Beer Market Size, Share & Industry Analysis, By Type (Lager, Ale, Stouts, and Others), By Packaging (Glass Bottle and Metal Can), By Distribution Channel (On-trade and Off-trade), By Production (Macro brewery and Microbrewery), By Category (Standard and Premium), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

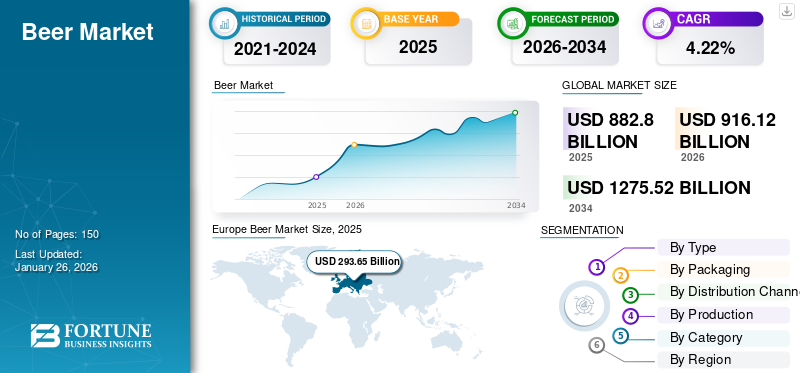

Beer Market Size and Future Outlook

The global beer market size was valued at USD 882.80 billion in 2025 and is projected to grow from USD 916.12 billion in 2026 to USD 1,275.52 billion by 2034, exhibiting a CAGR of 4.22% during the forecast period. Europe dominated the beer market with a market share of 33.26% in 2025. Moreover, the beer market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 149.12 billion by 2032, driven by increasing demand for hard drinks among millennials and working population.

Beer is one of the most beloved drinks across the globe as compared to any other alcoholic beverages and is gaining immense popularity, especially amongst the millennials and Gen Z, owing to its various formulations, varieties, and flavor offerings. Earlier, flavored brewed beverage was majorly consumed in regions, such as Europe and North America, but in recent times, its demand across the world has grown exponentially. This factor has positively affected the overall business. The emergence of new brewing technologies in developing economies has also positively impacted the customers’ consumption pattern. Furthermore, consumers are looking for innovative alcoholic drinks that come in different flavors, which is augmenting the global beer market growth.

The COVID-19 pandemic and associated government restrictions related to people’s mobility significantly affected the alcohol consumption patterns and places of consumption. According to The Brewers of Europe, COVID-19 measures taken by governments in 2020 had a disproportionate impact on bars and restaurants, reducing 42% of beer sales in Europe. It also weakened the positive contribution of beer value chain to the region’s economy. Some brewers also faced legislative challenges including a complete ban on the sale of alcohol in India and South Africa, and a ban on home brewing in Mexico. According to the Beer Institute, the U.S. saw a drop of nearly USD 20 billion in retail sales of this drink. Alcohol sales in bars and restaurants also plummeted, severely hitting the industry. Whereas, off-market sales, such as those of e-commerce and retail stores rose significantly. These stores are anticipated to help the market regain its usual pace in the forthcoming years.

Download Free sample to learn more about this report.

BEER MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 882.80 billion

- 2026 Market Size: USD 916.12 billion

- 2034 Forecast Market Size: USD 1,275.52 billion

- CAGR: 4.22% from 2026–2034

- Europe dominated the beer market with a market share of 33.26% in 2025.

- Based on type, the market is contributing 76.87% in 2026

- The off-trade segment is expected to lead the market, contributing 56.71% share in 2026.

North America

The North America market generated USD 172.91 billion in 2025, representing 19.59% of the global market landscape, and is expected to reach USD 181.94 billion in 2026.

Europe

Europe contributed 33.26% to the global market in 2025, with a valuation of USD 293.65 billion, and is projected to reach USD 302.45 billion in 2026.

Asia Pacific

Asia Pacific accounted for USD 237.45 billion in 2025, representing 26.90% of the global market share, and is projected to reach USD 246.28 billion in 2026.

U.S.

