Biodegradable Paper & Plastic Packaging Market Size, Share & Industry Analysis, By Material (Plastic and Paper), By Type (Starch Based Plastic, Cellulose Based Plastic, Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Paper & Paperboard, and Others), By End Users (Food & Beverages, E-commerce, Healthcare, Personal Care & Cosmetics, Agriculture, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

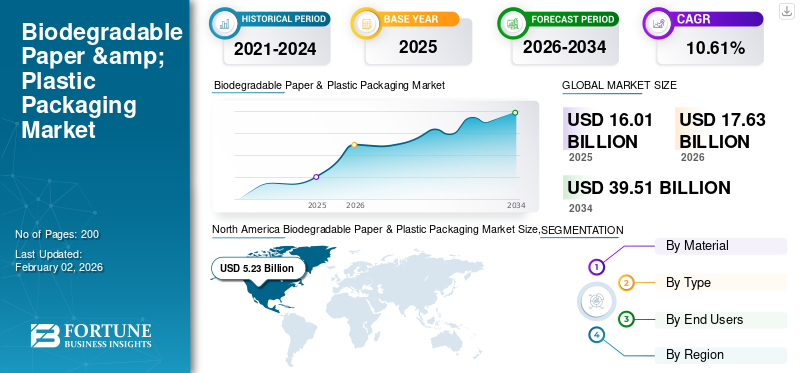

The global biodegradable paper & plastic packaging market size was valued at USD 16.01 billion in 2025. The market is projected to grow from USD 17.63 billion in 2026 to USD 39.51 billion by 2034, exhibiting a CAGR of 10.61% during the forecast period. North America dominated the biodegradable paper & plastic packaging market with a market share of 32.68% in 2025.

Biodegradable paper & plastic packaging are environmentally friendly materials engineered to break down into non-harmful elements such as water, carbon dioxide, and biomass through the action of microorganisms in certain environmental settings. The primary advantage of using biodegradable paper and plastic packaging is their natural decomposition, which helps lessen ongoing pollution and the buildup of waste in landfills. These biodegradable packaging materials decompose within a few months, substantially reducing the ecological harm inflicted by conventional plastics, which can last for hundreds of years.

The market encompasses several key players, Smurfit Kappa, Mondi, and Amcor, at the forefront. Broad portfolio with innovative product launch, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Environmental Concerns and Government Regulations Drive Market Growth

The rising awareness of environmental issues among consumers and the enforcement of strict government regulations aimed at reducing plastic waste are significant factors driving the market for biodegradable paper and plastic packaging. Numerous nations have enacted bans or limitations on single-use plastics, encouraging industries to transition toward eco-friendly alternatives. Biodegradable materials break down naturally, which helps to reduce pollution and the amount of waste in landfills. Additionally, the growing consumer preferences for eco-friendly packaging options in sectors such as food and beverage, healthcare, and personal care are fueling market expansion. For example, businesses are making substantial investments in compostable and recyclable packaging to satisfy both regulatory requirements and their sustainability goals.

MARKET RESTRAINTS

High Production Costs and Limited Material Performance Hampers Market Growth

Although demand is on the rise, the market encounters challenges due to the comparatively higher expense of biodegradable materials compared to traditional plastics. The manufacturing of biodegradable packaging frequently requires sophisticated technologies and raw materials sourced from nature, such as corn starch, polylactic acid (PLA), or cellulose, which drives up production costs. Furthermore, biodegradable plastics may have lower barrier properties, diminished durability, and a shorter shelf life, making them less appropriate for certain uses, such as extended food storage or environments with high moisture. These performance limitations and cost differences impede wider adoption, especially among industries that are sensitive to price and in developing areas.

MARKET OPPORTUNITIES

Expansion in the Food & Beverage and E-commerce Sectors Creates Lucrative Growth Opportunities

The increasing demand in the food & beverage and e-commerce industries offers substantial growth potential for biodegradable paper and plastic packaging. Rising consumption of packaged foods, ready-to-eat meals, and online grocery deliveries has amplified the requirement for safe and sustainable packaging options. Numerous e-commerce leaders and food delivery services are making a shift toward biodegradable mailers, wraps, and trays to lessen their carbon footprints. Additionally, advancements in packaging technologies, such as water-resistant biodegradable coatings, bio-based barrier films, and compostable laminates, are improving the effectiveness and attractiveness of sustainable options, creating new revenue opportunities for manufacturers.

