Battery Coating Market Size, Share & Industry Analysis, By Battery Component Type (Separator Coating, Cathode Coating, Anode Coating, and Others), By Material Type (Ceramic Materials, Fluoropolymers (PVDF), Aqueous Polymers (SBR/CMC), and Others), By Application (Electric Vehicles, Energy Storage Systems, Consumer Electronics, and Others), and Regional Forecast, 2026-2034

BATTERY COATING MARKET SIZE AND FUTURE OUTLOOK

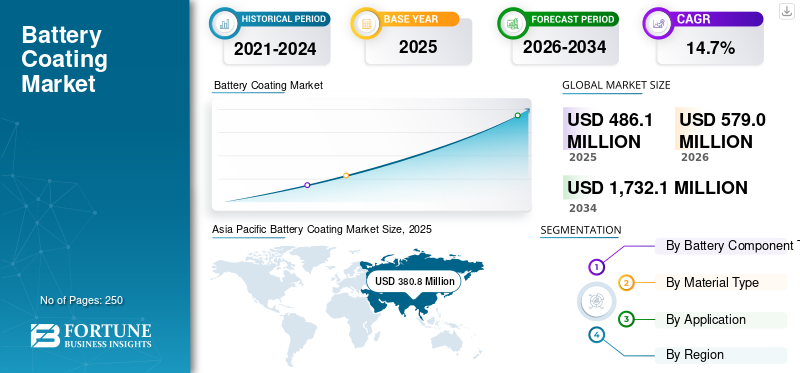

The global battery coating market size was valued at USD 486.1 million in 2025. The market is projected to grow from USD 579.0 million in 2026 to USD 1,732.1 million by 2034 at a CAGR of 14.7% during the forecast period. Asia Pacific dominated the battery coating market with a market share of 78.33% in 2025.

Battery coating is a specialized material layer applied to battery components such as cathodes, anodes, and separators to enhance electrochemical stability, thermal resistance, adhesion, and overall battery lifespan. These coatings play a critical role in lithium-ion and next-generation battery technologies by improving energy density, preventing short circuits, and enhancing safety performance. Among battery component types, cathode battery coating holds the leading share due to its direct impact on energy output and cycle life. The increasing adoption of electric vehicles (EVs), grid-scale energy storage systems, and portable electronics is accelerating demand for advanced battery coatings. Additionally, technological advancements in high-nickel cathodes and solid-state battery research are expanding battery coating material innovation. As performance expectations rise and battery architectures evolve, battery coating technologies are becoming increasingly critical to battery efficiency and durability, thereby strengthening the strategic importance of the market. The major key players operating in the market are Arkema S.A., Solvay S.A., Kureha Corporation, Shenzhen Capchem Technology Co., Ltd., ZEON Corporation, and JSR Corporation.

Download Free sample to learn more about this report.

BATTERY COATING MARKET Key Takeaways

- 2025 Market Size: USD 486.1 Million

- 2026 Market Size: USD 579.0 Million

- 2034 Forecast Market Size: USD 1,732.1 Million

- CAGR: 14.7% from 2026–2034

- Asia Pacific dominated the battery coating market with a 78.33% share in 2025.

- Cathode coating held the largest market share due to its critical role in improving battery energy density, cycle life, and thermal stability.

- PVDF led the market due to strong binding performance and lithium-ion battery compatibility.

Asia Pacific

Asia Pacific led the market in 2025, driven by EV production and battery manufacturing.

Europe

Europe’s growth is driven by EV adoption, gigafactory investments, and battery innovation.

North America

North America is expanding rapidly with growing domestic battery manufacturing, EV adoption, and government incentives supporting localized supply chains.

U.S.

The battery coating market reached USD 56.7 million in 2025.

Japan

The market generated USD 32.2 million in 2025.

Read More

BATTERY COATING MARKET TRENDS

High Energy Density Targets and Safety Standards Shaping Market Evolution

The market is evolving in response to growing energy density targets and stricter battery safety regulations. A major trend is the shift toward ceramic-coated separators to enhance thermal stability and prevent internal short circuits. Additionally, increasing the use of PVDF binders in cathode battery coating supports improved adhesion and electrochemical stability. The rise of high-nickel cathode chemistries requires advanced coating solutions to mitigate degradation and extend battery life. Sustainability trends are also influencing material selection, with aqueous polymer systems gaining attention for environmentally friendly processing. Furthermore, solid-state battery research is driving exploration of next-generation battery coating materials. These evolving technical and regulatory requirements are shaping material innovation and manufacturing processes, thus influencing the long-term direction of the battery coating market growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Regulatory Emphasis on Battery Safety & Durability Boosts Market Expansion

The primary driver of the market is the rapid expansion of electric vehicle production worldwide. Cathode battery coating enhances capacity retention and structural stability, while separator battery coating improves thermal safety, making them essential for high-energy-density batteries. Growing consumer demand for longer battery life and faster charging capabilities further strengthens adoption. Additionally, increased investment in gigafactories and battery manufacturing facilities ensures consistent coating demand. Rising regulatory emphasis on battery safety and durability also supports the adoption of advanced coating solutions. As battery technology continues to advance toward higher energy densities, coating materials become increasingly critical to performance optimization, thus sustaining robust growth in the market.

