Bispecific Antibody Market Size, Share & Industry Analysis, By Mechanism of Action (T-Cell Engaging, Dual Blockers/ Inhibitors, Co- factor Mimetics, and Others), By Application (Oncology, Hematology, Ophthalmology, and Others) By Route of Administration (Intravenous, Subcutaneous, and Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Others), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

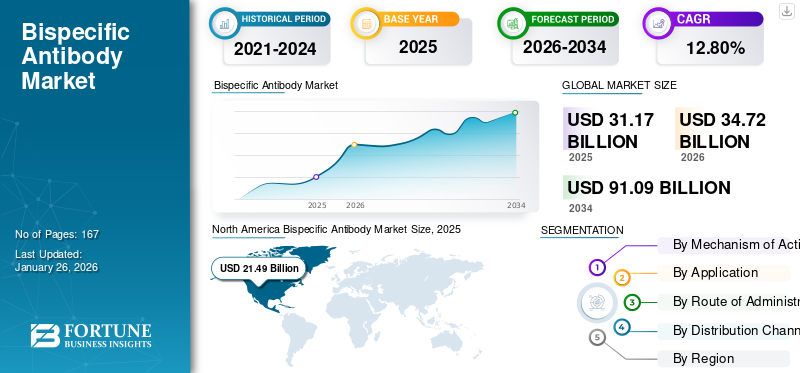

The global bispecific antibody market size was valued at USD 31.17 billion in 2025 and is projected to grow from USD 34.72 billion in 2026 to USD 91.09 billion by 2034, exhibiting a CAGR of 12.80%% during the forecast period. North america dominated the bispecific antibody market with a market share of 51.80% in 2025.

Bispecific antibody offers effective therapeutic application for key diseases such as cancer and other blood disorders. These bispecific antibodies are bioengineered with precision and target multiple antigens simultaneously. Their potential applications are expanding in a multitude of medical domains, including oncology, hematology, ophthalmology, and rare and complex diseases, due to continuous research and development.

The increasing prevalence of cancer, regulatory approvals from the U.S. FDA and EMA, and rising investment and increasing clinical trials are anticipated to augment the global bispecific antibody market demand and bolster the growth. Such factors are anticipated to impact the forecast period significantly.

Attributing to these advantages, many key industry players are actively investing resources toward the development of numerous pipeline candidates to support the increasing demand.

- For instance, in May 2024, Regeneron Pharmaceuticals, Inc. showcased positive results from an ongoing Phase 1/2 trial evaluating its costimulatory bispecific antibody, REGN7075 (EGFRxCD28), in combination therapies with Libtayo (cemiplimab) in patients with advanced solid tumors.

Furthermore, many key industry players, such as AbbVie Inc., Pfizer Inc., and Bristol-Myers Squibb Company, operating in the market, are focusing on developing various pipeline candidates to support the rising demand for effective therapeutics for diverse disease indications with the help of bispecific antibodies.

Download Free sample to learn more about this report.

Bispecific Antibody Market Takeaways

- 2025 Market Size: USD 31.17 billion

- 2026 Market Size: USD 34.72 billion

- 2034 Forecast Market Size: USD 91.09 billion

- CAGR: 12.80% from 2026–2034

- North America dominated the bispecific antibody market with a 51.80% share in 2025.

- The oncology segment is projected to account for 41.99% of the market share in 2026.

- The intravenous segment is expected to hold a dominant 58.90% share in 2026, supporting the market’s 12.80% CAGR.

North America

North America led the global market in 2025, generating USD 21.49 billion in revenue and is projected to reach USD 23.99 billion in 2026.

Europe

Europe accounted for 25.80% of the global market in 2025, with revenue of USD 3.98 billion, and is expected to grow to USD 4.36 billion in 2026.

Asia Pacific

Asia Pacific generated USD 4.44 billion in 2025, representing 15.90% of global revenue, and is projected to reach USD 5.01 billion in 2026.

U.S.

The U.S. bispecific antibody market is estimated to reach USD 22.86 billion in 2026, driven by strong oncology research and adoption of advanced biologic therapies.

