 2034, exhibiting a CAGR of 6.09% during the forecast period. Asia Pacific dominated the automotive wiper market with a market share of 53.75% in 2025.

Automotive wipers, or windshield wipers, are essential safety devices installed on vehicles to clear rain, snow, dust, and debris from windshields, ensuring optimal visibility for drivers. They consist of a metal arm with a rubber blade that moves across the glass surface, powered by an electric motor or, in some cases, pneumatic systems. Modern advancements include rain-sensing wipers, heated blades for icy conditions, and aerodynamic designs for reduced noise. Wipers are mandatory in most jurisdictions due to their critical role in road safety, and they are found in cars, trucks, buses, and even some aircraft and watercraft.

Increasing vehicle production, stringent safety regulations, and technological advancements such as smart wipers with automatic rain sensors drive the global market. Key players namely Robert Bosch GmbH, Denso Corporation, Valeo SA, and HELLA GmbH & Co. KGaA, dominates the industry through innovation in durable materials and energy-efficient designs. The aftermarket segment is significant due to frequent wiper replacements, while OEM demand remains steady with new vehicle production. Emerging markets in Asia Pacific are major growth contributors due to rising automobile sales.

The COVID-19 pandemic initially disrupted the automotive wiper market due to factory shutdowns, supply chain delays, and reduced vehicle production. However, the aftermarket segment witnessed resilience as consumers prioritized maintenance for existing vehicles. Post-pandemic, the market rebounded with increased emphasis on vehicle safety and hygiene, accelerating demand for advanced wiper systems. The shift toward personal mobility over public transport also boosted passenger car sales, indirectly supporting wiper demand. Additionally, manufacturers adopted contactless features including automatic sensors, aligning with heightened consumer focus on convenience and safety in the new norm.

Download Free sample to learn more about this report.

Automotive Wiper Market Trends

Integration of Smart and Rain-Sensing Wiper Technologies

The global automotive wiper market trend is the rapid adoption of smart and rain-sensing wiper systems, driven by advancements in sensor technology and the growing demand for enhanced driver safety and convenience. These systems use optical or infrared sensors to detect moisture on the windshield and automatically activate wipers, adjusting speed based on rainfall intensity. This eliminates manual adjustments, improving visibility while reducing driver distraction, a critical factor as Advanced Driver-Assistance Systems (ADAS) and autonomous driving technologies gain traction.

Leading suppliers such as Bosch, Valeo, and Denso are pioneering innovations in this space. For instance, Bosch’s Rain Light Sensor integrates rain detection with ambient light sensing, enabling automatic headlight activation alongside wiper control. Similarly, Valeo’s latest Gen3 rain-sensing wipers leverage AI to predict wiping needs based on weather patterns, enhancing efficiency. Tesla has also contributed to this trend with its electromagnetic wiper system, patented in 2021, which uses a single-blade design for improved aerodynamics and energy efficiency critical for electric vehicles (EVs).

The shift toward connected and autonomous vehicles further accelerates this trend. For example, BMW and Mercedes-Benz now embed rain-sensing wipers as standard in premium models, while mid-range automakers such as Hyundai and Toyota are adopting them in mass-market vehicles. Additionally, aftermarket upgrades are gaining popularity, with brands such as Rain-X and ACDelco offering retrofit kits for older vehicles. This trend aligns with broader automotive priorities safety, automation, and sustainability as smart wipers reduce energy consumption and extend blade lifespan through optimized usage. With regulatory bodies emphasizing vehicle safety standards, the demand for intelligent wiper systems is expected to grow, particularly in regions with extreme weather conditions.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Increasing Consumer and Regulatory Demand for Sustainability Drive Market Growth

One of the most pivotal driving factors in the market is the growing trend toward sustainability and eco‑design, driven by manufacturers and OEMs responding to consumer demand and stricter environmental goals. Valeo, a major OEM and wiper system innovator, recently introduced the Canopy wiper blade, designed to reduce CO₂ emissions by 61% compared to conventional models by using over 80% renewable/recycled rubber, 15% recycled steel, and 50% recycled plastic in its components, packaged in fully recyclable cardboard.

