Butadiene Market Size, Share & Industry Analysis, By Derivative (Acrylonitrile-Butadiene-Styrene (ABS), Adiponitrile (ADN), Nitrile-Butadiene Latex (NBL), Styrene-Butadiene Latex (SBL), Polybutadiene Rubber (PBR), Styrene-Butadiene Rubber (SBR), and Others), By End-Use Industry (Automotive & Transportation, Plastics & Electronics, Construction & Infrastructure, Healthcare & Medical, and Others), and Regional Forecast, 2026-2034

Butadiene Market Size and Future Outlook

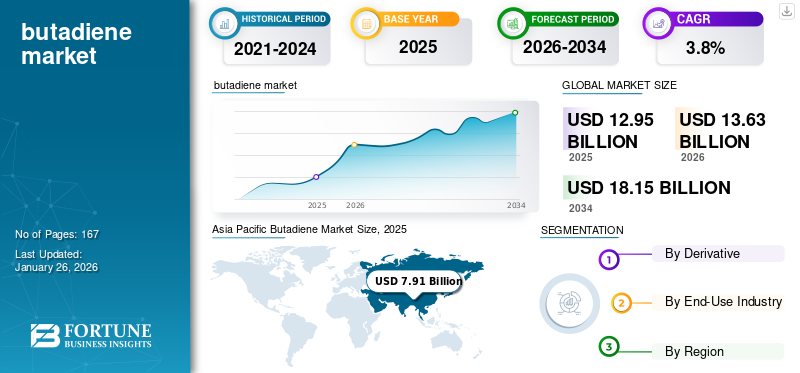

The global butadiene market size was valued at USD 12.95 billion in 2025. The market is projected to grow from USD 13.63 billion in 2026 to USD 18.15 billion by 2034, exhibiting a CAGR of 3.8% during the forecast period. Asia Pacific dominated the butadiene Market with a market share of 61% in 2025.

Butadiene is a key petrochemical building block used primarily as a monomer in the production of synthetic rubbers and thermoplastics. It provides critical properties such as elasticity, resilience, and abrasion resistance, making it indispensable in automotive tires, industrial rubber goods, plastics, and specialty chemicals. Its versatility ensures widespread use in industries where performance, durability, and cost-efficiency are essential, and alternatives including natural rubber or other polymers fall short.

The market is led by INEOS, Sinopec, LyondellBasell, TPC Group, and Versalis. Their large-scale production capacities, integration across downstream derivatives such as SBR, PBR, and ABS, and established presence in key geographies enable them to dominate the market. Continuous investments in technology upgrades, capacity expansions, and partnerships with the automotive and plastics industries further reinforce their competitive advantage and global influence.

Download Free sample to learn more about this report.

Butadiene Market Key Takeaways

- 2025 Market Size: USD 12.95 billion

- 2026 Market Size: USD 13.63 billion

- 2034 Forecast Market Size: USD 18.15 billion

- CAGR: 3.8% from 2026-2034

- Asia Pacific dominated the butadiene market with a 61.00% share in 2025.

- The polybutadiene rubber (PBR) segment accounted for a 33.35% share in 2026.

- The automotive & transportation segment held a 43.65% share in 2026.

Asia Pacific

Asia Pacific reached USD 7.91 billion in 2025 and is projected to grow to USD 8.32 billion in 2026.

Europe

Europe accounted for USD 2.88 billion in 2025 and is expected to reach USD 3.03 billion in 2026.

North America

North America stood at USD 1.60 billion in 2025 and is projected to reach USD 1.70 billion in 2026.

U.S.

The market is estimated to reach USD 1.52 billion in 2026.

Latin America

Latin America generated USD 0.27 billion in 2025 and is projected to reach USD 0.28 billion in 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Tire Production Fuels Stronger Pull on Product Demand

The automotive and tire industry is the primary engine driving market growth. Synthetic rubbers such as SBR and PBR, both heavily reliant on butadiene, are indispensable for producing durable, high-performance tires. As mobility expands in emerging economies and replacement cycles shorten in mature markets, tire manufacturers are creating a consistent and rising pull on demand.

