Cabin Retrofit and Reconfiguration Market Size, Share & Industry Analysis, By Aircraft Platform (Narrowbody, Widebody, Regional, Business Aviation, and Military), By Retrofit Workscope (Layout & Capacity Changes, Class-Mix Reconfiguration, Cabin Product Refresh, & Others), By Cabin Workscope (Seats & Restraints, Monuments, Bins & Stowage, Lining & Interiors, and Others), By Offering (Cabin Design & Engineering, Certification & Approvals, Kits Supply, & Others), By End User (Airlines, Aircraft Lessors, Leisure Operators, Government / VIP Operators, and MROs), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

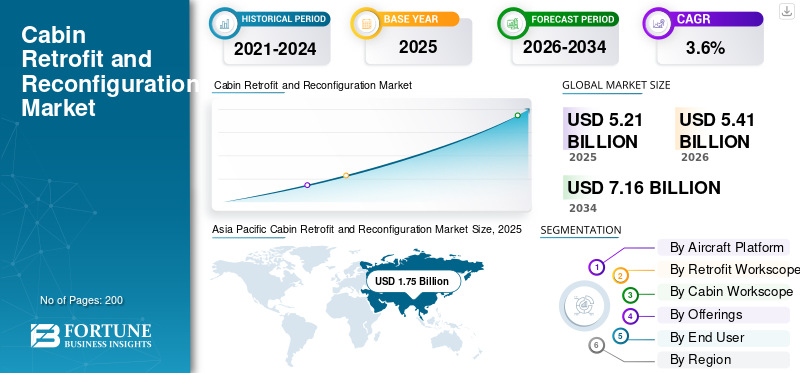

The global cabin retrofit and reconfiguration market size was valued at USD 5.21 billion in 2025. The market is projected to grow from USD 5.41 billion in 2026 to USD 7.16 billion by 2034, exhibiting a CAGR of 3.6% during the forecast period. Asia Pacific dominated the global cabin retrofit and reconfiguration market with a market share of 33.59% in 2025.

Cabin retrofit and reconfiguration involve upgrading cabin interiors and changing the cabin layout, including seat count, LOPA, monuments, and class mix, to enhance passenger comfort and enhance the overall experience while increasing operational efficiency. After the COVID-19 pandemic, airlines and low-cost carriers are focusing more on cabin reconfiguration, particularly for high-cycle narrow-body aircraft. At the same time, network carriers are refreshing premium cabins in wide-body aircraft. Several changes are mandated to go through certification routes regulated by the European Union Aviation Safety Agency and similar organizations worldwide.

Key players such as Lufthansa Technik, Safran Cabin, and Collins Aerospace assist airlines in providing upgrades more quickly by bundling engineering, kitting, and installation, often associated with maintenance, repair, and overhaul events. On the digital front, Panasonic Avionics and Thales InFlyt Experience continue to set new standards with cutting edge connectivity and in-flight entertainment systems, which are crucial for market growth in America and the Middle East & Africa.

Download Free sample to learn more about this report.

CABIN RETROFIT AND RECONFIGURATION MARKET TRENDS

Rise in OEM-Licensed Cabin Modification Networks Leading to Increasing Capacity and Standardization

A significant trend in the market is that OEMs and leading players are defining who can perform complex cabin work. This helps airlines achieve faster turnaround and consistent quality, along with easier certification processes. More upgrades are being packaged as known solutions through licensed maintenance repair and overhaul (MRO) capabilities, especially for wide body aircraft cabins, where downtime is costly and modifications are complicated. The outcome is more predictable cabin reconfiguration programs that still aim to enhance passenger comfort, enhance the passenger experience, and boost operational efficiency.

- In July 2024, Boeing and Lufthansa Technik announced a license agreement that designates Lufthansa Technik as the first Boeing-licensed Service Center for 787 Dreamliner cabin modifications. This agreement aims to increase interior modification capacity and options, with the first project expected to begin in 2025.

