Cargo Vans Market Size, Share & Industry Analysis, By Vehicle Size (Small Cargo Vans, Mid-Size Cargo Vans, and Large Cargo Vans), By Propulsion (ICE and Electric), By Application (Last-Mile Delivery & E-commerce, Logistics & Freight Transport, Construction & Utilities, Cold Chain/Refrigerated Transport, and Others), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026-2034

Cargo Vans Market Size and Future Outlook

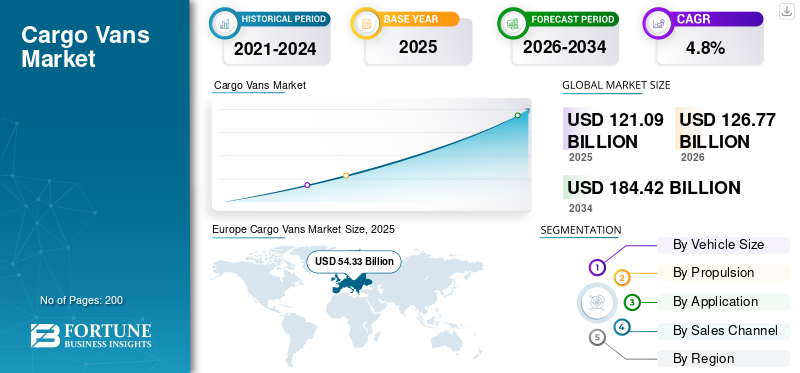

The global cargo vans market size was valued at USD 121.09 billion in 2025. The market is projected to grow from USD 126.77 billion in 2026 to USD 184.42 billion by 2034, exhibiting a CAGR of 4.8% during the forecast period. Europe dominated the cargo vans market with a market share of 44.86% in 2025.

The global market covers the worldwide demand for cargo-focused vehicles used to move goods in commercial settings, typically classified as a light commercial vehicle and purchased by businesses to support transport and service activity. Cargo vans sit at the center of modern commerce as they provide enclosed, secure space for transporting parcels, tools, and temperature-controlled goods across cities and regional corridors. The market spans both conventional and newer powertrains, including internal combustion models and the electric vehicle category, as fleets balance performance requirements with regulatory and sustainability goals.

Over the coming years, the industry will evolve around three practical forces such as the growth of e-commerce, tighter delivery windows, and city-level access constraints that reshape how goods move through dense areas. These shifts are directly connected to the rising demand for last mile delivery solutions, where cargo vans enable high-frequency delivery operations in urban logistics environments. At the same time, businesses are modernizing fleet management through telematics, route optimization, and predictive maintenance, turning vans into connected work assets supported by technological advancements.

Operational resilience is another growth lever. As global supply chains become more complex, shippers and service firms are expanding fleets to keep deliveries reliable, driving increasing demand for vehicles that can be deployed quickly and run cost effectively across different route profiles. Vehicle sizing also matters: mid-size vans often balance payload, parking practicality, and utilization efficiency, while some applications require heavier configurations for tons and above 3 tons payload classes, depending on local regulations and duty cycles.

During the forecast period, the vans market is expected to grow steadily, supported by electrification policies, operating-cost optimization, and expanding commercial delivery networks. Leading OEMs such as Mercedes Benz and Ford Motor company are broadening product lineups and digital services to capture fleet customers and improve uptime.

Download Free sample to learn more about this report.

CARGO VANS MARKET TRENDS

Connected Telematics and Data Platforms Transform Fleet Productivity

A defining trend is the expansion of connected vehicle services that improve utilization and uptime. Fleets are adopting cloud platforms to track energy use, driver behavior, maintenance schedules, and route performance in near real time. This strengthens fleet management, reduces unplanned downtime, and supports scaling without losing service quality. As technological advancements spread, connectivity becomes a purchase driver especially for operators managing large multi-city delivery networks.