The U.S. market is projected to reach USD 120.58 billion by 2026.

Japan

The Japan market is projected to reach USD 18.99 billion by 2026.

Read More

Beer Market Trends

Rising Alcohol-based E-commerce Channels is a Key Trend

The COVID-19 pandemic promoted the value of mainstream e-commerce channels. Beer has usually been under-traded online as these channels offer low margins. However, this is predicted to change as consumers continue to buy more groceries online, and beer cart is becoming a part of their shopping list. In particular, the Direct-to-Consumer (DTC) channel expanded rapidly in this industry in 2021. It not only allowed many small breweries to continue operating during the pandemic, but also ensured that they thrived in the future. In response to this trend, 12 leading spirits, and wine companies formed the International Alliance for Responsible Drinking (IARD). Around 14 leading global and regional online retailers and e-commerce distribution platforms have come together in this initiative to safeguard and ensure strong standards throughout the alcohol supply chain. Online sales of this non-alcoholic beverage have captured the largest market share in countries such as Japan, the U.K., and the U.S. From a low base, online sales of such products will grow rapidly, which will help the market share to grow in future.

Download Free sample to learn more about this report.

Beer Market Growth Factors

Improving Disposable Income and Rising Westernization to Trigger Consumption

The improving economic conditions and growing Gross Domestic Product (GDP) of developing regions, such as Asia Pacific and South America, have resulted in improved per capita disposable incomes of consumers. This rise in the disposable income of consumers is an important factor contributing to the growth of the alcoholic beverage industry. According to a leading Japanese beverage company Kirin Holdings Co., global beer consumption in 2021 increased for the first time during the COVID-19 recovery period. The market growth was majorly supported by strong demand in China and Asia as they experienced strong economic growth. Global consumption increased by 4% to 185.60 million kiloliters owing to reduced impact of the COVID-19 pandemic. In recent years, craft beer has been gaining traction in the Asian market, including China, India and Japan, owing to its quality, taste, and flavors and stakeholders have continued to expand their business operations. According to Brewers Association, the active craft brewery number has increased from 9,119 in 2022 to 9,336 in 2023 in the U.S. Therefore, factors such as growing GDP, rising influence of craft beers in Asian countries, and increasing number of craft breweries across the globe are anticipated to push the global beer market growth.

Increasing Prevalence of Alcohol Socialization among Consumers to Aid Market Growth

Historically, alcohol plays an important role in social engagements. The trend is still growing along with the demand for bold flavored drinks in the market. Beer is one of the most famous alcoholic beverages, which is gaining huge popularity among youngsters and millennials owing to its low ABV (Alcohol by Volume) and refreshing appeal to consumers. Since low ABV, low calorie, and lower carb beer becoming popular worldwide, companies are introducing new products to serve their clientele base. For instance, in March 2023, Heineken, one of the leading beverage companies, launched Heineken® Silver with low-carb, low-calorie labels in the U.S. market. The growing diversification of cultural groups of consumers and their social status are some of the major factors promoting the growth of the market.

RESTRAINING FACTORS

Restricted Provincial Acts for Marketing and Advertising of Alcoholic Beverages in Several Regions to Hamper Market Growth

The global alcohol market has long been facing the obstacle of marketing and advertising of alcoholic beverages to support and reinforce the concept of healthy living among consumers. Governments of major economies, such as India, China, the U.K., and others, have banned the promotion of alcohol-based beverages. The restricted provincial acts for its marketing can hinder the growth of the overall market in the upcoming years. However, manufacturers are promoting their products by using surrogate advertising, which is used to promote alcohol and other banned products in the disguise of another product in the market.

Beer Market Segmentation Analysis

By Type Analysis

Lager Segment to Dominate Market with Growing Consumer Inclination Toward Premium Drinks

Based on type, the market is segmented into lager, ale, stouts, and others. Out of all, lager is inarguably the most famous type of beer segment is expected to lead the market, contributing 76.87% in 2026, due to its novel brewing process, which offers a refreshing and crisp appeal to consumers. It is bottom-fermented and brewed with 5 to 11% of ABV at a lesser temperature - typically between 7 and 13°C, which enhances the drinking experience for consumers. The growing trend of premium beverages among consumers led to increased consumption of premium lagers in the market. The varying consumer preferences, improving living standards, and rising modernization are rapidly propelling the demand for premium category, which is likely to promote lager consumption in the global marketplace.

