Van Market Size, Share & Industry Analysis, By Van Type (Compact Vans, Mid-size Vans, and Full-size Vans), By Vehicle Category (Passenger Vans and Cargo Vans), By Propulsion (ICE and Electric), By Application (E-commerce and Logistics, Construction & Infrastructure, Passenger Transport & Shuttle Services, Healthcare & Emergency Services, Mobile Workshops & Service Vans, and Municipal Services) and Regional Forecast, 2026-2034

Van Market Size and Future Outlook

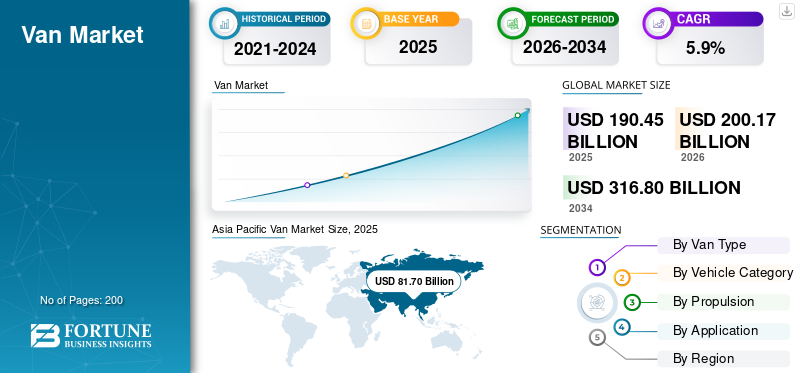

The global van market size was valued at USD 190.45 billion in 2025. The market is projected to grow from USD 200.17 billion in 2026 to USD 316.80 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period. Asia Pacific dominated the global van market with a market share of 42.9% in 2025.

The van market encompasses the production, sales, and utilization of light commercial vehicles specifically designed for transporting goods and passenger across urban and intercity routes. Vans are widely used for delivery service, logistics, mobility services, construction support, and public utilities. The market includes multiple configurations tailored to size, body style, propulsion, and application, catering to small businesses and large enterprises.

The market is expected to witness steady growth during the forecast period, supported by the rising demand for last-mile logistics, the expansion of organized retail, and the rapid growth of e-commerce platforms. Vans offer an optimal balance between payload capacity, maneuverability, and operating cost, making them a preferred choice for urban logistics and service-based industries. Increasing penetration of fleet-based operations has further strengthened their position as a key market segment within commercial mobility.

The industry is also evolving due to regulatory pressure on emissions and fuel efficiency. While the internal combustion engine remains dominant due to its cost advantages and established fuel networks, advancements in electric powertrains are gaining attention. EVs are increasingly adopted by automobile manufacturers and fleet operators aiming to reduce operating costs and comply with emission norms. However, the pace of adoption remains linked to the availability of charging infrastructure.

Technological integration such as telematics, route optimization, and safety systems is improving fleet efficiency and uptime. Investments by major van manufacturers such as Toyota Motor, Hyundai and Ford in modular platforms and scalable production further support long-term demand. Applications such as courier services, mobile workshops, healthcare logistics, and passenger shuttles are expanding, reinforcing the market’s relevance across regions. Overall, the global market is expected to grow steadily, driven by logistics modernization, urbanization, and fleet electrification initiatives.

Download Free sample to learn more about this report.

Van Market Key Takeaways

- 2025 Market Size: USD 190.45 Billion

- 2026 Market Size: USD 200.17 Billion

- 2034 Forecast Market Size: USD 316.80 Billion

- CAGR: 5.9% from 2026–2034

- Asia Pacific dominated the van market with a 42.9% share in 2025.

- Mid-size vans held the largest market share due to their balance of cargo capacity, fuel efficiency, and maneuverability.

- E-commerce and logistics accounted for the largest application segment share in 2025.

Asia Pacific

Asia Pacific generated USD 81.70 billion in revenue in 2025 and remained the largest regional market.

