Bicycle Roller Brake Market Size, Share & Industry Analysis, By Product (Standard Roller Brakes, High-Performance Roller Brakes, Integrated Hub-Gear Roller Brakes, and Coaster Brakes), By Brake (Mechanical and Hydraulic), By Bicycle Type (Conventional and E-bike), By Application (Mountain, Road, Hybrid, Cargo, and Others) and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

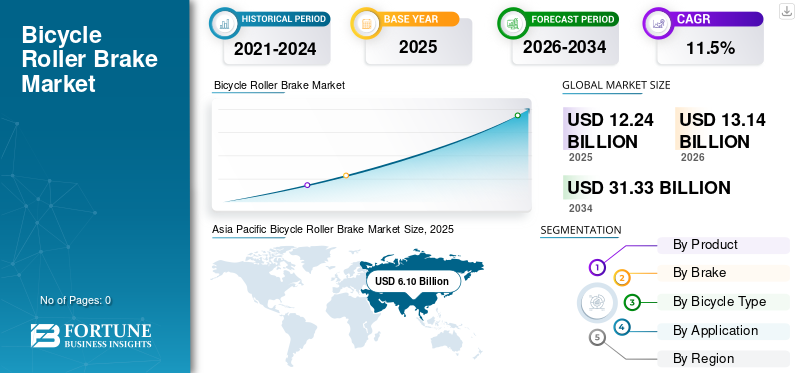

Bicycle Roller Brake Market Size and Future Outlook

The global bicycle roller brake market size was valued at USD 12.24 billion in 2025. The market is projected to grow from USD 13.14 billion in 2026 to USD 31.33 billion by 2034, exhibiting a CAGR of 11.5% during the forecast period. Asia Pacific dominated the bicycle roller brake market with a market share of 49.84% in 2025.

The bicycle roller brake industry involves the manufacturing, distribution, and sale of roller brake systems for bicycles. Roller brakes are enclosed braking mechanisms, typically integrated with the hub, offering low maintenance, consistent performance, and durability. This market serves commuter, city, and utility bicycles, driven by demand for reliable, weather-resistant braking solutions.

Key growth drivers of the market include rising urban cycling for commuting, demand for low-maintenance braking systems, growth of city and utility bicycles, increasing focus on rider safety, and preference for durable, weather-resistant components, especially in regions with high daily bicycle usage and varying climatic conditions.

Major players in the market include Shimano, Tektro, Sturmey-Archer, SunRace, and Promax, competing through durable brake designs, low-maintenance systems, integration with hub assemblies, improved heat dissipation, and enhanced safety performance for urban and commuter bicycles.

Download Free sample to learn more about this report.

Bicycle Roller Brake Market Key Takeways

- 2025 Market Size: USD 12.24 billion

- 2026 Market Size: USD 13.14 billion

- 2034 Forecast Market Size: USD 31.33 billion

- CAGR: 11.5% from 2026–2034

- Asia Pacific dominated the bicycle roller brake market with a 49.84% share in 2025.

- The standard roller brakes segment held the largest market share due to widespread adoption in commuter and utility bicycles.

- The mechanical brake segment accounted for the largest share, supported by its affordability, reliability, and easy maintenance.

Asia Pacific

Asia Pacific is the largest and fastest-growing regional market, driven by high bicycle ownership and expanding e-bike adoption.

Europe

Europe is the second-largest market, supported by strong cycling infrastructure and growing commuter bicycle demand.

North America

North America is the third-largest market, fueled by increasing urban cycling and shared mobility adoption.

U.S.

U.S. The U.S. bicycle roller brake market is estimated at USD 1.83 billion in 2026, driven by rising demand for commuter and electric bicycles.

Japan

Japan Japan remains a key market due to its high bicycle commuting rate and strong demand for durable, low-maintenance braking systems.

Read More

BICYCLE ROLLER BRAKE MARKET TRENDS:

Integration of Low-Maintenance Designs is a Key Market Trend

A prominent trend in the market is the growing focus on low-maintenance, long-lasting braking solutions. Manufacturers are investing in improved materials, better heat management, and sealed mechanisms to enhance durability and consistency. As urban cyclists and fleet operators seek hassle-free ownership, roller brake designs are being optimized for extended service intervals without frequent adjustments. This trend aligns with broader consumer preferences for convenience and reliability over high performance. Additionally, integration of roller brakes with hub gear systems is gaining traction, simplifying bicycle architecture and supporting the demand for clean, enclosed drivetrains in city and commuter bicycles.