Ales are produced through top-fermentation, a process in which yeast ferments at a warmer temperature and then settles at the top of the drink. Ale is quite common among craft brewers as ale yeast can create beer in just 7 days, making it more convenient for small breweries that do not have enough space for fermentation tanks to make lager frequently. In addition, the rising inclination of youngsters and millennials toward low alcohol based beverages is likely to boost the demand for ales and stouts in the future.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel Analysis

Off-trade Distribution Channel to Hold Major Market Share Owing to its Low-Price Products

Based on distribution channel, the market is distributed into on-trade and off-trade. The off-trade segment is expected to lead the market, contributing 56.71% share in 2026, as it is one of the most efficient sales channels to sell brewed drinks across the globe. Consumers in several economies are price conscious and do not spend money to drink liquor in pubs, bars, and other on-trade platforms. The off-trade channel consists of supermarkets, wine shops, specialty stores, and others which offer products at a low cost as compared to on-trade channels. According to The Brewers of Europe, during the pandemic, Europe saw an 8% increase (20 million hectoliters) in off-trade sales. Nowadays, increasing adoption of different types of alcohol drinking practices in countries has enhanced the popularity of dine-out trends among consumers.

On the other hand, consumers in developed economies prefer to be entertained while consuming quick serving alcohol; this is proliferating on-trade consumption across the world. Although, after the pandemic, the on-trade channel was negatively impacted, it could experience significant improvement as restrictions are lifted in several countries.

By Production Analysis

Macro Brewery Production Segment to Lead Due to its Easy Product Availability

Based on production, the market is segmented into microbrewery and macro brewery. Macro brewery segment is projected to lead the market with a 66.48% share in 2026 and is recognized as one of the most effective production methods to fulfill consumer demands. Rising number of alcohol consumers is intensifying the need for market players to develop new flavored alcohol, which will help in captivating a large consumer base. Nowadays, millennials are one of the largest demographics in the global population, and thus their growing inclination toward trying new products has resulted in breweries to adopt and incorporate newer flavors and ingredients in their offerings.

Microbreweries have also gained considerable traction as they have made it possible for consumers to enjoy a wide variety of drinks by bringing minimal changes to their favorite restaurants. According to the Brewers Association, in 2021, the number of operating breweries in the U.S. climbed to 9,247 from 9,025 in 2020. The number includes 1,886 microbreweries, 3,307 brewpubs, 3,702 taproom breweries, and 223 regional craft breweries. Moreover, the microbrewery business is keeping in touch with the tradition along with adding newness to their production processes, which has motivated foodservice restaurants to experiment with the latest flavors using their creativity.

By Category Analysis

Premium Category to be the Most Prominent Segment Owing to High Quality Product Offerings

Based on category, the market is distributed into standard and premium. The premium segment holds a major share in the market and is anticipated to dominate this industry during the forecast period. These are primarily made up of high-quality grains, which are highly priced. The surging demand for premium quality products in developing countries is one of the crucial factors augmenting the segment’s growth. Owing to the rising purchasing power of the middle-class population, there is a strong demand for high-quality brewed drinks as individuals seek more innovative products in the food & beverage sector. According to Budweiser Brewing Company, 70% of the total beer consumption will be of premium or super-premium brands by 2025. Moreover, premium alcohol has become one of the most liked seltzers among younger people, particularly due to its health advantages over mass-produced beverages as well as the availability of novel varieties.

The standard segment also accounts for an appreciable market share due to its affordability as compared to premium products. In addition, standard beverages have limited alcohol content of around 5%, which, in turn, minimizes the intake of alcohol.