MARKET RESTRAINTS

High Material Costs and Manufacturing Complexity Limit Market Growth

The market faces restraints related to high material costs and complex manufacturing processes. Ceramic materials and fluoropolymers such as PVDF, are relatively expensive, thereby increasing overall battery production costs. Additionally, achieving uniform coating thickness and adhesion requires advanced equipment and precise process control. Variability in raw material supply and price fluctuations further impact profitability. Smaller battery manufacturers may face challenges in adopting advanced coating technologies due to capital constraints. Environmental regulations related to solvent-based coating processes also add compliance costs. These economic and operational limitations restrict rapid scalability, hence moderating overall market growth.

MARKET OPPORTUNITIES

Electrification and Renewable Integration Expanding Product Demand Scope

The global shift toward electrification presents substantial opportunities for the market. Rapid growth in electric vehicle production significantly increases demand for high-performance cathode and separator battery coating. Additionally, the expansion of renewable energy capacity drives the adoption of grid-scale energy storage systems, which requires durable and thermally stable battery components. Advancements in next-generation batteries, including solid-state and lithium-sulfur technologies, create opportunities for specialized coating materials with enhanced conductivity and chemical resistance. Government incentives for EV adoption and domestic battery manufacturing further support market expansion. Increasing focus on battery safety and lifecycle performance also promotes innovation in coating formulations. These structural drivers collectively create strong growth potential, therefore reinforcing long-term expansion prospects for the market.

MARKET CHALLENGES

Regional Demand Concentration and Logistics Constraints Affecting Market Stability

The market faces several challenges, including regional demand concentration and logistical limitations. Due to safety risks and high transportation costs, the product is typically consumed near production sites, limiting long-distance trade. This leads to regional oversupply in some markets and shortages in others. Another challenge is overcapacity in fertilizer-linked regions, which results in price pressure and margin volatility. Dependence on cyclical industries, such as agriculture, mining, and metals, further exposes the market to demand fluctuations. Additionally, aging infrastructure in certain regions increases maintenance costs and operational risks. These structural and logistical challenges require careful capacity planning and regional alignment strategies, which in turn affect overall market stability.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D activities focus on developing nano-ceramic battery coating, high-performance PVDF binders, and environmentally friendly aqueous systems. Innovations aim to enhance thermal stability, reduce degradation, and extend battery cycle life. These advancements strengthen long-term technological competitiveness.

SEGMENTATION ANALYSIS

By Battery Component Type

High Energy Density and Stability Requirements Driving Cathode Coating Segment Dominance

Based on battery component type, the market is segmented into separator coating, cathode coating, anode coating, and others.

Cathode coating represents the leading battery coating market share due to its direct impact on battery energy density, longevity, and electrochemical stability. Advanced coating enhances the structural integrity of high-nickel and lithium-rich cathode materials, reducing degradation during repeated charge–discharge cycles. With global EV production accelerating, demand for high-performance cathode materials continues to rise. Coating also mitigates surface reactivity and improves thermal stability, supporting fast-charging applications. Gigafactory expansions across Asia, North America, and Europe further strengthen demand for value.

Separator coating plays a vital role in enhancing battery safety by improving thermal resistance and preventing internal short circuits. Ceramic-coated separators are widely used in high-energy lithium-ion batteries to increase mechanical strength and heat tolerance. As battery capacities increase, the risk of thermal runaway becomes more significant, necessitating advanced separator technologies. Electric vehicle manufacturers increasingly adopt coated separators to meet stringent safety standards and regulatory requirements. The segment is expected to grow at a CAGR of 15.6% during the forecast period.

Anode coatings are gaining importance as battery manufacturers incorporate silicon-based materials to increase energy density. Silicon anodes offer higher capacity but suffer from volume expansion and structural degradation during cycling. Coating technologies help stabilize the anode surface, reduce side reactions, and improve lithium-ion diffusion efficiency. Growing research into advanced anode materials is driving innovation in polymer and ceramic-based coatings. The segment is projected to grow at a CAGR of 14.1% during the forecast period.

By Material Type

Superior Adhesion and Electrochemical Stability Sustaining Segment Leadership of Fluoropolymers

Based on material type, the market is segmented into ceramic materials, fluoropolymers (PVDF), aqueous polymers (SBR/CMC), and others.

