Autonomous Tractors Market Size, Share & Industry Analysis, By Autonomy level (L2/L3 and L4/L5), By Propulsion (Conventional and Electric), By Power Classes (<60 hp, 60–129 hp, 130–199 hp, and 200+ hp), By Application (Tillage and seeding, Spraying and Precision Application, Harvest Support, Mowing, Landscaping & Grass operations, and Specialty Tasks), and Regional Forecast, 2026-2034

Autonomous Tractors Market Size and Future Outlook

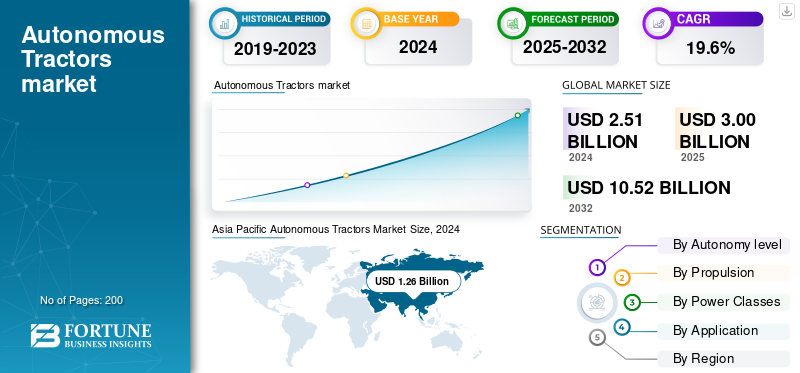

The global autonomous tractors market size was valued at USD 3.00 Billion in 2025. The market is projected to grow from USD 3.59 Billion in 2026 to USD 14.98 Billion by 2034, exhibiting a CAGR of 19.56% during the forecast period. Asia Pacific dominated the autonomous tractors market with a market share of 50.76% in 2025.

Autonomous tractors are farming vehicles equipped with advanced sensors, GNSS, cameras, and onboard software that let them perform field work with minimal human input. They execute tasks such as plowing, seeding, spraying, and harvest support using automated guidance, obstacle detection, and path-planning systems. Some operate as tele-operated or driver-assist, while higher-level machines carry out complex routines and adapt to changing conditions autonomously. By improving precision and enabling long operating hours, they reduce labor dependence and raise productivity, particularly valuable where skilled labor is scarce or repetitive tasks dominate.

The global market share is rapidly evolving as OEMs, tech firms, and retrofit specialists commercialize automation across farms of every size and region. Early phases emphasized retrofit kits and pilot projects; established manufacturers offer factory-integrated autonomous platforms alongside specialist retrofit and service models. Adoption varies by farm scale: large commercial operations favor high-power full-autonomy units, while smallholders often access automation through shared services or retrofits for specific tasks. Key enablers are GNSS precision, computer vision, machine learning, and telematics; constraints include regulation, financing, and on-farm infrastructure. Major manufacturers leading the field include John Deere, Kubota, CNH Industrial, and Mahindra, plus a range of startups and retrofit providers.

Tariffs on tractors and key electronic components can significantly slow autonomous tractor diffusion by increasing import costs and extending supply-chain lead times. Higher duties raise end-user prices, which dampens farmer demand and often shifts preference toward locally produced machines or retrofit/service models assembled domestically. Tariffs may also deter cross-border OEM investment and delay technology transfer, while encouraging regional suppliers, local partnerships, or higher local content requirements. Manufacturers typically respond by redesigning sourcing, boosting local production, or accepting margin compression actions that influence deployment speed, price dynamics, and overall market structure.

Download Free sample to learn more about this report.

Autonomous Tractors market Takeaways

- 2025 Market Size: USD 3.00 billion

- 2026 Market Size: USD 3.59 billion

- 2034 Forecast Market Size: USD 14.98 billion

- CAGR: 19.56% from 2026–2034

- Asia Pacific dominated the autonomous tractors market with a 50.76% share in 2025.

- The L2/L3 (semi-autonomous) segment is projected to lead the market with a 69.46% share in 2026.

- The retrofit segment is expected to dominate with a 55.11% share in 2026.

North America

North America generated USD 0.54 billion in 2025 and is projected to reach USD 0.64 billion in 2026.

Europe

Europe accounted for 20.96% of the global market in 2025, reaching USD 0.63 billion and is expected to grow to USD 0.74 billion in 2026.