BIODEGRADABLE PAPER & PLASTIC PACKAGING MARKET TRENDS

Technological Advancements and Circular Economy Initiatives Emerge as a Market Trend

The worldwide market is experiencing significant trends focused on innovative materials and circular economy practices. Businesses are increasingly allocating resources toward research and development to create cutting-edge biodegradable polymers, hybrid composites of paper and plastic, and coatings that improve strength and moisture resistance while still being environmentally friendly. Furthermore, the move toward sustainability-driven branding is evident in the growing adoption of closed-loop recycling systems, bio-based inks, and minimalist packaging designs. Collaboration among packaging manufacturers, recyclers, and consumer goods enterprises is becoming more prevalent to guarantee material traceability and effective end-of-life recovery. The use of digital tracking tools, including QR codes and blockchain for packaging transparency, further illustrates the ongoing consumer demand for sustainable and smart packaging.

MARKET CHALLENGES

Inadequate Composting Infrastructure and Consumer Misconceptions to Challenge Market Growth

A significant challenge facing the biodegradable paper & plastic packaging market is the insufficient composting and recycling facilities present in numerous areas. While biodegradable packaging is intended to break down in specific industrial composting environments, the scarcity of such facilities hinders its proper disposal, resulting in environmental pollution when mixed with traditional plastics. Additionally, consumer misunderstanding of the differences between "biodegradable," "compostable," and "recyclable" materials frequently results in incorrect waste sorting and management. This deficiency in both knowledge and infrastructure undermines the circular economy model and impedes the overall progress toward sustainable packaging solutions.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Significant Environmental Benefits Dominated the Paper Material Propel Segment Growth

In terms of material, the market is categorized into plastic and paper.

The paper material segment is expected to capture the largest share of 62.80% in 2026.and is projected to reach of the biodegradable paper & plastic packaging market in 2024. In 2025, the segment is anticipated to dominate with a 62.96% share. Biodegradable paper material provides significant environmental benefits by naturally breaking down without leaving harmful residues. In contrast to traditional plastics that can last for centuries, biodegradable paper decomposes into organic matter, water, and carbon dioxide within a few months under composting conditions. This substantially decreases pollution in soil and water, reduces landfill waste, and contributes to lower carbon emissions. The renewable nature of its materials, usually sourced from wood pulp, agricultural by-products, or recycled paper, ensures a minimal effect on non-renewable resources, thereby supporting global sustainability efforts, further driving the segment’s growth.

The plastic material segment is expected to grow at a CAGR of 10.94% over the forecast period.

By Type

Versatility of Starch-Based Plastics Boosted the Segment’s Growth

In terms of type, the market is categorized into starch based plastic, cellulose based plastic, polylactic acid (PLA), polyhydroxyalkanoates (PHA), paper & paperboard, and others.

The starch-based plastic segment is projected to dominate the market with a share of 33.64% in 2026. The starch-based plastic segment captured the largest biodegradable paper & plastic packaging market share in 2024. In 2025, the segment is anticipated to dominate with a 33.39% share. Starch-based plastics are produced from naturally occurring polymers present in corn, potatoes, and tapioca. These ingredients are biodegradable for packaging purposes and come from renewable sources. The versatility of starch-based bioplastics is impressive, making them ideal for both rigid and flexible packaging applications. Whether used as protective foam for shipping boxes or as biodegradable bags, they are becoming more prevalent in the realm of sustainable packaging.

The polylactic acid (PLA) type segment is expected to grow at a CAGR of 10.69% over the forecast period.

By End Users

Rising Demand from the Food & Beverages Sector Propelled Segment Growth

Based on end users, the market is segmented into food & beverages, e-commerce, healthcare, personal care & cosmetics, agriculture, and others.

To know how our report can help streamline your business, Speak to Analyst

In 2026, the global market was dominated by food and beverages in terms of end users. Furthermore, the segment is set to hold a 31.37% share in 2026. The food and beverages (F&B) industry has become one of the primary drivers of biodegradable paper & plastic packaging market growth. The growing demand for ready-to-eat meals, convenience foods, and takeaway items, along with the worldwide increase in food delivery services, has heightened the need for sustainable and safe packaging options. With consumers becoming more conscious of the environmental issues linked to single-use plastics, food brands, restaurants, and beverage companies are turning to biodegradable paper and plastic substitutes such as compostable trays, cups, wraps, pouches, and cutlery. This shift has increased the utilization of biodegradable packages, further propelling segmental growth.

