Predictive Airplane Maintenance Market Size, Share & Industry Analysis, By Aircraft Type (Fixed Wing, Rotary Wing, and UAVs & Urban Air Mobility), By Fleet Age (Mid-Life (6–12 yrs), Young (0–5 yrs), and Mature (13+ yrs)), By System Monitored (Airframe & Structures, Engines & APU, Landing Gear & Brakes, & Others), By Product Offerings (Analytics Platforms (SaaS) & Apps, Digital Twins & Physics/Hybrid Models, Edge Hardware & Embedded Health Systems, & Others), By Deployment Model (Hybrid, Single-Tenant Cloud, and On-Premise), By Solution, By End User, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

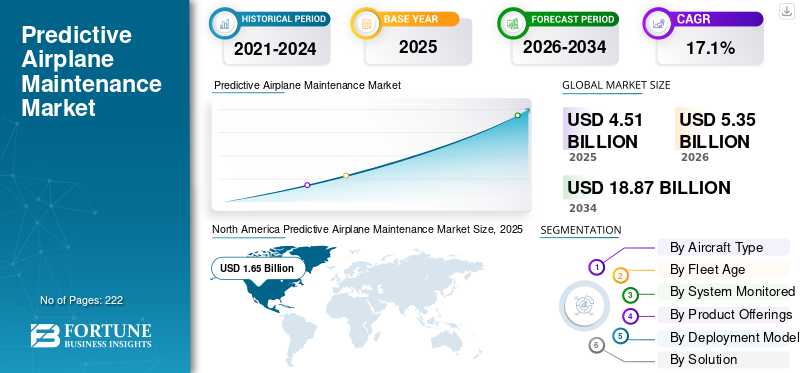

The global predictive airplane maintenances market size was valued at USD 4.51 billion in 2025 and is projected to grow from USD 5.35 billion in 2026 to USD 18.87 billion by 2034, exhibiting a CAGR during the forecast period of 17.1%. North America dominated the global market with a share of 36.59% in 2025.

Predictive airplane maintenance involves continuously monitoring the health of aircraft components and engines, using physics-based and machine-learning models, along with analyzing maintenance records. This helps estimate the remaining useful life (RUL) and schedule interventions before any failures occur. From 2026 to 2034, the market is expected to grow as aircraft connectivity and the number of sensors increase. The main factors driving this growth include the need for higher dispatch reliability, a reduction in unscheduled removals, lower costs of edge computing and SATCOM, workforce constraints in maintenance, repair, and operations (MRO), and goals for efficiency and sustainability that promote optimal timing of tasks.

Key players include Airbus (Skywise), Boeing (AHM/AnalytX), GE Aerospace (engine health management and digital twins), Rolls-Royce (IntelligentEngine/Blue Data Thread), Pratt & Whitney (EngineWise), Safran (Prognos), Honeywell (Forge), Collins Aerospace (aircraft health monitoring), Lufthansa Technik (AVIATAR), IFS Maintenix, Swiss-AS AMOS, Ramco, and among others. These companies provide data platforms that collect fleet telemetry, connect predictions to maintenance planning and supply chain actions, and reduce downtime through connected troubleshooting and automated work card creation.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Outcome-Based Uptime Deals and Airline Adoption of OEM Predictive Platforms are Accelerating Market Growth

Airlines and OEM/MROs are tying revenue and penalties to aircraft availability. This makes advanced predictive maintenance strategies an important tool for meeting dispatch reliability service level agreements, reducing unscheduled removals, and positioning parts and slots in advance, in turn driving the predictive airplane maintenance market growth. This connection, along with better integration between predictive platforms and maintenance/engineering systems, is encouraging carriers to standardize on OEM analytics stacks and connected maintenance workflows across large fleets. Moreover, Airlines and OEMs/MROs are connecting revenue and penalties to aircraft availability. This makes artificial intelligence powered analytics key to proactive maintenance strategies. These strategies help meet dispatch reliability service level agreements, reduce unscheduled removals, and prepare parts and slots in advance.

- For instance, in February 2025, Emirates signed an agreement with Airbus to implement Skywise Fleet Performance+ (S.FP+) and the Core X3 analytics platform. Their goal is to improve dispatch reliability for the A380/A350 fleet.