Asia Pacific

Asia Pacific led the global market with USD 1.52 billion in 2025 and is projected to reach USD 1.84 billion in 2026.

U.S.

The autonomous tractors market is valued at USD 0.47 billion by 2026.

Japan

The market is valued at USD 0.13 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Acute and Persistent Farm Labor Scarcity Drives Market Growth

Rising labor costs, shrinking rural workforces, and an aging farmer population make automation an economic necessity rather than a novelty. As many farms struggle to hire seasonal and skilled workers, manufacturers and service providers position autonomy to keep fields running longer and to reduce dependence on hired labor. However, OEMs explicitly cite labor shortages when accelerating product launches and retrofit programs. Mechanization gaps amplify the pressure in regions with low tractor density, and labor constraints push farms toward shared, automated services and retrofit kits to multiply effective machine hours. In advanced agriculture systems, the average producer age is high, which correlates with greater interest in advanced technologies that reduce physical workload. Practical pilots and fleet approaches show the concept scales, digital tractor-sharing platforms and tracked fleets are already being used at scale.

MARKET RESTRAINTS

Regulatory and Safety Uncertainty Hampers Market Growth

Regulatory and safety uncertainty increases both risk and cost for manufacturers and slows adoption. Autonomous tractors operate in complex, dynamic, and current legislative frameworks often lag behind the technology. For example, in California, a law from the 1970s requires a rider to be on board self‐propelled farm equipment even if it is designed to function autonomously; changing that law has become a pressing issue for growers seeking to use driverless tractors. Relatedly, authorities in many countries have not yet implemented clear rules governing autonomous tractors on public roads, liability in case of accidents, or certification of sensors and software.

Another dimension is the cost and complexity of compliance. In many jurisdictions, safety systems, software validation, and liability insurance add significant upfront investment beyond just hardware. Farmers in developing markets often cite affordability and lack of infrastructure (e.g., reliable GPS, cellular/Internet connectivity, and local maintenance) as obstacles. Moreover, uncertainty about whether authorities will accept autonomous operation without an onboard operator or allow certain levels of autonomy (L4/L5) imposes legal risk. These uncertainties make many manufacturers proceed more cautiously, investing in pilot programs and retrofit kits rather than full factory-built autonomous machines, slowing overall market rollout.

MARKET OPPORTUNITIES

Integration of Autonomy with Precision Agriculture Systems Creates Lucrative Growth Opportunities

Integration of autonomy with precision agriculture systems to boost productivity, reduce input waste, and open new service models for smallholders. Autonomous tractors act as mobile, high-precision platforms for GPS-guided seeding, variable-rate spraying, and real time data collection. When paired with precision tools, they let operators apply seed, fertilizer, and chemicals only where needed, extending operating hours and improving the timeliness of operations and real time decisions. Evidence of this potential is visible in farm technology adoption patterns for example, yield monitors, yield maps and soil maps are used on roughly 68% of large-scale crop farms, showing how precision tools scale with farm size and in service-model traction.

OEM moves also underline market momentum, major manufacturers are commercially advancing factory autonomy and retrofit kits, enabling quicker adoption and broader deployment across farm sizes. The combined effect is multifold, modest per-hectare productivity gains from current precision practices can compound when machines operate autonomously for longer daily windows and with higher path accuracy, this raises the economic case for autonomy in both large commercial farms and for subscription/service models that let smallholders access high-grade automation without owning it outright. Overall, precision and autonomy creates scalable yield, cost, and labor advantages that can accelerate autonomous tractors market growth globally.

AUTONOMOUS TRACTORS MARKET TRENDS

Proliferation of Factory-Integrated Autonomy Kits and Retrofit Partnerships is One of the Significant Market Trends

The proliferation of factory-integrated autonomy kits and retrofit partnerships enables farmers to adopt automation without wholly replacing their existing fleets. OEMs are increasingly collaborating with software and autonomy specialists to embed AI, perception systems, and autonomous systems controls into both new tractors and existing models. For example, Kubota has partnered with Agtonomy to commercialize autonomous operations on its M5N diesel tractors, targeting specialty-crop growers who traditionally rely on manual labor for spraying and mowing. Also, Deere recently unveiled its second-generation autonomy kit for its large tractors (e.g., the 9RX series), featuring a 16-camera Halo system to deliver 360-degree visibility. These moves reflect a shift toward modular autonomy, where farmers can choose retrofit or add-on solutions rather than committing to wholly new robot tractors.