North America

North America is experiencing strong demand driven by e-commerce growth, fleet replacement, and van electrification initiatives.

Europe

Europe is expanding steadily due to stringent emission regulations and increasing adoption of electric vans.

U.S.

Demand remains strong for cargo vans supporting last-mile delivery and service industry operations.

Japan

Market growth is supported by commercial activity, fleet modernization, and rising adoption of electric vans.

Read More

VAN MARKET TRENDS

Shift Toward Connected and Fleet-Optimized Vans Emerges as a Market Trend

One of the prominent trends in the market is the integration of telematics, connectivity, and fleet management software. These technologies enable operators to monitor vehicle health, optimize routes, and reduce downtime. Manufacturers embedding digital solutions into vans enhance value for logistics companies, supporting efficiency-driven market growth across commercial transportation ecosystems.

- For instance, Mercedes-Benz Connectivity Services promotes Fleet Pilot as a ready-to-use fleet portal, featuring key figures that enable transparency, process improvement, and cost optimization without vehicle retrofit.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of E-Commerce and Urban Delivery Networks Accelerates Product Demand

The rapid expansion of e-commerce and same-day delivery service models is a major driver of global van market growth. Businesses increasingly rely on vans for efficient last-mile distribution due to their flexibility, lower operating costs, and urban compatibility. Growing parcel volumes and shorter delivery windows are pushing fleet operators to expand and modernize their van fleets.

- For instance, Amazon stated that it will deploy Rivian-designed electric delivery vans at scale as part of its Climate Pledge logistics push, reinforcing its fleet expansion to serve growing parcel demand.

MARKET RESTRAINTS

High Electrification Costs and Limited Charging Networks Restrain Product Adoption

The high upfront cost of EVs and inadequate charging infrastructure in many regions limit the rapid electrification of the market. Small fleet operators often face financial constraints, while inconsistent charging access increases operational risk. These factors slow the transition from internal combustion engine vans, particularly in developing economies, negatively impacting overall adoption rates.

- For instance, ACEA’s charging infrastructure analysis warns that the current pace and uneven distribution of public chargers across Europe are insufficient, creating a practical barrier to widespread electric commercial-van adoption.

MARKET OPPORTUNITIES

Fleet Electrification Initiatives Create Long-Term Growth Opportunities

Government incentives and corporate sustainability targets present strong opportunities for advancing electric vans. Fleet operators adopting EVs benefit from lower fuel and maintenance costs over time. As battery technology improves and charging infrastructure expands, manufacturers offering scalable electric van platforms can unlock significant growth across urban logistics and municipal services.

- For instance, the U.K. government lists vans among vehicles eligible for plug-in grants, helping narrow the price gap for zero-emission models and improving the business case for electric fleet procurement.

MARKET CHALLENGES

Supply Chain Disruptions Impacting Production Stability Emerges as a Market Challenge

Ongoing supply chain volatility, particularly in semiconductor and battery materials, presents a significant challenge for major market players. Production delays and cost inflation affect delivery timelines and profitability. Smaller manufacturers face higher vulnerability, while demand fluctuations complicate inventory planning, negatively influencing consistent market expansion.

- For instance, Reuters reported Nissan planned further production cuts at its Kyushu plant due to semiconductor supply issues, highlighting how chip disruptions can quickly constrain vehicle availability and deliveries.

Download Free sample to learn more about this report.

Segmentation Analysis

By Van Type

Mid-Size Vans Dominate Due to Balanced Cargo Capacity, Fuel Efficiency, and Urban Usability

On the basis of van type, the market is divided into compact vans, mid-size vans and full-size vans.

Mid-size vans dominate the market due to their optimal balance between cargo capacity, fuel efficiency, and maneuverability. They are widely used in urban logistics, service fleets, and passenger transport. Their adaptability across applications and lower operating costs compared to large vans support sustained demand growth globally.