MARKET DYNAMICS

MARKET DRIVERS

Post Pandemic Fleet Life Extension and New Aircraft Delivery Delays to Drive Product Demand

Airlines keep their aircraft in service longer and use maintenance, repair, and overhaul (MRO) windows to push cabin reconfiguration projects. These updates protect profits and brand image. Such updates consists of new seats, refreshed cabin interiors, upgraded flight entertainment systems, and smarter layouts that improve passenger experience and operational efficiency. This trend is particularly strong on long-haul wide-body aircraft, especially in premium cabins and business class retrofits, and is anticipated to drive cabin retrofit and reconfiguration market growth. It is also seen in high-cycle narrow-body fleets where low-cost carriers and network airlines aim for better utilization and lower costs.

- In March 2025, Emirates, operating in the Middle East and Africa, shared plans to invest around USD 5 billion to refit about 220 aircraft. The airline is tying this investment to delivery delays and the need to maintain and expand its network while enhancing customer experience.

MARKET RESTRAINTS

Supply Chain Issues and Certification Backlogs to Create Delays in Cabin Reconfiguration

Cabin reconfiguration can be delayed by long lead times for key items. This is true in the case of premium seats, monuments, and in-flight entertainment systems. As these components are highly customized and strictly regulated, they often require additional time for testing, paperwork, and approvals before installation can begin. It becomes harder to schedule maintenance, aircraft downtime costs rise, and some operators choose to delay or phase upgrades. While this is especially noticeable on wide-body aircraft, high-volume narrow-body aircraft also feel the impact.

MARKET OPPORTUNITIES

Digital Cabin Retrofits (Connectivity and Next-Gen IFE) to Create Growth Opportunities

Airlines see fast Wi-Fi, smarter cabin networks, and modern inflight entertainment systems as tools for revenue and customer loyalty, opening up a strong retrofit opportunity. Operators can upgrade the onboard digital systems without waiting for new aircraft deliveries. They can often schedule this work during regular maintenance downtime. This leads to better passenger experience, improved operational efficiency, and a more future-ready platform for onboard services.

- In January 2025, Delta Air Lines and Thales announced a partnership to deliver Delta’s next-generation Delta Sync seatback experience. This is powered by Thales FlytEDGE, which is a cloud-based inflight entertainment system designed to enhance the connected passenger experience.

MARKET CHALLENGES

Limited MRO capacity and Skilled Labor Shortages to Emerge as Major Challenges

Large cabin retrofit and reconfiguration jobs usually require hangar space during planned heavy checks and specialized technicians, engineers, and certification support. Currently, the industry’s MRO system is under pressure due to issues with capacity, labor, and parts flow. As a result, airlines often struggle to secure slots. Even ready-to-go cabin kits can be waiting for available workers or shop space. This leads to longer aircraft downtime, higher shop rates, and more phased upgrades instead of completing everything in one visit. This is particularly challenging for widebody cabins, where each day out of service is costly.

- In July 2024, GE Aerospace planned a USD 1 billion investment to expand and upgrade its engine MRO network. This move aims to reduce turnaround times. The company specifically pointed to capacity shortages, labor constraints, and supply chain issues in the MRO system, as airlines keep aircraft in service longer due to delivery delays.

Impact of Russia Ukraine War

Sanctions and Compliance Controls Limit Russia-linked Cabin Retrofit Work and Create Supply Chain Challenges

The Russia-Ukraine war brought a significant alteration in air routes and also changed what is permitted. EU restrictive measures prevent the provision of aircraft parts and technical support to Russia or for use in Russia, which directly reduces access to OEM-grade cabin interiors (seats, monuments, and IFE spares) and Western MRO support. Even outside Russia, companies are tightening screening and paperwork to avoid end-use risk. This approach can delay the movement of cabin kits and STC workflows across borders, affecting cabin retrofit and reconfiguration industry expansion.

- In March 2022, EASA’s FAQs on restrictive measures, coordinated with the EU Commission, clarified how EU sanctions impact maintenance and continuing airworthiness as well as the provision of services and parts for aircraft intended for use in Russia. This references the EU sanctions framework (Reg. 833/2014 as amended).

Download Free sample to learn more about this report.

Segmentation Analysis

By Aircraft Platform

Narrowbody Segment Leads Due to High Volume and Use of Short-Haul Fleets

In terms of aircraft platform, the market is categorized into narrowbody, widebody, regional, business aviation, and military.

