Fungicides Market Size, Share & Industry Analysis, By Type (Chemical [Triazoles, Strobilurins, Dithiocarbamates, Inorganics, Chloronitriles, and Others] and Biological), By Form (Liquid and Dry), By Application Method (Foliar Treatment, Chemigation, Seed Treatment, and Others), By Crop Type (Cereals, Oilseeds & Pulses, Fruits & Vegetables, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

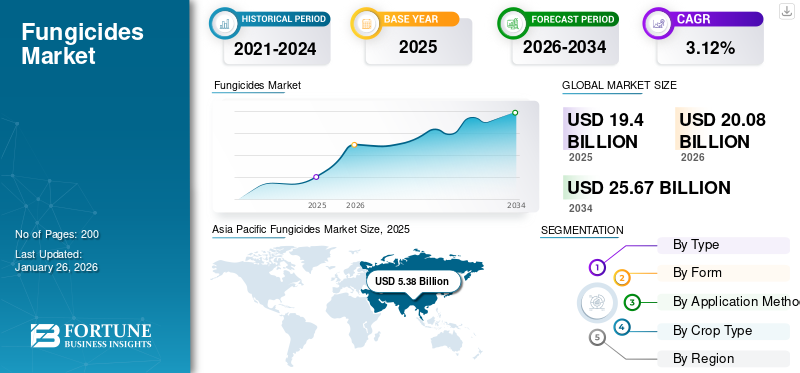

Fungicides Market Size and Future Outlook

The global fungicides market size was valued at USD 19.40 billion in 2025. The market is projected to grow from USD 20.08 billion in 2026 to USD 25.67 billion by 2034, exhibiting a CAGR of 3.12% during the forecast period. Asia Pacific dominated the fungicides market with a market share of 27.75% in 2025.

Fungicides are chemical compounds applied to kill or suppress the development of fungi and their spores, which can cause serious damage to crops in agriculture and lead to yield and quality losses. They manage parasitic fungi and oomycetes by being applied in the form of sprays, dusts, or seed dressings and may be contact, translaminar, or systemic based on the way they act within plant tissues. With the global population growing to 9.7 billion in 2050, there is a rising need to expand food production while coping with limited arable land. The rising incidence of crop diseases and increasing focus on high agricultural productivity continue to drive the demand for fungicides worldwide. Farmers rely on fungicides to protect crops from fungal diseases, which helps improve crop productivity and yield, fueling the global fungicides market demand. Countries in the Asia Pacific, South America, and parts of Europe are witnessing rapid growth in fungicide consumption due to expanding agricultural activity, improving farming practices, and food security concerns.

The leading companies dominating the global market include BASF SE, Bayer AG, Syngenta AG, Corteva Agriscience, FMC Corporation, and others. The long-term prosperity of these players depends on creating innovative active ingredients to fight resistance, continuing to develop bio-based and sustainable solutions, expanding distribution networks, and merging digital and precision modern agriculture technologies.

Download Free sample to learn more about this report.

Fungicides Market Key Takeaways

- 2025 Market Size: USD 19.40 Billion

- 2026 Market Size: USD 20.08 Billion

- 2034 Forecast Market Size: USD 25.67 Billion

- CAGR: 3.12% from 2026–2034

- Asia Pacific dominated the fungicides market with a 27.75% share in 2025.

- The chemical segment is projected to account for 83.81% of the market in 2026.

- Fruits & vegetables will hold a 39.04% market share in 2026.

Europe

Europe led the global market with a 28.91% share and a value of USD 5.61 billion in 2025.

Asia Pacific

Asia Pacific reached USD 5.38 billion in 2025, accounting for 27.75% of global revenue.

Latin America

Latin America generated USD 5.10 billion in 2025 and represented 26.27% of the global market.

U.S.

The fungicides market is expected to reach USD 2.03 billion by 2026.

Japan

The fungicides market is anticipated to reach USD 0.61 billion by 2026.

Read More

MARKET DYNAMICS

Market Drivers

Introduction of Novel Products to Drive Market Growth

The area under fruits & vegetables is increasing with the change of the global food structure and the changing cropping pattern. This has further resulted in an increasing demand for fungicide products comprising novel active ingredients. These innovations bring new active ingredients and advanced formulations that improve the efficacy, spectrum, and environmental profile of fungicides.

