Biofungicides Market Size, Share & Industry Analysis, By Source (Microbial and Botanical), By Species (Trichoderma spp, Bacillus spp., Pseudomonas, Streptomyces, and Others), By Form (Powder and Liquid/Aqueous), By Mode of Application (Foliar Application, Soil Application, Seed Treatment, and Others ), By Crop Type (Cereals, Oilseeds, Fruits & Vegetables, and Others), and Regional Forecast, 2026-2034

(Offer valid till 30th Jun 2026)

KEY MARKET INSIGHTS

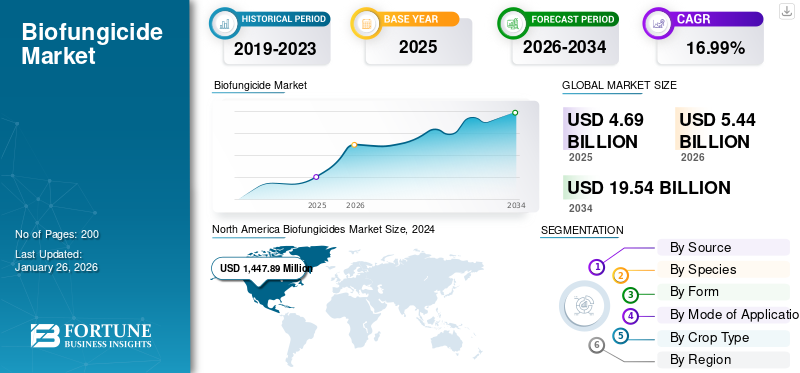

The global biofungicides market size was valued at USD 4.69 billion in 2025. The market is projected to grow from USD 5.44 billion in 2026 to USD 19.54 billion by 2034, exhibiting a CAGR of 17.32% during the forecast period. North America dominated the biofungicides market with a market share of 35.70% in 2025.

The global market is growing rapidly, fueled by growing concerns for the environment, demand for no to less chemical crop protection products, and the move toward sustainable farming practices. These elements support the use of biofungicides as environmentally friendly and non-toxic substitutes for chemical fungicides. The market is anticipated to expand with the leading regions being North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

In addition, the industry key players such as Bayer AG, BASF SE, Syngenta AG, Marrone Bio Innovations, Inc., and FMC Corporation. These players maintain their global biofungicides market share by virtue of innovations, high R&D investments, strategic partnerships and acquisitions, international distribution networks, and focus on sustainability and compliance.

Download Free sample to learn more about this report.

Biofungicides Industry Key Takeaways

- 2025 Market Size: USD 4.69 billion

- 2026 Market Size: USD 5.44 billion

- 2034 Forecast Market Size: USD 19.54 billion

- CAGR: 17.32% from 2026–2034

- North America dominated the biofungicides market with a 35.70% share in 2025.

- The microbial segment is projected to account for 71.28% of the market share in 2026.

- The powder segment is expected to register the fastest growth with a CAGR of 17.21% during the forecast period.

North America

North America generated USD 1.67 billion in revenue in 2025 and is projected to reach USD 1.94 billion in 2026.

Europe

Europe accounted for 33.15% of the global market in 2025 and is expected to reach USD 1.80 billion in 2026.

Asia Pacific

Asia Pacific generated USD 0.81 billion in revenue in 2025.

U.S.

The U.S. leads the region with approximately 83.7% market share

Japan

Rising focus on sustainable agriculture and increasing demand for environmentally friendly crop protection solutions are supporting biofungicide market growth.

Read More

MARKET DYNAMICS

Market Drivers

Increase in Consumer Demand for Organic Products to Drive Market Growth

Consumer demand for organic and residue-free products is rising steadily globally, driving significant growth in the organic farming sector. Biofungicides are a key driver of this market transition by offering efficient crop protection fungicide products that do not deposit toxic chemical residues, thus meeting certification criteria and consumer safety and health expectations. Additionally, consumers are increasingly ready to pay premium prices for organic produce due to its perceived health advantages and lower risk of chemical exposure, thus driving the biofungicides market growth.

- According to the Organic Trade Association, the retail sales of organic produce in the U.S. increased from USD 20.5 billion to USD 21.5 billion.

Market Restraints

Cost Factors to Impede Market Growth

Biofungicides tend to be more expensive to produce and apply than traditional chemical fungicides and thus less affordable for small farmers, particularly in developing countries. These costs result from various factors, among which are sophisticated manufacturing conditions, availability of active ingredients, trained staff, storage capacities, and distribution requirements. Packaging, storage, and distribution of biofungicides further contribute to the cost, with shorter shelf lives and specialty handling requirements adding complexity to end users. Surveys and industry association statistics indicate that the biocontrol market remains considerably smaller than the traditional crop-protection market. The time it takes for regulatory approvals, gradual product entry, and scale-up are also realities that drive per-unit costs higher than for mass-produced synthetics.