MARKET RESTRAINTS

Supply Chain and MRO Capacity Constraints are Hindering Scalable Deployment

Even when faults are predicted, limited shop capacity, long parts lead times, and engine availability issues delay planned removals. This forces operators back into reactive maintenance. These problems increase maintenance costs, lengthen turnaround times, and weaken the ROI of predictive programs by preventing timely execution of planned interventions.

- For instance, in October 2025, IATA, along with Oliver Wyman, estimated that airlines would face over USD 11 billion in additional costs due to ongoing supply-chain disruptions. This includes USD 3.1 billion for extra maintenance and USD 2.6 billion for leased engines during delayed shop visits. Highlighting the capacity and parts constraints facing maintenance operations.

MARKET OPPORTUNITIES

Regulatory Acceptance of E-Records and e-Techlogs Enables Closed-Loop Predictive Execution

As authorities establish guidelines for electronic signatures, recordkeeping, and electronic technical logbooks, airlines can turn predictive alerts into authorized digital workcards and maintenance records. This eliminates paper delays, speeds up approval processes, and allows for scalable updates across mixed fleets. It transforms prognostics into quicker, trackable task execution and measurable availability improvements.

- For example, in January 2025, the FAA issued AC 120-78B, updating standards for electronic signatures, recordkeeping, and manuals that meet 14 CFR requirements. This provides a clear acceptable way to comply with fully digital maintenance records.

PREDICTIVE AIRPLANE MAINTENANCE MARKET TRENDS

Open OEM, M&E Integrations are Turning Predictions into Executable Workflows

Airlines are standardizing on open interfaces that connect OEM engine and airframe health data streams to maintenance and engineering (M&E) systems. This allows predictive alerts to automatically generate workcards, parts kits, and shop-slot reservations. As a result, it reduce costs, time and aircraft-on-ground exposure, while schedule adherence improves. Additionally, Airlines are standardizing on open interfaces that connect OEM health data streams to M&E systems, while embedding artificial intelligence models for anomaly detection, remaining-useful-life estimation, and automated workcard creation.

- For example, in April 2025, Trax and Rolls-Royce launched an interface that links Trax eMRO with Blue Data Thread. This enables real time data exchange. Predicted engine issues can then trigger maintenance actions and reduce downtime.

MARKET CHALLENGES

Data Governance and Cybersecurity Compliance Requirements Are Slowing Cross-Enterprise Integration

Predictive maintenance strategies requires continuous telemetry sharing among airlines, OEMs, and MROs. However, new information security rules add controls on data access, storage, and exchange. Compliance programs, audits, and risk management related to these rules increase integration costs, delay deployment timelines, and limit the movement of health and usage data across organizational boundaries.

- For example, in February 2023, the EU adopted Implementing Regulation (EU) 2023/203, which sets mandatory information security risk management requirements for aviation organizations. These organizations must implement these rules alongside enhance safety processes. This directly impacts the data flows that predictive maintenance solutions depends on.

Russia Ukraine War Impact

Sanctions, Airspace Closures, and Titanium Re-sourcing Are Reshaping Predictive Maintenance Solutions Execution

The conflict has tightened critical inputs and logistics that predictive programs rely on. Sanctions and export controls, along with the politicization of Russian titanium, have forced OEMs and airlines to seek alternatives to VSMPO-linked supply. This shift has extended lead times for structural and engine-grade parts and complicated planned removals. At the same time, detours from Russian airspace due to closures in Europe and Asia have lengthened flight times and duty cycles. This situation raises the demand for maintenance driven by utilization and puts pressure on shop capacity. As a result, it is more challenging to turn predictions into timely workscopes. This means more buffer inventory, longer planning horizons, and a greater dependence on digital scheduling to secure slots, materials, and labor.

- For instance, in April 2024, Airbus Aerostructures signed a Master Supply Agreement with Norsk Titanium to reduce reliance on Russian titanium after the invasion. This highlights the need for structural re-sourcing of aerospace-grade titanium.

- In 2024, a peer-reviewed study found that closures of Russian and Ukrainian airspace led to significant detours on Europe-Asia routes. This increase in travel times and operational costs puts additional pressure on maintenance planning cycles.