By Packaging Analysis

Glass Bottle to be Widely Used for Packaging Due to Its Rapid-Cooling Property

Based on packaging, the market is segmented into glass bottle and metal can. Glass bottle segment is projected to lead the market with a 50.01% share, the most popular packaging used to pack a variety of alcohol, owing to its low processing cost. Manufacturers also believe that drinking alcoholic beverages from a glass bottle gives a more premium appeal to consumers compared to a metal can. A beer bottle made of glass is reliable, sustainable, 100% recyclable, and reusable. The glass bottle can also cool the liquor rapidly, thereby enhancing customers’ drinking experience. These inherent characteristics are the reasons for the continued demand for glass bottles and their renewed popularity in certain industries and regions across the world.

Consumers in developed countries, such as the U.S., the U.K., Canada, and others, are inclining toward canned drinks owing to its beneficial preservation properties such as effective & convenient container for holding and limiting the liquor’s exposure to flavor-damaging UV (Ultra-Violet) rays. Thus, it is assumed that the shelf life of the beverage is preserved more when packed in cans as compared to bottles.

REGIONAL INSIGHTS

Europe to Witness Significant Growth Due to Rising Consumption of Alcoholic Drinks

Europe

Europe Beer Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe contributed 33.26% to the global market in 2025, with a valuation of USD 293.65 billion, and is projected to reach USD 302.45 billion in 2026. Hard drinks play an important role in all European countries and is an integral part of the region’s culture, heritage, and nutrition. The European Union is one of the main beer producing regions in the world. According to the Brewers of Europe, the consumption of beer in Europe in 2021 stood at 342,212 thousand hectoliters, which showed minimal increment of 0.25% from the past year. In terms of structure, the European alcohol industry is a diverse industry, which is mainly made up of small and medium-sized companies including microbreweries and breweries operating at local, regional, or national levels. The UK market is projected to reach USD 27.9 billion by 2026, and the Germany market is projected to reach USD 58.39 billion by 2026.

It also includes major European breweries that are world leaders in their fields. The emergence of new micro and small breweries in the past few years is a significant sign of the industry's potential for innovation. The overall alcohol content and harmful use of alcohol in Europe have declined as some consumers are switching to low-alcohol products, and non-alcoholic varieties in this category. Thus, these consumer preferences are anticipated to support the growth of the European market.

Asia Pacific

Asia Pacific accounted for USD 237.45 billion in 2025, representing 26.90% of the global market share, and is projected to reach USD 246.28 billion in 2026. The region has a massive potential for liquor manufacturers and its production across the world. The regional market is led by countries, such as India, China, Australia, and others where consumers are increasing their alcohol consumption. According to the Anheuser-Busch InBev Company, the Asia Pacific region is the largest growing region in the beer industry and is estimated to account for 53% of the growth between 2014 and 2025. The refreshing flavor profiles and premium alcoholic appeal are some of the key factors boosting the acceptance of such beverages among consumers in their busy schedules. The consumers are accepting westernized patterns and favoring dine-out trends, which are proliferating the growth of on-trade channels in the region. The Japan market is projected to reach USD 18.99 billion by 2026, the China market is projected to reach USD 162.03 billion by 2026, and the India market is projected to reach USD 9.22 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

North America

The North America market generated USD 172.91 billion in 2025, representing 19.59% of the global market landscape, and is expected to reach USD 181.94 billion in 2026. The region has a variety of major market places in the world that show immense potential for the business to grow owing to the high consumer association with malt-based beverages and growing number of breweries. According to the Alcohol and Tobacco Tax and Trade Bureau (TTB), there were 9,500 reported brewery locations in the U.S. in 2022. Moreover, in 2021, the U.S. beer industry shipped approximately 208.6 million barrels across the globe as per the Alcohol and Tobacco Tax and Trade Bureau (TTB) and the U.S. Commerce Department. The growing popularity of hard drinks in the region is directly proportional to the increasing demand from millennials and young working population owing to their changing taste preferences. The evolving consumer preferences and growing demand for low ABV drinks are expected to trigger the consumption of ale in the coming years. The U.S. market is projected to reach USD 120.58 billion by 2026.