Market Opportunities

Integration with Integrated Pest Management (IPM) to Unlock New Growth Opportunities

Biofungicides are being increasingly incorporated into Integrated Pest Management (IPM) systems, offering a sustainable solution for plant disease management. This synergy is achieved through the application of biofungicides in combination with traditional, mechanical, and occasionally chemical methods to create a systematic approach that maximizes disease control and environmental stewardship. Biofungicides typically provide minimal or no chemical residue, enabling farmers to satisfy food safety standards and consumer demand for cleaner products. A number of companies have been embracing this practice as a means of optimizing the effectiveness and consistency of biofungicide products used in commercial farming.

- For instance, in February 2025, Veganic, a farming business, reinforced vine protection with its new biofungicide BELVINE, specifically formulated to fight downy mildew and powdery mildew on grapes. BELVINE minimizes the use of standard fungicides such as copper and sulfur, promoting sustainable viticulture and integrated pest management (IPM) schemes.

Biofungicides Market Trends

Rising Shift Toward Microbial-Based Solutions to Shape Industry

Microbial biofungicides, especially those derived from Bacillus and Trichoderma species, are increasingly gaining prominence. They are opted for due to multiple modes of action, greater adaptability, and harmonization with integrated pest management (IPM) systems. Bacillus-based formulations are particularly picking up steam with improved shelf life, hence being apt for international marketing. The microbials not only combat pathogens but also stimulate plant health through inducing systemic resistance.

- For instance, in February 2023, Seipasa, a Spanish specialist in natural crop solutions, launched Furity as its patented technology powering the microbiological fungicide Fungisei. The new product is an innovative formulation platform built around a highly effective strain of Bacillus subtilis, enabling superior microbial stability, efficacy, and field-use flexibility.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Source

Efficacy and Specificity to Lead Microbial Segment’s High Market Proportion

On the basis of the source, the market is segmented into microbial and botanical.

The microbial segment dominates the biopesticides market by source with a 71.28% share in 2026, and a projected CAGR of 16.88% through 2026-2034. Microbial biopesticides, including Bacillus subtilis and Trichoderma spp., provide site-specific control against targeted fungal diseases with less risk of non-target injury and the development of resistance. As the focus on sustainable agriculture continues to grow, microbial biofungicides fit into practices that de-emphasize the use of chemical pesticides and support environmental well-being.

The botanical segment is expected to grow significantly in the forecast period with a CAGR of 17.27% in 2025.

By Species

Wide Adoption Across Various Crop Types to Lead Bacillus spp. Segment Growth

On the basis of the species, the market is segmented into trichoderma spp., bacillus spp., pseudomonas, streptomyces, and others.

The bacillus spp segment is anticipated to maintain a significant position in the market chiefly owing to its robust biocontrol effectiveness, widespread use across a variety of crop types, regulatory favor, and formulation technology developments. Bacillus-type biofungicides such as Bacillus subtilis and Bacillus amyloliquefaciens are used for controlling a wide range of fungal and bacterial pathogens. The Bacillus-based biofungicides market is valued at approximately USD 1,528.96 million in 2025 and is projected to grow to USD 5,316.64 million by 2032, reflecting a CAGR of 16.99%.with a share of 37.84% in 2026

The streptomyces segment is expected to grow significantly at a CAGR of 18.11% during the forecast period.

By Form

Ease of Application and Effectiveness to Fuel Liquid/Aqueous Market Leadership

On the basis of form, the market is segmented into powder and liquid/aqueous.

The liquid/aqueous market segment is likely to capture a significant portion of the world's biofungicides market mainly due to its simplicity in application, greater efficiency, and compatibility with contemporary farming mechanisms. Liquid biofungicides have improved coverage and penetration on plant surfaces, resulting in quicker absorption and more rapid disease control outcomes, which is essential for early fungal disease management. Liquid formulations also easily fit into contemporary modern-day sprayers, irrigation systems, such as drip irrigation, making them suitable for extensive farming operations. They also have better stability, longer shelf life, and flexibility for blending with other products. with a share of 59.89% in 2026

- For instance, in January 2024, Sipcam Agro USA introduced a liquid biofungicide called Mevalone in the U.S., aimed at diseases such as bunch rot and powdery mildew in vineyards, reflecting the growing need for liquid biofungicides in practical uses.

The powder segment is anticipated to grow at the fastest CAGR of 17.21% during the forecast period.

By Mode of Application

Rapid Disease Control and Cost-Effectiveness Fuelled Foliar Application Market Leadership

On the basis of mode of application, the market is segmented into foliar application, soil application, seed treatment, and others.