- In June 2025, BASF SE, a European multinational company and one of the largest chemical producers, started the registration process for its new fungicide innovation Adapzo Active (Flufenoxadiazam) to control Asian Soybean Rust (ASR), a major disease affecting soybean crops in South America. This new active ingredient is the industry's first histone deacetylase (HDAC) inhibitor. It offers a novel mode of action for effective control and resistance management of ASR, including mutated fungal strains resistant to existing products.

Market Restraints

Growing Resistance to Active Ingredients May Hamper Growth

Among the various types of pesticides available in the market, chemical pesticides are widely used for protecting crops due to their affordability and convenience. The use of these products indiscriminately on the crops leads to several negative side effects. For instance, beneficial non-target microorganisms present in crops, such as Trichoderma, Arbuscular Mycorrhizal Fungi, may be negatively affected by the use of these products on crops.

Additionally, the continuous use of these products on the crops may cause the fungus present in the crops to develop resistance against the products.

- Botrytis cinerea, a grey mold fungus present in fruits and vegetables, developed resistance against fungicides. Several other fungi have also developed resistance against fungicide products. This acts as a major factor restraining the adoption of fungal pesticide products for crop protection.

Market Opportunities

Technological Advancements and Precision Agriculture to Unlock New Growth Opportunities

The incorporation of precision agriculture tools, including drone spraying and sensor-driven applications, enhances the effectiveness of fungicide application in minimizing wastage and the environmental footprint. These technologies present prospects for new formulations and modes of application. For instance, firms are designing fungicides that are well-suited for drone spraying systems to provide optimal droplet size and formulation stability, enhancing coverage and bioavailability. This fusion of drone technology with fungicide technology results in increased efficiency, cost-effectiveness, and reduced environmental impact.

Fungicides Market Trends

Shift Toward Combination and Multi-Mode Products to Shape the Industry

The recent trend in the fungicides market shows a shift toward combination and multi-mode products to effectively tackle the issue of resistance development in pathogens. Farmers are increasingly using mixtures such as triazoles combined with strobilurins or triazoles paired with Succinate Dehydrogenase Inhibitors (SDHIs) to improve both the spectrum of disease control and the efficacy of treatment.

- According to the Organisation for Economic Co-operation and Development (OECD) and CropLife International, over 60% of new fungicide registrations between 2018 and 2024 involve co-formulated products. This trend is reinforced by industry guidelines promoting integrated pest management programs that include multi-site and multi-mode formulations as key strategies to sustainably manage diseases.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Chemical Segment Dominates Owing to Its High Usage in Developing Nations

On the basis of type, the market is segmented into chemical and biological.

The chemical segment is projected to dominate the market with a share of 83.81% in 2026, and a projected CAGR of 2.20% through 2026-2034. Chemical origin fungicidal, also known as synthetic fungicides, are biocidal substances that can kill or prevent the growth of fungi and their spores. The chemical fungicidal products are predominantly preferred over the biological products due to their immediate effect in controlling the growth of fungi. Moreover, the high stability and easy availability of chemical fungicide products in the market are the crucial factors that are responsible for the dominance of this segment.

The biological segment is expected to grow significantly in forecast period with a CAGR of 7.93% in 2025. The rising demand for effective crop protection solutions is driving innovation in the development of advanced fungicides and bio-based products.

To know how our report can help streamline your business, Speak to Analyst

By Form

Ease of Application and Rapid Absorption & Action of Liquid Fungicides Helps Segment Growth

On the basis of form, the market is segmented into liquid and dry.

The liquid segment is anticipated to maintain a significant position in the global fungicides market, securing a value of USD 13.63 billion in 2024. Fruits and vegetables are very susceptible to fungal diseases such as blights, mildews, rusts, anthracnose, and rots, which lead to heavy yield loss and reduce the quality of produce. Prevention of these losses is essential through effective control of fungi. Rising health awareness globally and pressure for fresh, high-quality fruits and vegetables are pushing farmers to apply fungicides to achieve market quality and consumer satisfaction. The liquid segment is projected to dominate the market with a share of 73.16% in 2026.

