Autonomous Networks Market Size, Share & Industry Analysis, By Component (Solutions and Services), By Autonomy Level (Level 1 Assisted Operations, Level 2 Partial Automation, Level 3 Conditional Autonomy, and Level 4 High Autonomy), By End User (Telecom Operators, Cloud Providers, Large Enterprises, and Government and Defense), and Regional Forecast, 2026-2034

Autonomous Networks Market Overview

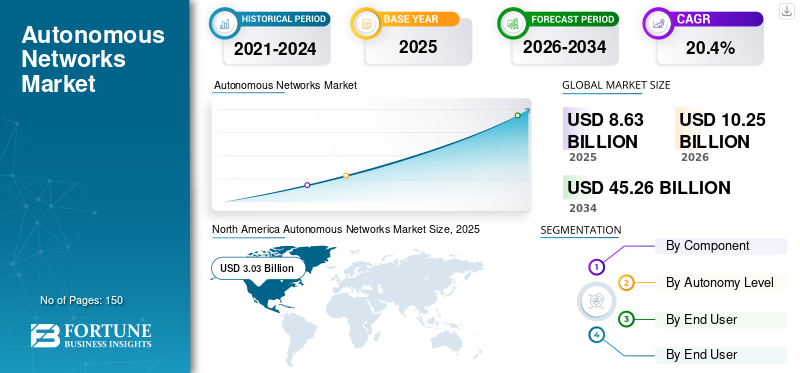

The global autonomous networks market size was valued at USD 8.63 billion in 2025. The market is projected to grow from USD 10.25 billion in 2026 to USD 45.26 billion by 2034, exhibiting a CAGR of 20.4% during the forecast period. North America dominated the autonomous networks market with a market share of 35.11% in 2025.

A communication network that utilizes AI, machine learning, and closed-loop automation to continuously configure, manage, optimize, and repair network operations with little or no human involvement is known as an autonomous network. It is capable of automatically analyzing its own data and making real-time decisions to improve overall performance, reliability, and service delivery across complex infrastructures such as 5G, cloud, and edge. The market growth is driven by the rapid deployment of 5G networks, rising network complexity from cloud and edge computing, increasing telecom operators’ focus on reducing operational costs through automation, and the adoption of AI and machine learning for self-optimizing and self-healing network operations.

Many key market players, such as Huawei Technologies Co., Ltd., Telefonaktiebolaget LM Ericsson, Nokia Corporation, Cisco Systems, Inc., and Juniper Networks, Inc., operating in the market are focusing on integrating artificial intelligence and automation capabilities into their network management and orchestration platforms while forming strategic partnerships with telecom operators and cloud providers to accelerate the deployment of autonomous network solutions.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Gen AI Assists In Increasing Productivity In Operations Support Systems And Assurance, Accelerating Service Rollout

Generative AI creates highly efficient autonomous networks that automate network operations into natural language, agent-driven workflows capable of diagnosing issues, proposing solutions, and executing corrective actions via closed-loop remediation in a fraction of the time compared to traditional ML automation. This increases productivity in Operations Support Systems (OSS) and assurance with the ability for engineers to query telemetry data, generate reports, and produce run books without having to write specialized scripts, thereby reducing time to resolution and accelerating service rollout.

With the introduction of cross-domain coordination capabilities, it is possible to achieve greater autonomy across an entire network from radio access networks (RAN) through core, transport, and security, thus allowing for the movement from level 2 and level 3 to level 4 autonomy. This leads to increased spend on autonomous network software layers (AI ops, orchestration, and assurance) and related integration services to link Generative AI models with telecommunications data, policies, and governance. For instance,

- In February 2025, Nokia announced new Agentic AI capabilities across its autonomous networks portfolio, including an AI-powered threat hunting assistant that claims to reduce threat dwell time from days to minutes, plus GenAI-enabled analytics and an AI studio to speed creation of AI use cases.

AUTONOMOUS NETWORKS MARKET TRENDS

Industry Benchmarking and Certification Frameworks Accelerating Adoption of Autonomous Networks

The telecommunications industry has begun using several benchmarks to assess network autonomy. These include an industry-standard maturity model developed by TM Forum and criteria based on different operational scenarios, instead of relying on vendors' claims. The frameworks and certification processes validate autonomy levels across independently defined, high-value operational scenarios using a common certifying authority. This allows telecommunications service providers to base procurement decisions on validated performance metrics, such as the projection of future energy efficiency, reductions in manual tickets, and faster service activation times.

Additionally, the adoption of standardized frameworks is driving the market toward scalable and repeatable deployment models, ensuring that advancements to higher autonomy levels align with defined requirements for data integration, operational processes, and closed-loop automation. Over time, the certifications for these levels will serve as a form of credit for autonomy maturity when negotiating partnerships, managed service contracts, and product roadmaps.