- In June 2025, NYC DOT’s Citi Bike expansion plan (2025–2026) outlined +250 stations and +2,900 bikes, expanding coverage and increasing fleet scale, favoring durable, low-service braking solutions for high-usage shared bikes.

MARKET DYNAMICS

MARKET DRIVERS:

Rising Urban Commuting and Utility Cycling to Drive Roller Brake Adoption

The increasing shift toward bicycles as a primary mode of urban transportation is a major driver for the market. Rapid urbanization, traffic congestion, and policies promoting sustainable mobility have encouraged bicycle commuting, especially in Europe and parts of Asia. Roller brakes are well suited for this application due to their enclosed design, consistent braking performance, and minimal maintenance requirements. Unlike rim brakes, they are less affected by rain, dust, and road grime, making them ideal for year-round city use. Growing investments in cycling infrastructure, such as bike lanes and shared mobility programs, further boost demand for durable, reliable braking systems on commuter and utility bicycles. These factors drive the bicycle roller brake market growth.

- For instance, in January 2026, PeopleForBikes highlighted multiple new protected bike-lane projects completed in 2025 across U.S. cities, reflecting continued investment in safer cycling infrastructure that supports everyday commuting demand.

MARKET RESTRAINTS:

Limited High-Performance Appeal to Restrain Market Expansion

Despite their advantages, roller brakes face limited adoption due to their limited appeal in high performance and sports cycling segments. Compared to disc brakes and advanced rim brakes, roller brakes offer lower braking power and heat dissipation, making them less suitable for high-speed riding, steep terrains, or competitive cycling. Enthusiast and professional cyclists often prioritize lightweight components and superior modulation, areas where roller brakes lag. As performance bicycles gain popularity globally, bicycle manufacturers tend to favor disc brake systems, limiting roller brake penetration beyond urban and recreational categories. This constraint narrows the overall addressable market and slows adoption in premium bicycle segments.

MARKET OPPORTUNITIES:

Growth of E-Bikes and Shared Mobility Fleets to Create New Opportunities

The rapid expansion of electric bicycles and shared mobility fleets presents a strong opportunity for the market. E-bikes used for urban commuting and rental services require braking systems that are durable, weather-resistant, and reliable, with minimal servicing requirements. Roller brakes meet these needs through enclosed construction and long service intervals. Fleet operators prioritize reduced maintenance costs and operational downtime, making roller brakes an attractive solution. Additionally, government-supported bike-sharing programs in urban centers are driving bulk procurement of standardized, low-maintenance bicycles, creating sustained demand for roller brake systems in both OEM and aftermarket channels.

Download Free sample to learn more about this report.

MARKET CHALLENGES:

Balancing Heat Management and Cost Efficiency to Challenge Manufacturers

One of the key market challenges is achieving effective heat dissipation while maintaining cost competitiveness. Roller brakes are enclosed systems, which can lead to heat buildup during prolonged braking, especially on heavier bicycles or in stop-and-go urban traffic. Enhancing thermal performance requires advanced materials and design improvements, which can increase manufacturing costs. At the same time, roller brakes are typically positioned as economical solutions for mass-market bicycles. Manufacturers must balance performance upgrades with price sensitivity, particularly in emerging markets, without compromising reliability or safety standards.

Segmentation Analysis

By Product

Low-Cost Reliability and Urban Utility Usage to Drive Standard Roller Brakes Segment Dominance

Based on product, the market is divided into standard roller brakes, high-performance roller brakes, integrated hub-gear roller brakes, and coaster brakes.

The standard roller brakes segment dominates the market due to its widespread use in city, commuter, and utility bicycles. These brakes offer enclosed construction, consistent performance, and minimal maintenance, making them ideal for daily urban riding and shared mobility fleets. High increased adoption across Europe and Asia, coupled with OEM preference for cost-effective braking systems, sustains steady replacement demand in both OEM and aftermarket channels.

High-performance roller brakes represent the second largest bicycle roller brake market share and the fastest-growing segment, projected to expand at a CAGR of 12.5% over the forecast period. Rising adoption in premium urban e-bikes and heavier commuter bicycles is driving demand for improved heat dissipation, enhanced braking power, and durability without compromising low-maintenance benefits.

