Biofuels Market Size, Share & Industry Analysis, By Type (Solid {Woody Materials, Crops, Municipal Solid Waste (MSW), and Others}, Liquid {Fuel Ethanol, Biodiesel, Renewable Diesel, and Others}, and Gaseous), By Category (First-Generation, Second-Generation, and Others), By Application (Transport, Power Generation, Residential, Commercial & Industrial Heating, and Others), and Regional Forecast, 2026-2034

Biofuels Market Size and Future Outlook

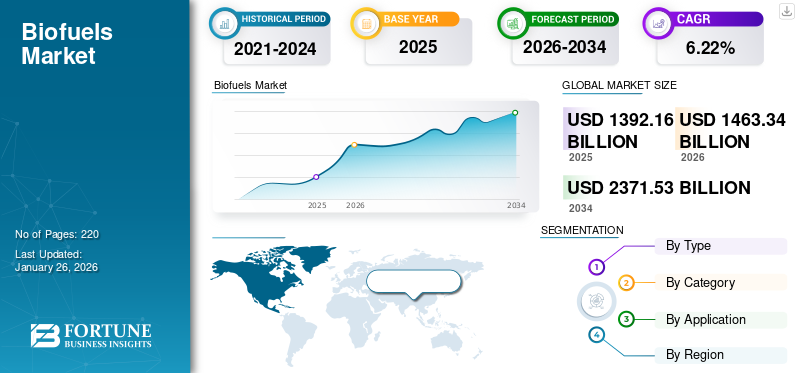

The global biofuels market size was valued at USD 1,392.16 billion in 2025. The market is projected to grow from USD 1,463.34 billion in 2026 to USD 2,371.53 billion by 2034, exhibiting a CAGR of 6.22% during the forecast period. North America dominated the biofuels market with a market share of 38.23% in 2025.

The biofuels sector is expanding largely due to the increasing global focus on transitioning to clean energy and the pressing necessity to decrease greenhouse gas (GHG) emissions from transportation and energy industries. Globally, governments are enacting favorable policies, including blending mandates, subsidies, and carbon pricing measures, to encourage the adoption of biofuels as a viable alternative to fossil fuels. The aviation and maritime sectors, which have few options for electrification, are progressively adopting advanced biofuels and sustainable aviation fuels SAF to achieve their decarbonization goals.

Furthermore, concerns over energy security, especially in nations that import oil, are spurring investments in local biofuel production to lessen dependence on crude oil imports and unpredictable fossil fuel markets. Innovations in technology, such as the commercialization of second-generation and advanced biofuels sourced from agricultural residues, waste oils, and non-food feedstocks, are expanding the industry's possibilities by resolving the food-versus-fuel issue and improving production efficiency.

For instance, in September 2025, Mitsubishi Heavy Industries met its performance goals with a pilot facility for membrane dehydration systems located at MHI's Nagasaki Carbon Neutral Park within the Nagasaki District Research & Innovation Centre, achieving over 99.5% ethanol purity. Bioethanol is increasingly recognized as a clean alternative to gasoline and as a feedstock for Sustainable Aviation Fuel (SAF). However, to utilize bioethanol as fuel, it is crucial to eliminate the moisture present during the manufacturing process, particularly in the dehydration stage, which typically requires substantial energy consumption. The MMDS® technology intends to enhance the process by substituting the traditional method with a molecular sieve separation technique, resulting in more efficient production while cutting energy usage by more than 30%. This innovation will lead to significant reductions in operational expenses and enable consistent production. Moving forward, MHI aims to expedite the development of a demonstration facility for an early rollout based on data from various tests conducted at the pilot plant.

Download Free sample to learn more about this report.

Biofuels Market Key Takeaways

- 2025 Market Size: USD 1,392.16 billion

- 2026 Market Size: USD 1,463.34 billion

- 2034 Forecast Market Size: USD 2,371.53 billion

- CAGR: 6.22% from 2026–2034

- North America dominated the biofuels market with a 38.23% share in 2025.

- The solid segment is expected to lead the market with an 85.43% share in 2026.

- The transport segment is projected to account for 84.38% of the market in 2026.

North America

In 2025, the North America market stood at USD 532.22 billion and is projected to grow to USD 553.55 billion in 2026, supported by strong biofuel production capacity and favorable renewable fuel policies.