The dry segment is expected to grow at a CAGR of 2.66% during the forecast period.

By Application Method

Foliar Treatment Segment to Exhibit High Growth Stoked by Their Increasing Preference

On the basis of application method, the market is segmented into foliar treatment, chemigation, seed treatment, and others.

The foliar segment is expected to lead the market, contributing 67.13% globally in 2026. The high preference given to the foliar treatment is due to its uniform application and low volume requirement per hectare. The reduction in volume requirement per hectare increases the profitability of farmers by saving input costs and protecting the crop yields from damage. In addition to this, the foliar application covers vulnerable plant surfaces and blocks the entry of pathogens that invade the crop. The foliar application also helps to eradicate the already established infections and reduce the secondary inoculum.

The chemigation segment is anticipated to grow significantly at a CAGR of 4.40% during the forecast period.

By Crop Type

High Susceptibility to Fungal Diseases and Growing Consumer Demand Fuels the Fruits & Vegetables Segment Market Leadership

On the basis of crop type, the market is segmented into cereals, oilseeds & pulses, fruits & vegetables, and others.

The fruits & vegetables segment will account for 39.04% market share in 2026. Fruits and vegetables are very susceptible to fungal diseases such as blights, mildews, rusts, anthracnose, and rots, which lead to heavy yield loss and reduce the quality of produce. Prevention of these losses is very much essential through effective control of fungi. Rising health awareness globally and pressure for fresh, high-quality fruits and vegetables are pushing farmers to apply fungicides to achieve market quality and consumer satisfaction.

The cereal segment is anticipated to grow at a CAGR of 3.10% during the forecast period.

Fungicides Market Regional Outlook

Regionally, the global fungicides report covers the market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Europe

Asia Pacific Fungicides Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Europe held 28.91% of the global market, reaching a valuation of USD 5.61 billion, and is projected to grow to USD 5.75 billion in 2026. The fungicides market is currently dominated by Europe, which accounted for 29.19% of the global market share in 2024. Europe is a major producer of cereals, grains, and high-value crops, with Spain, France, Italy, and the U.K. leading in crop production. Wheat alone is vital, with Europe being the world’s largest wheat producer. The large cultivated area and high crop value stimulate continuous fungicide use. The United Kingdom fungicides market is estimated to reach USD 0.41 billion by 2026, while the Germany fungicides market is forecast to reach USD 0.47 billion by 2026.

Asia Pacific

The market in Asia Pacific reached USD 5.38 billion in 2025, representing 27.75% of total market revenue, and is projected to reach USD 5.62 billion in 2026. Asia Pacific is expected to grow significantly with a 27.49% revenue share in 2024, driven by rapid urbanization, increasing food demand, a burgeoning population, and strong agricultural production in China and India. The region benefits from government initiatives, technological adoption such as precision farming, and the favorable tropical climate, promoting fungal diseases, resulting in a projected CAGR of 4.15% from 2025 onwards. The Japan fungicides market is anticipated to reach USD 0.61 billion by 2026, the China fungicides market is set to attain USD 2.64 billion by 2026, and the India fungicides market is likely to reach USD 1.09 billion by 2026.

South America

South America ranked third after Asia Pacific in market size in 2024, largely due to expansive agricultural activities and crop disease management needs, driving continued fungicide adoption. The South American market is predicted to expand at the fastest pace during the foreseeable years. The rapid increase in fungicide consumption in the region, especially for the cultivation of cereals and oilseeds, presents a resilient opportunity for the companies to increase their footprint. Brazil, Argentina, and Colombia are the key consumers in the region. However, the fungicide consumption in Brazil and Argentina is projected to grow at a stable rate, while the consumption in Colombia is declining.

North America

The North America market was valued at USD 2.62 billion in 2025, capturing 13.48% of global revenue, and is estimated to reach USD 2.7 billion in 2026. North America was the fourth-largest market in 2024, with a focus on technological advancements, precision agriculture, increasing awareness of fungal threats to crops, and ongoing R&D in crop protection supporting a CAGR of 2.88%. The U.S. especially emphasized innovative fungicide solutions to maintain agricultural productivity. The United States fungicides market is expected to reach USD 2.03 billion by 2026.