In addition, the e-commerce end user is projected to grow at a CAGR of 10.82% during the study period.

Biodegradable Paper & Plastic Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America Biodegradable Paper & Plastic Packaging Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America

North America dominated the market with a valuation of USD 5.23 billion in 2025 and is projected to reach USD 5.77 billion in 2026. North America held the dominant share in 2023, valued at USD 4.31 billion, and also took the leading share in 2024 with USD 4.75 billion. North America dominates the global biodegradable paper & plastic packaging market. The U.S. and Canada are experiencing significant policy changes that promote the adoption of compostable packaging. Brand initiatives focused on sustainability, driven by consumers, from companies such as PepsiCo, Coca-Cola, and Unilever, are boosting the demand for biodegradable plastic films and paper cartons. In 2026, the U.S. market is estimated to reach USD 4.65 billion.

Other regions, such as the Asia Pacific and Europe, are anticipated to witness a notable growth in the coming years. During the forecast period, the Asia Pacific region is projected to record a growth rate of 11.60%, which is the second-highest amongst all the regions, and reach the valuation of USD 4.46 billion in 2025. The fast-paced industrial growth and expanding consumer market in the region are opening up significant opportunities. Authorities in India, Japan, and Australia are encouraging the use of biodegradable packaging through incentives and restrictions on plastic. The increase in sustainable fast-moving consumer goods (FMCG) and food delivery services is driving growth in the region.

In the region, India and China are both estimated to reach USD 1.34 and USD 1.62 billion each in 2026.

Asia Pacific

Asia Pacific contributed approximately USD 4.46 billion to the global market in 2025, accounting for 27.83% share, and is expected to reach USD 4.95 billion in 2026. and secure the position of the third-largest region in the market. The market is growing significantly owing to the EU’s Single-Use Plastics Directive (SUPD) and policies promoting a circular economy and a ban on single-use plastics. Nations such as Germany, France, and the U.K. have established increased quotas for compostable packaging, encouraging the swift uptake of biodegradable materials. Compared to traditional plastic packaging, biodegradable packages are gaining traction.

Backed by these factors, countries including the U.K. are expected to record the valuation of USD 0.56 billion, Germany to record USD 0.67 billion in 2026, and France to record USD 0.45 billion in 2025.

Europe

The market in Europe reached USD 2.82 billion in 2025, representing 17.58% of total market revenue, and is projected to reach USD 3.08 billion in 2026.

Latin America

In 2025, Latin America generated USD 2.23 billion, contributing 13.92% to global market revenue, and is projected to grow to USD 2.43 billion in 2026. Over the forecast period, Latin America is expected to witness moderate growth, with the market projected to reach a valuation of USD 2.23 billion in 2025. Growth is supported by increasing adoption of sustainable packaging solutions, particularly in countries such as Brazil, Chile, and Mexico, where biodegradable packaging regulations are being implemented to combat plastic waste. Additionally, the presence of local paper manufacturers offering affordable, eco-friendly alternatives is further driving market expansion.

Middle East & Africa

The Middle East & Africa region captured 7.99% of the global market in 2025, generating USD 1.28 billion in revenue, and is projected to reach USD 1.39 billion in 2026. The Middle East & Africa region is also anticipated to experience moderate growth, driven by rising sustainability initiatives and demand from the tourism sector for eco-friendly packaging. Countries such as the UAE and South Africa are actively promoting bio-based packaging to align with global environmental goals. In this region, South Africa is projected to reach a market value of USD 0.37 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Companies Focus on Strategic Partnerships to Support their Market Position

The global biodegradable paper & plastic packaging industry shows a semi-concentrated structure with numerous small- to mid-size companies actively operating across the globe. These players are actively involved in product innovation, strategic partnerships, and geographic expansion.

Smurfit Kappa, Amcor, and Mondi are some of the dominating players in the market. A comprehensive range of unit-dose packaging products, global presence through a strong distribution network, and collaborations with research and academic institutes are a few characteristics of these players that support their dominance.