Asia Pacific

Asia Pacific reached USD 240.81 billion in 2025, accounting for 17.30% share, and is expected to reach USD 257.49 billion in 2026., driven by increasing renewable energy adoption and growing energy demand.

Europe

Europe captured 12.44% of the global market in 2025, generating USD 173.2 billion in revenue and is projected to reach USD 181.98 billion in 2026, supported by decarbonization initiatives and sustainable fuel mandates.

U.S.

In 2025, the U.S. market is estimated to reach USD 510.3 billion. The country is the world's leading producer and consumer of biofuels, with ethanol widely used in gasoline blending under the Renewable Fuel Standard (RFS).

Japan

Growing efforts to reduce carbon emissions and diversify energy sources are supporting the adoption of biofuels across key end-use sectors.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Biofuels in Transport Sector to Propel Market Growth

The transportation sector is among the fastest-growing areas for global biofuel demand, propelled by policies, commitments to reduce carbon emissions, and increasing fuel requirements in developing nations. The International Energy Agency (IEA) indicates that between 2023 and 2028, biofuel demand is expected to rise by 38 billion liters, marking nearly a 30% increase compared to the prior five years. By 2028, the total demand is anticipated to reach around 200 billion liters, with ethanol and renewable diesel comprising approximately two-thirds of the increase.

- For instance, in 2022, biofuels already contributed over 3.5% of the global energy demand for transport, primarily in road transport. Also, the IEA predicts that this figure could more than double to nearly 9% by 2030 within its Net Zero Emissions scenario.

MARKET RESTRAINTS

High Production Costs & Infrastructure Limitations to Restrict Market Expansion

High production costs and limitations in infrastructure are major barriers to the growth of the biofuels industry. For instance, in Europe, biodiesel and bioethanol are priced 70-130% higher than their fossil fuel equivalents, depending on the type of feedstock used (such as vegetable oils, used cooking oil, or cereals). In the U.S., Sustainable Aviation Fuel (SAF) can be as much as five times costlier than regular jet fuel, according to estimates from the industry.

At the same time, infrastructure issues exacerbate these cost challenges. Numerous retail fuel stations do not have the necessary equipment (such as tanks, pumps, and blending hardware) that can accommodate higher biofuel blends such as E15, E85, or biodiesel mixtures exceeding B20, which requires further capital investment.

MARKET OPPORTUNITIES

Expansion of Sustainable Aviation Fuel is Anticipated to Create Growth Opportunities

Sustainable Aviation Fuel (SAF) is rapidly becoming a key element in the aviation sector’s efforts to reduce carbon emissions. As reported by the International Air Transport Association (IATA), global production of SAF increased from approximately 0.5 million tons (around 600 million liters) in 2023 to about 1.0 million tons (nearly 1.3 billion liters) in 2024, which accounts for roughly 0.3% of the total jet fuel consumption. Projections indicate that this figure will continue to grow, reaching 2 million tons (approximately 2.7 billion liters) or about 0.7% of jet fuel use by 2025. Regulatory mandates are playing a significant role in promoting this growth. For instance, the EU’s ReFuelEU Aviation regulation requires a 2% SAF inclusion by 2025, increasing to 6% by 2030, and aiming for as much as 70% by 2050. Similarly, the U.K. has set a mandate beginning at 2% in 2025, with plans to raise it to 10% in 2030 and 22% by 2040.

BIOFUELS MARKET TRENDS

Growing Demand for Advanced Biofuels to Drive Market Growth

Advanced biofuels, derived from feedstocks that do not compete with food sources such as agricultural waste, municipal solid waste, algae, and lignocellulosic materials, are a recent trend in first-generation fuels. In contrast to traditional ethanol and biodiesel, advanced biofuels provide lower life-cycle greenhouse gas emissions, enhanced sustainability, and diminished competition with food crops. The International Energy Agency (IEA) indicates that the production of advanced biofuels needs to increase nearly fivefold by 2030 to align with global pathways for net-zero emissions. Although current production levels are still relatively low, there is a significant upward trend.

For instance, Renewable Energy Policy Network for the 21st Century (REN21) reported that by 2022, global output of advanced biofuels reached almost 11 billion liters, primarily driven by renewable diesel (HVO) and cellulosic ethanol. This growth is significantly supported by policies such as the U.S. Renewable Fuel Standard, the EU’s Renewable Energy Directive II, and new mandates in India and Brazil. Furthermore, Sustainable Aviation Fuel (SAF), which is largely produced through advanced biofuel methods, is anticipated to play a major role in achieving decarbonization in aviation by 2050, showcasing the sector's potential for transformation.