It is now available across Europe via Speedy garages since May 2024. These eco‑friendly blades are manufactured locally in Issoire, France, which underscores Valeo’s commitment to sustainable production and reduction of carbon footprint. Bosch has focused on eco‑friendly packaging and user convenience with its launch of the XpressFIT PRO 95 % universal wiper at AAPEX November 2024, featuring recyclable, plastic‑free packaging and a “HydroDefense” liquid graphite coating for quieter performance.

Market Restraints

Supply Chain Disruptions and Raw Material Volatility are Restraining Market Growth

A critical restraining factor in the market is the ongoing supply chain disruptions and raw material volatility, which significantly inflate costs and delay production. This concern transcends a minor inconvenience, a persistent bottleneck affecting OEMs, Tier‑1 suppliers, and aftermarket chains. First and foremost, semiconductor shortages have profoundly impacted the production of advanced electronic wiper systems. According to a recent analysis, Tier‑1 suppliers in Germany reported a 34% drop in output in 2022 due to missing MCUs. This resulted in delivery delays of 6–10 months for smart wiper modules used in rain-sensing models. This shortage is particularly acute for mid-range vehicles, as premium EVs often receive prioritized access to scarce chips.

With that, raw material prices, especially synthetic rubber, silicone, and plastics, have been extremely volatile. Around 38% of the production cost stems from these inputs. With prices shifting unpredictably, nearly 44% of small and midsized manufacturers are forced to adjust procurement strategies mid-cycle; 29% of OEMs report delayed operations because materials arrived inconsistently. Aftermarket distribution networks are feeling the strain. These inflated costs erode margins and transfer expenses to end consumers, making premium wipers less accessible.

Market Opportunities

Integration of Wiper Systems with Advanced Sensing Technologies Drive Market Opportunities

One of the most promising opportunities in the market is the convergence of wiper systems with advanced sensing and ADAS technologies, enabling smarter and integrated visibility solutions that enhance safety and convenience. For instance, Valeo has teamed up with Volkswagen Group and Mobileye to develop “Level 2+” driver assistance solutions for future MQB-platform vehicles, featuring a 360° sensor suite including cameras and radar integrated seamlessly into the vehicle’s windshield and positioned to work in tandem with automatic wipers to keep sensors unobstructed.

This integration ensures that wipers are activated proactively to maintain clear sensor functionality, rather than relying solely on driver input, offering increased reliability for ADAS features. Moreover, Bosch is ramping up its ADAS offerings, launching mid-tier systems in China set to enter serial production in mid-2025. These include radar sensors paired with SoC-based processors and multifunction cameras capable of lane-keeping and traffic-aware wiper activation. By embedding wiper control into comprehensive ADAS packages, Bosch enables tiered product lines with enhanced safety at every level.

Valeo’s digital-twin simulation platform, developed with Applied Intuition, aims to refine ADAS sensor performance, including LiDAR and camera systems, across varying weather conditions. This virtual validation allows manufacturers to test and optimize wiper algorithms for clearing rain, snow, or spray, accelerating time-to-market for advanced visibility features. In essence, the fusion of automatic wiper control with sensor-cleaning strategies and ADAS integration offers manufacturers a clear path to differentiate their vehicles, enhance safety, and tap into the growing demand for smarter, sensor-rich mobility solutions.

Segmentation Analysis

By Vehicle Type

Widespread Popularity and Versatility of SUV Makes them Dominate the Market

Based on vehicle type, the market is segmented into hatchback/sedan, SUV, LCV, and HCV.

SUVs claim the dominating and fastest automotive wiper market growth in the vehicle category. Global consumer preference has shifted decisively toward crossovers, prompting OEMs to adopt high-performance wiper systems that match SUV design and functionality. In April 2024, Trico launched a dedicated hybrid wiper series optimized for SUVs and EVs, offering enhanced durability, noise reduction, and improved airflow integration. Bosch also integrated advanced rain-sensing blades with automatic adjustment functions into myriad premium SUVs as recorded in September 2023, showcasing OEM confidence in this segment. SUVs demand larger wipers, more powerful motors, and aerodynamic beam or hybrid blades—factors that support greater ASP and frequent upgrades. The SUV segment is projected to dominate the market with a share of 39.47% in 2026.