- For instance, Ford’s official product page describes the Transit Custom as the “next generation of Europe’s best-selling one-tonne van,” supporting why mid-size vans remain central to fleets.

Compact vans segment is expected to grow at a CAGR of 7.3% over the forecast period.

By Vehicle Category

Rising Demand from Logistics, e-commerce, and Fleet Operations Drives Cargo Vans Segment Expansion

On the basis of vehicle category, the market is segmented into passenger vans and cargo vans.

Cargo vans dominate the market as the logistics, retail, and service sectors increasingly require efficient goods transport solutions. Their enclosed design improves cargo safety and versatility, making them essential for e-commerce and fleet operations across regions.

- For instance, DHL’s press release confirms large-scale deployment of Ford Pro e-vans for Post & Parcel Germany, showing cargo-focused vans are prioritized for high-frequency parcel distribution.

Passenger vans segment is expected to grow at a CAGR of 7.5% over the forecast period.

By Propulsion

ICE Vans Remain Dominant Due to Cost and Infrastructure Advantages

To know how our report can help streamline your business, Speak to Analyst

On the basis of propulsion, the market is segmented into ICE and electric.

The ICE segment dominates due to lower upfront costs, widespread fueling networks, and proven reliability. Despite growth in EVs, ICE vans remain preferred in regions with limited charging infrastructure, ensuring continued dominance during the forecast period.

- For instance, a U.K. government study on electric van adoption highlights barriers to uptake and charging behaviors, which support why fleets continue to rely heavily on conventional powertrains in many routes.

Electric segment is expected to grow at a CAGR of 7.8% over the forecast period.

By Application

E-Commerce and Logistics Drive the Highest Van Utilization

On the basis of application, the market is segmented into e-commerce and logistics, construction & infrastructure, passenger transport & shuttle services, healthcare & emergency services, mobile workshops & service vans and municipal services.

E-commerce and logistics segment dominate the market with the largest van market share, due to growing parcel volumes and urban delivery needs. Vans enable efficient route coverage, flexible loading, and quick turnaround times, making them indispensable for modern supply chains.

- For instance, DHL announced the acquisition of thousands of additional electric delivery vans for last-mile operations, directly reflecting how parcel logistics growth drives fleet investment and dominates van utilization.

E-commerce & logistics segment is expected to grow at a CAGR of 6.7% over the forecast period.

Van Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Van Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to rapid urbanization, expanding retail networks, and strong manufacturing ecosystems. Countries such as China, India, and Japan benefit from high commercial activity and increasing demand for small business logistics. Government support for local production and fleet modernization further strengthens growth. Increasing adoption of electric vans in urban centers also contributes to long-term expansion.

- For instance, China’s Ministry of Industry and Information Technology highlights light commercial vehicles as a priority segment, supported by domestic manufacturing scale and strong logistics demand across urban and regional markets.

North America

The North America market is driven by e-commerce expansion, fleet replacement cycles, and electrification initiatives. In the U.S. market, demand is strong for cargo vans supporting last-mile delivery and service industries. Federal incentives and private investment support the gradual adoption of electric commercial vehicles.

Europe

Europe’s market growth is supported by strict emission regulations and strong fleet electrification policies. Manufacturers focus on electric and low-emission vans to meet sustainability targets, particularly in urban logistics and municipal operations.

The rest of the world market continues to grow steadily due to infrastructure development and rising commercial activity. Latin America, the Middle East, and Africa are experiencing an increasing demand for cost-effective ICE vans in the construction, logistics, and public sectors.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Electrification, Platform Sharing, and Fleet-Focused Partnerships Define Competition in the Market

The competitive landscape of the global van market is characterized by the presence of established major players with strong manufacturing capabilities, extensive dealer networks, and diversified product portfolios. Leading automobile manufacturers compete on vehicle reliability, total cost of ownership, fuel efficiency, and aftersales support. Product customization and fleet-specific solutions have become essential strategies to retain commercial customers.