The narrowbody aircraft (A320 family, 737 family) segment dominates the market as these aircraft operate the most cycles and carry the majority of short-haul passengers. As a result, airlines refresh cabin interiors more often. They usually combine cabin reconfiguration (seat count, class mix, bins, lighting, and connectivity/IFE) with scheduled maintenance visits to improve passenger experience and operational efficiency. This effect is even greater with the rise of low-cost carriers, where small changes in layout and cabin products have a direct impact on unit economics and revenue per flight.

- In June 2025, Boeing’s 2025 Commercial Market Outlook reported that single-aisle aircraft will account for 72.00% of the global fleet, up from 66.00% in 2024. This increase is mainly driven by short-haul travel and low-cost carriers. This growth explains why narrowbody-led cabin retrofit demand is the highest compared to other categories by aircraft platform.

The business aviation segment is expected to show the fastest growth at a CAGR of 4.7% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Retrofit Workscope

Cabin Product Refresh Segment Leads due to Frequent Brand Maintenance

On the basis of retrofit workscope, the market is classified into layout & capacity changes, class-mix reconfiguration, cabin product refresh, digital cabin upgrades, and mandate-driven mods.

The cabin product refresh segment dominates the market as it is the most repeatable retrofit job. Airlines can swap or renew seats and soft goods, update panels, carpets, lighting, and selected cabin hardware during planned maintenance repair and overhaul visits without the complexity of a full cabin reconfiguration. This approach works for both narrow-body and wide-body aircraft fleets, making it the top workscope by volume and a significant source of value as airlines seek to enhance passenger comfort while keeping aircraft in service.

- In September 2024, Air India announced a USD 400 million program to refurbish cabin interiors on 67 aircraft, which is over half its fleet. This initiative covers both A320neo narrowbodies and 787/777 widebodies, showing how refresh work scales across fleets and drives most retrofit activity.

The digital cabin upgrades segment is expected to show the fastest growth at a CAGR of 5.1% over the forecast period.

By Cabin Workscope

Direct Effect on Comfort, Yield, and Safety Rules to Drive the Seats & Restraints Segment Growth

Based on cabin workscope, the market is segmented into seats & restraints, monuments, bins & stowage, lining & interiors, lighting & passenger comfort, and others.

The seats & restraints segment led the global cabin retrofit and reconfiguration market share in 2025. Seats typically make up the largest part of materials and labor in any cabin refresh or reconfiguration. Airlines replace them to improve passenger comfort, change class mix (premium economy/business), and increase density and operational efficiency. They must also meet strict safety standards (seat and restraint certification/testing). Once an airline decides to replace seats, it becomes a top priority. This task often shapes the entire retrofit visit for both narrow body and wide body aircraft.

The others segment, which consists of connectivity/IFE/power and cabin systems integration, is the fastest growing and is poised to expand at a CAGR of 5.8% during the forecast period.

By Offering

Installation and Modification Segment Leads with Major Share of Retrofit Budget

Based on offering, the market is segmented into cabin design & engineering, certification & approvals, kits supply, installation & modification, and post-mod support.

The installation & modification segment dominates the market. The real costs and time depend on the aircraft itself and not on the design. The services include removing the old cabin; installing seats, monuments, and bins; running wiring for power and in-flight entertainment systems; performing checks; and completing paperwork before the aircraft returns to service. Since this work is part of an MRO visit, often during heavy checks, installation and modification naturally receive the largest share of the retrofit budget, especially for complex cabin reconfigurations on widebody aircraft.

The certification & approvals segment is expected to show the fastest growth at a CAGR of 5.3% over the forecast period.

By End User

Airlines Dominate Due to their Control over Cabin Branding, Revenue Strategy, and Fleet Uptime

The market is segmented, by end user, into airlines, aircraft lessors, leisure operators, government / VIP operators, and MROs.

The airlines segment held the largest market share in 2025. Airlines experience the highs and lows of cabin performance every day, including seat revenue, premium yield, customer satisfaction, and turnaround efficiency. Hence, they lead spending on cabin refresh and reconfiguration. They decide the class mix, choose the seat and in-flight entertainment standards, and schedule the work around heavy-check maintenance windows to reduce aircraft downtime. Lessors influence specifications at transitions, but airlines generally manage the major, recurring retrofit cycles for both narrowbody and widebody fleets.

- In March 2025, Emirates announced plans to invest around USD 5 billion to refit 220 aircraft. This move aims to sustain and expand its network amid delays in new aircraft deliveries. It demonstrates that airlines are the main decision-makers and spenders for large-scale cabin retrofit programs.