- For instance, in June 2025, Ericsson and TDC NET announced the first Level 4 autonomy certification under TM Forum’s ANLAV for a live scenario focused on RAN energy efficiency optimization.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of 5G Standalone Networks Driving Demand for Autonomous Network Automation

The growth of autonomous networks is being significantly driven by the rollout of 5G standalone (SA) mobile networks. These 5G SA architectures require a high degree of orchestration, automation, and AI-driven management for the provision and management of complex network use cases, including network slicing, dynamic resource allocation, and ultra-low-latency services. In comparison to traditional non-standalone 5G networks, 5G SA operations involve cloud-native core networks and software-defined networking. As a result, they generate extremely high volumes of telemetry data that can be optimized through AI-driven autonomous operations. As telecom operators continue to scale 5G SA provision of enterprise service, IoT connectivity, and edge computing, manual management practices become increasingly inefficient, thereby driving investment in self-optimizing/self-healing networks.

Moreover, autonomous networks provide real-time fault detection, automated configuration changes, and predictive performance optimization across radio access network (RAN), core network, and transport (backhaul) domains. This supports telecom operators in improving service quality while reducing the complexity and cost of telecom operations. For instance,

- In February 2025, the Global System for Mobile Communications Association (GSMA) reported that global telecom operators are expected to invest about USD 1.3 trillion in mobile network CAPEX between 2024 and 2030, largely driven by 5G rollout and network modernization.

MARKET RESTRAINTS

High Initial Deployment and Integration Costs May Hinder Market Growth

The market faces a significant constraint due to the high upfront cost of deploying and integrating AI-driven automation. As a result, operators must make massive capital investments to implement these technologies, including Artificial Intelligence (AI)-based automations, cloud-based systems, and network orchestration (NO). Transitioning from existing OSS and legacy operational models to fully automated operational environments requires extensive system upgrades, data integration, and multi-supplier interoperability. In addition, telecom network operators must outlay significant expenditures on modernizing networks, creating new edge computing environments, and recruiting specialized AI talent to facilitate autonomous operations. Due to the high cost of implementing these technologies, especially for smaller operators, and limited capital availability, the adoption of an autonomous network may be delayed.

MARKET OPPORTUNITIES

Rising Demand for Edge Computing and Distributed Infrastructure Creating New Opportunities for Market Growth

The increasing need for edge computing and distributed infrastructure will provide significant opportunities for autonomous networks, as edge environments consist of thousands of geographically distributed nodes that need to be continuously monitored, optimized, and configured automatically. With multi-access edge computing (MEC), private 5G networks, and cloud-native cores being deployed closer to end-users, managing these environments manually is no longer feasible for operators.

Autonomous networks facilitate AI-driven orchestration and closed-loop automation to dynamically allocate resources, identify faults, and optimize traffic across multiple distributed edge sites. This capability enhances latency-sensitive services such as autonomous vehicles, industrial IoT, and real-time analytics, while also decreasing operational overheads for telecom operators. As edge infrastructure continues to scale around the world, operators are investing more heavily in autonomous network platforms so that they can provide customers with high-quality services, a consistent level of service quality, and a cost-effective solution to their network requirements. For instance,

- In February 2024, Ericsson partnered with Dell Technologies to develop open cloud RAN and edge infrastructure solutions aimed at simplifying automated network operations and accelerating 5G edge deployments.

Segmentation Analysis

By Component

Rising Deployment of AI-Driven Network Automation Platforms Boosted Solutions Segment Growth

Based on component, the market is bifurcated into solutions and services.

Solutions accounted for the largest market share in 2025 and are expected to grow at the highest CAGR of 22.3% during the forecast period. This growth is driven by increasing investments from telecom operators into artificial intelligence-driven network orchestration, network analytics, and network automation platforms, which enable self-optimizing and self-healing of the networks. The rapid rollout of 5G standalone networks and cloud-native telecom infrastructures has created a surge in demand for more advanced autonomous networking software solutions that incorporate real-time network monitoring, predictive maintenance capabilities, and closed-loop automation features.

Services are anticipated to grow at a prominent CAGR of 16.3% over the forecast period. This growth is propelled by the increasing need for consulting, integration, and managed services to modernize legacy OSS/BSS systems and implement AI-driven autonomous network platforms across multi-vendor and cloud-native environments.

By Autonomy Level

Level 2 Partial Automation Led due to Rising Inclination from Traditional to AI-Driven Network Management Systems

Based on autonomy level, the market is divided into level 1 assisted operations, level 2 partial automation, level 3 conditional autonomy, and level 4 high autonomy.