Key van manufacturer strategies include portfolio expansion across propulsion types, particularly hybrid and electric vehicles, to address regulatory and fleet sustainability goals. Several key players are investing in platform standardization to reduce development costs while enabling flexible body configurations. Partnerships with logistics companies, technology firms, and charging solution providers are increasingly used to strengthen ecosystem capabilities.

Geographic expansion remains a critical growth lever. Companies are enhancing their production capacity and local assembly to efficiently address regional demand, particularly in the Asia Pacific and North America. Digital sales channels, fleet leasing programs, and service-based contracts are also gaining traction as differentiation tools within the competitive landscape.

Mergers, collaborations, and joint ventures enable manufacturers to accelerate innovation and expand into new markets. Brand reputation, supply chain resilience, and compliance with safety regulations continue to influence competitive positioning. As market trends evolve, manufacturers focusing on operational efficiency and electrification are positioned to gain share.

- For instance, in September 2024, Ford Motor Company expanded E-Transit production in Europe to meet fleet electrification demand, strengthening its leadership in commercial EV vans.

LIST OF KEY VAN COMPANIES PROFILED

- Ford Motor Company (U.S.)

- Nissan Motor (Japan)

- Toyota Motor Corporation (Japan)

- Volkswagen AG (Germany)

- Mercedes-Benz Group (Germany)

- Stellantis NV (Netherlands)

- Renault Group (France)

- Hyundai Motor Company (South Korea)

- Kia Corporation (South Korea)

- Isuzu Motors (Japan)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Iveco launched the eJolly and eSuperJolly electric vans, positioned between light and medium segments, expanding its zero-emission lineup for urban and regional delivery operations.

- April 2025: Renault confirmed its Flexis joint venture plans to manufacture modular electric vans in Europe, focusing on last-mile logistics and scalable production for commercial fleet customers.

- April 2025: Stellantis announced updates to its large van range, introducing faster onboard charging and efficiency upgrades across Fiat Ducato, Peugeot Boxer, and Citroën Relay models.

- February 2025: Kia unveiled the PV5 electric van on its PBV platform, targeting cargo and passenger applications and signaling the brand’s strategic expansion into global electric commercial vehicle markets.

- September 2024: The 2025 Commercial Vehicle Show showcased several next-generation electric vans from Kia, Renault, Flexis, and Isuzu, highlighting industry focus on EV innovation and urban delivery fleet needs.

REPORT COVERAGE

The global van market analysis provides an in-depth study of market size and forecast for all the market segments included in the report. It includes details on the market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.9% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Van Type, Vehicle Category, Propulsion, Application and Region |

|

By Van Type |

· Compact Vans · Mid-size Vans · Full-size Vans |

|

By Vehicle Category |

· Passenger Vans · Cargo Vans |

|

By Propulsion |

· ICE · Electric |

|

By Application |

· E-commerce and Logistics · Construction & Infrastructure · Passenger Transport & Shuttle Services · Healthcare & Emergency Services · Mobile Workshops & Service Vans · Municipal Services |

|

By Geography |

· North America (By Van Type, Vehicle Category, Propulsion, Application and Country) o U.S. o Canada o Mexico · Europe (By Van Type, Vehicle Category, Propulsion, Application and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Van Type, Vehicle Category, Propulsion, Application and Country) o China o India o Japan o South Korea o Rest of Asia Pacific · Rest of the World (By Van Type, Vehicle Category, Propulsion, Application and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 190.45 billion in 2025 and is projected to reach USD 316.80 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 81.70 Billion.

The market is expected to exhibit a CAGR of 5.9% during the forecast period of 2026-2034.

ICE segment is leading the market by propulsion.

Expansion of e-commerce and urban delivery networks are the key factors driving the market.

Toyota Motor Corporation, Ford Motors, Hyundai Motor Company and Mercedes-Benz are some of the top players in the market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us