MARKET CHALLENGES

Limited Feedstock Availability to Hamper Market Growth

One of the major limitations on the expansion of the biofuel sector is the decreasing availability of feedstocks. The International Energy Agency (IEA) predicts that the demand for vegetable oils, waste and residue oils, and fats will rise by 56% from 2022 to 2027, reaching approximately 79 million tons globally. However, the supply of the most commonly utilized residues and waste oils is anticipated to approach its maximum capacity during that period.

Although the biofuel production from non-food feedstocks (such as wastes, residues, and designated crops on marginal land) is increasing, it still constituted only about 9% of liquid biofuel usage in 2021. Thus, under the IEA’s Net Zero Emissions scenario, this figure could increase to approximately 40% by 2030. In India, the impact of feedstock shortages is evident, with the ethanol supply year (ESY) of 2024-25 projected to experience a 20% decline in feedstock availability compared to the prior year, due to decreased sugarcane yield, limitations on using broken rice (to safeguard food reserves), and pest issues affecting sugar production.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Solid Biofuels Offers Reliable Renewable Energy for Heating & Power Generation to Drive Segment Growth

On the basis of the segmentation of type, the market is classified into solid, liquid, and gaseous.

In 2026, the solid segment is anticipated to dominate with an 85.43% biofuels market share. Solid biofuels, including wood pellets, wood chips, and agricultural byproducts, are favored for their accessibility, affordability, and contribution to renewable energy as well as heating solutions. The International Energy Agency (IEA) reports that in 2022, solid biofuels represented two-thirds of modern bioenergy use, providing around 45 exajoules (EJ) globally. Europe stands as the largest market, with the EU's demand for wood pellets surpassing 31 million tons in 2022, driven by policies promoting renewable heating and the transition from coal to biomass. Their capacity to deliver consistent baseload energy, particularly for generating power and heat, positions them as significant players in the effort to reduce carbon emissions.

The liquid biofuels market segment is experiencing the fastest growth and is expected to grow at a CAGR of 7.17%. Liquid biofuels, such as ethanol, biodiesel, and renewable diesel, are gaining significant popularity as they can be used as direct substitutes for gasoline and diesel, simplifying their integration into current transportation systems. The International Energy Agency (IEA) reported that global production of liquid biofuels reached 170 billion liters in 2022 (~4.3 EJ), meeting around 3.5% of the transport energy requirements. Nearly two-thirds of this total was comprised of ethanol, while biodiesel and renewable diesel are experiencing rapid growth. Their compatibility with existing vehicles and infrastructure, along with government-mandated blending requirements (such as E20 in India and 15% biodiesel in Brazil), positions liquid biofuels as crucial for reducing carbon emissions in transport.

By Category

Rising Popularity of First-Generation Biofuels Due to Established Technology and Strong Policy Support to Drive Segment Growth

In terms of category, the market is categorized into first-generation, second-generation, and others.

The first generation is the dominant segment in the market, and it is anticipated to show the fastest growth with a CAGR of 6.06% during the forecast period. By category, the first generation segment held the share of 89.83% in 2026. First-generation biofuels, which are made from food-based feedstocks such as sugarcane, corn, and vegetable oils, are becoming increasingly popular due to established technology, affordability, and robust policy backing.

The first-generation fuels, primarily ethanol and biodiesel, are extensively utilized in the transportation sector through blending mandates, providing a direct way to lower greenhouse gas emissions. As reported by REN21, first-generation biofuels represented the bulk of the 170 billion liters of biofuel produced globally in 2022, with ethanol alone accounting for almost two-thirds. Their compatibility with existing fuel systems and government initiatives such as India’s E20 ethanol program and Brazil’s biodiesel blending targets continues to boost demand.

By Application

Biofuels are Used in Transport for Reducing Emissions and Enhancing Energy Security

In terms of application, the market is categorized into transport, power generation, residential, commercial & industrial heating, and others.

The transport is the dominant segment in the market. This segment is set to hold the largest market share of 84.38% in 2026. Biofuels are widely used in the transport sector as they provide a renewable, low-carbon alternative to conventional fossil fuels while being compatible with existing vehicles and infrastructure. Ethanol and biodiesel can be blended directly with gasoline and diesel, making adoption cost-effective and practical.