Fluoropolymers (PVDF) remain the leading material type due to their strong binding properties and chemical resistance. It is extensively used as a binder in cathode coating, providing excellent adhesion between active materials and current collectors. Polyvinylidene fluoride enhances electrochemical stability and supports consistent charge–discharge performance. With lithium-ion battery production expanding globally, demand for PVDF-based coating continues to rise. Its compatibility with high-voltage cathode chemistries further strengthens adoption. While solvent-based processing raises environmental considerations, its performance advantages sustain widespread use. These structural advantages ensure the continued dominance of PVDF in battery manufacturing, thus maintaining its leadership position in the market.

Ceramic materials are widely used in separator coating to enhance thermal stability and prevent shrinkage at elevated temperatures. Their high heat resistance significantly reduces the risk of thermal runaway in lithium-ion batteries. Growing EV safety standards and stricter testing protocols support the adoption of ceramic-coated separators. The segment is projected to grow at a CAGR of 15.7% during the forecast period.

Aqueous polymer systems such as styrene-butadiene rubber (SBR) and carboxymethyl cellulose (CMC) are increasingly used as environmentally friendly alternatives to solvent-based binders. These water-based systems reduce volatile organic compound emissions and lower processing costs. Growing regulatory emphasis on sustainable manufacturing and green chemistry supports adoption. The segment is estimated to grow at a CAGR of 14.1% during the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rapid EV Production and High Energy Density Requirements Driving Dominant Demand

Based on application, the market is categorized into electric vehicles, energy storage systems, consumer electronics, and others.

Electric vehicles represent the leading application segment in the market due to their reliance on high-capacity, high-performance lithium-ion battery systems. EV batteries require advanced cathode coating to enhance energy density and cycle stability, while separator coating improves thermal safety under high operational loads. Increasing global EV adoption, supported by government incentives and emission regulations, continues to accelerate demand for coated battery components.

The energy storage systems segment is projected to grow at a CAGR of 14.1% from 2026 to 2034. Energy storage systems (ESS) are emerging as a key growth segment in the market due to increasing integration of renewable energy sources such as solar and wind. Grid-scale batteries require durable coating to enhance thermal management, prevent degradation, and extend operational lifespan under frequent cycling conditions. Separator and cathode coating are particularly important in large-format battery cells used for grid balancing and backup power systems. Government investments in renewable energy infrastructure and smart grid technologies are driving ESS deployment globally.

The consumer electronics segment is projected to grow at the highest CAGR of 13.3% from 2026 to 2034. Consumer electronics remain a significant application segment, driven by continuous innovation in smartphones, laptops, tablets, and wearable devices. These devices require compact batteries with high energy density and reliable thermal performance. Cathode coating improves charge retention and lifespan, while advanced binders enhance electrode adhesion and stability. As device manufacturers prioritize faster charging, longer battery life, and slimmer designs, coating technologies become increasingly important in maintaining performance consistency.

BATTERY COATING MARKET REGIONAL OUTLOOK

By geography, the market is studied into Asia Pacific, North America, Europe, and Rest of the World.

Asia Pacific

Asia Pacific Battery Coating Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the battery coating market due to its leadership in lithium-ion battery manufacturing and electric vehicle production. China, Japan, and South Korea host major battery manufacturers and gigafactories, driving large-scale demand for cathode and separator coating. Strong government incentives supporting EV adoption and domestic battery production further enhance growth. Additionally, the expansion of energy storage installations and consumer electronics manufacturing contributes to sustained demand. Vertical integration across battery supply chains strengthens cost competitiveness. Increasing investments in next-generation battery technologies further reinforce market expansion. These structural manufacturing advantages and strong regional demand ensure continued dominance, thus positioning Asia Pacific as the leading market for battery coating.

China Battery Coating Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues at USD 265.0 million, representing roughly 54.5% of market sales. The growth is driven by large-scale EV battery manufacturing capacity, strong government subsidies for electrification, and rapid expansion of domestic gigafactories.

India Battery Coating Market

The Indian market in 2025 was valued at USD 14.4 million, accounting for roughly 3.0% of revenues. Government-backed battery localization initiatives, rising EV adoption, and increasing investment in domestic lithium-ion cell production support the expansion.

Japan Battery Coating Market

The Japanese market in 2025 accounted for USD 32.2 million, accounting for roughly 6.6% of market revenues. The growth is fueled by advanced battery technology development, the strong presence of global battery manufacturers, and innovation in high-performance coating materials.

To know how our report can help streamline your business, Speak to Analyst

Europe

Europe’s market is expanding due to the rapid electrification of the automotive sector and strong sustainability regulations. The European Union’s focus on reducing carbon emissions and building domestic battery production capacity supports gigafactory development. Countries such as Germany and France are investing heavily in EV battery manufacturing facilities. Strict environmental standards also promote the adoption of aqueous polymer coating and sustainable processing technologies. The growth in renewable energy storage systems further supports demand.

