Canned Wines Market Size, Share & Industry Analysis, By Product Type (Sparkling, Fortified and Others), By Alcohol Content (Low ABV (Below 5%), Medium ABV (5–10%), and High ABV (Above 10%), By Distribution Channel (Hypermarket & Supermarket, On-Trade, and Online), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

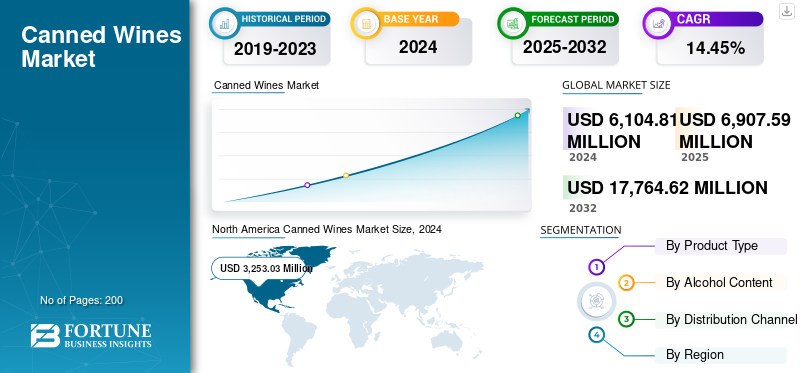

The global canned wines market size was valued at USD 6.91 billion in 2025. The market is projected to grow from USD 7.9 billion in 2026 to USD 23.62 billion by 2034, exhibiting a CAGR of 14.68% during the forecast period. North America dominated the canned wines market with a market share of 53.03% in 2025.

Canned wine represents an emerging segment within the global wine industry, offering a modern alternative to traditional bottled wine. Packaged in lightweight, portable, and recyclable aluminum cans, it meets the growing consumer preference for on-the-go, sustainable, and convenient beverage solutions. This innovation addresses key market shifts toward eco-conscious consumption, urban mobility, and premium ready-to-drink (RTD) beverages.

The industry is dominated by key players such as E. & J. Gallo Winery, Union Wine Company, Treasury Wine Estates Ltd., Constellation Brands, Inc., The Family Coppola, and others. The global canned wine market is highly competitive, featuring established wine producers and new entrants leveraging design, innovation, and marketing strategies to capture consumer attention.

Download Free sample to learn more about this report.

Canned Wines Market Key Takeaways

- 2025 Market Size: USD 6.91 billion

- 2026 Market Size: USD 7.90 billion

- 2034 Forecast Market Size: USD 23.62 billion

- CAGR: 14.68% from 2026–2034

- North America dominated the canned wines market with a 53.03% share in 2025.

- The sparkling wines segment is expected to account for 66.41% market share in 2026.

- The medium ABV (5–10%) segment is projected to hold 46.32% share in 2026.

North America

North America held a 53.03% share in 2025, valued at USD 3.67 billion.

Asia Pacific

Asia Pacific contributed 11.26% share in 2025, valued at USD 0.76 billion.

Europe

Europe accounted for 31.89% share in 2025, valued at USD 2.21 billion.

U.S.

The U.S. market is projected to reach USD 3.17 billion by 2026, driven by rising demand for premium RTD and sustainable beverage formats.

Japan

The Japan market is projected to reach USD 0.13 billion by 2026, supported by increasing demand for convenient and low-alcohol canned beverages.

Read More

MARKET DYNAMICS

Market Drivers

Increasing Female and Millennial Preference for Wine Consumption to Drive Market Growth

The canned wines industry has witnessed significant adoption among female consumers and millennial wine drinkers, who often favor lighter, more accessible, and design-oriented beverage options. The format’s portability, sustainability, and approachable branding align well with this demographic’s lifestyle preferences. According to the Pennsylvania State University, in 2023, 62% of U.S. consumers aged 18 and older had "occasion to use alcoholic beverages such as liquor, wine, or beer."