Level 2 partial automation is anticipated to account for the largest market share as telecom operators continue to transition from traditional to AI-driven network management systems. Therefore, the use of rule-based automated processes combined with human oversight remains the most common deployment model.

Level 4 high autonomy is anticipated to grow at the highest CAGR of 23.9% over the forecast period, owing to increasing adoption of AI-driven closed-loop automation. This enables self-optimizing, self-healing, and predictive network operations across complex 5G and cloud-native infrastructures with minimal human intervention.

By End User

To know how our report can help streamline your business, Speak to Analyst

Expansion of Large-Scale Telecom Network Infrastructure Boosted Telecom Operator Segment Growth

Based on end user, the market is classified into telecom operators, cloud providers, large enterprises, and government and defense.

Telecom operators witnessed a dominating market share in 2025, as they manage massive and dynamic mobile and fixed infrastructure that requires continuous monitoring, optimization, and automation to meet growing customer and traffic demands. Additionally, with the widespread deployment of 5G Standalone networks and increasing cost pressures, telecom operators are looking to use AI-based autonomous network solutions to improve network performance and operational efficiency.

Cloud providers are anticipated to grow at the highest CAGR of 22.8% during the forecast period. This growth is driven by the expansion of hyperscale data centers, edge computing infrastructure, and cloud-native telecom networks, which increase the need for AI-driven automation to effectively manage large-scale, distributed network environments efficiently.

Autonomous Networks Market Regional Outlook

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America Autonomous Networks Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest autonomous networks market share in 2024, valued at USD 2.59 billion, and also maintained its leading position in 2025, with USD 3.03 billion. The market in the region is expected to increase, owing to the early adoption of AI-based network automation technologies and the large-scale rollout of 5G stand-alone networks by major cellular service companies. The presence of many top telecommunications companies, hyperscale cloud worshippers, and large investments in advanced infrastructure for network systems is also helping the country's continued leadership position in the market. For instance,

- In February 2025, AT&T extended its voice core relationship with Nokia, including Nokia Digital Operations software and cloud-native IMS Voice Core upgrades to streamline network activities, enhance automation, and reduce manual intervention.

U.S Autonomous Networks Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market is expected to reach around USD 2.88 billion by 2026, accounting for roughly 28.1% of global sales.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe is projected to record a growth rate of 19.5% in the coming years, which is the second-highest among all regions, and reach a valuation of USD 2.74 billion by 2026. The market in Europe is experiencing steady growth as an increasing number of telecom operators are investing in AI-based automation of networks. This will allow them to effectively operate their complex 5G standalone deployments, as well as cut down on operational costs. Furthermore, a collaborative effort to develop solutions for implementing autonomous networks and intent-based operations will help speed up the rate of adoption throughout Europe. For instance,

- In October 2024, Nokia announced that Deutsche Telekom had adopted its autonomous network software solutions to automate network operations and accelerate the transition toward AI-enabled network management.

U.K Autonomous Networks Market

The U.K. market in 2026 is estimated to reach around USD 0.54 billion, representing roughly 5.3% of global revenues.

Germany Autonomous Networks Market

Germany’s market is projected to reach approximately USD 0.51 billion by 2026, equivalent to around 5.0% of global sales.

Asia Pacific

The Asia Pacific region is estimated to reach USD 2.70 billion in 2026 and is expected to grow at the highest CAGR during the forecast period. This growth is owing to the speedy rollout of 5G standalone networks and substantial investment by telecom companies in artificial intelligence (AI)-driven network automation to address rising network complexity and traffic demand. Additionally, governments & telecom firms throughout China, South Korea & Japan are also supporting infrastructure and operations that rely on intelligent networks and AI, further accelerating the adoption of autonomous network technologies. For instance,

- In October 2025, Ericsson announced that Malaysia’s DNB became the first mobile network validated at Level 4 autonomy for Service Assurance under TM Forum, powered by Ericsson’s AI-enabled intent-based operations.

In the region, India and China are both estimated to reach USD 0.37 billion and USD 0.63 billion, respectively, in 2026.

Japan Autonomous Networks Market

The Japanese market in 2026 is estimated at around USD 0.51 billion, accounting for roughly 5.0% of global revenues. Japan's advanced telecom infrastructure and large investments by telecom operators in AI-based network automation to facilitate the expansion of 5G and future 6G development are key factors driving market growth.

China Autonomous Networks Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.63 billion, representing roughly 6.1% of global sales.

India Autonomous Networks Market

The Indian market in 2026 is estimated at around USD 0.37 billion, accounting for roughly 3.6% of global revenues.