Combined with increasing labor shortages and rising operational costs, this trend accelerates adoption, Deere cites that one farmer with 300 acres was able to shorten their tillage work by two weeks by using autonomous tech. The benefit to producers is twofold, lower upfront investment, and a faster learning curve since operators can adopt autonomy incrementally. Over time, these retrofitted or modular systems serve as stepping stones toward full OEM factory autonomy. As regulation catches up and component costs decline, the retrofit + kit ecosystem is becoming a core trend that broadens the market’s reach and accelerates diffusion into more geographies and farm sizes.

Download Free sample to learn more about this report.

Segmentation Analysis

By Autonomy level

Faster and Low-risk Productivity Gains from L2/L3 Drive Autonomy Level Segmental Growth

On the basis of the segmentation of battery type, the market is classified into L2/L3 and L4/L5.

L2/L3 (semi-autonomous) is projecteed to dominate the market with a share of 69.46% in 2026 as it delivers immediate, low-risk productivity gains using proven components and retrofit routes. L2/L3 systems let tractors follow GNSS-guided paths, maintain implement control, and reduce operator fatigue while keeping a human available to override a model that fits existing farm practices and regulations. OEMs and retrofit suppliers, therefore, prioritize kits and camera/steering packages that convert existing fleets quickly, major OEM announcements show manufacturers balancing new factory models with retrofits. L2/L3 widens the addressable market fast, as farmers can adopt incremental automation without reworking finance, maintenance, or liability frameworks, and service models scale faster using these lower-risk systems.

By Propulsion

Availability of Existing ICE-Powered Vast Fleet to Drive Segment Growth

Based on propulsion, the market is segmented into conventional and electric.

Conventional diesel/ICE tractors currently dominate autonomous deployments as the existing global tractor fleet is overwhelmingly powered by internal combustion; converting those machines is simpler and cheaper than wholesale electrification. The retrofit segment is projecteed to dominate the market with a share of 55.11% in 2026. Most retrofit kits and early OEM autonomous platforms are optimized for conventional drivetrains, so conventional propulsion represents the bulk of autonomous operating hours today. Public rollouts and OEM announcements through 2023–25 emphasize diesel-based autonomy, particularly for high-horsepower fieldwork where energy density matters.

By Power Class

Flexibility of <60 Hp to Work in Smallholder and Specialty Farms Drives Segmental Growth

Based on the power class, the market is classified into <60 hp, 60–129 hp, 130–199 hp, and 200+ hp.

The 60–129 hp segment is projecteed to dominate the market with a share of 32.98% in 2026. Tractors under 60 hp dominate autonomous tractor uptake as they match the structure of smallholder and specialty farms, where compact, low-cost automation yields rapid returns. Smallholders and horticulture operations favor compact electric or conventional utility tractors that can navigate narrow rows and orchards; these use cases are ideal for retrofits or purpose-built small autonomous platforms. Field evidence and service platforms show that many early shared-use fleets and autonomous pilots use sub-60 hp machines, which represent a large portion of unit installations in developing and developed markets alike. Recent coverage of compact e-tractor registrations and specialty orchard deployments, plus manufacturer focus on small, driver-optional electric models, reinforces that sub-60 hp tractors are the practical entry point for scaled autonomous adoption and local service models.

By Application

To know how our report can help streamline your business, Speak to Analyst

Continuous and Repetitive Requirement of Tillage and Seeding Drives Demand

Based on application, the market is segregated into tillage and seeding, spraying and precision application, harvest support, mowing, landscaping, grass operations, and specialty tasks.

The tillage and seeding segment is projecteed to dominate the market with a share of 27.98% in 2026. Tillage and seeding lead applications as they are highly repetitive, deterministic, and benefit strongly from precise, fatigue-free execution, ideal for current autonomy tech. Autonomous guidance guarantees straight, non-overlapping passes and consistent depth/speed control, improving seed placement and reducing input waste. Many OEM demonstrations and retrofit trials have prioritized tillage and seeding, and service fleets often start with these chores to maximize machine utilization. Operators realize immediate efficiency gains from overnight or multi-shift operations; by automating tillage and seeding, farmers extend workable windows and improve timeliness, which directly raises yield potential. Recent OEM product rollouts and retrofit kit news highlight tillage/seeding as the initial high-value use case that scales both unit demand and ancillary services, driving broader market growth.