Japan

The Japan market is projected to reach USD 1.59 billion by 2026, supported by increasing demand for innovative cancer treatments and expanding biopharmaceutical development.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Cancer Burden Coupled with Advancements in Antibody Engineering Is Accelerating Adoption of Bispecific Antibodies

The increasing demand for effective and targeted therapies for oncology and hematological malignancies is one of the key factors driving the growth of the market. Conventional monoclonal antibodies exhibit certain limitations in relapsed or refractory patient populations. These factors intensify the need for novel modalities. Research and bispecific antibody development are being carried out through collaboration among key companies to provide oncology therapeutics using bispecific antibodies. Such rising collaboration to enhance the application of bispecific antibodies for therapeutic applications, offering global bispecific antibody market growth.

- For instance, in March 2025, Harbour BioMed collaborated with AstraZeneca to discover and develop next-generation multi-specific antibodies for various indications. The collaboration enabled the company to license multiple programs along with a USD 105.0 million equity investment by AstraZeneca.

MARKET RESTRAINTS

High Manufacturing Complexity and Cost of Bispecific Antibody Production to Impede Growth of Market

Bispecific antibodies are structurally more complex than conventional monoclonal antibodies, requiring sophisticated engineering to ensure correct folding, stability, and dual target specificity. Such high complexity in manufacturing requires more advanced purification techniques, resulting in higher production costs. In addition, maintaining batch consistency and meeting stringent regulatory quality standards adds further time and expense. The high manufacturing complexity and cost of bispecific antibody production remain significant restraints, slowing their broader adoption and restricting patient access compared with more established biologics or competing therapies such as checkpoint inhibitors and CAR-T.

- For instance, in August 2025, the U.S. FDA declined approval to Regeneron Pharmaceuticals Inc. of its blood cancer therapy, odronextamab, to treat follicular lymphoma, citing manufacturing issues.

MARKET OPPORTUNITIES

Expansion into Earlier Lines of Therapy to Offer a Prominent Opportunity for Market Growth

Bispecific antibodies are currently approved primarily for relapsed or refractory cancers, where treatment options are limited and patients have often failed prior therapies. However, these therapies have strong potential to expand into earlier lines of treatment, as it allows these therapies to be used in larger patient populations before disease progression or resistance develops. Combination with standard regimens therapies could significantly expand usage and improve patient outcomes

- For instance, in December 2024, Janssen-Cilag International NV, a Johnson & Johnson company, showcased new frontline data from two investigational studies of TECVAYLI (teclistamab). These studies established the potential of teclistamab for frontline combination therapy for patients with newly diagnosed multiple myeloma for use in newly diagnosed patients, with promising efficacy and a tolerable safety profile.

BISPECIFIC ANTIBODY MARKET TRENDS

Shift from IV Infusions to Subcutaneous (SC) Formulations is a Prominent Trend Observed

Shift toward subcutaneous formulation is a prominent global bispecific antibody market trend observed. IV infusions are comparatively difficult to administer. The shift toward subcutaneous formulations offer greater patient convenience, reduced hospital dependency, improved compliance, and enables easier administration. As more bispecifics advance in their pipelines, developers are investing in high-concentration, stable, low-viscosity formulations that can be delivered subcutaneously without losing efficacy or safety. This shift is fueled by patient preference, the need to reduce overall treatment, and the competitive edge gained by offering more user-friendly administration. Many key players are directing their resources toward development for novel bispecific formulations.

- For instance, in November 2024, Alphamab Oncology showcased data from a clinical trial of JSKN033, a subcutaneous co-formulation consisting of an anti-HER2 bispecific antibody-drug conjugate (ADC) and a PD-L1 immune checkpoint inhibitor. The drug is included in the pilot project by the Shanghai Municipal Drug Administration with the consent of the Center for Drug Evaluation (CDE).

Download Free sample to learn more about this report.

