Autorefractor and Keratometer Market Size, Share & Industry Analysis, By Product Type (Autorefractor, Keratometer, and Hybrid), By Portability (Tabletop and Handheld), By Indication (Hyperopia, Myopia, Astigmatism, and Others), By End-user (Hospitals, Ophthalmic Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

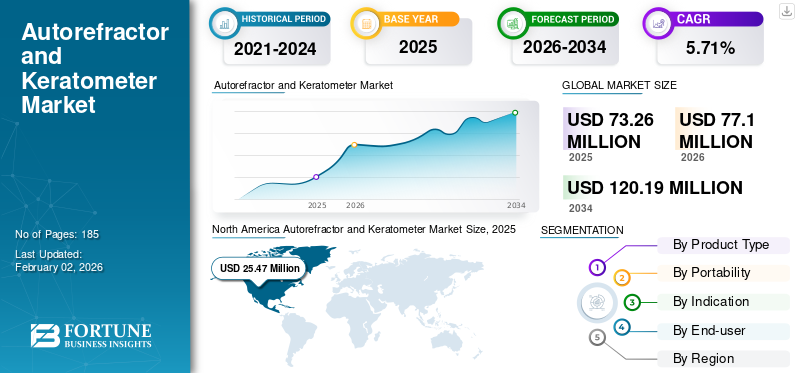

The global autorefractor and keratometer market size was valued at USD 73.26 million in 2025. The market is projected to grow from USD 77.1 million in 2026 to USD 120.19 million by 2034, exhibiting a CAGR of 5.71% during the forecast period. North America dominated the autorefractor and keratometer market with a market share of 2.45% in 2025

An autorefractor and a keratometer are essential ophthalmic instruments used to assess different aspects of eye health and vision correction needs. An autorefractor (also known as an automated refractor or auto-refractometer) measures a person's refractive error by analyzing how light changes as it enters the eye, thereby calculating the refractive error. A keratometer is an instrument used to measure the curvature of the anterior surface of the cornea. It projects a beam of light onto the cornea, and the reflected image is analyzed to determine the curvature. Additionally, an autorefractor keratometer (ARK) combines both autorefraction and keratometry in a single device, providing a comprehensive eye assessment.

Market growth is driven by the significant burden of eye conditions such as astigmatism, hyperopia, and cataracts, which may lead to vision impairments. This growing emphasis on early diagnosis of eye conditions is driving the autorefractor and keratometer demand.

Leading companies in the market include Topcon Corporation, NIDEK CO., LTD., Carl Zeiss Meditech AG, and others, concentrating on numerous growth tactics such as product advancements and geographic expansion to boost their product reach across the globe.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Prevalence of Ocular Diseases to Fuel Market Expansion

Over the past few years, there has been a surge in the incidence of ocular diseases driven by lifestyle changes, an aging population, and rising diabetic conditions. These conditions are responsible for increasing the burden of hyperopia, astigmatism, and myopia, necessitating detailed diagnosis assessments of refractive error and corneal surface.

- For instance, as per the data published by the National Center for Biotechnology Information (NCBI) in September 2023, the myopia incidence is growing globally, and nearly half of the population globally is anticipated to suffer from myopia by 2050, with approximately 10.0% highly myopic.

Additionally, several governments, healthcare agencies, and ophthalmic care suppliers are increasingly focusing on early diagnosis of eye conditions to better manage and alleviate vision-related diseases. Such preventive measures are expected to increase the autorefractor and keratometer utilization, thereby propelling market growth during the forecast period.

Market Restraints

Limited Awareness of Eye Diagnosis and Affordability Concerns May Hinder Market Growth

Despite the increasing prevalence of eye diseases across the globe, awareness of the importance of regular eye examinations remains limited in many low- and middle-income countries. Additionally, the substantial costs of high-end models present significant barriers to widespread adoption in these countries. This can make it prohibitive for smaller clinics and hospitals, reducing their availability in these settings.

- For instance, as of 2025, Bimedis mentioned that the high-end autorefractor models can cost upwards of USD 25,000, posing a substantial investment for resource-constrained healthcare settings.

Moreover, limited public awareness often leads to delayed access to essential eye care. This can diminish the autorefractor and keratometer demand, hampers market expansion.

Market Opportunities

Surge in Strategic Partnerships Among Key Participants to Boost Product Sales

With the surging demand for advanced diagnostic devices, top-tier players are shifting gears toward innovation. This evolving focus has led to a surge in clinical research targeting eye conditions and spurred a wave of collaborations, mergers, and acquisitions. This is intended to enhance product modernization, including the development of handheld autorefractors and other advanced tools.