Download Free sample to learn more about this report.

Segmentation Analysis

By Aircraft Type

Due to Size of Commercial Airline Fleets and Established OEM Platforms, Fixed-Wing Segment Leads Market

In terms of aircraft type, the market is categorized into fixed wing, rotary wing, and UAVs & urban air mobility.

Fixed-wing segments holds largest predictive airplane maintenance market share in 2025. Fixed-wing aircraft segments consist of narrow-body, wide-body, freighters, regional jets, and business jets. Commercial jets, produce the highest amount of operational telemetry. They also integrate deeply with OEM predictive platforms. Predictive alerts are often turned into planned workcards, parts kitting, and slot reservations. High usage, standardized electronic records, and widespread use of airframe and engine health monitoring make fixed-wing programs the main focus for spending and measurable improvements in reliability.

For instance, in October 2025, Korean Air agreed to implement Airbus’ upgraded Skywise Fleet Performance+ across its Airbus fleet to improve operational reliability and predictive maintenance solutions.

UAVs & urban air mobility segment is fastest growing segment in market expected to grow at a CAGR of 26.2% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Fleet Age

Record Utilization and Deferred Replacements, Mid-Life (6–12 yrs) Segment Dominates Market

On the basis of fleet age, the market is classified into mid-life (6–12 yrs), young (0–5 yrs), and mature (13+ yrs).

Mid-life aircraft are flying the most cycles. They are beyond early-life warranty limits and before late-life retirements, making them the top candidates where predictive alerts lead to meaningful, profit-positive maintenance. This includes planned removals, parts kitting, and slot booking. With delivery delays and limited capacity pushing airlines to make the most of their existing assets, mid-life jets support most telemetry-driven programs. They also experience the quickest conversion of predictions into completed workcards.

For instance, in August 2025, IATA reported record fleet utilization due to aircraft delivery delays and limited capacity growth. This situation forced operators to retain and work their existing aircraft harder, which increased maintenance planning for in-service mid-life fleets.

Young (0–5 yrs) segment is fastest growing segment in market expected to grow at a CAGR of 19.0% over the forecast period.

By System Monitored

Uptime-Critical Economics and Mature Health Monitoring, Engines and APU Segment Dominates Market

Based on system monitored segment, the market is segmented into, airframe & structures, engines & APU, landing gear & brakes, avionics, electrical power, and environmental/pressurization.

Engines & APU segments dominates the market share. They have the most developed embedded health monitoring, digital twins, and service models based on outcomes. Detailed engine telemetry allows for accurate remaining useful life estimates. These estimates reliably prompt planned shop visits, parts preparation, and slot reservations. This process converts predictions into measurable time-on-wing and improved dispatch reliability. APUs follow similar patterns, enhancing predictive execution across the propulsion ecosystem.

For instance, in April 2025, Trax and Rolls-Royce introduced an interface that connects Trax eMRO with Blue Data Thread. This integration streams engine data into maintenance workflows and reduce downtime from anticipated issues.

Electrical power segment is fastest growing segment in market expected to grow at a CAGR of 19.1% growth across the forecast period.

By Product Offerings

Bundled Availability Deals and Proprietary Health Data, Integrated OEM Offerings Dominate Market

Based on product offerings, the market is segmented into analytics platforms (saas) & apps, digital twins & physics/hybrid models, edge hardware & embedded health systems, integrated OEM offerings, data integration & exchange, and managed services (data science/mlops/change management).

Integrated OEM offerings dominates the market share. Advanced predictive maintenance strategies earns the most money when it is part of OEM service programs, such as power-by-the-hour or availability contracts, that use proprietary engine and airframe data along with digital twins. These bundles connect predictions directly to authorized workscopes, parts supply, and shop slots. They turn forecasts into guaranteed uptime on a large scale, which focuses spending on OEM-integrated offerings instead of standalone apps or tools.

Pratt & Whitney’s EngineWise Intelligence claims it offers predictive analytics and engine health management for over 10,000 engines across about 140 customers, as part of OEM services. This demonstrates the scale and integration benefits of OEM bundles.

Digital Twins & Physics/Hybrid Models segment is fastest growing segment in market expected to grow at a CAGR of 19.8% growth across the forecast period.

