Autonomous Port Operations Systems Market Size, Share & Industry Analysis, By Port Size (Large International Hub Ports, and Medium and Small Ports), By Deployment Mode (On-Premises, Cloud-Based, and Hybrid Deployment), By Automation Level (Semi-Autonomous Operations, Fully Autonomous Operations, and others), By System Type (Terminal Operating Systems (TOS), Equipment Control Systems (ECS), Autonomous Fleet Management Systems, and Others), By Component (Software Platforms, Hardware & Sensors, Autonomous Equipment, Connectivity Infrastructure, and others), and Regional Forecast, 2026-2034

Autonomous Port Operations Systems Market Size and Future Outlook

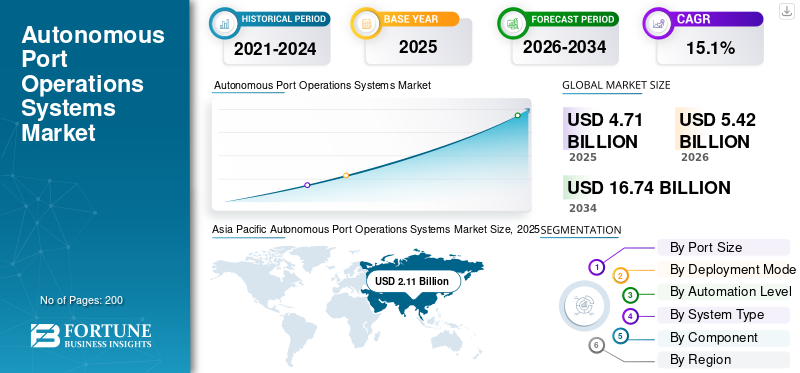

The global autonomous port operations systems market size was valued at USD 4.71 billion in 2025. The market is projected to grow from USD 5.42 billion in 2026 to USD 16.74 billion by 2034, exhibiting a CAGR of 15.1% during the forecast period. Asia Pacific dominated the autonomous port operations systems market with a market share of 44.79% in 2025.

The market encompasses the integration of advanced technologies designed to streamline terminal logistics, improve cargo handling precision, and enhance overall port throughput. By leveraging artificial intelligence, internet-of-things (IoT) connectivity, and robotics, these systems facilitate real-time tracking, predictive maintenance, and the orchestration of autonomous machinery. This digital transformation enables ports to optimize resource allocation and significantly reduce operational overhead. Ultimately, these solutions are essential for modernizing global supply chains, transforming traditional maritime hubs into highly efficient, data-driven environments capable of managing increasing trade complexities while minimizing human error in critical terminal activities.

Key players in the market include Kalmar, Konecranes, ABB, Siemens, TMEIC, Navis/Kaleris, INFORM GmbH, Huawei Technologies, CyberLogitec, and CERTUS Automation. These companies compete by developing sophisticated terminal operating systems (TOS), advanced automated container handling equipment, integrated software platforms for remote control, and AI-powered predictive analytics tools. They focus on delivering scalable, modular automation solutions tailored to the unique operational requirements of global shipping terminals, aiming to provide seamless interoperability, improved safety protocols, and optimized traffic management for high-volume, modern port infrastructures.

Download Free sample to learn more about this report.

Autonomous Port Operations Systems Market Key Takeaways

- 2025 Market Size: USD 4.71 billion

- 2026 Market Size: USD 5.42 billion

- 2034 Forecast Market Size: USD 16.74 billion

- CAGR: 15.1% from 2026–2034

- Asia Pacific dominated the market with a 44.79% share in 2025.

- Large International Hub Ports held the largest market share by port size in 2025.

- On-Premises dominated the market by deployment mode in 2025.

North America

The market is projected to reach USD 1.10 billion in 2026, driven by cargo automation, cybersecurity, and supply chain modernization.

Asia Pacific

The market reached USD 2.11 billion in 2025, driven by strong investments in smart ports and mega port infrastructure.

Europe

The market is projected to reach USD 1.38 billion in 2026, supported by automation, digital trade corridors, and sustainable port operations.

U.S.

The market is projected to reach USD 0.95 billion in 2026.

Japan

The market is projected to reach USD 0.45 billion in 2026.