South America

South America is expected to witness moderate growth in this market during the forecast period. The South American market is set to reach a valuation of USD 0.53 billion in 2026. This is owing to increasing investments by telecom operators in network modernization and 5G deployment, which is encouraging the adoption of AI-driven automation to improve network performance and operational efficiency.

Middle East & Africa

The Middle East & Africa is estimated to reach USD 0.72 billion in 2026 and is expected to grow at a prominent growth rate in the coming years. This growth is owing to the rapid deployment of 5G technologies, combined with mass telecom infrastructure investments being made throughout the region’s largest network operators. These investments are being made to create efficiencies and improvements to network services by many of the region's largest telecommunications providers. In the Middle East & Africa, the GCC is set to reach a value of USD 0.22 billion in 2026. For instance,

- In May 2025, Saudi Arabia allocated USD 5 billion for cybersecurity enhancements in the defense sector, part of its Vision 2030 plan, to ensure the protection of aerospace systems and infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Expanding Product Portfolio to Strengthen their Market Position

The global market holds a semi-consolidated market structure, with prominent players such as Huawei Technologies Co., Ltd., Telefonaktiebolaget LM Ericsson, Nokia Corporation, Cisco Systems, Inc., and Juniper Networks, Inc. holding significant positions. These companies are driving the autonomous networks market growth through ongoing strategic initiatives, including integrating artificial intelligence and machine learning into network management platforms, developing intent-based networking solutions, and expanding cloud-native telecom infrastructure. Partnerships with telecom operators, hyperscale cloud providers, and edge infrastructure developers are also playing a critical role in accelerating the deployment of autonomous network technologies, particularly for enabling real-time network optimization, predictive maintenance, and low-latency connectivity services.

Other notable players in the global market include ZTE Corporation, NEC Corporation, Samsung Electronics, Arista Networks, and Ciena Corporation. These companies are increasingly focusing on next-generation autonomous networking technologies, particularly AI-driven network analytics, closed-loop automation platforms, and advanced orchestration solutions. Strategic investments in AI capabilities, open network architectures, and edge computing infrastructure are expected to strengthen their market positioning and expand their global presence throughout the forecast period.

LIST OF KEY AUTONOMOUS NETWORKS COMPANIES PROFILED

- Huawei Technologies Co., Ltd. (China)

- Telefonaktiebolaget LM Ericsson (Sweden)

- Nokia Corporation (Finland)

- Cisco Systems, Inc. (U.S.)

- Juniper Networks, Inc. (U.S.)

- ZTE Corporation (China)

- NEC Corporation (Japan)

- Samsung Electronics (South Korea)

- Arista Networks (U.S.)

- Ciena Corporation(U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Verizon updated its AI strategy announcement for Verizon AI Connect, noting Google Cloud and Meta as early adopters and listing ecosystem partnerships including NVIDIA and Vultr, with collaboration on AI solutions for network maintenance and anomaly detection.

- June 2025: Ericsson launched Ericsson On-Demand (5G core SaaS), built with Google Cloud, “AI at the foundation,” positioning AI-assisted troubleshooting and lifecycle automation to reduce operational overhead.

- June 2025: Nokia launched an autonomous network fabric and highlighted GenAI-enabled, agentic workflows for operations using Google Cloud tools, including Vertex AI to support monitoring, anomaly detection, and zero-touch remediation.

- March 2025: NTT DOCOMO announced initiatives to accelerate AI-driven autonomous network operations to support future 6G development and next-generation intelligent telecom infrastructure.

- February 2025: Ericsson partnered with Singtel (Singapore) to deploy AI-powered network automation technologies that support advanced 5G network management and autonomous network capabilities.

- December 2024: Nokia and Kyndryl expanded their collaboration to deploy private 5G and edge computing solutions for enterprise customers, integrating automation and AI-driven network management capabilities.

- June 2024: Huawei introduced upgrades to its Autonomous Driving Network (ADN) solution to help telecom operators accelerate the transition toward Level 4 autonomous networks and improve network automation capabilities.

REPORT COVERAGE

The global autonomous networks market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 20.4% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Autonomy Level, End User, and Region |

| By Component |

|

| By Autonomy Level |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 8.63 billion in 2025 and is projected to reach USD 45.26 billion by 2034.

In 2025, the market value stood at USD 3.03 billion.

The market is growing at a CAGR of 20.4% during the forecast period (2026-2034).

By end user, the telecom operators segment led the market.

Expansion of 5G standalone networks is the key factor driving the market.

Huawei Technologies Co., Ltd., Telefonaktiebolaget LM Ericsson, Nokia Corporation, Cisco Systems, Inc., and Juniper Networks, Inc. are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us