By Deployment Model

On-Aircraft Data Capture Needs and Real-Time Turnarounds, Hybrid (Cloud + Edge) Model Dominates Market

Based on deployment model, the market is segmented into multi-tenant saas, hybrid (cloud + edge), single-tenant cloud, and on-premise.

Hybrid (Cloud + Edge) segments dominates by holding the largest market share in 2025. Segment dominance is attributed to advanced predictive maintenance needs continuous, high-quality data from aircraft systems and quick analytics. Airlines now process data and detect events on aircraft/interface devices, called edge devices. They rely on cloud platforms for fleet-level models, learning loops, and workcard management. This hybrid setup reduces satellite communication bandwidth, speeds up alerts, and makes predictions usable within short turnaround times.

For instance, in April 2023, American Airlines started installing Collins Aerospace InteliSight Aircraft Interface Devices on over 500 aircraft. These devices capture and securely send flight and maintenance data to Collins’ GlobalConnect ground platform. This is a clear edge-plus-cloud structure that supports reliability and predictive models.

Multi-Tenant SaaS is set to grow at rate of 18.6% growth across the Predictive Airplane Maintenance market forecast period

By Solution

Direct Time-on-Wing Gains and Shop-Visit Planning Impact, RUL Prediction (Components) Dominates Market

Based on solution, the market is segmented into rul prediction (components), spare parts forecasting, fault detection & isolation, maintenance slot optimization, and reliability-centered analytics, and fuel/performance optimization

RUL Prediction (aircraft components) segments dominates the market holding the largest market share. The dominance is attributed to Remaining Useful Life (RUL) estimation delivers the financial outcome in predictive maintenance solutions fewer unscheduled removals, optimized shop-visit timing, and higher engine/component utilization. Accurate RUL drives material pre-positioning, workscope definition, and slot booking, ensuring predictions translate into executed maintenance actions and measurable availability gains across large fleets. Artificial intelligence-driven RUL estimation underpins proactive maintenance strategies by reducing unscheduled removals, optimizing shop-visit timing, and maximizing component time-on-wing.

For instance, in July 2024, Rolls-Royce’s TotalCare agreement with Vietjet emphasized operational certainty and time-on-wing benefits, noting the service is supported by data from cutting edge engine health monitoring, i.e., predictive analytics feeding planned shop visits.

Maintenance Slot Optimization is set to grow at rate of 18.9% growth across the Predictive Airplane Maintenance market forecast period

By End User

Fleet Scale, Reliability SLAs, and Deep OEM Integrations, Network/Legacy Airlines Dominate Market

Based on end user, the market is segmented into low-cost carriers (lccs), cargo operators, independent mros, network/legacy airlines, OEM aftersales, and business aviation operators.

Network/legacy carriers operate the largest market share, most complex fleets with high utilization and strict on-time performance targets, so predictive programs deliver outsized ROI through fewer unscheduled removals, optimized shop visits, and guaranteed availability under outcome-based service deals. Their long-standing OEM/MRO relationships and mature IT stacks also mean predictive alerts are tightly linked to e-records, planning, and parts logistics—converting insights into executed work at scale.

For instance, in October 2025, Korean Air signed to implement Airbus’ Skywise Fleet Performance+ across its Airbus fleet to enhance operational reliability via predictive maintenance.

OEM Aftersales is set to grow at rate of 18.9% growth across the predictive airplane maintenance market forecast period

Predictive Airplane Maintenance Market Regional Outlook

Fleet Scale, Edge-to-Cloud Adoption, and Regulatory Enablement, North America Dominates Market

By geography, the market is categorized into Europe, North America, Asia Pacific, Rest of the World (Middle East & Africa, and Latin America).

NORTH AMERICA

North America Predictive Airplane Maintenance Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 valuing at USD 1.38 billion and also took the leading share in 2025 with USD 1.65 billion, led primarily by the U.S., which alone contributes over 91.18% share in 2025 of the regional share. The U.S. leads in regional leadership. The largest global carrier fleets, including AA, UA, DL, and WN, generate significant data and have switched to edge-to-cloud setups that support predictive workflows.