- For instance, in September 2024, Ford Pro described updates to its software platform, highlighting fleet optimization capabilities built from large-scale connected vehicle data and tools designed to improve commercial uptime.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Expansion of E-Commerce and Incentives for Last Mile Delivery Solutions Accelerate Market Demand

The rapid growth of e-commerce is directly increasing parcel volumes across urban and semi-urban regions, creating structural expansion in commercial vehicle fleets. At the same time, various governments are introducing incentives for last mile delivery solutions, encouraging fleet modernization and cleaner vehicle adoption. These measures support the rising demand for last mile delivery solutions, pushing businesses to expand cargo van capacity. As delivery timelines shorten and route density increases, operators require reliable vehicles to manage high-frequency delivery operations, resulting in sustained increasing demand during the forecast period.

- For instance, in January 2024, ACEA reported EU van registrations rose to 1,586,688 units in 2024, reflecting sustained logistics activity and replacement demand across major markets.

MARKET RESTRAINTS

High Upfront Costs and Charging Readiness Slow Fleet Transition

A key restraint is the higher upfront cost of battery-electric cargo vans and the uneven readiness of depot and public charging for commercial operations. Fleets often need to invest in chargers, electrical upgrades, and new processes before scaling purchases. In regions with tight utilization, downtime risk matters more than fuel savings, slowing adoption. This is especially relevant where government incentives are limited or where infrastructure buildout lags fleet expansion needs.

- For instance, in April 2025, AP reported GM temporarily halted BrightDrop production in Canada due to weaker-than-expected demand and high inventory, showing adoption volatility in electric commercial vehicles.

MARKET OPPORTUNITIES

Commercial EV Credits and Policy Support Helps in Fleet Modernization

A major opportunity comes from policy support that reduces total ownership costs and speeds fleet procurement. Many markets are using government incentives and targeted commercial credits to accelerate adoption of clean commercial vehicles. These programs make electrified vans more affordable, helping fleets modernize while improving compliance and operating economics. Over time, incentives also attract investment into charging and service ecosystems, reinforcing cargo vans market growth during the forecast period.

- For instance, in February 2026, The IRS states qualified businesses may claim a Commercial Clean Vehicle Credit under IRC 45W, with credits up to USD 40,000 for eligible commercial vehicles.

MARKET CHALLENGES

Supply Chain Disruptions Keep Production and Deliveries Uncertain

A persistent challenge is fragility in supply chains, especially for semiconductors and electronics needed for modern vans and safety systems. Even when demand is healthy, manufacturers can face production bottlenecks that delay vehicle availability, create backlogs, and raise costs for fleet customers. This uncertainty complicates procurement planning for large fleets and can push operators to extend vehicle life instead of upgrading, slowing market momentum.

Segmentation Analysis

By Vehicle Size

Mid-size Vans Dominate as they Balance Payload and City Practicality

On the basis of vehicle size, the market is segmented into small cargo vans, mid-size cargo vans, and large cargo vans.

Mid-size vans lead as they deliver strong cargo volume, easy maneuvering, and high utilization in urban logistics. They fit mixed routes, dense centers and suburban drops, while remaining cost effectively operated for fleets and SMEs. Their flexible upfit options support tools, parcels, and temperature-controlled goods. In many markets, these platforms serve payload needs ranging from compact parcels to regulated tons and above 3 tons duty cycles.

- For instance, in March 2024, Stellantis showcased its renewed Pro One van lineup across multiple brands, reflecting how mid-size platforms remain core products for professional and fleet buyers.

The large cargo vans segment is expected to grow at a CAGR of 5.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion

ICE Dominates as it Remains Simplest and Lowest-risk Fleet Choice

On the basis of propulsion, the market is bifurcated into ICE and electric.

ICE cargo vans remain dominant as refueling networks are mature, acquisition costs are lower, and fleets can maintain high utilization without charging constraints. Many operators need predictable range, fast turnaround, and broad service coverage, which ICE models provide today. Even as electrification expands, ICE remains essential for long routes and smaller fleets that cannot yet invest in charging infrastructure.

- For instance, in January 2025, ACEA reported diesel vans reached 84.5% share in EU 2024 registrations, while electrically chargeable vans declined to 6.1%, confirming ICE dominance.

The electric segment is expected to grow at a CAGR of 14.1% over the forecast period.

By Application

Last-mile Delivery Dominates Due to Rising Parcel Density

On the basis of application, the market is segmented into last-mile delivery & e-commerce, logistics & freight transport, construction & utilities, cold chain/refrigerated transport, and others.