- For instance, in April 2024, Carl Zeiss Meditech AG acquired D.O.R.C. (Dutch Ophthalmic Research Center) to reinforce its ophthalmic product lineup and digital workflow capabilities.

As companies increasingly join forces, their combined expertise and assets are set to accelerate the development of cutting-edge eye diagnostic equipment, including autorefractors and keratometers. This surge in collaboration is poised to trigger a wave of product rollouts, unlocking promising avenues for market expansion.

Market Challenges

Lack of Trained Experts May Hamper Market Growth

The dearth of experts in the ophthalmology field poses a significant challenge that is expected to hinder autorefractor and keratometer demand. This shortage may limit the effective deployment and use of advanced diagnostic technologies essential for accurate eye condition diagnosis and treatment.

Furthermore, the lack of trained personnel can reduce patient access to vital diagnostic services, potentially restraining market expansion.

- For instance, a report by the American Academy of Ophthalmology (AAO), published in February 2024, indicated that there were fewer than 60,000 ophthalmic technicians supporting over 19,000 practicing ophthalmologists in the U.S. This is expected to create a significant imbalance between supply and demand.

Such workforce shortages could lead to a decreased ability of healthcare providers to diagnose patients, thereby delaying such procedures and ultimately hindering the utilization of autorefractors and keratometers. This, in turn, is expected to hinder the market in the coming years.

Autorefractor and Keratometer Market Trends

Technological Advancements to Boost Market Growth

Recent advancements in autorefractors and keratometers are transforming the landscape of the diagnosis of eye conditions. The incorporation of digital and automated features has enhanced the functionality of these devices, allowing for more accurate examinations. Modern devices are capable of storing and analyzing patient data, integrating with EHR systems, and generating detailed diagnostic reports. Digital autorefractors enhance the accuracy and efficacy of eye exams through digital readouts and automated printouts.

Moreover, some of the recent advancements include enhanced imaging capabilities through high-resolution cameras, enabling the capture of detailed images and determining eye health. These advancements have enabled optometrists to detect subtle changes in the eye’s anatomy. This further helps in early diagnosis and determining the treatment of conditions such as cataracts and keratoconus.

Additionally, the integration of artificial intelligence (AI) and machine learning (ML) into autorefractor and keratometer systems has enabled precision analytics and real-time data analytics. These systems are recently offering features such as automated focusing, cloud integration, and patient data tracking. Such advancements are expected to increase their adoption in ophthalmic settings.

Download Free sample to learn more about this report.

Impact of COVID-19

The COVID-19 pandemic witnessed a negative impact on the global autorefractor and keratometer market growth. The widespread disruption of healthcare services during this period led to a decreased demand for examination and diagnostic tools, including ophthalmic. This was mainly due to the decreased patient visits to ophthalmic settings. As a result, prominent companies in the sector experienced a substantial decline in revenues during the pandemic.

- For instance, Carl Zeiss Meditech AG reported a decline of -7.0% in sales of ophthalmic devices in 2020, amounting to USD 991.0 million.

Moreover, during the outbreak, several patients postponed their visits to healthcare facilities for eye examinations, which led to decreased utilization of autorefractors and keratometers.

However, with the easing of lockdown restrictions in 2021 and a resurgence of patient visits to ophthalmic settings, the market began to recover, eventually returning to its pre-pandemic growth trajectory.

Segmentation Analysis

By Product Type

Hybrid Segment to Lead Market Due to High Accuracy of ARKs

Based on product type, the market is classified into autorefractor, keratometer, and hybrid. The hybrid segment is expected to hold a major market share during the forecast period. The segment’s growth is attributable to the high accuracy of autorefractor-keratometers (ARKs) (hybrid) compared to standalone devices for eye examinations. This has prompted key players to increase the launch of such devices and promote their usage in ophthalmic settings, which is expected to drive the segment’s growth.

- For instance, in April 2024, NIDEK CO., LTD. launched the ARK-F/AR-F auto ref/keratometer, featuring a fully automatic measurement of eye health.

The autorefractor segment is expected to witness substantial growth during the forecast period. Key companies are integrating new technology, such as AI and machine learning, to enhance the features of autorefractors, thereby enhancing their diagnostic outcomes. These advancements are expected to increase their adoption across healthcare settings, thereby driving the segment’s growth.

