Bicycle Component Market Size, Share & Industry Analysis, By Component (Frames, Wheels & Tires, Drivetrain Components, Braking Systems, and Others), By Bicycle Type (Mountain, Road, Hybrid, Cargo, and Others), By Material Type (Aluminum, Carbon Fiber, Steel, and Others), By Sales Channel (OEM and Aftermarket), By Distribution Channel (Online Retail and Offline Retail), By Propulsion Type (Conventional and E-bike), and Regional Forecast, 2026-2034

Bicycle Component Market Size and Future Outlook

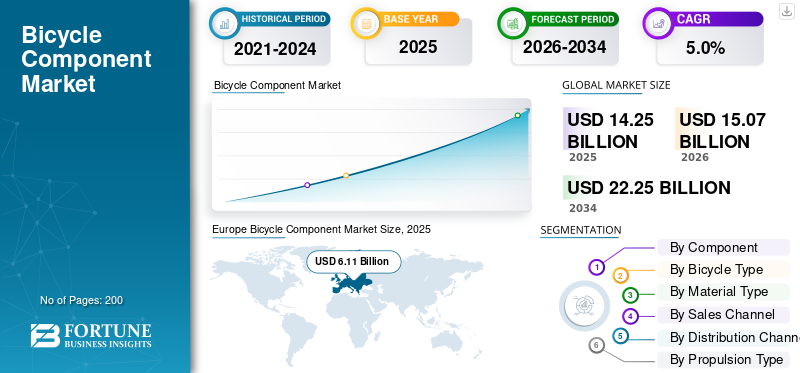

The global bicycle component market size was valued at USD 14.25 billion in 2025. The market is projected to grow from USD 15.07 billion in 2026 to USD 22.25 billion by 2034, exhibiting a CAGR of 5.0% during the forecast period. Europe dominated the bicycle component market with a market share of 42.88% in 2025.

The global market comprises the production, distribution, and sale of bicycle parts, including frames, drivetrains, wheels, brakes, suspension systems, and accessories. It spans OEM and aftermarket segments, serving road, mountain, hybrid, and electric bicycles. Market dynamics are influenced by urban mobility trends, cycling adoption, sustainability initiatives, and technological advancements in lightweight materials, performance, and smart connectivity worldwide, across developed and emerging regions, and by consumer preferences.

Key drivers of the market include rising health awareness, increased adoption of eco-friendly transportation, growth in urban commuting, and the expansion of e-bike adoption. Technological advancements in lightweight, high-performance components, supportive government policies, and growing cycling infrastructure further accelerate demand across both developed and emerging markets.

Major players in the market include Shimano Inc., SRAM LLC, Campagnolo S.r.l., Fox Factory Holding Corp., Trek Bicycle Corporation, and Giant Manufacturing Co., competing through lightweight materials, precision engineering, electronic shifting technologies, and integration of smart & performance-enhancing components to meet evolving consumer and professional cycling demands.

Download Free sample to learn more about this report.

Bicycle Component Market Key Takeaways

- 2025 Market Size: USD 14.25 billion

- 2026 Market Size: USD 15.07 billion

- 2034 Forecast Market Size: USD 22.25 billion

- CAGR: 5.0% from 2026–2034

- Europe dominated the bicycle component market with a 42.88% share in 2025.

- The carbon fiber segment is projected to grow at the fastest CAGR of 6.7% during the forecast period.

- The drivetrain components segment is anticipated to expand at a CAGR of 6.0% over the study period.

Europe

Europe led the global market in 2025, supported by strong cycling culture, growing e-bike adoption, and increasing investments in sustainable mobility infrastructure.

Asia Pacific

Asia Pacific held the second-largest market share, driven by rapid urbanization, rising demand for affordable transportation, and expanding bicycle manufacturing capabilities.

North America

North America ranked as the third-largest market due to increasing participation in recreational cycling, rising demand for premium bicycles, and growing e-bike adoption.

U.S.

The U.S. bicycle component market is witnessing steady growth supported by increasing interest in fitness cycling, outdoor sports, and premium bicycle customization trends.