Last-mile delivery and e-commerce lead as parcel networks require frequent stops, tight schedules, and reliable access to urban zones. Cargo vans are the standard tool for this work, enabling high-frequency delivery operations tied to the rising demand for last mile delivery solutions. As online retail expands and delivery windows shrink, fleets add capacity and replace vehicles faster, reinforcing this segment’s dominance globally.

- For instance, in December 2025, Mercedes-Benz stated its Charleston plant built an all-electric eSprinter as the five-millionth Sprinter and handed it to FedEx, highlighting delivery fleet priorities.

The last-mile delivery & e-commerce segment is expected to grow at a CAGR of 6.1% over the forecast period.

By Sales Channel

OEM Dominates as Fleets Prefer Direct Purchasing and Support

On the basis of sales channel, the market is segmented into OEM and aftermarket.

OEM sales dominate as large fleets buy directly for consistent specifications, warranty coverage, and coordinated service support. Direct OEM relationships also help with financing, upfitting, and uptime programs, which matter when fleets scale quickly. As connectivity and service bundles expand, OEM channels gain further advantage by offering integrated vehicle-plus-software packages that reduce operational risk for commercial customers.

- For instance, in March 2025, Ford Pro linked electrified Transit models with Ford Pro software, charging, and service solutions, reinforcing why fleets prefer OEM-led packages over fragmented purchasing.

The OEM segment is expected to grow at a CAGR of 4.9% over the forecast period.

Cargo Vans Market Regional Outlook

By region, the global market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Europe

Europe Cargo Vans Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe held the dominant cargo vans market share in 2025, valuing at USD 54.33 billion, and also maintained the leading share in 2024, with USD 52.49 billion. Europe leads as cargo vans are the default work vehicle for many SMEs and delivery networks, supported by dense cities and mature professional van ecosystems. Strong commercial replacement cycles and broad product choice keep utilization high in urban logistics. Policy direction and government incentives also push fleet modernization and technology upgrades, sustaining leadership through the forecast period.

- For instance, in January 2025, ACEA confirmed EU new van sales reached 1,586,688 units in 2024, with growth across key markets, reinforcing Europe’s structural dominance in van demand.

Germany Cargo Vans Market

Germany’s market size in 2025 was recorded at around USD 12.10 billion, accounting for roughly 10.0% of global revenues.

U.K. Cargo Vans Market

The U.K. market size in 2025 was valued at around USD 8.75 billion, accounting for roughly 7.2% of global revenues.

Asia Pacific

Asia Pacific is estimated to reach USD 41.83 billion in 2026 and secure the position of the second-largest region in the market. The Asia Pacific region’s expansion is supported by industrial growth, rapid urbanization, and fast scaling of delivery ecosystems tied to the growth of e-commerce. Local manufacturing depth strengthens supply chains, while cities prioritize efficient movement of goods. Electrification rises where policy is strong and fleet consolidation improves charging feasibility, creating long-term momentum in commercial vans.

China Cargo Vans Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 25.00 billion, representing roughly 20.6% of the global market.

India Cargo Vans Market

The Indian market value in 2025 was valued at around USD 2.90 billion, accounting for roughly 2.4% of global revenues.

North America

North America is projected to record a growth rate of 4.9% in the coming years, and reach a valuation of USD 8.91 billion by 2026. North America grows through fleet renewal, productivity-focused digitization, and expanding parcel networks. Large operators increasingly standardize vans for route density and depot operations, supported by connected fleet management and electrification policies. The U.S. remains the primary engine, with major OEM and fleet programs shaping procurement. California’s regulation pathway also influences corporate planning and ZEV adoption timelines.

U.S. Cargo Vans Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was analytically approximated at around USD 6.60 billion in 2025, representing roughly 12.5% of the global market.

Rest of the World

Growth in the rest of the world is uneven but positive, driven by modernization of logistics and service fleets. Latin America witnesses gradual commercial fleet upgrades as e-commerce penetration expands and urban delivery networks mature. Cost sensitivity remains high, so affordability, durability, and service coverage shape demand more than premium features, although selective electrification pilots are increasing.