Asia Pacific, Europe, and Rest of the world (Middle East & Africa, and Latin America) are expected to see significant growth in the predictive airplane maintenance market in the coming years.

EUROPE & ASIA PACIFIC

During the forecast period, the Europe region is projected to have a growth rate of 15.8%. The market in Europe is estimated to be USD 1.20 billion in 2025. In this region, both the France and Germany are expected to reach USD 0.21 billion and USD 0.19 billion, respectively, in 2026. Additionally, in Asia Pacific, countries including China, India, Japan, and Singapore rapid growth from major flag carriers adopting OEM predictive platforms at fleet scale in this region is resulting region growth e.g., Korean Air’s adoption of Airbus S.FP+ is lifting penetration and maturing closed-loop execution. Based on these factors, countries such as China expect to reach a valuation of USD 0.46 billion, and India is set to reach USD 0.21 billion by 2026.

REST OF THE WORLD

Meanwhile, Rest of the world (Middle East & Africa, and Latin America) contributes approximately 7.09% in 2025. Adoption is expanding via selective flagship programs and OEM service bundles, with growth tied to fleet modernization, connectivity upgrades, and integration with M&E/e-records in mixed-age fleets. In South Africa, carriers and MROs are increasingly aligning with OEM platforms and regional connectivity improvements to plug predictive insights into day-to-day maintenance execution. On the other hand, Latin America’s predictive airplane maintenance market is growing driven by major aviation hubs including Brazil, Mexico, Colombia, Chile, and Argentina are working to update their fleets while keeping operating costs down.

COMPETITIVE LANDSCAPE

Key Industry Players

OEM-Bundled Services and Open M&E Integrations are Consolidating Power as Predictive Maintenance Industrializes at Fleet Scale

Engine and airframe OEMs lead the way GE Aerospace, Rolls-Royce, Pratt & Whitney, Safran, Airbus (Skywise), and Boeing (AHM/AnalytX) embed prognostics into availability/PBH contracts. They also use proprietary health data and digital twins. Avionics, edge, and connectivity providers including Collins Aerospace, Honeywell, and Thales provide high-quality telemetry through aircraft interface devices and secure offload to cloud backends. Execution relies on airline Tech Ops platforms, including Lufthansa Technik’s AVIATAR, IFS Maintenix, Swiss-AS AMOS, Ramco, and Trax, where predictions turn into workcards, kits, and shop slots. Independent AI and analytics companies, such as Uptake, connect to this system, while PART 145 shops and component OEMs contribute specific models for engines, APUs, landing gear, brakes, and environmental systems.

At the same time, compliance, data sovereignty, and cybersecurity needs are driving vendors toward open, audited interfaces and electronic records and tech logs. Hybrid architectures that combine edge and cloud are common to reduce latency and bandwidth. North America leads in commercialization due to carrier scale and early edge deployments; Europe benefits from strong OEM and MRO ecosystems; Asia Pacific is growing rapidly through flagship airline launches. The overall result is that OEM-integrated offerings capture most of the revenue. Multi-tenant SaaS is growing the fastest from a smaller base.

LIST OF KEY PREDICTIVE AIRPLANE MAINTENANCE COMPANIES PROFILED

- Airbus (France)

- Boeing (U.S.)

- GE Aerospace (U.S.)

- Rolls-Royce (U.K.)

- Pratt & Whitney (U.S.)

- Safran (France)

- Honeywell Aerospace (U.S.)

- Collins Aerospace (U.S.)

- Lufthansa Technik (Germany)

- Lufthansa Technik (AVIATAR) (Germany)

- Swiss-AS (AMOS) (Switzerland)

- IFS (Maintenix) (Sweden/Canada)

- Ramco Systems (India)

- TRAX (U.S.)

- Uptake (U.S.)

- Thales (France)

- MTU Aero Engines (Germany)

KEY INDUSTRY DEVELOPMENTS

- In July 2025, Air Transat adopts Lufthansa Technik’s Digital Tech Ops Ecosystem (incl. AVIATAR). The Canadian carrier is rolling out AVIATAR across its A321/A330 fleet to standardize analytics, records, and predictive applications. Lufthansa Technik positions the move as a whole-fleet shift to an integrated digital Tech Ops stack.