Japan

Japan’s market is benefiting from rising demand for compact urban mobility solutions, advanced bicycle technologies, and growing adoption of electric bicycles.

Read More

BICYCLE COMPONENT MARKET TRENDS

Shift Toward Lightweight Materials and Electronic Integration to Enhance Performance

A key trend in the bicycle component market is growing emphasis on lightweight materials and electronic integration. Manufacturers are increasingly using carbon fiber, advanced alloys, and composite materials to reduce weight while maintaining strength and durability. Simultaneously, electronic shifting systems and wireless technologies are gaining traction among professional and enthusiast cyclists for improved precision and performance. These innovations are enhancing overall riding efficiency and user experience. The trend is also supported by rising participation in competitive cycling and demand for premium bicycles. As technology continues to evolve, component manufacturers are focusing on delivering high-performance, customizable, and aesthetically appealing products to stay competitive.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Urban Cycling Adoption and Sustainability Initiatives to Drive Component Demand

Increasing urbanization and congestion are prompting consumers to adopt bicycles as a convenient, eco-friendly mode of transportation. Governments and municipalities worldwide are promoting cycling through dedicated bike lanes, subsidies, and awareness campaigns to reduce carbon emissions. This shift is significantly boosting demand for reliable and high-performance bicycle components. Additionally, the growing popularity of fitness-oriented lifestyles is accelerating bicycle use across demographics. As more consumers turn to cycling for commuting and recreation, the need for durable, lightweight, and efficient components continues to rise. This sustained demand for both conventional and electric bicycles is a major driver of bicycle component market growth.

MARKET RESTRAINTS

High Cost of Advanced Components and Price Sensitivity to Limit Market Penetration

Despite growing demand, the high cost of advanced bicycle components poses a significant restraint on market growth. Premium materials such as carbon fiber, along with sophisticated technologies such as electronic shifting systems, increase overall product prices—this limits accessibility, particularly in price-sensitive markets across developing regions. Many consumers continue to prefer low-cost alternatives or refurbished components, which affects the adoption of high-end products. Additionally, fluctuations in raw material costs and supply chain disruptions can further raise prices, creating uncertainty for manufacturers and end users alike. As affordability remains a key concern, especially among entry-level and casual cyclists, this factor continues to restrict widespread market penetration.

MARKET OPPORTUNITIES

Expansion of E-Bikes and Smart Cycling Solutions to Create New Growth Avenues

The rapid growth of electric bicycles (e-bikes) is creating significant opportunities within the market. E-bikes require specialized components such as motors, sensors, batteries, and advanced drivetrains, opening new revenue streams for manufacturers. Furthermore, the integration of smart technologies, including GPS tracking, performance monitoring, and connectivity features, is enhancing user experience and attracting tech-savvy consumers. Emerging markets are also witnessing increased adoption due to improving infrastructure and rising disposable incomes. Manufacturers are investing in innovation to develop compatible and efficient components tailored for e-bikes. This evolution is not only expanding product portfolios but also reshaping the competitive landscape, offering long-term growth potential.

MARKET CHALLENGES

Supply Chain Disruptions and Component Standardization Issues to Challenge Market Stability

The market faces ongoing challenges, including supply chain disruptions and a lack of standardization across components. Global events, logistics constraints, and dependency on specific manufacturing hubs can lead to delays and inventory shortages. Additionally, varying specifications and compatibility issues between components from different manufacturers create complexity for both consumers and assemblers. This lack of uniform standards can hinder product interchangeability and increase maintenance difficulties. Smaller manufacturers, in particular, struggle to align with evolving technical requirements and global distribution networks. These factors collectively impact production efficiency, increase operational costs, and pose challenges in maintaining consistent product availability and high-quality components across global markets.

Segmentation Analysis

By Component

Widespread Usage Across Bicycle Types and Replacement Cycles to Drive Frame Segment Dominance

Based on component, the market is categorized into frames, wheels & tires, drivetrain components, braking systems, and others.