Hatchbacks and sedans are the second most dominant in the global wiper market due to their overwhelming production volumes. In 2023, they accounted for approximately 60% of overall wiper blade sales, driven by high production rates, well-established distribution networks, and consistent demand for routine maintenance components including wipers. OEMs typically equip such models with standard conventional or beam blades, and the aftermarket ecosystem remains robust with frequent 6-12‑month replacement cycles. Bosch and Valeo continue to support this dominance through mass-market product lines covering the entire hatchback/sedan fleet.

Light commercial vehicles (vans, pickups) and heavy commercial vehicles (trucks, buses) represent smaller market shares due to lower unit volumes. Still, both segments demand rugged, heavy-duty wiper systems built to excel in harsh environments and extended service intervals. OEMs typically deploy conventional or reinforced hybrid blades in these vehicles, but despite sector-specific reliability requirements, their overall market share remains trailing behind passenger vehicles.

By Blade Type

Conventional Wiper Blades Segment Led the Market Due to Widespread Use in Budget and Mid-Range Vehicles

Based on blade type, the market is classified as conventional wiper blades, flat wiper blades, and hybrid wiper blades.

The conventional wiper blades segment dominates the market, accounting for over maximum global revenue, primarily due to their widespread use in budget and mid-range vehicles. These blades, featuring a metal frame with rubber edges, are cost-effective and easy to replace, making them popular in emerging markets such as India and Southeast Asia. The conventional wiper blades segment is projected to dominate the market with a share of 43.42% in 2026.

However, flat (beam) wiper blades are the fastest-growing segment through 2032. Their aerodynamic design reduces wind lift and noise, making them ideal for luxury and electric vehicles (EVs). For instance, Bosch’s Aerotwin flat blades are now standard in many European premium cars, while Valeo’s beam blades are increasingly adopted in EVs for their low energy consumption.

Hybrid wiper blades, combining the durability of conventional blades with the performance of flat blades, are gaining traction in regions with extreme weather, such as North America and Northern Europe. For example, Denso’s Hybrid Blade series uses a reinforced frame to prevent snow buildup, addressing a key pain point in cold climates. Recent innovations include heated wiper blades for icy conditions, with companies including HELLA introducing models for commercial vehicles.

By Material

Cost-Effectiveness, Flexibility, and Widespread Availability of Rubber Wiper Blades Make It Dominant

Based on material, the market is categorized into rubber, silicon, and other composites.

Rubber dominates the global automotive wiper market share, due to its cost-effectiveness, flexibility, and widespread availability. Traditional rubber blades are preferred in budget and mid-range vehicles, particularly in emerging global markets where affordability is key. The rubber segment is expected to lead the market, contributing 61.69% globally in 2026.

However, silicon-based wiper blades are the fastest-growing segment, driven by their superior durability, resistance to extreme temperatures, and longer lifespan (up to 2-3 times longer than rubber). Silicon blades are increasingly adopted in premium vehicles and electric cars (EVs) due to their ability to maintain performance in harsh conditions. Other composites (e.g., graphite-infused, Teflon-coated) are gaining considerable traction in commercial vehicles and luxury segments. For instance, Bosch’s Aerotwin silicon blades and Denso’s hybrid graphite-coated blades offer reduced friction and noise, aligning with EV manufacturers’ demand for energy-efficient components.

To know how our report can help streamline your business, Speak to Analyst

By Sales Channel

Aftermarket Sales Lead Due to Periodic Recurring Replacements and Availability via Independent Retailers

By sales channel, the market is classified as aftermarket and OEM. Aftermarket channel remains the dominant and fastest-growing force in global wiper sales. This dominance stems from essential, recurring purchase cycles; wiper life typically spans 6–18 months, making replacements via independent retailers, service centers, and fast-fit networks routine. Both Bosch and Valeo have reinforced aftermarket leadership—Bosch launched a high-durability aftermarket wiper line in March 2024, while Valeo expanded its EV-specific wiper motor and control product line in January 2024. Competitive pricing, broad SKU availability, and online retail platforms, especially e-commerce, further entrench aftermarket fast-growth and dominance. The aftermarket segment will account for 65.47% market share in 2026.

While smaller in volume, the OEM channel exhibits a considerable growth rate due to increasingly widespread adoption of high-value features directly at vehicle assembly. OEMs are equipping new models—particularly SUVs and EVs—with enhanced wiper systems featuring rain sensors, aerodynamics-optimized beam blades, and eco-conscious materials. For example, Bosch’s premium wiper systems with integrated rain-sensing and speed-adaptive functionality entered series production in premium OEM models in late 2024.