This expansion in tire production directly translates into higher consumption, compelling producers to align capacity, pricing, and feedstock strategies with automotive sector growth. For market participants, keeping pace with tire industry trends is critical, as they remain the most decisive factor shaping near- and medium-term outlook.

- The U.S. Tire Manufacturers Association projects U.S. tire shipments to reach 338.9 million units in 2024, compared with 331.9 million units in 2023.

MARKET RESTRAINTS:

Feedstock Shifts Limits Consistent Supply

The market faces a structural restraint due to its dependence on steam cracker operations. Since it is produced as a by-product, changes in cracker feedstock directly impact availability. The industry’s increased reliance on lighter streams such as ethane favors ethylene production but yields fewer co-products, including butadiene. This shift has created supply tightness in regions including North America, even when downstream demand remains steady.

- The International Energy Agency highlights that lighter feedstock, such as ethane produces far lower yields of co-products such as butadiene compared with heavier naphtha feedstock.

MARKET OPPORTUNITIES:

Growth in Electric Vehicle Adoption to Drive Market

The accelerating adoption of electric vehicles is creating a strong opportunity for producers. EVs require specialized tires with lower rolling resistance and greater durability to handle higher torque and battery weight. These performance standards increase the demand for synthetic rubber such as SBR and PBR, both of which are butadiene-based. As EV penetration rises globally, tire manufacturers are placing greater reliance on these materials, creating a structural pull on demand.

- The International Energy Agency reports that global electric car sales surpassed 17 million units in 2024, representing more than 20 percent of all new car sales.

The strong connection between EV growth and advanced tire requirements is opening a long-term opportunity for the market. Unlike cyclical demand shifts, this linkage reflects a structural trend in mobility, giving producers a durable channel for growth as the automotive sector transitions to new technologies.

BUTADIENE MARKET TRENDS:

Shift Toward Lighter Cracker Feedstock Reshapes Market Dynamics

A key trend shaping the market is the move toward lighter cracker feedstocks such as ethane, particularly in North America and the Middle East. While this shift improves ethylene economics, it reduces the yield of co-products, including butadiene. As more crackers globally optimize for lighter slates, the industry is experiencing tighter supply relative to demand, pushing producers and end users to rethink sourcing strategies and regional balance.

- The U.S. Energy Information Administration reported that U.S. ethane production reached an average of 2.8 million barrels per day in 2024, up 7 percent from 2023, reflecting a continued shift toward lighter feedstock use in crackers.

MARKET CHALLENGES:

Price Volatility Creates Persistent Challenge for Market Stability

One of the most significant challenges in the market is price volatility, driven by its status as a co-product of steam crackers. As output depends on ethylene production and feedstock choices rather than direct demand, supply often swings out of sync with consumption trends. This mismatch results in sharp price fluctuations, which complicate procurement planning for downstream users and margin management for producers.

- The European Chemical Industry Council (Cefic) highlights that co-product dependency in petrochemicals such as butadiene increases exposure to feedstock and energy market volatility, creating imbalances between supply and demand cycles.

Download Free sample to learn more about this report.

Segmentation Analysis

By Derivative

Increasing Demand for High Performance Tires Strengthens Polybutadiene Rubber’s Role

On the basis of the segmentation of Derivative, the market is classified into acrylonitrile-butadiene-styrene (ABS), adiponitrile (ADN), nitrile-butadiene latex (NBL), styrene-butadiene latex (SBL), polybutadiene rubber (PBR), styrene-butadiene rubber (SBR), and others.

To know how our report can help streamline your business, Speak to Analyst

The polybutadiene rubber (PBR) segment accounted for the significant butadiene market share 33.35 in 2026. PBR is becoming one of the most critical derivatives in the market as automotive trends shift toward higher performance requirements. PBR offers resilience, wear resistance, and low heat build-up, making it indispensable in premium and heavy-duty tire formulations. Beyond tires, it also finds use in golf balls, industrial belts, and impact-resistant plastics, reflecting its versatility. These applications make PBR a strategic growth anchor in the overall market.