The frames segment dominates the bicycle component market share due to its fundamental role in structural integrity and compatibility across all bicycle types, including road, mountain, and electric bicycles. Frames account for a significant share of overall component value and are frequently upgraded to improve performance, reduce weight, and enhance durability. Rising demand for lightweight materials such as aluminum and carbon fiber further strengthens segment growth. Additionally, the OEM production volumes and customization trends sustain consistent global demand.

The drivetrain components segment is set to be the grow with the fastest growing CAGR of 6.0% over the forecast period. Increasing adoption of e-bikes and demand for high-performance gear systems are driving growth, supported by innovations in electronic shifting and efficiency-focused component designs.

By Bicycle Type

Versatility and Urban Commuting Demand to Strengthen Hybrid Bicycle Segment Dominance

Based on bicycle type, the market is categorized into mountain, road, hybrid, cargo, and others.

The hybrid segment dominates the bicycle market due to its versatility, combining features of road and mountain bikes to suit both urban commuting and recreational use. These bicycles are widely adopted across diverse consumer groups for daily travel, fitness, and leisure activities. Their comfort, durability, and adaptability across varied terrains drive consistent global demand. Additionally, growing urbanization and the preference for cost-effective mobility solutions further support the segment's dominance.

The road segment is projected to be the fastest-growing with a CAGR of 5.9% during the forecast period. Increasing interest in fitness cycling, long-distance riding, and competitive sports, along with demand for lightweight and high-speed bicycles, is accelerating growth in this segment.

To know how our report can help streamline your business, Speak to Analyst

By Material Type

Cost Efficiency and Lightweight Performance to Drive Aluminum Segment Dominance

Based on material type, the market is categorized into aluminum, carbon fiber, steel, and others.

The aluminum segment dominates the market due to its optimal balance between cost, weight, and durability. Aluminum is widely used across mid-range and premium bicycles, making it highly preferred by both manufacturers and consumers. Its corrosion resistance, ease of manufacturing, and affordability compared to carbon fiber support large-scale adoption. Additionally, its application across frames, wheels, and other components ensures consistent demand. Growing urban cycling and mass-market bicycle production further reinforce aluminum’s dominance globally.

The carbon fiber segment is set to be the fastest-growing segment with a CAGR of 6.7% over the forecast period. Increasing demand for ultra-lightweight, high-performance bicycles, particularly in road and professional cycling, along with advancements in composite technologies, is driving rapid adoption of carbon fiber components.

By Sales Channel

High OEM Integration and Large-Scale Bicycle Production to Drive Segment Dominance

Based on the sales channel, the market is bifurcated into OEM and Aftermarket.

The OEM segment dominates the market due to strong demand from large-scale bicycle manufacturers integrating components during initial production. OEMs ensure standardization, performance compatibility, and cost efficiency, making them the primary distribution channel for frames, drivetrains, and braking systems. Rising global bicycle production, especially in Asia-Pacific and Europe, further strengthens this dominance. Additionally, partnerships between component manufacturers and bicycle brands support continuous innovation and bulk procurement, ensuring steady demand through OEM channels.

The aftermarket segment is expected to grow with a CAGR of 5.7% during the forecast period. Increasing replacement cycles, customization trends, and rising maintenance needs are driving demand for upgraded and performance-enhancing bicycle components.

By Distribution Channel

Strong Retail Network and Consumer Preference for Physical Inspection to Drive Offline Segment Dominance

Based on the distribution channel, the market is categorized into Online Retail and Offline Retail.

The offline retail segment dominates the market due to the strong presence of specialty stores, dealerships, and service workshops offering hands-on product experience. Consumers prefer offline channels for component compatibility checks, expert guidance, and immediate availability. Additionally, professional installation and after-sales services provided by physical stores enhance customer trust. The widespread network of independent retailers and authorized distributors further ensures consistent sales, particularly in developing markets.