AUTOMOTIVE WIPER MARKET REGIONAL OUTLOOK

Regionally, the market segmentation is into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Automotive Wiper Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific recorded a market size of USD 3.36 billion in 2025, capturing 53.75% of the global market share, and is projected to reach USD 3.5 billion in 2026. Asia Pacific dominates the global automotive wiper market with the largest share, driven by rapid urbanization, industrial expansion, and rising disposable incomes, leading to increased vehicle ownership. China, Japan, India, and South Korea exhibit high vehicle production and sales rates, creating a large demand for wiper systems. The diverse weather conditions in the region also necessitate the need for cars equipped with advanced wiper systems for optimal visibility and safety. Manufacturers are investing heavily in research and development to create smart wiper systems and are also influenced by government initiatives promoting the automotive industry.

The aftermarket segment is expanding rapidly in Asia Pacific due to rising awareness and frequent blade replacements, driven by tropical and monsoon climates, making it the fastest-growing region. China holds the largest share within the region, followed by Japan, India, and South Korea, each contributing significantly to the market’s growth. The Japan market is forecast to attain USD 0.55 billion by 2026, the China market is poised to reach USD 1.50 billion by 2026, and the India market is set to achieve USD 0.92 billion by 2026.

North America

In 2025, North America generated USD 1.01 billion, contributing 16.08% to global market revenue, and is projected to grow to USD 1.03 billion in 2026. North America represents a mature and technologically advanced market, driven by high vehicle ownership, stringent safety regulations, and a strong presence of major automotive OEMs and aftermarket suppliers. The region, particularly the U.S. and Canada, also experiences varied climatic conditions, from harsh winters requiring specialized blades to heavy rainfall, fueling a consistent demand for high-performance and durable wiper blades. Consumers in this region prioritize quality and reliability, leading to a strong aftermarket segment and the adoption of advanced technologies including rain-sensing and heated wipers.

North America’s market also serves as a testing ground for innovative technologies, influencing global wiper system design trends. The U.S. holds a significant share due to its large automotive industry and vehicle ownership, while Canada shows rapid growth fueled by safety regulations. Mexico’s market is also projected to grow, supported by a strong industrial base and proximity to the U.S. automotive sector. The U.S. market is estimated at USD 0.73 billion by 2026.

Europe

The Europe market accounted for USD 1.26 billion in 2025, representing 20.12% of the global industry, and is expected to reach USD 1.28 billion in 2026. Europe’s growth is characterized by its robust automotive sector, stringent safety regulations, and a growing emphasis on sustainability. Strict European rules and per-household spending on automobiles contribute to the demand for high-quality, efficient, and durable wiper blades. Northern Europe, in particular, demonstrates a faster adoption of advanced technologies, while Southern Europe shows a strong demand for cost-effective solutions. Key players in the European automotive market, for instance, Germany and France, are investing in advanced technologies and sustainable practices, influencing the overall market dynamics. The increasing popularity of electric vehicles in the region further drives demand for lightweight and advanced wiper systems. The UK market is expected to reach USD 0.32 billion by 2026, while the Germany market is anticipated to account for USD 0.40 billion by 2026.

Rest of the World

The Rest of the World market was valued at USD 0.63 billion in 2025, capturing 10.05% of global revenue, and is estimated to reach USD 0.65 billion in 2026. This region encompasses Latin America and the Middle East & and Africa. While representing a smaller share of the overall market than the regions above, it exhibits promising growth prospects fueled by rising urbanization, increasing vehicle sales, and a growing awareness of automotive safety features. Saudi Arabia and Brazil are leading the growth in their respective sub-regions, driven by expanding automotive industries, increasing vehicle imports, and rising consumer awareness about vehicle maintenance. In particular, the Middle East & Africa region presents opportunities as market penetration increases with rising automobile imports and urbanization. There is also a growing interest in advanced wiper technologies, with a rise in demand for beam-style and hybrid wipers among premium vehicle owners.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation, Diverse Product Portfolio, Quality, and Reliability makes Bosch a Leading Player.