Apart from this, other prominent players in the market include DS Smith, Stora Enso, PLAMFG, and others. These companies are undertaking various strategic initiatives, such as investments in R&D and partnerships with pharmaceutical companies to enhance their market presence.

LIST OF KEY BIODEGRADABLE PAPER & PLASTIC PACKAGING COMPANIES PROFILED

- Smurfit Kappa (Ireland)

- Mondi (U.K.)

- Amcor (Switzerland)

- DS Smith (U.K.)

- Stora Enso (Finland)

- PLAMFG (China)

- Notpla (U.K.)

- Klabin SA (Brazil)

- Tipa Corporation (Israel)

- Paperfoam (Netherlands)

- Universal Protective Packaging, Inc. (U.S.)

- Tetra Pak International S.A. (Switzerland)

- Riverside Paper Co. Inc. (U.S.)

- Hosgör Plastik (Turkey)

- BASF SE (Germany)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Amazon began the process of packing and delivering groceries for customers in Spain with the use of eco-friendly bags made from plant materials sourced in Europe, such as corn starch and vegetable oils, which could eventually be recycled into new bags. The initial trials of these new bags, created by materials specialists at the Italian company Novamont, which is part of Versalis (Eni), have been launched for Amazon Fresh orders in Valencia, with assistance from materials scientists at Amazon.

- December 2024: Symphony Environmental introduced a biodegradable resin aimed at the plastics sector. The innovative product, named NbR, incorporates natural minerals to lessen the reliance on fossil-derived polyethylene (PE) or polypropylene (PP), and the company claims it has also been designed to break down safely in nature if it inadvertently escapes recycling and becomes litter in the environment.

- October 2024: NUA COSMETICS and ITC Packaging introduced a compostable, bio-based bottle. This new bottle, created from PLA, has been designed for Provei Global through the collaborative efforts of Nua Cosmetics, ITC Packaging, and ADBioplastics. The material enhances transparency and offers better barriers against both oxygen and water vapor, while also increasing tenacity and impact resistance.

- July 2022: Mondi, a worldwide leader in the packaging and paper industry, collaborated with Fiorini International, a prominent converter and packaging manufacturer based in Italy, to develop and introduce a new fully recyclable paper package for a high-end Italian pasta brand. The collaboration between Mondi and Fiorini International has led to the creation of a novel paper bag design featuring a significant window made of transparent, recyclable, and biodegradable cellulose, enabling consumers to view the contents.

- November 2019: Smurfit Kappa introduced a range of eco-friendly and biodegradable packaging solutions designed for bundling beverages in cans and bottles. This new collection made from corrugated materials removes the necessity for single-use plastics and is fully recyclable, renewable, and biodegradable. The GreenClip product from Smurfit Kappa serves as a substitute for the plastic rings typically used to hold six packs of cans together.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 10.61% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Type, End Users, and Region |

|

By Material |

· Plastic · Paper |

|

By Type |

· Starch Based Plastic · Cellulose Based Plastic · Polylactic Acid (PLA) · Polyhydroxyalkanoates (PHA) · Paper & Paperboard · Others |

|

By End Users |

· Food & Beverages · E-commerce · Healthcare · Personal Care & Cosmetics · Agriculture · Others |

|

By Geography |

· North America (By Material, Type, End Users, and Country) o U.S. o Canada · Europe (By Material, Type, End Users, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Russia o Poland o Romania o Rest of Europe · Asia Pacific (By Material, Type, End Users, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Material, Type, End Users, and Country/Sub-region) o Brazil o Mexico o Argentina o Rest of Latin America · Middle East & Africa (By Material, Type, End Users, and Country/Sub-region) o Saudi Arabia o UAE o Oman o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 16.01 billion in 2025 and is projected to reach USD 39.51 billion by 2034.

In 2025, the market value stood at USD 16.01 billion.

The market is expected to exhibit a CAGR of 10.61% during the forecast period (2026-2034).

The starch based plastics segment led the market by type.

The key factors driving the market growth are the rising environmental concerns and government regulations.

Smurfit Kappa, Mondi, Amcor, DS Smith, Stora Enso, and PLAMFG are some of the prominent players in the market.

North America dominated the market in 2025.

Augmenting demand from the food industry is one of the factors expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us