The online retail segment is gaining traction with a growing share, driven by increasing e-commerce adoption and digital convenience. Wider product availability, competitive pricing, and direct-to-consumer strategies are encouraging cyclists to purchase components online. The segment is expected to hold a CAGR of 5.7% during the forecast period.

By Propulsion Type

Large Installed Base and Affordability to Drive Conventional Bicycle Segment Dominance

Based on propulsion type, the market is categorized into conventional and e-bike.

The conventional segment dominates the market due to its large global installed base and widespread affordability. Conventional bicycles are extensively used for daily commuting, recreation, and fitness across both developed and emerging markets. Lower acquisition and maintenance costs compared to e-bikes support higher adoption, especially in price-sensitive regions. Additionally, the steady replacement demand for essential components such as chains, brakes, and tires sustains consistent aftermarket growth. The simplicity of conventional systems also makes servicing easier and increases accessibility, reinforcing their continued dominance.

The e-bike segment is expected to witness a rapid growth with a CAGR of 5.9% during the forecast period, driven by rising demand for assisted mobility and urban commuting solutions. Increasing adoption of electric bicycles, supported by government incentives and advancements in battery and motor technologies, is accelerating demand for specialized components.

Bicycle Component Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Europe

Europe Bicycle Component Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe dominates the market due to its well-established cycling culture, extensive bike-friendly infrastructure, and strong government support for sustainable mobility. Countries such as Germany, the Netherlands, and Denmark exhibit high bicycle penetration for daily commuting and recreation. Additionally, favorable regulations, subsidies for e-bikes, and growing environmental awareness further boost demand. The presence of leading component manufacturers and a mature aftermarket ecosystem ensures continuous innovation, replacement demand, and premium product adoption, reinforcing Europe’s leading position in the global market.

Germany Bicycle Component Market

The German market in 2026 is estimated at around USD 2.33 billion, accounting for a significant share of global bicycle component revenues. High e-bike penetration, strong OEM presence, and advanced cycling culture support sustained growth and innovation.

Italy Bicycle Component Market

The Italian market in 2026 is estimated at around USD 0.68 billion, accounting for a notable share of global bicycle component revenues. Strong cycling infrastructure, rising e-bike adoption, and increasing fitness trends continue to drive steady component demand.

Asia Pacific

The Asia Pacific market holds the second-largest share of the market and is projected to grow at a CAGR of 5.3% over the forecast period. Rapid urbanization, increasing population density, and rising demand for cost-effective transportation are driving bicycle adoption. Countries such as China, India, and Japan are witnessing strong growth in both conventional and electric bicycles. Additionally, expanding manufacturing capabilities and government initiatives promoting clean mobility further support market expansion. The growing middle-class population and increasing fitness awareness also contribute to the rising demand for bicycle components.

China Bicycle Component Market

The Chinese market in 2026 is estimated at around USD 2.73 billion, accounting for a major share of global bicycle component revenues. Large-scale manufacturing, strong domestic demand, and rapid e-bike adoption are driving market expansion.

North America

North America is the third-largest market, driven by rising participation in recreational cycling, fitness, and outdoor sports. The U.S. and Canada are witnessing growing consumer interest in premium bicycles and high-performance components. Additionally, the rising popularity of e-bikes for urban commuting and leisure is contributing to market growth. While infrastructure development is progressing gradually, supportive policies and increasing awareness of sustainable transportation are encouraging adoption. Strong aftermarket demand and customization trends further sustain steady growth in the region.

U.S. Bicycle Component Market

The U.S. market in 2026 is estimated at around USD 1.57 billion, accounting for a considerable share of global bicycle component revenues. Growing recreational cycling, premium bike demand, and increasing e-bike adoption are fueling consistent aftermarket and OEM growth.