MARKET CHALLENGES

Cytokine Release Syndrome (CRS) and Neurotoxicity Safety Concerns Associated with Bispecific Antibody Pose a Critical Challenge to Market Growth

Cytokine Release Syndrome (CRS) and neurotoxicity remain significant safety concerns for bispecific antibodies, especially T-cell engagers. These immune-related toxicities can lead to severe adverse events, requiring step-up dosing and hospitalization during initial therapy. Such risks complicate clinical management, increase treatment costs, and may discourage physician adoption. As a result, safety challenges directly restrain market growth and slow broader acceptance of bispecific antibodies.

- For instance, in November 2024, the American Society of Hematology published an article that reported practical implications of Multi-Institution Cytokine Release Syndrome (CRS) and Immune Effector Cell-Associated Neurotoxicity (ICANS) rates in lymphoma-targeted bispecific antibodies (BsAb).

Segmentation Analysis

By Mechanism of Action

Increasing Product Launches for T-Cell Engaging in Markets to Propel Segmental Growth

Based on the mechanism of action, the market is divided into T-Cell engaging, dual blockers/ inhibitors, Co-factor mimetic, and others.

To know how our report can help streamline your business, Speak to Analyst

The T-Cell engaging is expected to account for a dominant revenue share in the global market. The dominance of the segment is due to its potency and target-specific anti-tumor activity. Also, their ability to overcome resistance to standard therapies has led to strong clinical efficacy in heavily pretreated, relapsed, or refractory cancers where treatment options are limited to one of the significant factors for higher market share.

Furthermore, the expanding pipelines from major pharma companies ensure sustained investment and rapid development, positioning T-cell engagers as the leading segment in bispecific antibody therapeutics.

- For instance, in February 2023, Atreca, Inc., collaborated with Xencor, Inc., to launch the first program combining an Atreca-discovered antibody with Xencor’s XmAb bispecific Fc domain and a cytotoxic T-cell binding domain (CD3).

By Application

Rising Prevalence of Cancer Boosted Growth of Oncology Segment

By application, the market is further segmented into oncology, hematology, ophthalmology, and others.

The oncology segment segment will account for 41.99% market share in 2026. The high share of the segment is due to various factors such as the increasing prevalence of cancer and the current limitations of therapeutics. This gives rise to the need for effective therapeutic alternatives such as bispecific antibodies.

Furthermore, many key operational entities in the market are directing their investment and participating in strategic activities such as collaboration and acquisition to expand their product offering in the market.

- For instance, in November 2024, Merck & Co., Inc., collaborated with LaNova Medicines Ltd. to develop, manufacture, and commercialize LM-299, a novel investigational PD-1/VEGF bispecific antibody from LaNova targeting distinct tumor-associated antigens (TAAs).

The hematology segment is growing at a CAGR of 6.43% over the study period.

By Route of Administration

Novel Product Launches in Intravenous Segment to Propel Growth of Market

On the basis of the route of administration, the market is segmented into intravenous, subcutaneous, and others.

The intravenous segment is projected to dominate the market with a share of 58.90% in 2026. By route of administration, the intravenous segment held a share of 58.90% in 2026. The dominance of the segment is attributed to higher bioavailability. These intravenously administered bispecific antibodies ensure rapid and complete systemic exposure, enabling tight control over plasma drug levels and immediate onset of effects. It allows delivery of higher doses and volumes than subcutaneous routes, which is useful for large biologics or loading doses. Key players in the global bispecific antibodies are focusing their resources on commercializing these advantages with new product offerings.

- For instance, in September 2024, EpimAb Biotherapeutics, Inc. collaborated with Vignette Bio, Inc. for EpimAb’s BCMA-targeting T-cell engager (TCE) EMB-06. The clinical stage drug is administered intravenously.

The segment of subcutaneous route of administration is anticipated to propel with a growth rate of 14.05% growth across the global bispecific antibody market forecast period.

By Distribution Channel

New Launches of Hospital Pharmacies to Commercialize Growth Potential Placed them in Leading Position

On the basis of distribution channel, the market is categorized into hospital pharmacies, retail pharmacies, and others.