By End-Use Industry

Automotive and Transportation Drives Sustained Market Growth owing to Rising Product Demand from Tire Production

In terms of end-use, the market is categorized into automotive & transportation, plastics & electronics, construction & infrastructure, healthcare & medical, and others.

The automotive & transportation segment accounted for the largest share in 2025. In 2026, the segment is anticipated to dominate with a 43.65% share. The automotive and transportation sector continues to anchor global demand, primarily through its reliance on PBR and SBR for tire production. These materials provide durability, fuel efficiency, and safety, making them indispensable in both new and replacement tires. Rising vehicle ownership in emerging economies, coupled with steady replacement cycles in mature markets, ensures that automotive demand remains a stable and resilient product growth channel.

- Michelin reported in its 2024 results that the global passenger and light truck tire market grew by 2%, with replacement demand rising by 4%. While this data reflects only the passenger and light truck segment, it represents the largest outlet for SBR and PBR, making it a reliable indicator of the upward pull on product demand.

Construction & Infrastructure segment is expected to grow at a CAGR of 3.7% over the forecast period.

Butadiene Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and Middle East & Africa.

ASIA PACIFIC

Asia Pacific Butadiene Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific held 61.00% of the global market, reaching a valuation of USD 7.91 billion, and is projected to grow to USD 8.32 billion in 2026. Asia-Pacific is the leading region for product demand, anchored by its vast automotive industry and expanding downstream tire and plastics capacities. Rapid vehicle ownership growth in China, India, and Southeast Asia has made the region both the largest consumer and producer of synthetic rubber. Localized capacity additions reduce dependence on imports, giving the region a structurally resilient demand base. In 2026, the China market is estimated to reach USD 4.25 billion.

- The China Association of Automobile Manufacturers (CAAM) reported that China produced 31.28 million vehicles in 2024, including over 10 million new-energy vehicles, cementing its role as the largest global automotive hub and a key driver of product demand.

To know how our report can help streamline your business, Speak to Analyst

EUROPE

The Europe market was valued at USD 2.88 billion in 2025, capturing 22.00% of global revenue, and is estimated to reach USD 3.03 billion in 2026. Europe is anticipated to witness notable growth in the coming years. During the forecast period, the European region is projected to record a growth rate of 3.7%, and reach a valuation of USD 2.88 billion in 2025. Europe’s product demand is shaped by high-performance automotive applications and stringent regulatory standards. Tire makers and OEMs continue to require advanced synthetic rubbers to meet durability and efficiency goals, ensuring their continued role despite slower volume growth compared to APAC. Construction and specialty plastics also provide steady outlets. Backed by these factors, the U.K. is anticipated to record a valuation of USD 0.46 billion, Germany to record USD 0.76 billion, and France to record USD 0.42 billion in 2026.

NORTH AMERICA

North America accounted for USD 1.6 billion in 2025, representing 12.00% of the global market share, and is projected to reach USD 1.7 billion in 2026. North America’s demand is sustained by a large and aging vehicle fleet, steady replacement tire cycles, and the popularity of SUVs and light trucks that require performance-focused rubber. Innovation in tire technologies and regulatory push for efficiency standards support consistent consumption of SBR and PBR across the region. In 2026, the U.S. market is estimated to reach USD 1.52 billion.

- According to a report on North American production and sales, U.S. light vehicle output is forecast at ~15.5 million units in 2024, matching strong OEM activity and suggesting firm tire demand.

LATIN AMERICA

The Latin America region captured 2.10% of the global market in 2025, generating USD 0.27 billion in revenue, and is projected to reach USD 0.28 billion in 2026. in its valuation. Latin America presents a medium-term growth opportunity as automotive ownership expands and local tire and rubber manufacturing increases. Brazil remains the hub of automotive production in the region, while rising middle-class consumption sustains replacement tire demand. This gradual build-up of downstream industries is expected to support a stronger pull over time.

MIDDLE EAST & AFRICA

Middle East & Africa contributed approximately USD 0.29 billion to the global market in 2025, accounting for 2.00% share, and is expected to reach USD 0.3 billion in 2026. The Middle East and Africa currently contribute a smaller share of global demand but remain strategically important as emerging automotive and infrastructure markets. While much of the region relies on imports of synthetic rubber and derivatives, rising vehicle ownership and industrialization create incremental demand growth opportunities.