Read More

AUTONOMOUS PORT OPERATIONS SYSTEMS MARKET TRENDS

Expansion of AI-Driven Predictive Maintenance are Emerging as the Defining Market Trend

The market is witnessing a clear shift toward AI-enabled predictive maintenance as port operators look to reduce equipment downtime, improve asset reliability, and avoid costly operational delays. Advanced analytics, IoT sensors, edge computing, and digital twin platforms are being used to monitor cranes, autonomous vehicles, conveyors, gates, power systems, and terminal equipment in real time. Instead of relying only on scheduled maintenance, operators are increasingly using condition-based insights to detect early signs of mechanical stress, component wear, overheating, and system faults. This trend is strengthening the move toward smarter, more resilient port ecosystems where maintenance decisions are data-driven, disruption is minimized, and critical assets remain available during high-volume cargo operations.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Increasing Need for Port Operational Efficiency Continue to Support Market Expansion

The primary driver for the autonomous port operations systems market growth is the urgent necessity to enhance operational throughput and reduce port congestion in response to expanding global trade volumes. Automated systems drastically shorten vessel turnaround times and optimize yard storage capacity by streamlining complex container stacking and retrieval processes. Furthermore, by reducing reliance on manual labor for repetitive tasks, these technologies significantly mitigate risks associated with human error and occupational hazards. As shipping companies and port authorities prioritize cost reduction and faster cargo movement, the shift toward autonomous, high-precision operations remains a critical imperative for maintaining competitive maritime logistics.

MARKET RESTRAINTS

High Initial Capital Expenditure Limit the Pace of Adoption

The significant upfront investment required for deploying autonomous port systems acts as a major market restraint, particularly for smaller terminals or those in developing regions with limited budgets. Implementing full-scale automation necessitates substantial funding for specialized robotic equipment, robust wireless communication infrastructure, and sophisticated software integration. Additionally, the long-term return on investment is often difficult to calculate due to complex project timelines and the necessity for extensive employee retraining. These high financial barriers, combined with the risks of long-term technology obsolescence, frequently lead to hesitant adoption and slower project realization periods within the industry.

MARKET OPPORTUNITIES

Deployment of Smart Port Infrastructure are Creating Strong Market Opportunity

Rising investments in smart port infrastructure represent a significant growth opportunity for technology providers capable of delivering comprehensive, interconnected automation suites. As global shipping hubs face increasing pressure to handle larger vessels and faster turnaround times, they are prioritizing end-to-end digital transformation projects. These initiatives create high demand for unified platforms that integrate autonomous terminal equipment with 5G-enabled communication networks and real-time logistics visibility. Companies that offer modular, scalable solutions that can be seamlessly retrofitted into existing brownfield operations or integrated into greenfield smart port projects are well-positioned to capitalize on this expanding capital expenditure.

MARKET CHALLENGES

Interoperability and Standardization Hurdles are Major Challenges in the Market

The lack of universal interoperability standards between disparate hardware and software components poses a persistent challenge for seamless terminal automation. Ports often rely on a mix of legacy systems and equipment from various vendors, creating significant friction when trying to integrate new autonomous solutions into existing ecosystems. Achieving a unified, plug-and-play environment requires complex, customized software middleware that is often proprietary and difficult to scale. This technological fragmentation complicates the deployment of end-to-end automation, necessitating costly integration services and limiting the flexibility of port operators to switch or upgrade vendors without significant disruption to their daily operations.

Segmentation Analysis

By Port Size

Need for Faster Vessel Turnaround and Higher Terminal Productivity Is Driving Demand for Large International Hub Ports Segment

Based on port size, the market is segmented into large international hub ports and medium and small ports.

The large international hub ports segment is anticipated to account for the largest autonomous port operations systems market share in 2025. Demand for the large international hub ports segment is rising because these ports handle heavy vessel calls, dense container flows, and complex intermodal movements. Automation helps hub ports improve berth planning, yard utilization, crane productivity, cargo visibility, and gate coordination, enabling faster turnaround and more reliable operations across terminals, customs, shipping lines, and logistics networks.

The medium and small ports segment is anticipated to rise with a CAGR of 15.6% over the forecast period.

By Deployment Mode

Cybersecurity and Mission-Critical Reliability are Driving Demand for On-Premises Segment

Based on deployment mode, the market is segmented into on-premises, cloud-based, and hybrid deployment.

In 2025, the on-premises segment dominated the global market share. Demand for on-premises deployment is rising as port operators still prefer local control for safety-critical systems such as crane automation, equipment control, gate systems, and terminal operating platforms. Ports cannot afford connectivity failures during cargo operations, so local infrastructure remains important for resilience, cybersecurity, latency control, and operational continuity.