The government/VIP operators segment is expected to show the second fastest growth at a CAGR of 3.5% during the forecast period.

Cabin Retrofit and Reconfiguration Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world (Middle East & Africa and Latin America).

Asia Pacific

Asia Pacific Cabin Retrofit and Reconfiguration Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global market in 2025 and is estimated to expand at a CAGR of 4.1% over the forecast period. The regional market spans China, India, Japan, and the rest of Asia Pacific, where many narrow body aircraft are entering service with high usage rates. Airlines are continually updating cabin interiors to remain competitive. This leads to more frequent cabin reconfigurations and updates, including seats, monuments, lighting, connectivity, and in-flight entertainment systems. These updates are often scheduled during heavy maintenance checks so that aircraft do not remain grounded for long. Based on these factors, China is expected to reach a valuation of USD 0.64 billion and India, USD 0.29 billion, by 2026.

North America

North America has a high-frequency cabin retrofit market as airlines operate large fleets of narrow-body aircraft. The U.S. held the largest share of around 90.66% in the regional market in 2025. The demand for cabin retrofits mainly involves narrow-body aircraft. High-cycle fleets are refreshed frequently to maintain reliability and improve passenger experience along with operational efficiency. Airlines plan cabin reconfigurations and refreshes during heavy maintenance windows. Furthermore, there is a strong push for digital upgrades, such as Wi-Fi and in-flight entertainment systems, to stay competitive in a challenging market.

Europe

Europe is expected to see significant market growth in the cabin retrofit and reconfiguration market in the coming years. During the forecast period, the Europe region is projected to grow at a CAGR of 2.7%. The market in Europe reached USD 1.27 billion in 2025. In this region, the U.K. and Germany are expected to reach USD 0.18 billion and USD 0.21 billion, respectively, in 2026. Europe’s retrofit market is influenced by a strict certification culture and the European Union Aviation Safety Agency (EASA) framework. This means that engineering and approvals play a major role in how programs operate. The region also has strong capabilities among key players, with Lufthansa Technik standing out as an important integrator. They handle both premium cabin work for wide-body aircraft and refresh cycles for narrow-body planes.

Rest of the World

The rest of the world, including Latin America and the Middle East & Africa, accounted for a share of 13.77% in 2025. This is the fastest-growing regional segment and is poised to grow at the highest CAGR of 4.5% over the forecast period. In Latin America, retrofit work focuses on cost-effective updates and densification of narrowbody aircraft. This often happens during scheduled maintenance to reduce downtime. In the Middle East and Africa, premium cabins on widebody planes and standards for long-haul products lead to more valuable reconfigurations and digital upgrades. As a result, the region leans more toward premium interiors, connectivity, and brand-oriented cabin programs.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Integrating their Engineering Capabilities with Paperwork Precision to Gain an Edge

The cabin retrofit and reconfiguration market is tough and has limited capacity. The main challenge is not new ideas but getting aircraft into hangars and then back out with certified and compliant cabin interiors. For anything beyond minor changes, gaining approvals and ensuring compliance, especially under the European Union Aviation Safety Agency framework and tools such as CS-STAN, become major problems. Established integrators with strong engineering and paperwork skills tend to succeed. After the COVID-19 pandemic, the push to improve passenger comfort and operational efficiency, particularly on high-cycle narrow-body aircraft, remains steady and aligns with the growth of the broader services market, often highlighted by compound annual growth rate (CAGR) forecasts and market size figures.

Around this, cabin OEMs, such as Safran and Collins, along with digital specialists in connectivity and flight entertainment systems, compete by offering more modular and faster-to-certify solutions. However, the seat shortage has significantly impacted the market, with customization issues and a lack of certification engineers delaying programs. In the U.S., the Middle East, and Africa, airlines are responding to delivery delays by investing heavily in retrofits. Emirates’ roughly USD 5 billion program shows how operators prioritize keeping the fleet modern instead of waiting for new aircraft.

LIST OF KEY CABIN RETROFIT AND RECONFIGURATION COMPANIES PROFILED

- Lufthansa Technik AG (Germany)

- Safran Cabin (France)

- Collins Aerospace (U.S.)