U.K. Battery Coating Market

The U.K. market in 2025 reached USD 5.0 million, representing 1.0% of market revenues. The demand is supported by emerging gigafactory projects, automotive electrification policies, and investment in sustainable battery supply chains.

Germany Battery Coating Market

Germany’s market was valued at USD 13.86 million in 2025, equivalent to around 2.9% of market sales.

North America

North America is witnessing rapid growth in demand for battery coatings driven by increased domestic battery manufacturing investments. Government incentives promoting localized supply chains and EV adoption are encouraging gigafactory expansions in the U.S. Rising production of electric vehicles directly drives demand for cathode and separator coating. Additionally, grid-scale energy storage projects contribute to incremental consumption. Technological innovation and collaboration between material suppliers and battery manufacturers support the development of advanced coatings.

U.S. Battery Coating Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market reached a value of USD 56.7 million in 2025, accounting for roughly 11.7% of market sales. The expansion is supported by federal incentives for domestic battery production, gigafactory expansion, and strong EV market growth.

Rest of the World

The rest of the world includes Latin America, and the Middle East & Africa region. Latin America represents an emerging market driven by gradual EV adoption and renewable energy integration. While battery manufacturing capacity remains limited, growing investments in energy storage systems indirectly increase coating demand. On the other hand, the Middle East & Africa region is experiencing incremental growth supported by renewable energy projects and industrial diversification efforts. Increasing solar and energy storage installations drive demand for battery systems, indirectly supporting coating consumption. Moreover, the Government initiatives to localize advanced manufacturing create future opportunities.

Latin America Battery Coating Market

The GCC market reached USD 3.2 million in 2025, representing 0.7% of market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Rising Material Innovation and Battery Manufacturing Hubs by Key Players Strengthening the Market Position

BASF SE, Nouryon, The Mosaic Company, PVS Chemicals, Inc., and Aurubis AG are the key players in the market. The market is moderately consolidated, with competition driven by material innovation, vertical integration, and proximity to battery manufacturing hubs. Leading players include specialty chemical companies and battery material suppliers that provide PVDF binders, ceramic coating, and advanced polymer systems. Companies compete on coating performance, thermal stability, adhesion efficiency, and compatibility with evolving battery chemistries such as high-nickel and silicon-based electrodes. Strategic collaborations with battery manufacturers and long-term supply agreements with gigafactories enhance competitive positioning.

LIST OF KEY BATTERY COATING COMPANIES PROFILED

- Arkema S.A. (France)

- Solvay S.A. (Belgium)

- Kureha Corporation (Japan)

- Shenzhen Capchem Technology Co., Ltd. (China)

- ZEON Corporation (Japan)

- JSR Corporation (Japan)

- LG Chem Ltd. (South Korea)

- SK Innovation Co., Ltd. (South Korea)

- Sumitomo Chemical Co., Ltd. (Japan)

- Dongyue Group Limited (China)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Sumitomo Chemical announced the expansion of its battery materials business through increased investment in advanced components used in lithium-ion batteries. The initiative focuses on strengthening production capabilities for materials that enhance battery performance, safety, and durability, particularly for electric vehicle applications. By scaling up manufacturing capacity and reinforcing its supply chain network, the company aims to meet rising global demand driven by accelerating electrification and energy storage deployment.

- February 2025: Arkema has announced an increase in its PVDF production capacity in the U.S. to support the growing demand for lithium-ion battery materials, particularly from the electric vehicle sector. The expansion strengthens Arkema’s position as a key supplier of high-performance fluoropolymers used as binders in battery cathodes and separators.

- November 2022: LG Chem announced plans to expand its battery materials business by increasing cathode material production capacity to meet rapidly growing demand from the electric vehicle market. The company outlined investments aimed at strengthening its global supply network and enhancing competitiveness in advanced battery components. The expansion supports major automotive customers seeking stable, high-volume supplies of high-nickel cathode materials.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, battery component types, material types, and applications. Additionally, it provides valuable insights into the market and current industry trends, as well as highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Million), Volume (Kiloton) |

| Growth Rate | CAGR of 14.7% from 2026 to 2034 |

| Segmentation | By Battery Component Type, By Material Type, By Application, By Region |

| By Battery Component Type |

|

| By Material Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 486.1 million in 2025 and is projected to reach USD 1,732.1 million by 2034.

Recording a CAGR of 14.7%, the market is slated to exhibit steady growth during the forecast period.

By material type, the Fluoropolymers (PVDF) segment led in 2025.

Asia Pacific held the highest market share in 2025.

The growing consumer demand for longer battery life and faster charging capabilities further strengthens adoption.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us