The cloud-based segment is projected to grow at a CAGR of 15.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Automation Level

Need for Practical Automation Without Full System Replacement is Driving Demand for Semi-Autonomous Operations Segment

Based on automation level, the market is segmented into semi-autonomous operations, fully autonomous operations, remote-controlled operations, and AI-assisted decision support.

The semi-autonomous operations segment is anticipated to witness a dominating market share over the forecast period. Demand for the segment is rising as many ports want automation benefits without completely replacing existing labor, equipment, and workflows. Semi-autonomous systems support assisted driving, automated dispatch, remote supervision, safety alerts, and optimized routing, allowing terminals to improve productivity gradually while managing regulatory, labor, and investment risks.

The AI-assisted decision support segment is projected to grow at a high CAGR of 16.0% over the forecast period.

By System Type

Centralized Cargo Planning and Equipment Coordination are Driving Demand for Terminal Operating Systems

Based on system type, the market is segmented into Terminal Operating Systems (TOS), Equipment Control Systems (ECS), autonomous fleet management systems, Port Community Systems (PCS), digital twin platforms, and others.

The Terminal Operating Systems (TOS) segment dominated the market share. The demand for TOS is rising as these platforms act as the core digital backbone of port operations. They coordinate vessel planning, yard allocation, gate movement, container tracking, billing, equipment dispatch, and documentation workflows. Further, making them essential as ports shift toward integrated, data-driven, and autonomous operating models.

In addition, digital twin platforms are projected to grow at a CAGR of 17.4% during the forecast period.

By Component

Rising Need for Integrated Port Intelligence is Driving Demand for Software Platforms Segment

Based on component, the market is segmented into software platforms, hardware & sensors, autonomous equipment, connectivity infrastructure, control rooms & remote operation centers, and services.

The software platforms segment dominated the market share. The demand for such platforms is rising as autonomous port operations depend on integrated planning, equipment coordination, cargo tracking, berth scheduling, gate processing, and performance analytics. Software connects TOS, ECS, digital twins, fleet management, and port-community systems, helping operators improve visibility, reduce delays, automate workflows, and support safer, faster terminal decisions.

In addition, autonomous equipment are projected to grow at a CAGR of 16.2% during the study period.

Autonomous Port Operations Systems Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Autonomous Port Operations Systems Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2024, valuing at USD 1.84 billion, and also maintained the leading share in 2025, with USD 2.11 billion. Demand is rising as the region handles the largest share of global container traffic and continues investing in mega ports. China, India, Japan, Singapore, and South Korea are driving automation for throughput, efficiency, and competitiveness.

China Autonomous Port Operations Systems Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 1.14 billion. Demand in China is rising as the country operates some of the world’s largest and most automated container ports. Heavy cargo volumes, government-backed smart port programs, and strong domestic automation suppliers support large-scale deployment.

Japan Autonomous Port Operations Systems Market

The Japan market share in 2026 is estimated at around USD 0.45 billion, accounting for roughly 14.9% of CAGR during the forecast period. Demand in Japan is rising as ports need automation to offset labor shortages, improve terminal reliability, and support high-value trade flows. Japanese operators are adopting digital systems, remote equipment control, and efficient cargo-handling technologies.

India Autonomous Port Operations Systems Market

The Indian market size in 2026 is estimated at around USD 0.38 billion. Demand in India is rising as port modernization, logistics corridor development, and growing manufacturing exports are increasing the need for automated terminals. New deepwater projects and digital customs initiatives are creating strong demand from a lower base.

Europe

Europe is estimated to reach USD 1.38 billion in 2026 and secure the position of second-largest region in the market. Demand in Europe is rising as ports are prioritizing automation, emissions reduction, rail-port integration, and digital trade corridors. Strong logistics networks, strict environmental rules, and advanced terminal operators support adoption of smart port platforms and autonomous equipment.

U.K. Autonomous Port Operations Systems Market

The U.K. market growth in 2026 is estimated at around USD 0.26 billion, representing roughly 14.7% of CAGR over the forecast period. Demand in the U.K. is rising as ports are modernizing customs-linked digital workflows, container handling, and terminal planning after trade-process changes. Automation helps improve cargo movement, reduce delays, and support competitive maritime logistics.

Germany Autonomous Port Operations Systems Market

Germany’s market is projected to reach approximately USD 0.35 billion in 2026. The country’s demand is rising as ports such as Hamburg and Bremerhaven are tied closely to industrial exports, rail logistics, and European supply chains. Automation supports yard efficiency, digital documentation, emissions control, and reliable cargo movement.