Bosch holds the top global position for automotive wiper systems, dominating OEM supply and aftermarket sales due to its unmatched technological edge and scale. With over 50,000 units produced daily and ISO 9001 quality certifications, Bosch leverages nearly a century of engineering expertise to deliver innovative, reliable wiper solutions. Their wiper portfolio includes beam-style blades including the ICON, which use ClearMax 365 rubber for year-round durability, bracketless Clear Advantage, conventional Excel+, and XpressFIT PRO blades featuring HydroDefense for enhanced wiping and long edge life. Bosch also offers integrated mechatronic drives such as EC motors and Jet Wiper systems for optimal fluid delivery, noise reduction, and system weight efficiency.

Valeo stands among major global players, achieving leadership through deep OEM partnerships and premium innovation. Its acquisition of SWF in 1998 bolstered its reach; today, Valeo produces six wiper blades per second and operates 18 wiper plants with 13 R&D centres. Valeo’s product range spans its award‑winning Silencio and Everguard silicone blades. It is recognized for silent operation, hydrophobic performance, and exceptional longevity assets which won top marks in a March 2025 Automotive Insights test. Through its SWF brand, Valeo offers full coverage for front and rear applications in passenger and commercial vehicles, maintaining “premium” positioning with OE-level quality across Europe.

LIST OF KEY AUTOMOTIVE WIPER COMPANIES PROFILED

- Bosch (Germany)

- Valeo (France)

- Denso (Japan)

- Trico Products (U.S.)

- Mitsuba Corporation (Japan)

- HELLA (Germany)

- Kohler (Germany)

- Federal-Mogul (U.S.)

- Clarion Co., Ltd. (Japan)

- Continental AG (Germany)

- Japan Wiper Co., Ltd. (Japan)

- Wiper Blade System (U.S.)

- APF Wipers (India)

- Eiko Corporation (Japan)

- Schaeffler Group (Germany)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Tesla has pioneered and developed a unique approach that exemplifies the company’s software-centric philosophy. Unlike traditional manufacturers who rely primarily on physical rain sensors, Tesla’s system utilizes cameras. Model Y detects precipitation and adjusts wiping speed through its Auto setting, part of the vehicle’s broader autonomous driving capabilities.

- June 2025: Petra Automotive launched its new PetraBlades Premium Beam Wiper Blades. Engineered for superior wiping performance and enhanced durability, these blades are designed to provide optimal visibility, even in the harshest weather conditions. Focused on innovation, ease of installation, and vehicle compatibility, Petra's premium beam wiper blades address the needs of modern drivers, from everyday commuters to those navigating extreme weather.

- April 2025: KIMBLADE innovated KIMBLADE X, the latest features with a multi-joint rectangular blade that eliminates reverse noise. Inspired by vehicle suspension systems, it stays evenly balanced and maintains steady contact with the windshield, resulting in a quieter, longer-lasting, higher-performing wipe.

- January 2024: Almighty Auto Ancillary Pvt. Ltd. showcased its expertise in the automotive wiper system, highlighting its global ascent in the industry. The company manufactures complete windshield wash and wipe systems and precision-machined components for various applications. Almighty Auto offers various wiper systems tailored for vehicles, including passenger cars, trucks, buses, and agricultural machinery. Their products include light to heavy-duty wiper arms, blades, and motors for specific vehicle requirements.

- April 2021: Robert Bosch introduced an enhanced version of its renowned Aerotwin Wiper. This latest iteration boasts a new AeroClip adaptor designed for optimum aerodynamics. The innovative design increases contact pressure between the wiper and the automotive windshield, improving wiping performance even at high speeds. By introducing such advanced wiper technology, German manufacturers prioritize safety and strive for superior driving experiences.

REPORT COVERAGE

The global automotive wiper market report provides detailed analysis and focuses on key aspects such as leading companies, vehicle types, design, and technology. Besides this, the report offers insights into the latest market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market’s growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.09% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Blade Type

By Material

By Vehicle Type

By Sales Channel

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market will reach USD 10.37 billion by 2034 from USD 6.25 billion in 2025.

The market is expected to grow at a CAGR of 6.09% during the forecast period.

Increasing consumer and regulatory demand for sustainability and eco‑design.

Asia Pacific led the market in 2025.

Asia Pacific market size was USD 3.36 billion in 2025.

Bosch, Valeo, and Denso are a few of the major players operating in the global automotive wiper market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us