To know how our report can help streamline your business, Speak to Analyst

The foliar application segment accounted for more than 79.18% of the biofungicides market share in 2025 and is expected to maintain this majority share through the coming years. Foliar application enables rapid uptake of biofungicides, resulting in timely suppression of the disease. This application is especially valuable for high-value crops where the time of intervention is critical. Foliar sprays are also generally cost-effective relative to soil applications, making them favored by farmers who want affordable options.

The seed treatment segment is anticipated to grow at the fastest CAGR of 18.29% during the forecast period.

By Crop Type

Rising Area Under High-Value Crops Including Fruits & Vegetables to Lead Segment’s Market Leadership

Based on the crop type channel, the market is segmented into cereals, oilseeds, fruits & vegetables, and others.

The market is dominated by the fruits and vegetables segment on account of the high vulnerability of these crops to fungal diseases and the high demand from consumers for residue-free and organic produce. In 2024, fruits and vegetables dominated a whopping 42.43% share of the global biofungicides market due to their sheer need to be protected from fungal diseases in order to maintain high-quality and visually acceptable produce. North America, as one of the highest producers of organic fruits and vegetables, and is at the forefront of this leadership, fueled by sustainable agriculture practices and integrated pest management adoption.

The oilseeds segment is expected to grow significantly in the forecast period at a CAGR of 16.78% from 2025 to 2032.

Biofungicides Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

NORTH AMERICA

North America Biofungicides Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

In 2025, North America held 35.70% of the global market share, reaching a valuation of USD 1.67 billion, and is projected to grow to USD 1.94 billion in 2026. North America dominates the global market primarily due to a robust shift toward sustainable agriculture, stringent regulations on chemical pesticide use, and strong government support and adoption of organic farming practices.

The U.S. leads the region with approximately 83.7% of the North American biofungicides market value in 2024, driven by extensive organic cultivation areas and supportive USDA initiatives promoting biopesticide adoption. Organic farming prohibits synthetic chemical fungicides, requiring farmers to use biofungicides derived from natural organisms or substances that are approved by USDA’s National Organic Program (NOP). This regulatory framework ensures biofungicides are essential tools for disease management in organic crop production.

- For instance, the Organic Trade Association reports U.S. organic food sales reached USD 63.8 billion in 2023, with organic produce comprising more than 15% of all fruit and vegetable sales. Rising demand for organic food directly increases the use of biofungicides, which are required on organic crops and help farmers comply with organic certification standards

Other regions, such as Europe and the Asia Pacific, are anticipated to witness a notable growth in the coming years.

EUROPE

The market in Europe reached USD 1.55 billion in 2025, representing 33.15% of total market revenue, and is projected to reach USD 1.8 billion in 2026. This is driven mainly by strict European Union regulations, including the Farm-to-Fork strategy and chemical pesticide reduction requirements for a 50% reduction in chemical pesticide usage and enhanced organic farming coverage by 2030, which significantly promotes the use of biofungicides.

ASIA PACIFIC

Asia Pacific contributed approximately USD 0.81 billion to the global market in 2025, accounting for 17.29% share, and is expected to reach USD 9.46 billion in 2026. China and India, being key producers and consumers of agricultural biologicals, are spearheading this growth with efforts to curtail chemical pesticide usage and encourage biopesticides in the Asia Pacific. The region is expected to register a CAGR of 13.02% during the forecast period.

SOUTH AMERICA

Over the forecast period, South America is expected to be the fastest-growing region with a CAGR of 14.05%. The South America market in 2025 is set to record USD 572.41 million as its valuation. Brazil and Argentina have put strong regulations to minimize the use of synthetic pesticides, which leads farmers to move toward safer and more environment-friendly options such as biofungicides.

MIDDLE EAST & AFRICA

The Middle East & Africa region captured 1.44% of the global market in 2025, generating USD 0.07 billion in revenue, and is projected to reach USD 0.08 billion in 2026. The Middle East & Africa is expected to have moderate growth having a CAGR of 11.57%. The agricultural modernization programs in the region focus on increasing crop yields and food security while fighting developing pest resistance in major crops such as cotton, citrus, and dates.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Focus on New Product Launches to Support Market Growth of Key Players

The market comprises a mix of large agrochemical companies and specialized biological product manufacturers, with many regional players dominating specific agricultural zones due to localized expertise. Market leaders emphasize innovation in biofungicide formulations, including microbial, botanical, and biochemical types, targeting multiple crop diseases with environmentally friendly profiles. Key players are Bayer AG, BASF SE, Syngenta AG, Marrone Bio Innovations, Inc., and FMC Corporation.

Apart from this, other prominent players in the market include Nufarm, Novozymes, Certis, and others.