By Brake

Cost Efficiency and Ease of Maintenance to Support Mechanical Brake Segment Dominance

In terms of brake, the market is categorized into mechanical and hydraulic.

The mechanical brake segment dominates the market due to its simple design, affordability, and ease of installation and maintenance. These systems are widely adopted in commuter, city, and utility bicycles, particularly in cost-sensitive markets. Strong OEM integration, reliable performance under daily urban use, and widespread service familiarity support sustained demand across mass-market bicycles.

Hydraulic roller brakes are the fastest-growing segment, expected to register a CAGR of 14.6% during the forecast period. Growing penetration of premium e-bikes and heavier urban bicycles is driving adoption due to superior braking force, smoother modulation, and improved safety performance.

By Bicycle Type

Established User Base and Cost-Sensitive Demand to Sustain Conventional Bicycle Dominance

Based on bicycle type, the market is segmented into conventional and e-bike.

The conventional bicycle segment dominates the market due to its large installed base across urban and semi-urban regions. Affordable pricing, simple drivetrain compatibility, and low maintenance requirements make roller brakes well suited for conventional city and utility bicycles. Strong penetration in developing markets and continued OEM fitment ensure stable replacement demand.

E-bikes are the fastest-growing segment, expected to register a CAGR of 12.8% over the forecast period. Rising urban electrification, shared e-mobility programs, and demand for durable, low-service braking systems are accelerating roller brake adoption in e-bikes.

By Application

Versatile Urban Usage and Commuter Preference to Anchor Hybrid Segment Dominance

Based on application, the market is segmented into mountain, road, hybrid, cargo and others.

The hybrid application segment dominates the market due to its strong presence in urban commuting and recreational cycling. Hybrid bicycles balance comfort, durability, and practicality, making them ideal for daily use where low-maintenance, weather-resistant roller brakes are preferred. High adoption in city commuting, shared mobility programs, and personal transportation supports consistent OEM demand and steady aftermarket replacement volumes.

The road segment is the fastest growing, projected to expand at a CAGR of 12.7% during the forecast period. Increasing adoption of road-style commuter bicycles and performance-oriented urban bikes is driving demand for lighter, smoother-operating roller brake systems.

To know how our report can help streamline your business, Speak to Analyst

Bicycle Roller Brake Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific Bicycle Roller Brake Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

Asia Pacific dominates and remains the fastest-growing region in the market, supported by high bicycle ownership, dense urban populations, and strong demand for low-maintenance mobility solutions. Countries such as China, Japan, and India rely heavily on bicycles for daily commuting, shared mobility, and last-mile transport. OEM preference for cost-effective, durable braking systems and expanding e-bike adoption further accelerate growth, supported by government initiatives promoting sustainable urban transportation.

China Bicycle Roller Brake Market

The Chinese market in 2026 is estimated at around USD 2.30 billion, led by commuter bicycle parc, strong OEM sourcing, and shared-mobility fleets, sustaining roller brake demand.

India Bicycle Roller Brake Market

The Indian market in 2026 is estimated at around USD 1.80 billion, growing fastest in urban mobility, bicycles, expanding e-bike adoption, and maintenance-light braking preference in cities.

Europe

Europe represents the second-largest market, projected to grow at a CAGR of 10.4% over the forecast period, driven by a well-established cycling culture and advanced urban infrastructure. High penetration of commuter and utility bicycles, coupled with strict safety and durability standards, supports roller brake adoption. Growing investments in cycling lanes, the expansion of e-bike adoption, and strong aftermarket demand in countries such as Germany, the Netherlands, and France continue to reinforce regional market stability and growth.

Germany Bicycle Roller Brake Market

The German market in 2026 is estimated at around USD 0.39 billion, supported by commuter cycling, safety expectations, and replacement cycles, which favor enclosed brakes for dependable riding.

Italy Bicycle Roller Brake Market

The Italian bicycle roller brake market in 2026 is estimated at around USD 0.62 billion, aided by city-bike demand, the adoption of integrated hub gears, and aftermarket networks, which sustains adoption in everyday segments.

North America

North America ranks as the third-largest market, supported by rising interest in urban cycling, recreational biking, and electric bicycles. Increasing congestion, sustainability awareness, and city-level investments in cycling infrastructure are encouraging bicycle usage beyond leisure. Roller brakes are in demand in shared mobility fleets and commuter bicycles, where low maintenance is critical. While disc brakes dominate performance segments, steady OEM and aftermarket demand support gradual regional expansion.