Middle East & Africa

In 2025, the Middle East & Africa market stood at USD 0.7 billion, representing 3.59% of global demand, and is projected to grow to USD 0.71 billion in 2026. The fungicides market growth in the Middle East & Africa is primarily driven by increased usage of chemical fungicide products and the adoption of advanced agricultural practices. South Africa is the major consumer in the African region. The consumption of these products in the region is driven by the optimum application of products in high-value crops such as fruits & vegetables, and nuts.

Latin America

Latin America maintained a strong presence in the global market, reaching USD 5.1 billion in 2025, accounting for 26.27% share, and is expected to reach USD 5.3 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Holds a Fragmented Structure Owing to Presence of Domestic, Regional, and Global Players

Major agro-chemical companies such as Syngenta AG, FMC Corporation, Bayer AG, ADAMA Ltd., and BASF SE have established a separate product portfolio of crop protection products, which include fungicides, to meet the growing demand among farmers. Additionally, local manufacturers and regional players are competing with major players to increase their market share. Growing investments in research and development are enabling companies to introduce effective and sustainable agricultural solutions. Furthermore, they are also focused on acquisitions and mergers to consolidate their position and compete with other key players.

- For instance, in September 2025, Corteva Agriscience launched a new fungicide called Zorvec Entecta in India. This fungicide is specifically designed for grapes and potatoes to provide long-lasting protection against two major diseases: Downy Mildew (Plasmopara viticola) in grapes and Late Blight (Phytophthora infestans) in potatoes.

Key Players in the Fungicides Market

|

Rank |

Company Name |

|

1 |

BASF SE |

|

2 |

Bayer AG |

|

3 |

Syngenta AG |

|

4 |

Corteva Agriscience |

|

5 |

FMC Corporation |

List of Key Fungicides Companies Profiled

- Bayer AG (Germany)

- BASF SE (Germany)

- Syngenta AG (Switzerland)

- Corteva, Inc. (U.S.)

- FMC Corporation (U.S.)

- Sumitomo Chemicals (Japan)

- UPL Ltd. (India)

- Nufarm (Australia)

- ADAMA Agricultural Solutions Ltd. (Israel)

- Isagro SpA (Italy)

KEY INDUSTRY DEVELOPMENTS

- June 2025: IHARA Manufacturing Co., Ltd., a Japanese company, launched two novel fungicides in Brazil named MIGIWA and PROPERTY. MIGIWA contains the active ingredient ipflufenoquin and is particularly effective in preventing apple black spot disease.

- September 2024: FMC Corporation unveiled three innovative crop protection solutions for farmers in India. The new products include Velzo Fungicide and two other herbicides. The launch involved interactions with farmers and recognition of key channel partners, underscoring FMC's collaborative approach in India.

- October 2023: “Bayer”, one of the well-known agriculture products companies based in the U.K., received approval from the Chemicals Regulation Division (CRD) for its new active substance to be used in fungicides. The new substance is isoflucypram, which will be used in its product called Vimoy.

- September 2022: BASF, a well-known agriculture nutrition manufacturer, announced the launch of its all-new innovative fungicide product called Revylution, which received approval for use in New Zealand.

- November 2022: Bayer announced the launch of its new fungicide called Luna Flex under its Luna brand, which is registered for critical crops, fruits, and vegetables, including apples. The new product is designed to deal with scab, melanosis, powdery mildew, and gummy stem blight.

REPORT COVERAGE

The global fungicides market industry report analyzes the market in depth and highlights crucial aspects such as market trends, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.12% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

|

|

By Form

|

|

|

By Application Method

|

|

|

By Crop Type

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market was at USD 19.40 billion in 2025 and is anticipated to reach USD 25.67 billion by 2034.

The global market will exhibit a CAGR of 3.12% over the forecast period.

By type, the chemical segment leads the market.

In 2025, Europe accounted for the largest market share, at 28.91%.

The introduction of novel products is a crucial factor driving market growth.

BASF SE, Bayer AG, Syngenta AG, Corteva Agriscience, and FMC Corporation are the leading companies in the market.

The shift toward combination and multi-mode products is shaping the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us