South America

South America is the fastest growing market owing to rapid urbanization and increasing disposable incomes in the region. Global companies, such as AB InBev, are also opting for customer-centric strategies by introducing innovative products in the market. For instance, in April 2022, Novo Brazil Brewing Company announced the opening of its new microbrewery in Imperial Beach in San Diego, Brazil. The firm aims to increase its production capacity by 30% by next year with the added production unit.

Middle East & Africa

In 2025, Middle East & Africa held 5.70% of the global market, reaching a valuation of USD 50.29 billion, and is projected to grow to USD 52.35 billion in 2026.

Latin America

Latin America contributed approximately USD 128.51 billion to the global market in 2025, accounting for 14.56% share, and is expected to reach USD 133.1 billion in 2026.

Key Industry Players

Global Market is Highly Consolidated Due to Strong Presence of Key Companies

Over the past few years, the wave of consolidation has transformed the global market, leading to new product launches and mergers & acquisitions between various multinational brewing companies. The increased focus on achieving production efficiency, ability to understand market needs & trends, and strong distribution networks are some of the major factors that the manufacturers are focusing on. Heineken N.V., China Resources Breweries, Carlsberg A/S, and Molson Coors Beverage Company are some of the other key players in the market.

List of Top Beer Companies:

- Anheuser-Busch InBev (Belgium)

- Heineken N.V. (Netherlands)

- China Resources Breweries (China)

- Carlsberg A/S (Denmark)

- Diageo Plc (U.K.)

- Molson Coors Beverage Company (U.S.)

- Boston Beer Company (U.S.)

- Asahi Group Holdings Ltd (Japan)

- Kirin Holdings Co. Ltd (Japan)

- Beijing Yanjing Beer Group Corporation (China)

KEY INDUSTRY DEVELOPMENTS

- April 2023 – BIRA 91 introduced two new limited – edition beers – the 022 Session Ale and 011 Gully Pilsner as well as customized merchandise paid homage to the Mumbai Indians and Delhi Capital cricket teams. The global beer industry witnessed increasing premiumization trends, with growing demand for craft beer, flavored beer, IPA variants, and premium imported brands across Europe, North America, and Asia-Pacific.

- November 2022 – Kenya Breweries Limited launched a new fruit flavored beer called “Rockshire Tropical Lager.” This new product is said to be infused with natural tropical African fruit flavors, such as pineapple and passion fruit, and claims to have an ABV of around 4.2%.

- April 2022 – Indian company BIRA 91 announced the launch of “Imagined in India.” This included the release of four new limited release beers such as Kokum Sour, Bollywood IPA, Mango Lassi, and Brown Ale. These new launches helped the company expand its product ranges and strengthen its market image across the globe.

- September 2022 – United Breweries introduced a new variant of beer brands, “Heineken Silver”. This product is the brand’s latest addition to the new premium segment of the company.

- July 2021 - Heineken NV, a Dutch multinational brewing company, announced that following the Annual General Meeting of United Breweries Limited (UBL), it has acquired control of UBL in India.

REPORT COVERAGE

The report provides qualitative and quantitative insights into the industry. It also offers a detailed analysis of its utility, distribution channels, availability of raw materials, types, their market size, and growth rate for all possible segments in the market. Along with this, the report provides an elaborative analysis of the market dynamics and competitive landscape. Various key insights presented in the report are an overview of related markets, recent industry developments such as mergers & acquisitions, regulatory scenario in critical countries, and key industry trends.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.22% over 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Type

By Packaging

By Distribution Channel

By Production

By Category

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 916.12 billion in 2026 and is projected to reach USD 1,275.52 billion by 2034.

Expanding at a CAGR of 4.22%, the market will exhibit steady growth during the forecast period (2026-2034).

The lager segment is expected to be the leading segment in the market based on type during the forecast period.

Increasing socialization among consumers and improving disposable income are the key factors driving the growth of the market.

Anheuser-Busch InBev, Heineken N.V., and Carlsberg A/S are few of the key players in this market.

Europe dominated the beer market with a market share of 33.26% in 2025.

The on-trade distribution channel is anticipated to grow at the fastest pace during the forecast period.

Rising alcohol-based e-commerce channels is a key market trend.

- 2021-2034

- 2025

- 2021-2024

- 150

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us