Rest of the World

The Rest of the World region is experiencing gradual growth, supported by increasing awareness of cycling as an affordable and eco-friendly transportation option. Regions such as Latin America, the Middle East, and Africa are witnessing rapid urbanization and increased investment in cycling infrastructure. Government initiatives promoting health and sustainability, along with growing interest in recreational cycling, are contributing to market expansion. Although the market is still developing, improving economic conditions and expanding distribution networks are expected to drive steady demand for bicycle components in the coming years.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation, Strategic Partnerships, and Aftermarket Expansion Intensifying Competitive Landscape

The global bicycle component market is characterized by intense competition among established players and emerging manufacturers, with a focus on innovation, performance, and product differentiation. Leading companies such as Shimano Inc., SRAM LLC, and Campagnolo S.r.l. dominate through strong brand positioning, extensive product portfolios, and continuous investment in advanced technologies such as electronic shifting and lightweight materials. Strategic partnerships with bicycle OEMs and sponsorship of professional cycling events further strengthen their global market presence and brand visibility.

Additionally, companies are increasingly focusing on expanding their aftermarket presence and direct-to-consumer channels to boost revenue. Regional players, particularly in the Asia Pacific, compete on cost efficiency and large-scale manufacturing capabilities, intensifying price competition. Innovation in e-bike components, smart integration, and sustainability-driven materials is becoming a key competitive differentiator. Furthermore, mergers, acquisitions, and product launches are commonly adopted strategies to strengthen market positioning and expand geographic reach in this evolving and dynamic market landscape.

LIST OF KEY BICYCLE COMPONENT COMPANIES PROFILED

- Shimano Inc. (Japan)

- SRAM LLC (U.S.)

- Campagnolo S.r.l. (Italy)

- Fox Factory Holding Corp. (U.S.)

- Giant Manufacturing Co. (Taiwan)

- Trek Bicycle Corporation (U.S.)

- DT Swiss (Switzerland)

- Merida Industry Co., Ltd. (Taiwan)

- Magura GmbH (Germany)

- Bosch eBike Systems (Germany)

KEY INDUSTRY DEVELOPMENTS

- March 2026: SRAM LLC launched an upgraded e-bike drivetrain platform integrating advanced sensor-based shifting technology, targeting improved efficiency and durability for urban mobility and cargo bike applications across Europe and North America.

- February 2026: Shimano Inc. announced the expansion of its electronic shifting lineup, introducing next-generation wireless drivetrain systems aimed at enhancing precision and performance for both road and mountain bicycles globally.

- January 2026: Giant Manufacturing Co. expanded its component manufacturing capacity in Taiwan, focusing on lightweight aluminum and carbon fiber parts to meet rising global demand for high-performance and electric bicycles.

- December 2025: Bosch eBike Systems introduced a new smart system upgrade featuring enhanced connectivity, over-the-air updates, and integrated performance tracking, strengthening its position in the growing e-bike component ecosystem.

- December 2025: Bikone introduced a new lightweight, aero bottom bracket for Tadej Pogačar and UAE Team Emirates-XRG. This new unit is the lightest the brand has ever produced at 77 grams, 15 grams lighter than the previous unit, and for comparison, about 3 grams lighter than the CeramicSpeed BB Alpha.

- November 2025: Fox Factory Holding Corp. launched advanced suspension systems designed for electric mountain bikes, improving shock absorption and durability while addressing the increasing demand for high-performance off-road cycling components.

- October 2025: Ceramic Speed launched a brand new bottom bracket range today, named the BB Alpha, which will replace all existing CeramicSpeed bottom brackets and become the brand's new standard. The BB Alpha units represent a complete overhaul of the current CeramicSpeed bottom bracket offering.

REPORT COVERAGE

The global bicycle component market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, By Bicycle Type, By Material Type, By Sales Channel, By Distribution Channel, By Propulsion Type, and By Region |

| By Component |

|

| By Bicycle Type |

|

| By Material Type |

|

| By Sales Channel |

|

| By Distribution Channel |

|

| By Propulsion Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 14.25 billion in 2025 and is projected to reach USD 22.25 billion by 2034.

In 2025, the market value stood at USD 6.11 billion.

The market is expected to exhibit a CAGR of 5.0% during the forecast period.

The hybrid segment led the market by bicycle type.

Rising urban cycling adoption and sustainability initiatives to drive component demand.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us