Key Players in the Biofungicides Market

|

Rank |

Company Name |

|

1 |

Bayer AG |

|

2 |

BASF SE |

|

3 |

Syngenta AG |

|

4 |

Marrone Bio Innovations, Inc. |

|

5 |

FMC Corporation |

List of Key Biofungicides Companies Profiled

- BASF SE (Germany)

- Bayer Crop Science (Germany)

- Koppert Biological Systems (Netherlands)

- Certis Biologicals (U.S.)

- BioWorks, Inc. (U.S.)

- Marrone Bio Innovations (U.S.)

- Valent BioSciences (U.S.)

- Syngenta AG (Switzerland)

- FMC Corporation (U.S.)

- Andermatt Group (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Nitro, a Brazilian ag-tech company, launched Égide Max, a new foliar biofungicide designed to protect high-value crops from foliar diseases in Brazil. The new product aims to significantly elevate foliar disease management, targeting a range of crops such as soybeans, corn, cotton, coffee, and sugarcane.

- December 2024: Koppert and Amoéba entered into a strategic partnership to launch an innovative biofungicide solution called AXPERA. This solution leverages the lysate of the amoeba Willaertia magna C2c Maky to combat a wide range of fungal diseases in crops.

- October 2024: Biotalys expanded its R&D pipeline with a new biofungicide program called BioFun-8, focused on developing a protein-based biofungicide to control Alternaria, a major leaf spot fungal disease affecting fruits, vegetables, and specialty crops. This program leverages Biotalys' proprietary AGROBODY 2.0 technology platform to create an effective and sustainable crop protection solution.

- January 2024: Certis Biologicals launched Convergence Biofungicide, specifically formulated for corn, soybeans, and peanuts. The product leverages the biological action of Bacillus amyloliquefaciens strain D747, providing disease control against key soil-borne pathogens such as Pythium, Rhizoctonia, Fusarium, and Phytophthora, as well as tackling foliar diseases such as tar spot, rusts, and leaf spots.

- November 2023: FMC Corporation, an American chemical manufacturing company, launched a new insecticide/biofungicide premix product called Ethos Elite LFR for the U.S. market. This product combines a trusted pyrethroid insecticide, bifenthrin, with two proprietary biological strains, Bacillus velezensis strain RTI301 and Bacillus subtilis strain RTI477, to provide broad-spectrum control against early-season soilborne pests and diseases.

REPORT COVERAGE

The global biofungicides market industry report analyzes the market in depth and highlights crucial aspects such as global market trends, market dynamics, prominent companies, investment in research and development and end-use. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 17.32% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentations |

By Source, Species, Form, Mode of Application, By Crop Type, and by Region |

|

By Segmentation |

By Source · Microbial

|

|

By Species · Trichoderma spp · Bacillus spp. · Pseudomonas · Streptomyces · Others |

|

|

By Form · Powder

|

|

|

By Mode of Application · Foliar Application · Soil Application · Seed Treatment · Others |

|

|

By Crop Type · Cereals · Oilseeds · Fruits & Vegetables · Others |

|

|

By Region · North America (By Source, Species, Form, Mode of Application, By Crop Type, and Country) • U.S. (By Mode of Application) • Canada (By Mode of Application) • Mexico (By Mode of Application) · Europe (By Source, Species, Form, Mode of Application, By Crop Type, and Country) • Germany (By Mode of Application) • Spain (By Mode of Application) • Italy (By Mode of Application) • France (By Mode of Application) • U.K. (By Mode of Application) • Rest of Europe (By Mode of Application) · Asia Pacific (By Source, Species, Form, Mode of Application, By Crop Type, and Country) • China (By Mode of Application) • Japan (By Mode of Application) • India (By Mode of Application) • Australia (By Mode of Application) • Rest of Asia Pacific (By Mode of Application) · South America (By Source, Species, Form, Mode of Application, By Crop Type, and Country) • Brazil (By Mode of Application) • Argentina (By Mode of Application) • Rest of South America (By Mode of Application) · Middle East & Africa (By Source, Species, Form, Mode of Application, By Crop Type, and Country) • South Africa (By Mode of Application) • UAE (By Mode of Application) • Rest of the Middle East & Africa (By Mode of Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 5.44 billion in 2026 and is anticipated to reach USD 19.54 billion by 2034.

At a CAGR of 17.32%, the global market will exhibit steady growth over the forecast period.

By species, the Bacillus spp. segment leads the market.

North America held the largest market share in 2025.

An increase in consumer demand for organic products drives the market growth.

Bayer AG, BASF SE, Syngenta AG, Marrone Bio Innovations, Inc., and FMC Corporation are the leading companies in the market.

Government support and new product development are shaping the industry

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 30th Jun 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us