Urban living encourages informal gatherings and on-the-go consumption, further boosting the market potential for canned beverages.

Market Restraints

Regulatory Restrictions and Premium Product Pricing to Impede Market Growth

Despite growing acceptance, the canned wine market faces limitations due to stringent alcohol regulations, import duties, and varying labeling laws across countries. Many markets, including parts of Asia and the Middle East, impose restrictions on alcoholic product distribution, which hampers sales. Furthermore, premium canned wines often cost more per serving compared to bottled wines, due to small-batch production and packaging investments.

- According to the Organization for Economic Co-operation and Development (OECD), wine tax rates range from USD 0 to more than USD 6 per liter in the U.S, whereas the highest rate, including USD 1,197.66 per hectoliter of sparkling wine, is imposed by Turkey. Most countries, which apply various rates, charge higher rates for sparkling wines than for non-sparkling wines.

Market Opportunities

Rising Air Traffic to Unlock New Growth Opportunities

Canned wines are gaining traction in hotels, airlines, stadiums, and event catering, where portability and portion control are vital. Airlines and rail operators increasingly prefer canned formats to minimize spillage, reduce weight, and simplify service operations.

- According to the International Air Transport Association (IATA), global passenger traffic grew by 10.4% in 2024, surpassing 2019 levels by 2.8%, indicating strong growth potential for onboard catering beverages such as canned wine.

Similarly, event organizers, outdoor venues, and cruise operators are incorporating canned wines into their menus due to their space efficiency and single-use convenience.

Canned Wines Market Trends

Innovation in Low- and No-Alcohol Canned Wines to Shape the Industry

The growing global shift toward “mindful drinking”, social media, and health-conscious lifestyles offers a major opportunity for producers to develop low-alcohol and non-alcoholic canned wines. Consumers, especially millennials and Gen Z, are reducing alcohol intake but still seek sophisticated and social drinking experiences. Canned wines with an ABV below 5% appeal to those who prefer flavor-rich, calorie-conscious alternatives to beer or cocktails. Major players are investing in low-alcohol spritzers and fruit-infused options to cater to this segment.

- For instance, in March 2025, Boutinot, a major company specializing in the production and distribution of high-quality wines, launched a new low-alcohol canned wine range called Tuttavia. The Tuttavia range includes three Moscatos, a Rosato, and an orange spritz, targeting younger consumers who are moderating their alcohol intake and seeking lighter alternatives.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product Type

Convenience and Portability Lead the Sparkling Wine Segment’s Growth

On the basis of product type, the market is segmented into sparkling, fortified, and others.

The sparkling wines segment will accounting for the largest revenue share of 66.41% in 2026. These wines are preferred for their refreshing profile, celebratory appeal, and wide availability across both retail and on-trade channels. Moreover, canned sparkling wines are single-serve and portable, making them perfect for on-the-go consumption, outdoor activities, picnics, and casual social occasions.

The fortified segment is expected to grow significantly during the forecast period with a CAGR of 15.11% from 2026 to 2034.

By Alcohol Content

Balanced Alcohol Content Appeal and Health and Moderation Trends Lead the Medium ABV (5-10%) Segment Growth

On the basis of alcohol content, the market is segmented into low ABV (Below 5%), medium ABV (5–10%), and high ABV (Above 10%).

The medium ABV (5–10%) segment will lead with the largest share of 46.32% in 2026, reflecting consumer preference for a balanced taste and seasonable consumption. Medium ABV wines provide a balanced drinking experience, appealing to both casual drinkers and those seeking moderation without sacrificing flavor and enjoyment. Moreover, rising health consciousness encourages consumers to prefer moderate alcohol consumption, and medium ABV canned wines fit well into this lifestyle by allowing controlled servings without opening a whole bottle.

The low ABV (Below 5%) segment is expected to grow significantly, with a compound annual growth rate (CAGR) of 14.93% during the forecast period.