In 2024, the global market was dominated by hospital pharmacies in terms of distribution channel. These pharmacies are often the primary channel for biologics and bispecific antibodies since many are administered intravenously in controlled settings. They ensure proper cold chain storage, sterile compounding, and adherence to hospital protocols. These factors make hospital pharmacies critical for timely patient access to advanced therapies. Furthermore, the segment is set to hold 67.19% share in 2026.

- For instance, in February 2025, Walmart Canada launched its first pharmacy clinic in St. Catharines, Ontario. The development is anticipated to maximize the potential of professional pharmacists by enabling them to provide direct consultations and healthcare services. Such developments are expected to propel the growth of the hospital pharmacies segment in the forecasted period.

In addition, retail pharmacies as a distribution channel are projected to grow at a CAGR of 11.94% during the forecast period.

Bispecific Antibody Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

North America

North America Bispecific Antibody Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America region captured 51.80% of the global market in 2025, generating USD 21.49 billion in revenue, and is projected to reach USD 23.99 billion in 2026. The bispecific antibody market in North America is expected to grow strongly due to the region’s strong biotechnology ecosystem, extensive clinical trial activity, and high adoption of cutting-edge immunotherapies. The population in the region in the global bispecific antibodies market also witnesses favorable reimbursement frameworks coupled with significant healthcare spending, which supports rapid patient access to novel biologics.

Furthermore, accelerated approval from regulatory bodies such as the U.S. FDA and Health Canada enables the rapid commercialization of novel therapies. In 2026, the U.S. market is estimated to reach USD 22.86 billion.

- For instance, in November 2024, Jazz Pharmaceuticals plc received approval from the U.S. FDA for Ziihera (zanidatamab-hrii) 50mg/mL for injection for intravenous use for the treatment of adults with previously treated, unresectable, or metastatic HER2-positive (IHC 3+) biliary tract cancer (BTC). Such developments reinstate the region’s dominance in the market.

In the U.S., market growth is fueled by the large volumes of bispecific antibody clinical trials and early regulatory approvals globally. Strong uptake of newly approved therapies and a rising population of cancer in the country to heighten the demand and support growth. The presence of advanced manufacturing facilities and venture capital funding accelerates the commercialization of pipeline candidates, along with the rising prevalence of chronic diseases such as cancer. These factors boost the growth of the market in the country.

- For instance, in 2025, the American Cancer Society projected that by 2025 2,041,910 new cancer cases would emerge and 618,120 cancer deaths are projected to occur in the U.S. alone.

Europe

Europe maintained a strong presence in the global market, reaching USD 3.98 billion in 2025, accounting for 25.80% share, and is expected to reach USD 4.36 billion in 2026. This growth in the region is primarily due to strong oncology research hubs, innovation, and clinical adoption that facilitate product adoption. Improving healthcare infrastructure, and greater investment in biologics is expected to further support growth. Attributed by these factors, countries including the U.K. anticipate to record the valuation of USD 0.84 billion, Germany to record USD 1.03 billion in 2026 and France to record USD 0.64 billion in 2025.

Asia Pacific

In 2025, Asia Pacific generated USD 4.44 billion, contributing 15.90% to global market revenue, and is projected to grow to USD 5.01 billion in 2026. In the region, China is projected to reach USD 1.80 billion in 2025. The Japan market is projected to reach USD 1.59 billion by 2026, the China market is projected to reach USD 2.04 billion by 2026, and the India market is projected to reach USD 0.3 billion by 2026.