COMPETITIVE LANDSCAPE

Key Industry Players

Fleet-Centric Platforms and Electrification Shape Competitive Advantage in Market

Competition in the global market is led by manufacturers that can deliver high-volume platforms, reliable aftersales support, and strong ecosystem partnerships for commercial users. Winning strategies increasingly focus on total lifecycle value including connected services, uptime guarantees, and integrated charging or fuel solutions for fleets. Companies are also strengthening regional manufacturing footprints to reduce risk and improve responsiveness when commercial demand spikes.

Large OEMs are investing in modular vehicle architectures that support multiple body styles and payload needs, helping them serve both parcel delivery and specialist use cases (utilities, refrigerated transport, and service fleets). Product portfolios are expanding in both ICE and battery-electric ranges, but the competitive edge often comes from software and services such as bundled maintenance, predictive diagnostics, and platform-level integration with customer fleet systems. This pushes manufacturers to build end-to-end commercial offerings rather than only selling vehicles.

Commercial vehicle leaders also compete through partnerships with logistics operators, upfitters, and charging providers, allowing faster deployment for big fleets. Brand strength and trust are critical as fleet buyers prioritize durability, repair networks, and residual value. In parallel, companies keep improving productivity features, driver-assistance, connectivity, load-area design, and energy efficiency to differentiate in a crowded van segment.

- For instance, in March 2025, Ford Pro said it now offers electrified variants across the Transit family and began production of the all-new E-Transit Courier, expanding fleet-focused capability.

LIST OF KEY CARGO VANS COMPANIES PROFILED

- Mercedes-Benz Group (Germany)

- Ford Motor Company (U.S.)

- Stellantis (Netherlands)

- Renault Group (France)

- Volkswagen Commercial Vehicles (Germany)

- Toyota Motor Corporation (Japan)

- Nissan Motor Co. (Japan)

- General Motors (U.S.)

- Iveco Group (Italy)

- Hyundai Motor Company (South Korea)

KEY INDUSTRY DEVELOPMENTS

- February 2026: The IRS continued to publish guidance for the Commercial Clean Vehicle Credit under IRC 45W, supporting the economics of commercial EV adoption. This type of policy support influences OEM commercialization plans for electric vans.

- January 2026: PlusAI announced expansion of its partnership with IVECO for Southern Europe’s first Level 4 autonomous trucking deployment program. The announcement shows growing collaboration between OEMs and autonomy software providers.

- May 2025: Kia publicly introduced its PV5 and commercial vehicle strategy in the U.K., including plans for a specialist network supporting its PBV approach. This marks Kia’s structured entry into electric commercial vehicles in Europe.

- April 2025: Stellantis announced expanded production capacity for its Pro One commercial van range at key European manufacturing facilities to meet sustained demand from logistics and professional fleet customers. The move strengthens supply availability across Peugeot, Citroën, Opel, and Fiat Professional cargo van brands.

- March 2025: Ford Pro announced production expansion of the all-electric E-Transit Courier in Europe, targeting growing fleet demand for compact electric cargo vans used in last-mile delivery operations. The move supports Ford’s commercial electrification strategy.

- March 2025: Ford Pro emphasized integration of vans with software, charging, and service solutions designed to maximize uptime. This expands the “vehicle + ecosystem” model that fleets increase demand.

- January 2025: The U.S. Postal Service disclosed procurement steps toward electrification, including E-Transit vehicles and charging infrastructure planning. This created a large public-sector reference program for commercial EV deployment.

REPORT COVERAGE

The global cargo vans market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Vehicle Size, Propulsion, Application, Sales Channel, and Region |

| By Vehicle Size |

|

| By Propulsion |

|

| By Application |

|

| By Sales Channel |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 121.09 billion in 2025 and is projected to reach USD 184.42 billion by 2034.

In 2025, the market value stood at USD 54.33 billion.

The market is expected to exhibit a CAGR of 4.8% during the forecast period.

The mid-size cargo vans segment led the market by vehicle size.

The expansion of e-commerce and incentives for last mile delivery solution is driving the global market.

Mercedes-Benz Group, Ford Motor Company, Stellantis, and Renault Group are some of the top players in the market.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us