By Portability

Tabletop Segment to Dominate Market Owing to Its High Preference in Optometric Offices

Based on portability, the market is classified into tabletop and handheld. The tabletop segment is expected to hold a major market share during the forecast period. The segment’s growth is attributable to a high preference for tabletop systems in optometric offices, as they are ideal for conducting comprehensive eye examinations.

The handheld segment is expected to witness substantial growth over the forecast period. Handheld devices offer flexibility and convenience and are particularly useful for mobile clinics, home visits, and screenings in schools or workplaces. There is an increasing demand for portable, battery-powered, and lightweight devices, especially in rural or underserved regions, which is encouraging prominent players to launch new devices and contribute toward segment growth.

- For instance, in October 2022, Remidio Innovative Solutions Pvt Ltd. launched Instaref R20, a handheld portable auto refractometer that uses Shack-Hartmann aberrometry-based technology to determine refractive error.

By Indication

Growing Prevalence of Hyperopia to Fuel the Segment’s Growth

Based on indication, the market is divided into hyperopia, myopia, astigmatism, and others. The hyperopia segment held the largest market share in 2024. The increased prevalence of hyperopia in both adults and pediatrics is propelling the use of effective diagnostic solutions such as autorefractors and keratometers, which is expected to fuel the segment’s growth.

- For instance, as of March 2023, the Cleveland Clinic stated that hyperopia is projected to affect around 4.6% of children and 30.9% of adults across the globe.

The myopia segment is projected to experience notable growth in the forthcoming years, propelled by factors such as the increasing geriatric population and increased screen time of individuals due to rising digital device usage. These conditions may further increase the incidence of myopia and fuel the autorefractor and keratometer demand.

The astigmatism segment is anticipated to hold a substantial share during the forecast timeframe, attributed to the increased availability of modern and advanced featured devices that enhance the diagnostic scenario for this condition.

The others segment is anticipated to hold a stagnant share due to the increasing burden of refractive errors caused by keratoconus, cataracts, and others. These conditions may necessitate the need for frequent diagnosis, which is expected to fuel the autorefractor and keratometer demand.

By End-user

Increase in Number of Ophthalmic Diagnostic Procedures Encouraged Hospitals Segment Growth

Based on end-user, the market is segmented into hospitals, ophthalmic clinics, and others.

The hospitals segment dominated the market in 2024, attributed to the high volume of ophthalmic diagnostic procedures conducted in hospital settings. This is due to the large resources available in these settings, which lead to widespread access to advanced equipment.

The ophthalmic clinics segment is expected to grow at the fastest CAGR during the forecast period. This growth is driven by the increasing number of ophthalmic clinics globally, which is fueling the need for the installation of advanced diagnostic equipment such as autorefractors and keratometers.

- For instance, in December 2022, UC Davis Health launched a new cutting-edge eye care facility in Sacramento.

The others segment, including telehealth and academic clinics, is projected to expand significantly in the forthcoming years due to increasing initiatives and partnerships aimed at improving the diagnostic landscape in healthcare settings, thereby enhancing access to vision care.

AUTOREFRACTOR AND KERATOMETER MARKET REGIONAL OUTLOOK

By geography, the market is studied across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Autorefractor and Keratometer Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 25.47 million in 2025, representing 2.45% of the global industry, and is expected to reach USD 26.65 million in 2026. The advanced healthcare infrastructure, reimbursement policies, and strong presence of major players are leading to higher availability of autorefractors and keratometers in the region, fueling market growth.

In the U.S., the growing number of ophthalmic disorders driven by the significant burden of diabetes is leading to increased patient visits to ophthalmic settings. This trend is expected to propel the adoption of cutting-edge diagnostic systems and contribute to the country’s market growth.

- For instance, in May 2024, the Centers for Disease Control and Prevention (CDC) stated that nearly 38.4 million individuals were living with diabetes in the U.S.

In Canada, the growing incidence of ocular conditions such as irregular astigmatism, keratoconus, and other vision-related problems is driving the adoption of aberrometers for diagnosis, further contributing to the market expansion in the country.

Europe

Europe recorded a market size of USD 30.63 million in 2025, capturing 3.55% of the global market share, and is projected to reach USD 32.39 million in 2026. The market in Europe held a substantial share in 2024 due to standard medical device regulations that promote high-quality diagnostic tools, driving the autorefractor and keratometer demand. Moreover, the large population of ophthalmologists in the region is supporting the higher diagnosis rates of eye health, which is further expected to propel market growth.