LATIN AMERICA & MIDDLE EAST & AFRICA

Over the study period, Latin America and Middle East & Africa regions would witness a moderate growth in this marketspace. The Latin America market generated USD 0.79 billion in 2025, representing 4.00% of the global market landscape, and is expected to reach USD 0.86 billion in 2026. Improving access to advanced biologics, rising cancer incidence, and government initiatives is expected to drive market growth in these regions further. In the Middle East & Africa, GCC is estimated to attain the value of USD 0.23 billion in 2025. Middle East & Africa recorded a market size of USD 0.46 billion in 2025, capturing 2.50% of the global market share, and is projected to reach USD 0.49 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Strategic Expansion Opportunities by Key Players to Propel Market Progress

The global bispecific antibody market holds a semi-consolidated market structure, constituting prominent players such as Bristol-Myers Squibb Company, Pfizer Inc., F. Hoffmann-La Roche Ltd, and AbbVie Inc. The significant share of these companies in the market is due to numerous strategic activities such as key mergers and acquisitions for robust product offerings, collaboration among operating entities for advancing, along a focus on research and development to enhance their market positions.

- For instance, in June 2025, BioNTech SE collaborated with Bristol Myers Squibb for the co-development and commercialization of the company’s investigational bispecific antibody BNT327 across numerous solid tumor types.

Other notable players in the global market include Genentech, Inc., Regeneron Pharmaceuticals Inc., and Harbour BioMed. These companies are anticipated to prioritize new product launches and collaborations to boost their global bispecific antibody market share during the forecast period.

LIST OF KEY BISPECIFIC ANTIBODY COMPANIES PROFILED

- Bristol-Myers Squibb Company (U.S.)

- Pfizer Inc (U.S.)

- Merck & Co., Inc. (U.S.)

- Candid Therapeutics (U.S.)

- Dualitas Therapeutics (U.S.)

- Genentech, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Regeneron Pharmaceuticals Inc. (U.S.)

- Harbour BioMed (Hong Kong)

KEY INDUSTRY DEVELOPMENTS

- August 2024: Merck & Co., Inc., acquired CN201, a novel investigational clinical-stage bispecific antibody for the treatment of B-cell-associated diseases, from Curon Biopharmaceutical. The development aimed to expand and diversify the company’s bispecific pipeline.

- December 2024: Merus N.V. received approval from the U.S. FDA for BIZENGRI (zenocutuzumab-zbco), indicated for adults with pancreatic adenocarcinoma or non–small cell lung cancer (NSCLC) that are advanced, unresectable, or metastatic and harbor a neuregulin 1 (NRG1) gene fusion who have disease progression on or after prior systemic therapy.

- January 2025: Biohaven Ltd. collaborated with Merus N.V. to co-develop three novel bispecific antibody drug conjugates (ADCs), leveraging Merus’ leading Biclonics technology platform and Biohaven’s next-generation ADC conjugation and payload platform technologies.

- July 2024: Dren Bio, Inc. collaborated with Novartis AG for the discovery and development of therapeutic bispecific antibodies for cancer using Dren Bio’s proprietary Targeted Myeloid Engager and Phagocytosis Platform.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 12.80% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Mechanism of Action, Application, Route of Administration, Distribution Channel, and Region |

|

By Mechanism of Action |

|

|

By Application |

|

|

By Route of Administration |

|

|

By Distribution Channel |

|

|

By Region |

North America (By Mechanism of Action, Application, Route of Administration, Distribution Channel, and Country)

Europe (By Mechanism of Action, Application, Route of Administration, Distribution Channel, and Country/Sub-region)

Asia Pacific (By Mechanism of Action, Application, Route of Administration, Distribution Channel, and Country/Sub-region)

Latin America (By Mechanism of Action, Application, Route of Administration, Distribution Channel, and Country/Sub-region)

Middle East & Africa (By Mechanism of Action, Application, Route of Administration, Distribution Channel, and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 34.72 billion in 2026 and is projected to reach 91.09 USD billion by 2034.

In 2025, the market value stood at USD 23.99 billion.

The market is expected to exhibit a CAGR of 12.80% during the forecast period of 2026-2034.

The T-cell engaging segment led the market by mechanism of action.

Increased prevalence of various forms of cancers, and key regulatory approvals is expected to lead to the market growth during the forecast period.

Bristol-Myers Squibb Company, Pfizer Inc., F. Hoffmann-La Roche Ltd, and AbbVie Inc., are the major players in the global market

North america dominated the bispecific antibody market with a market share of 51.80% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us