AUTONOMOUS TRACTORS MARKET REGIONAL OUTLOOK

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific

Asia Pacific Autonomous Tractors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for USD 1.52 Billion in 2025, representing 50.76% of the global market share, and is projected to reach USD 1.84 Billion in 2026. Asia Pacific is the dominant and fastest-growing region due to sheer tractor volume (China and India), active OEM initiatives, and a mix of large commercial farms and millions of smallholders accessible via service models. OEMs and regional manufacturers (alongside retrofit and platform providers) are launching products and pilot programs tailored to diverse needs ranging from high-power autonomous tractors for commercial grain farms to compact robots for specialty farms. The combination of massive addressable fleets, government mechanization programs, and expanding retrofit/service offerings accelerates diffusion. The visible OEM demonstrations and new product concepts showcased at major trade events underline the region’s rapid commercialization potential, further fueling dominance in autonomous tractors market share. The Japan market is valued at USD 0.13 billion by 2026, the China market is valued at USD 0.79 billion by 2026, and the India market is valued at USD 0.60 billion by 2026.

North America

The North America market generated USD 0.54 Billion in 2025, representing 17.87% of the global market landscape, and is expected to reach USD 0.64 Billion in 2026. North America leads early commercial adoption due to large-scale farms, strong OEM presence, and accessible capital for pilots and fleets. Major manufacturers and dealers are actively fielding factory autonomous platforms and retrofit kits while service providers offer teleoperation and fleet & farm management, combining to shorten payback periods for automation. Labor scarcity and the ageing farm workforce further push mechanization which correlates with heightened interest in labor-saving autonomy. OEMs are accelerating rollout, creating a dense innovation and distribution network that benefits broad deployment.

The U.S. market is the most commercially mature within North America. As large row-crop operations, high labor costs, and established dealer networks make the U.S. a primary proving ground for factory and retrofit autonomy. Federal and state research programs, combined with OEM pilot fleets and retrofit offerings, help validate technical and business models quickly. Recent high-profile OEM reveals and demonstrations at trade shows underline U.S. leadership in commercialization and the rapid transition from pilots to limited production runs. The U.S. market is valued at USD 0.47 billion by 2026.

Europe

Europe contributed 20.96% to the global market in 2025, with a valuation of USD 0.63 Billion, and is projected to reach USD 0.74 Billion in 2026. Europe’s outlook combines strong precision-agriculture adoption, regulatory emphasis on sustainability, and a diverse farm structure. Further, large commercial farms in some countries and dense specialty/horticulture farms in others. This heterogeneity favors both full-size autonomous platforms for large arable farms and compact autonomous/electric units for orchards and vineyards. European OEMs and startups are actively demonstrating electric and autonomy concepts and pilots, while IoT and farm-data integration projects strengthen precision use cases. Subsidies, emissions rules, and sustainability programs accelerate demand for lower-emission, highly automated solutions, and established dealer channels make Europe a high-value market for factory autonomy and integrated services. The U.K. market is valued at USD 0.08 billion by 2026, while the Germany market is valued at USD 0.17 billion by 2026.

Rest of the World

In 2025, the Rest of the World market stood at USD 0.31 Billion, representing 10.41% of global demand, and is projected to grow to USD 0.37 Billion in 2026. The rest of world region presents an opportunistic but uneven outlook. However, Latin America’s large commercial farms are attractive for high-power autonomous platforms, while Africa and parts of the Middle East lean toward shared-use service models and retrofit solutions owing to smallholder prevalence and infrastructure constraints. Platforms that enable tractor-sharing and digitally managed fleets are already proving traction in Africa, expanding access without requiring upfront purchase. Infrastructure, financing, and local service networks remain constraints, but growing pilot programs, retrofit kit rollouts, and service operators are creating scalable pathways for autonomy across the region’s varied farm structures.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Leadership, Strong Investment, and Continuous Innovation by John Deere Drive Competitive Edge

John Deere is widely considered the foremost global manufacturer of autonomous tractors due to its early investment, product breadth, and ecosystem strength. It was among the first to offer autonomy-ready tractors (8R, 8RX, 9R, 9RX) that come from the factory with hardware configured for autonomous perception, combined with autonomy kits that retrofit existing machines. The company’s presence in precision guidance (AutoTrac, AutoPath, and others), cloud-enabled operations center, and multi-camera/sensor perception systems makes its offerings among the most technically mature. Also, its Autonomy Precision Upgrade allows turning existing tillage tools and tractors into autonomous units through hardware/software dropdowns. This product portfolio spans factory autonomous tractors, retrofit kits, perception systems, and precision-guidance upgrades.