- For instance, in December 2023, the Royal College of Ophthalmologists (RCOpth) mentioned that around 3,377 ophthalmologists were listed on the specialist register in the U.K.

Asia Pacific

In 2025, Asia Pacific represented USD 11.85 million, accounting for 1.97% of the worldwide market, and is projected to grow to USD 12.59 million in 2026. The growth is attributed to the increasing investment in ophthalmic diagnostics by countries such as India, China, and Japan, which is supporting the adoption of autorefractors and keratometers across the region. Moreover, the large patient pool suffering from eye diseases is further expected to drive the demand for such devices.

- For instance, according to the study published by the International Journal of Community Medicine and Public Health in November 2022, there was 47.8% of astigmatism in school-aged children in the south Delhi region of India.

Latin America and Middle East & Africa

The Latin America market was valued at USD 2.94 million in 2025, capturing 2.07% of global revenue, and is estimated to reach USD 3.05 million in 2026. Middle East & Africa contributed 3.16% to the global market in 2025, with a valuation of USD 2.37 million, and is projected to reach USD 2.43 million in 2026.

The Latin American and Middle East & Africa markets are expected to grow at a moderate CAGR during the forecast period. High incidence of visual impairments, a large number of ophthalmologists, and an expanding focus on healthcare infrastructure development are expected to enhance the penetration of ophthalmic diagnostic devices in these regions.

- For instance, in January 2024, the Saudi Arabian government announced an investment of over USD 65.0 billion to improve the country’s healthcare infrastructure under its Vision 2030 program.

COMPETITIVE LANDSCAPE

Key Industry Players

Prominent Players’ Focus on Introduction of Novel Products to Gain Competitive Edge

The global market is consolidated with major players such as Carl Zeiss Meditech AG, Topcon Corporation, and NIDEK CO., LTD. These players accounted for the significant global autorefractor and keratometer market share in 2024. This is attributed to a strong market presence, supported by robust distribution networks (both indirect and direct), and a diversified product portfolio of diagnostic solutions. Moreover, these companies are focusing on introducing new products, entering untapped markets, and prioritizing the development of technologically advanced products to maintain their competitive edge. Other players operating in the market include EssilorLuxottica, CANON MEDICAL SYSTEMS CORPORATION (Canon Inc.), Bausch + Lomb, and other small & medium-sized players. These players are concentrating on partnerships, collaborations, and other strategies to expand their market reach.

LIST OF KEY AUTOREFRACTOR AND KERATOMETER COMPANIES PROFILED

- EssilorLuxottica(France)

- Carl Zeiss Meditech AG (Germany)

- Topcon Corporation (Japan)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- NIDEK CO., LTD. (Japan)

- Bausch + Lomb (Canada)

- Visionix (U.S.)

- Remidio Innovative Solutions Pvt Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- July 2024: EssilorLuxottica acquired an 80.0% stake in Heidelberg Engineering, a company specializing in diagnostic solutions, healthcare IT, and digital surgical technologies for clinical ophthalmology.

- December 2023: Carl Zeiss Meditech AG announced its agreement to acquire a 100.0% share in Dutch Ophthalmic Research Center (International) B.V. (D.O.R.C.) from Eurazeo SE.

- November 2023: CANON MEDICAL SYSTEMS CORPORATION partnered with the Cleveland Clinic to develop innovative imaging and healthcare IT technologies aimed at improving diagnosis and care for patients, including ophthalmic.

- May 2022: Visionix and Right MFG. Co., Ltd. signed a partnership agreement for the distribution of the popular Retinomax handheld autorefractor/keratometer in Europe, the Americas, and Asia Pacific.

- June 2019: NIDEK CO., LTD. launched the ARK-F/AR-F keratometer, a fully automated device for eye measurements.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.71% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Product Type

|

|

By Portability

|

|

|

By Indication

|

|

|

By End-user

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 73.26 million in 2025 and is projected to reach USD 120.19 million by 2034.

In 2025, the market value stood at USD 25.47 million.

The market is expected to exhibit a CAGR of 5.71% during the forecast period (2026-2034).

By end-user, the hospitals segment led the market.

The key factors driving the market are the increasing prevalence of ophthalmic conditions and technological advancements in diagnostic systems.

Carl Zeiss Meditech AG, Topcon Corporation, and NIDEK CO., LTD. are the top players in the market.

North America held the largest market share in 2024.

- 2021-2034

- 2025

- 2021-2024

- 185

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us