For instance, according to the International Energy Agency (IEA), biofuels supplied about 3.5% of global transport energy demand in 2022, equivalent to nearly 170 billion liters. They help reduce greenhouse gas emissions, improve energy security by lowering dependence on imported oil, and support national climate goals. With growing mandates and policies, their role in transport continues to expand. The transport sector is anticipated to grow at a CAGR of 6.14% during the study period.

To know how our report can help streamline your business, Speak to Analyst

Biofuels Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Biofuels Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the North America market stood at USD 532.22 billion, representing 38.23% of global demand, and is projected to grow to USD 553.55 billion in 2026. The demand for biofuels in North America is rising steadily, fueled by robust policy initiatives, concerns about energy security, and the drive to reduce carbon emissions in transportation.

In 2025, the U.S. market is estimated to reach USD 510.3 billion. The U.S. stands as the leading producer and consumer of biofuels globally, responsible for nearly 70 billion liters of ethanol in 2022, mainly utilized in gasoline blending as per the Renewable Fuel Standard (RFS). Canada has also enhanced its Clean Fuel Regulations, mandating progressively greater reductions in carbon intensity, which is increasing the demand for both biodiesel and renewable diesel. The rising implementation of Sustainable Aviation Fuel (SAF) contributes additional momentum, bolstered by tax incentives included in the U.S. Inflation Reduction Act. With an increasing focus on lowering greenhouse gas emissions and reducing oil imports, the biofuels sector in North America is poised for ongoing growth.

- For instance, the U.S. Energy Information Administration (EIA) has stated that the production capacity for renewable diesel saw a 7% increase in 2023 and reached 24 billion gallons per year in early 2024, reflecting a surge in investment in advanced fuel technologies.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 240.81 billion in 2025, accounting for 17.30% share, and is expected to reach USD 257.49 billion in 2026. Other regions, such as Latin America and the Asia Pacific, are anticipated to witness a notable growth in the coming years. During the forecast period, the Latin America region is projected to record a growth rate of 6.79%, which is the second highest amongst all the regions, and reach the valuation of USD 306.36 billion in 2025. The market in Latin America is experiencing growth due to the abundant availability of feedstock, favorable governmental policies, and strong regional demand for energy. In 2022, Brazil, the world’s second-largest producer of ethanol, produced more than 37 billion liters, largely due to its established ethanol blending initiatives. Nations such as Argentina and Colombia are also increasing their biodiesel production derived from soybean oil. With increasing needs for transport fuels and climate objectives, Latin America is positioning biofuels as a crucial strategy for energy security and achieving decarbonization.

Europe

The Europe region captured 12.44% of the global market in 2025, generating USD 173.2 billion in revenue, and is projected to reach USD 181.98 billion in 2026. The Europe biofuels market growth is strong, driven by ambitious decarbonization targets, large government investments, and coordinated internal industrial efforts, making biofuels a key component of Europe's energy transition. Backed by these factors, countries including Germany are expected to record a valuation of USD 42.72 billion, and the rest of Europe to record USD 28.27 billion in 2025. After Europe, the market in Latin America is estimated to reach USD 306.36 billion in 2025 and secure the position of the second-largest region in the market. In the region, Brazil is estimated to reach USD 231.24 billion in 2025.

Middle East & Africa

The Middle East & Africa market accounted for USD 139.57 billion in 2025, representing 10.03% of the global industry, and is expected to reach USD 144.16 billion in 2026. Over the forecast period, the Asia Pacific and Middle East & Africa regions are anticipated to show tremendous opportunities for biofuels, as energy consumption continues to rise, and supportive policies are being implemented to decrease reliance on imported fossil fuels. Countries such as India, China, and Indonesia are leading growth in the Asia Pacific region with mandates for ethanol and biodiesel. For instance, India has reached 18.4% ethanol blending as of March 2025, progressing toward its E20 goal. The Asia Pacific market in 2025 is set to record USD 240.81 billion as its valuation. In the Middle East and Africa, nations such as South Africa, Saudi Arabia, and the UAE are investing in biofuels to diversify their energy sources, improve energy security, and meet climate commitments, which is driving consistent market growth in these areas. In the Middle East & Africa, GCC is set to attain the value of USD 33.61 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors Actively Expanding Market Presence through Business Expansion, Strategic Acquisitions, and Partnerships

Linde plc and Air Liquide are acknowledged as major participants in the market as each firm is very experienced, innovative, and has invested heavily in biofuels infrastructure.