- In January 2025, FAA issues AC 120-78B (e-signatures, e-recordkeeping, e-manuals). The advisory circular sets an acceptable means of compliance for digital maintenance records and signatures under 14 CFR, removing paper bottlenecks that slow predictive execution.

- In July 2024, Rolls-Royce TotalCare agreement with Vietjet (40 Trent 7000 engines). The services package embeds health monitoring and predictive support for Vietjet’s A330neo fleet. It complements existing TotalCare coverage on Vietjet’s Trent 700-powered A330ceo aircraft.

- In November 2024, GE Aerospace, Microsoft & Accenture unveil gen-AI maintenance-records solution. The tool is designed to let airlines and lessors retrieve and normalize maintenance records in minutes, accelerating technical records and asset management.

- In April 2023, American Airlines to install 500+ Collins InteliSight AIDs. The project equips a large portion of AA’s fleet with aircraft interface devices to capture and securely offload operational/maintenance data. Collins’ InteliSight and GlobalConnect provide the edge-to-cloud backbone feeding reliability and predictive workflows.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 17.1% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Aircraft Type · Fixed Wing · Rotary Wing · UAVs & Urban Air Mobility |

|

By Fleet Age · Mid-Life (6–12 yrs) · Young (0–5 yrs) · Mature (13+ yrs) |

|

|

By System Monitored · Airframe & Structures · Engines & APU · Landing Gear & Brakes · Avionics · Electrical Power · Environmental/Pressurization |

|

|

By Product Offerings · Analytics Platforms (SaaS) & Apps · Digital Twins & Physics/Hybrid Models · Edge Hardware & Embedded Health Systems · Integrated OEM Offerings · Data Integration & Exchange · Managed Services (Data Science/MLOps/Change Management) |

|

|

By Deployment Model · Multi-Tenant SaaS · Hybrid (Cloud + Edge) · Single-Tenant Cloud · On-Premise |

|

|

By Solution · RUL Prediction (components) · Spare Parts Forecasting · Fault Detection & Isolation · Maintenance Slot Optimization · Reliability-Centered Analytics · Fuel/Performance Optimization |

|

|

By End User · Low-Cost Carriers (LCCs) · Cargo Operators · Independent MROs · Network/Legacy Airlines · OEM Aftersales · Business Aviation Operators |

|

|

By Region · North America (By Aircraft Type, By Fleet Age, By System Monitored, By Product Offerings, By Deployment Model, By Solution, End User, and By Country) o U.S. (By Aircraft Type) o Canada (By Aircraft Type) · Europe (By Aircraft Type, By Fleet Age, By System Monitored, By Product Offerings, By Deployment Model, By Solution, End User, and By Country) o U.K. (By Aircraft Type) o Germany (By Aircraft Type) o France (By Aircraft Type) o Russia (By Aircraft Type) o Rest of Europe (By Aircraft Type) · Asia-Pacific (By Aircraft Type, By Fleet Age, By System Monitored, By Product Offerings, By Deployment Model, By Solution, End User, and By Country) o China (By Aircraft Type) o India (By Aircraft Type) o Japan (By Aircraft Type) o Singapore (By Aircraft Type) o Rest of Asia-Pacific (By Aircraft Type) · Rest of the World (By Aircraft Type, By Fleet Age, By System Monitored, By Product Offerings, By Deployment Model, By Solution, End User, and By Country) o Middle East & Africa (By Aircraft Type) o Latin America (By Aircraft Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.35 billion in 2026 and is projected to reach USD 18.87 billion by 2034.

In 2025, the market value stood at USD 1.65 billion.

The market is expected to exhibit a CAGR of 17.1% during the forecast period of 2026-2034.

The fixed wing segment led the market by aircraft type.

Outcome-based uptime deals and airline adoption of OEM predictive platforms are accelerating market growth.

Airbus (France), Boeing (U.S.), GE Aerospace (U.S.), Rolls-Royce (U.K.), Pratt & Whitney (U.S.), Safran (France), Honeywell Aerospace (U.S.), Collins Aerospace (U.S.), Lufthansa Technik (Germany), Lufthansa Technik (Germany), and among others are the top companies in the Predictive Airplane Maintenance market.

North America dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 222

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us