- Thales InFlyt Experience (France)

- Panasonic Avionics Corporation (U.S.)

- ST Engineering Aerospace (Singapore)

- HAECO Group (Hong Kong)

- AAR Corp. (U.S.)

- Diehl Aviation (Germany)

- RECARO Aircraft Seating (Germany)

- Safran Seats (France)

- JAMCO Corporation (Japan)

- FACC AG (Austria)

- Air France Industries KLM Engineering & Maintenance (France/Netherlands)

- Sabena technics (France)

- SR Technics (Switzerland)

- Turkish Technic (Turkey)

- Etihad Engineering (UAE)

- Viasat (U.S.)

- Gogo Business Aviation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- In November 2025, Emirates and Safran Seats signed a memorandum of understanding to set up an aircraft seat manufacturing and assembly facility in Dubai. The target completion is Q4 2027, with an initial output of up to 1,000 business-class seats per year.

- In January 2025, Thales and Delta Air Lines revealed the next-gen Delta Sync seatback experience powered by FlytEDGE, which is a cloud-native IFE system. This highlights the shift toward upgrades in digital cabins.

- In September 2024, Air India announced the start of its USD 400 million refit program for 67 legacy aircraft. This program would cover new seats and refreshed cabin interiors for both narrowbody and widebody fleets.

- In July 2024, Boeing and Lufthansa Technik signed a license agreement. This made Lufthansa Technik the first Boeing-licensed Service Center for 787 Dreamliner cabin modifications. The first project is set to start in 2025.

- In February 2024, Saudia announced new seating for upcoming B787s and a seat retrofit program for its current A330 and B777 fleet, planned from late 2025 to late 2027.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 3.6% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Aircraft Platform · Narrowbody · Widebody · Regional · Business Aviation · Military |

|

By Retrofit Workscope · Layout & Capacity Changes · Class-Mix Reconfiguration · Cabin Product Refresh · Digital Cabin Upgrades · Mandate-Driven Mods |

|

|

By Cabin Workscope · Seats & Restraints · Monuments · Bins & Stowage · Lining & Interiors · Lighting & Passenger Comfort · Others |

|

|

By Offering · Cabin Design & Engineering · Certification & Approvals · Kits Supply · Installation & Modification · Post-Mod Support |

|

|

By End User · Airlines · Aircraft Lessors · Leisure Operators · Government / VIP Operators · MROs |

|

|

By Region |

· North America (By Aircraft Platform, By Retrofit Workscope, By Cabin Workscope, By Offerings, By End User, and By Country) o U.S. (By Aircraft Platform) o Canada (By Aircraft Platform) · Europe (By Aircraft Platform, By Retrofit Workscope, By Cabin Workscope, By Offerings, By End User, and By Country) o U.K. (By Aircraft Platform) o Germany (By Aircraft Platform) o France (By Aircraft Platform) o Netherlands (By Aircraft Platform) o Russia (By Aircraft Platform) o Rest of Europe (By Aircraft Platform) · Asia Pacific (By Aircraft Platform, By Retrofit Workscope, By Cabin Workscope, By Offerings, By End User, and By Country) o China (By Aircraft Platform) o India (By Aircraft Platform) o Japan (By Aircraft Platform) o South Korea (By Aircraft Platform) o Indonesia(By Aircraft Platform) o Rest of Asia Pacific (By Aircraft Platform) · Rest of the world (By Aircraft Platform, By Retrofit Workscope, By Cabin Workscope, By Offerings, By End User, and By Country) o Latin America (By Aircraft Platform) o Middle East & Africa (By Aircraft Platform) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.41 billion in 2026 and is projected to reach USD 7.16 billion by 2034.

In 2025, the North America market value stood at USD 1.47 billion.

The market is expected to exhibit a CAGR of 3.6% during the forecast period of 2026-2034.

The narrowbody segment leads the market by aircraft platform.

Post pandemic fleet life extension and new aircraft delivery delays are key factors driving the market.

Lufthansa Technik AG, Safran Cabin, Collins Aerospace, Thales InFlyt Experience, Panasonic Avionics Corporation, ST Engineering Aerospace, HAECO Group, AAR Corp., Diehl Aviation, and RECARO Aircraft Seating, among others are the top companies in the market.

Asia Pacific dominated the market in terms of share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us