By Distribution Channel

Widespread Distribution Network Fuels Hypermarkets & Supermarkets Segment Expansion

On the basis of distribution channel, the market is segmented into hypermarket & supermarket, on-trade, and online.

To know how our report can help streamline your business, Speak to Analyst

The hypermarkets & supermarkets segment will accounting for 72.50% of the share in 2026. This dominance is supported by strong brand visibility and impulse buying patterns. Hypermarkets and supermarkets provide the most extensive physical retail presence, allowing canned wine brands to reach a large and diverse consumer base easily. Their broad footprint offers widespread availability and visibility, which is crucial for market penetration and encouraging consumer trials.

The online retail segment is anticipated to grow at a CAGR of 16.01% during the forecast period.

Canned Wines Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

North America Canned Wines Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America

The North America region captured 53.03% of the global market in 2025, generating USD 3.67 Billion in revenue, and is projected to reach USD 4.19 Billion in 2026, led by the U.S., where canned wine has evolved from a niche product to a mainstream option. Consumer inclination toward sustainable, on-the-go formats and premium RTDs continues to drive global canned wines market growth. Major players such as E.&J. Gallo Winery and The Wine Group lead the market through innovation and marketing strategies targeting younger audiences. The U.S. market is projected to reach USD 3.17 billion by 2026.

Europe

Europe remains a mature yet innovative market, with strong adoption in the U.K., France, and Germany. Increasing eco-consciousness and a shift toward lightweight packaging are influencing purchasing decisions. Europe maintained a strong presence in the global market, reaching USD 2.21 Billion in 2025, accounting for 31.89% share, and is expected to reach USD 2.52 Billion in 2026. The UK market is projected to reach USD 0.62 billion by 2026, while the Germany market is projected to reach USD 0.42 billion by 2026.

Asia Pacific

In 2025, Asia Pacific generated USD 0.76 Billion, contributing 11.26% to global market revenue, and is projected to grow to USD 0.89 Billion in 2026. The Asia Pacific region is the fastest-growing region in the canned wines market, driven by rising population and urbanization, growing western influence, increasing disposable incomes, and a younger demographic that favors convenient and portable beverage options. Countries such as China and India are key contributors, supported by favorable government norms and expanding retail and distribution networks. The Japan market is projected to reach USD 0.13 billion by 2026, while the China market is projected to reach USD 0.37 billion by 2026, and the India market is projected to reach USD 0.1 billion by 2026.

South America

The South America market was valued at USD .21 Billion in 2025, capturing 3.11% of global revenue, and is estimated to reach USD .25 Billion in 2026. Countries such as Brazil and Argentina are witnessing increasing demand for convenient and affordable alcoholic beverages, especially among younger consumers.

Middle East and Africa

Middle East & Africa recorded a market size of USD 0.05 Billion in 2025, capturing 0.71% of the global market share, and is projected to reach USD 0.06 Billion in 2026. The market for canned wines in the Middle East and Africa is experiencing rising interest in low-alcohol and non-alcoholic canned wines, coupled with premium imports in Gulf Cooperation Council (GCC) countries.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players’ Strong Focus on Product Innovation and Packaging to Reduce Environmental Impact

The global canned wine market is moderately consolidated, with both established beverage conglomerates and niche startups actively expanding through partnerships, acquisitions, and eco-friendly product offerings. Major players focus on expanding flavor portfolios, improving aluminum recycling, and creating appealing designs that emphasize sustainability and lifestyle appeal.

- For instance, in September 2025, Familia Torres, in partnership with its Dutch importer Walraven Sax, launched a circular wine bottle and keg system in the Netherlands, marking a pioneering step in sustainable wine packaging. The circular system also includes reusable stainless steel kegs, further reducing packaging materials and environmental impact.

Key Players in the Canned Wines Market

|

Rank |

Company Name |

|

1 |

E. & J. Gallo Winery |

|

2 |

Union Wine Company |

|

3 |

Treasury Wine Estates Ltd |

|

4 |

Constellation Brands, Inc. |

|

5 |

The Family Coppola |

List of Key Canned Wines Companies Profiled

- &J. Gallo Winery (U.S.)