Kubota is generally recognized as the major player in the autonomous tractor space. Kubota’s portfolio blends concept-electric tractors (e.g., its Future Cube vision for a fully automated electric tractor), specialty-crop autonomous units, and partnerships such as with Agtonomy to retrofit specialty tractor-sprayer operations. Recent exhibits show Kubota’s autonomous offerings for safety, labor saving, and remote control. Its blend of compact autonomous machines, electric powertrain R&D, and retrofit/autonomy-kit development gives it a strong second position behind Deere in terms of product diversity and market focus.

LIST OF KEY AUTONOMOUS TRACTOR COMPANIES PROFILED

- Deere & Company (U.S.)

- CNH Industrial (Netherlands)

- AGCO Corporation (U.S.)

- Kubota Corporation (Japan)

- CLAAS (Germany)

- SDF Group (Italy)

- Mahindra & Mahindra (India)

- Yanmar Co., Ltd. (Japan)

- Iseki & Co., Ltd. (Japan)

- Kinze Manufacturing (U.S.)

- Monarch Tractor (U.S.)

- Bobcat Company (U.S.)

- Sabanto, Inc. (U.S.)

- Agtonomy (U.S.)

- Muddy Machines (U.K.)

KEY INDUSTRY DEVELOPMENTS

- August 2025: AGCO launched four new Fendt 1000 Vario Gen4 tractors, with Fendt DynamicPerformance engine, artificial intelligence, and factory-integrated OutRun autonomy. The new Gen4 runs on a 12.4-liter MAN D26 engine. The tractors, 1040, 1044, 1048, and 1052, range in maximum horsepower from 400–520 hp. With Fendt DynamicPerformance, farmers are able to manage engine power, reducing horsepower to match an implement’s needs and increase fuel efficiency, or increase output by a maximum of an additional 30 hp, depending on the model.

- June 2025: Kubota North America collaborated with Agtonomy, a leader in agricultural autonomy software, to commercialize autonomous operations on Kubota diesel tractors for spraying and mowing. This joint effort reflects Kubota's ongoing commitment to pioneering solutions for specialty crop growers, equipping them with smart technology that enhances efficiency, adaptability, and productivity.

- April 2025: Carbon Robotics introduced the Carbon AutoTractor, a new autonomy kit designed to convert existing John Deere 6R and 8R series tractors into remotely monitored, autonomous machines. The system addresses growing labor shortages by enabling around-the-clock operation for tasks such as laser weeding, mowing, mulching, and discing. Designed for 24/7 operation of tasks such as laser weeding, it helps reduce labor dependence and increase field productivity.

- March 2025: AGCO launched autonomous tractor retrofit kits for mixed fleets. The retrofit kits will enable select Fendt and John Deere tractors to autonomously perform grain cart and tillage functions, with more tractor compatibility and functions coming in the future.

- January 2025: John Deere & Co. (DE.N) strengthened its bet on autonomous agricultural machinery by unveiling new tractors and industrial equipment, capable of operating without the need for a human being in the cab, at the CES trade show in Las Vegas. It is making strides toward automating manual work amid a shortage of skilled workers and high labor costs.

REPORT COVERAGE

The global autonomous tractors market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market forecasts a detailed competitive landscape with information on the market share, growing opportunities, and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 19.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Autonomy level, Propulsion, Power Classes, Application, and Region |

| By Autonomy level |

|

| By Propulsion |

|

| By Power Classes |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.59 Billion in 2026 and is projected to reach USD 14.98 Billion by 2034.

In 2025, the market value stood at USD 1.52 billion.

The market growth is expected to exhibit a CAGR of 19.56% during the forecast period.

The conventional segment led the market in the propulsion segment.

Acute and persistent farm labor scarcity drives the market growth.

Top players in the autonomous tractors include John Deere, Kubota, CNH Industrial, and Mahindra.

Asia Pacific dominated the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us