North America

North America is projected to record a growth rate of 14.3% during the forecast period, and is estimated to reach a valuation of USD 1.10 billion by 2026. Demand in North America is rising as ports are modernizing cargo handling, gate processing, cybersecurity, and maritime security systems. U.S. and Canadian terminals are adopting automation to manage congestion, labor constraints, vessel delays, and resilient supply chain requirements.

U.S. Autonomous Port Operations Systems Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 0.95 billion in 2026, accounting for roughly 14.1% of CAGR over the forecast period. Demand in the U.S. is rising as ports need stronger cargo visibility, security screening, gate automation, and terminal efficiency. High import volumes, labor constraints, and supply chain resilience programs support investment in autonomous port operations systems.

Rest of the World

The rest of the world includes the Middle East & Africa and Latin America regions. These regions are expected to witness moderate growth in this market space during the forecast period. The Middle East & Africa and Latin America market is set to reach a valuation of USD 0.31 billion and USD 0.18 billion in 2026, respectively. Demand in the rest of the world is rising as Middle Eastern, African, and Latin American ports upgrade terminals, customs systems, and cargo visibility platforms. Gulf ports are especially active in smart port investments and transshipment automation.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players’ Focus on Integrated Port Automation, Remote Operations, and Digital Terminal Intelligence Is Boosting Market Growth

The autonomous port operations systems market is being strengthened by key players that are moving ports away from fragmented terminal tools toward integrated, automation-ready operating environments. Companies such as Kalmar, Konecranes, ABB, Siemens, TMEIC, Kaleris/Navis, INFORM, Huawei, CyberLogitec, and CERTUS Automation are focusing on terminal operating systems, equipment control systems, autonomous fleet coordination, remote crane operations, gate automation, private connectivity, cybersecurity, digital twins, and AI-based optimization. Kalmar is positioning its automation platforms around scalable, vendor-agnostic terminal control, while Konecranes is advancing automated container handling across greenfield, brownfield, and retrofit terminals. ABB is contributing through electrical, automation, and remote crane operation solutions that improve safety, reliability, and operational predictability, while Kaleris/Navis is strengthening the software backbone through TOS platforms used across hundreds of terminals globally. Together, these strategies are boosting market growth by helping ports reduce vessel turnaround time, improve yard productivity, enhance cargo visibility, lower operational risk, and modernize without immediately shifting to full autonomy.

LIST OF KEY AUTONOMOUS PORT OPERATIONS SYSTEMS COMPANIES PROFILED

- Kalmar (Finland)

- Konecranes (Finland)

- ABB (Switzerland)

- Siemens (Germany)

- TMEIC (Japan)

- Navis / Kaleris (U.S.)

- INFORM GmbH (Germany)

- Huawei Technologies (China)

- CyberLogitec (South Korea)

- CERTUS Automation (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Port of Shanghai & Technology Partners launched a pilot project for autonomous cranes to increase terminal efficiency and reduce operational costs.

- January 2026: Port of Felixstowe (U.K.) & Technology Partners expanded their autonomous truck fleet with 34 additional units operating in mixed traffic, supported by a private 5G network.

- January 2026: Busan Port (South Korea) & Hyundai Motor announced a partnership to implement AI-based smart port technologies, including autonomous robotics and planning systems.

- January 2026: Westwell & Middle East Operators strengthened ties, with over 156,000 TEUs handled by Q-Trucks in Q1, utilizing WellCrane solutions for automated container handling.

- December 2025: BTG Positioning Systems B.V. & GPR Inc.acquired/partnered to integrate advanced port automation and navigation systems into global port services.

REPORT COVERAGE

This research offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 15.1% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Port Size, By Deployment Mode, By Automation Level, By System Type, By Component, and Region |

| By Port Size |

|

| By Deployment Mode |

|

| By Automation Level |

|

| By System Type |

|

| By Component |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.71 billion in 2025 and is projected to reach USD 16.74 billion by 2034.

In 2025, the market value stood at USD 2.11 billion.

The market is expected to exhibit a CAGR of 15.1% during the forecast period.

By component, the software platforms segment is expected to dominate the market.

Increasing need for port operational efficiency continue to support market expansion.

Kalmar (Finland), Konecranes (Finland), ABB (Switzerland), Siemens (Germany), TMEIC (Japan), and Navis/Kaleris (U.S.) are few major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us