U.S. Bicycle Roller Brake Market

The U.S. market in 2026 is estimated at around USD 1.83 billion, driven by e-bike commuting, bike-share fleets, and preference for low-maintenance braking, while disc brakes remain dominant.

Rest of the World

The rest of the world market, including Latin America, the Middle East, and Africa, is experiencing gradual growth driven by rising demand for affordable and durable transportation. Urbanization, rising fuel costs, and limited public transit infrastructure are driving increased bicycle use for daily commuting. Roller brakes benefit from their simplicity and low servicing needs, particularly in cost-sensitive markets, supporting incremental adoption through OEM installations and replacement demand.

COMPETITIVE LANDSCAPE

Key Industry Players

OEM-Centric Competition, Reliability-Led Product Positioning,Incremental Innovation and Fleet-Oriented Differentiation Strategies Drives Market Expansion

The bicycle roller brake market is moderately consolidated, with competition driven by product reliability, cost efficiency, and long-term OEM relationships rather than rapid technological disruption. Key players such as Shimano, Sturmey-Archer, and Tektro leverage strong brand equity, integrated component portfolios, and established manufacturing scale. Their strategies focus on standardized roller brake systems optimized for commuter, city, and utility bicycles. A broad geographic presence, compatibility with hub gears, and consistent performance across varied weather conditions strengthen their positioning, particularly in high-volume Asia Pacific and Europe.

Competitive dynamics are increasingly influenced by rising demand from e-bikes and shared mobility fleets, encouraging manufacturers to enhance durability, thermal performance, and load-handling capability. Mid-sized and regional players compete by offering cost-competitive solutions tailored to local market requirements, especially in emerging economies. Innovation remains incremental, emphasizing improved materials, brake technologies, and integrated hub solutions. With disc brakes dominating performance segments, competition within roller brakes centers on lifecycle cost optimization, reduced maintenance needs, and sustained relevance in urban mobility applications.

LIST OF KEY BICYCLE ROLLER BRAKE COMPANIES PROFILED:

- Campagnolo (Italy)

- Clarks Cycle Systems (U.S.)

- Hayes Performance Systems (U.S.)

- Hope Technology (IPCO) (U.K.)

- Magura (Germany)

- Promax Components (U.S.)

- Shimano (Japan)

- SRAM (U.S.)

- Tektro Technology (Taiwan)

- Alhonga (Taiwan)

KEY INDUSTRY DEVELOPMENTS:

- March 2026: Tektro announced capacity optimization across its braking portfolio to support rising global bicycle production, with emphasis on cost-efficient mechanical and hydraulic systems designed for commuter, hybrid, and e-bike applications in high-volume markets.

- February 2026: TRP (Tektro’s high-end brand) showcased its 2026 brake range at Eurobike Frankfurt 2025, highlighting innovations across racing, MTB, and urban braking tech.

- January 2026: Cyclonline previewed new 2026 bike models across road, MTB, gravel, and e-bike categories, signaling heightened demand for component innovation.

- November 2025: Sturmey-Archer reported renewed OEM interest in integrated hub and brake assemblies, driven by expanding shared mobility fleets and city bicycles prioritizing reliability, simplified drivetrain integration, and reduced servicing intervals.

- September 2025: Shimano expanded its urban mobility component strategy, focusing on braking systems compatible with hub gears and electric bicycles, reflecting increased procurement from European city bike manufacturers and public bike-sharing operators.

- July 2025: SunRace increased production of commuter-focused braking components to meet rising demand from Asian OEMs, supported by sustained bicycle usage for daily transport and growth in entry-level and mid-range urban bicycles.

- April 2025: Tektro unveiled the EVO PRO & EVO X hydraulic disc brakes, targeting improved modulation and control.

REPORT COVERAGE

The global bicycle roller brake market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTES | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.5% from 2026-2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Product

By Brake

By Bicycle Type

By Application

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 12.24 billion in 2025 and is projected to reach USD 31.33 billion by 2034.

In 2025, the Asia Pacific’s market value stood at USD 6.10 billion.

The market is expected to exhibit a CAGR of 11.5% during the forecast period.

The conventional segment is leading the market by bicycle type.

Rising urban commuting and utility cycling are the key factors driving the market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 0

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us