- Canned Wine Co. (U.K.)

- Treasury Wine Estates (Australia)

- Constellation Brands Inc. (U.S.)

- Integrated Beverage Group (U.S.)

- Union Wine Company (U.S.)

- Francis Ford Coppola Winery (U.S.)

- Anheuser-Busch InBev (Belgium)

- Barefoot Cellars (U.S.)

- Sula Vineyards (India)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Eisberg, an alcohol free wine brand, launched a new non-alcoholic canned wine range called Be Free, featuring 200ml ready-to-drink cans in two expressions: sparkling white and sparkling rosé. This range is designed specifically to appeal to a younger generation of consumers who value moderation, convenience, and freedom of choice.

- September 2025: Archer Roose Wines partnered with Princess Cruises to launch the first official canned wine fleetwide. The partnership features four varietals on offer: Bubbly, Pinot Noir, Rosé, and Sauvignon Blanc. These wines can be enjoyed in various settings on the ships, such as poolside, during excursions, in casinos, through the Ocean Now app, in-room delivery, at Princess Cay, and at Alaska lodges.

- August 2025: Casillero del Diablo expanded its presence in the U.K. by launching canned wines, specifically the Cabernet Sauvignon Reserva and Sauvignon Blanc Reserva, in 187ml format. These canned wines are now available in 1,000 Tesco Express stores nationwide, marking a strategic move to meet changing consumer preferences for convenience and portability in the wine category.

- June 2024: Asda Stores Limited (ASDA), a British supermarket and petrol station chain, launched its first-ever range of canned wines called "Pica Pica," which includes six varieties: two white wines, two rosé wines, and two sparkling wines.

- February 2020: Sula Vineyards launched India's first canned wine called "Dia Sparkler," available in both red and white wine flavors in 330 ml cans. This launch made Sula the first Indian winery to enter the canned wine segment.

REPORT COVERAGE

The global canned wines market industry report analyzes the market in depth and highlights crucial aspects such as global canned wines market trends, secondary research market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global canned wines market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.68% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type

|

|

By Alcohol Content · Low ABV (Below 5%) · Medium ABV (5–10%) · High ABV (Above 10%) |

|

|

By Distribution Channel · Hypermarket & Supermarket · On-Trade · Online |

|

|

By Region · North America (By Product Type, Alcohol Content, Distribution Channel, and Country) • U.S. (By Product Type) • Canada (By Product Type) • Mexico (By Product Type) · Europe (By Product Type, Alcohol Content, Distribution Channel, and Country) • Germany (By Product Type) • Spain (By Product Type) • Italy (By Product Type) • France (By Product Type) • U.K. (By Product Type) • Rest of Europe (By Product Type) · Asia Pacific (By Product Type, Alcohol Content, Distribution Channel, and Country) • China (By Product Type) • Japan (By Product Type) • India (By Product Type) • Australia (By Product Type) • Rest of Asia Pacific (By Product Type) · South America (By Product Type, Alcohol Content, Distribution Channel, and Country) • Brazil (By Product Type) • Argentina (By Product Type) • Rest of South America (By Product Type) · Middle East & Africa (By Product Type, Alcohol Content, Distribution Channel, and Country) • South Africa (By Product Type) • Turkey (By Product Type) • Rest of the MEA (By Product Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market was valued at USD 6.91 billion in 2025 and is anticipated to reach USD 23.62 billion by 2034.

At a CAGR of 14.68%, the global market will exhibit steady growth over the forecast period.

By product type, the sparkling segment leads the market.

North America holds the largest market share in 2025.

Increasing female and millennial preference for wine consumption drives market growth.

E. & J. Gallo Winery, Union Wine Company, Treasury Wine Estates Ltd., Constellation Brands, Inc., and The Family Coppola are the leading companies in the market.

Innovation in low- and no-alcohol canned wines is the key market trend.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us