COMPETITIVE LANDSCAPE

Key Industry Players:

Consolidation Among Global Petrochemical Leaders Strengthens Supply and Innovation Capacity

The global market is moderately consolidated, with a group of large petrochemical and synthetic rubber producers driving production, technology improvements, and trade flows. These major players emphasize capacity expansions, downstream integration, and strategic partnerships with tire, automotive, and plastics manufacturers to secure long-term demand and reinforce their positions in the value chain.

Key players in the global market include INEOS, Sinopec, LyondellBasell, TPC Group, and Versalis. Their broad product portfolios across SBR, PBR, and ABS derivatives, combined with extensive cracker and processing capacities, give them significant influence in both regional and global markets. Their integration into downstream synthetic rubber and plastics further strengthens market control.

Other notable participants, such as LG Chem, LANXESS, SIBUR, Borealis, and Shell Chemicals, expand market competitiveness through targeted investments. These include bio-based product R&D, new elastomer grades, circular feedstock initiatives, and collaborations with automotive and electronics customers. Collectively, such initiatives enhance innovation pipelines and support broader adoption of product derivatives in high-growth end-use industries such as automotive, plastics & electronics, and construction.

LIST OF KEY BUTADIENE COMPANIES PROFILED:

- INEOS (U.K.)

- Shell (U.K.)

- TPC Group (U.S.)

- LyondellBasell Industries Holdings B.V. (Netherlands)

- Versalis S.p.A. (Italy)

- Borealis GmbH (Austria)

- PJSC SIBUR Holding (Russia)

- LG Chem (South Korea)

- LANXESS (Germany)

- China Petrochemical Technology Development Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS:

- Feb 2024: Borealis announced breakthroughs in circular technologies to convert waste into feedstock for its chemical production. These initiatives aim to reduce reliance on virgin fossil inputs and allow crackers to process recycled raw materials, indirectly affecting butadiene supply dynamics.

- March 2024: SIBUR’s Voronezhsintezkauchuk plant started producing new butadiene rubbers, including neodymium polybutadiene and soluble butadiene-styrene rubber. The project, worth 800 million rubles, keeps total capacity at 160 ktpa but adds higher-value grades.

- Aug 2023: INEOS and Sinopec signed their second 50:50 joint venture to build a 300,000 tpa ABS plant in Tianjin, China, using Terluran technology. Start-up is scheduled for April 2025. This follows their first 600,000 tpa ABS project in Ningbo.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. This market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.8% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Derivative, End-Use Industry, and Region |

|

By Derivative |

|

|

By End-Use Industry |

|

|

By Region |

o U.S. (By End-Use Industry) o Canada (By End-Use Industry)

o Germany (By End-Use Industry) o U.K. (By End-Use Industry) o France (By End-Use Industry) o Italy (By End-Use Industry) o Rest of Europe (By End-Use Industry)

o China (By End-Use Industry) o Japan (By End-Use Industry) o India (By End-Use Industry) o South Korea (By End-Use Industry) o Rest of Asia Pacific (By End-Use Industry)

o Brazil (By End-Use Industry) o Mexico (By End-Use Industry) o Rest of Latin America(By End-Use Industry)

o Saudi Arabia (By End-Use Industry) o South Africa (By End-Use Industry) o Rest of the Middle East & Africa (By End-Use Industry) |

Frequently Asked Questions

The global butadiene market size is projected to grow from $13.63 billion in 2026 to $18.15 billion by 2034, at a CAGR of 3.8% during the forecast period

In 2025, the market value stood at USD 7.91 billion.

The market is expected to exhibit a CAGR of 3.8% during the forecast period of 2026-2034.

The polybutadiene rubber (PBR) segment led the market by Derivative.

The key factors driving the market are the increasing tire demand in the automotive & transportation sectors.

INEOS, Sinopec, LyondellBasell, TPC Group, and Versalis are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Growth in electric vehicle adoption and rising construction, electronics, and healthcare industries are some of the factors that are expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us