In March 2025, Aramco, a leading integrated energy and chemicals company, and Air Products Qudra (APQ) announced that Aramco had completed the acquisition of a 50% equity interest in the Blue Biofuels Industrial Gases Company (BHIG) in Jubail, Saudi Arabia. This agreement combines expertise and capabilities to supply Biofuels, including lower-carbon Biofuels, to the Jubail Industrial City area at scale.

LIST OF KEY BIOFUELS COMPANIES PROFILED

- Archer Daniels Midland (U.S.)

- Cargill Inc. (U.S.)

- Neste Corporation (Finland)

- Bunge Limited (Switzerland)

- Wilmar International Ltd. (Singapore)

- Louis Dreyfus Company (Netherlands)

- POET LLC (U.S.)

- Green Plains Inc. (U.S.)

- The Andersons Inc. (U.S.)

- Raízen Energia SA (Brazil)

- CropEnergies AG (Germany)

- Algenol (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In September 2025, India anticipated to remove all restrictions on ethanol production from sugarcane juice, syrup, and molasses for the 2025/26 supply year beginning November 1. This policy change is intended to assist sugar mills, increase renewable energy production, and further help to achieve India’s ethanol blending objectives. Prior limitations were placed due to low cane yields, but favorable monsoons have improved cultivation conditions, enhancing supply expectations. Industry stakeholders have praised this decision, calling for higher procurement prices to enable mills to compensate farmers. The Food Ministry stated that the diversion of ethanol will be tracked to ensure sufficient domestic sugar availability, maintaining a balance between energy aspirations and consumer demands. This represents a significant advancement for India’s biofuel industry.

- In August 2025, Cemvita reached an agreement with Invest RS to establish a facility in Rio Grande do Sul, Brazil, for the production of FermOil™, a sustainable oil intended for sustainable aviation fuel (SAF), and FermNPK™, a biofertilizer that promotes regenerative agriculture. The plant will utilize crude glycerol to produce low-carbon feedstock for SAF. Previously, Cemvita collaborated with Be8, a local biofuel innovator, to enhance the SAF value chain. Officials state that the initiative fosters innovation, sustainability, and bioeconomy prospects in the area.

- In July 2025, Avalon Energy Group and Sulzer Chemtech formed a strategic alliance to scale sustainable aviation fuel (SAF) production using Sulzer’s BioFlux technology. Their first project, a fully integrated biorefinery in Uruguay, will produce low-carbon SAF from non-edible oilseed crops, serving as a global model. Avalon is also advancing projects in India, Eswatini, and the U.S., with Sulzer providing proven technology to ensure efficient, reliable SAF production.

- In June 2025, Neste and Chevron Lummus Global (CLG) achieved a key milestone in developing technology to convert lignocellulosic biomass into renewable fuels such as SAF and renewable diesel. Early pilot results show significant performance gains over existing methods, highlighting the potential of underutilized forest and agricultural residues. The partnership combines Neste’s renewable fuels expertise with CLG’s proven refining technologies to enable scalable, lower-emission fuel production.

- In May 2025, Masdar and OMV signed a Letter of Intent in Vienna to collaborate on developing synthetic sustainable aviation fuel (eSAF) and other sustainable products. The partnership will explore opportunities in Austria, the UAE, and Central and Northern Europe, reinforcing both companies’ commitment to advancing clean energy and decarbonizing aviation.

REPORT COVERAGE

The global biofuels market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and biofuel market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.22% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Type

By Category

By Application

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1,392.16 billion in 2025 and is projected to reach USD 2,371.53 billion by 2034.

In 2025, the market value stood at USD 1,392.16 billion.

The market is expected to exhibit a CAGR of 6.22% during the forecast period.

The transport segment led the market by application.

Rising energy demand and energy security needs to propel the market growth.

Archer Daniels Midland, Neste Corporation, and Wilmar International Ltd., among others are some of the prominent players in the market.

North America dominated the market in 2025.

Major factors favoring biofuels adoption include supportive government policies, emission reduction goals, abundant feedstock availability, technological advancements, and rising demand for sustainable transport fuels such as SAF and biodiesel.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us